Liquid Crystal Polymers (LCP) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

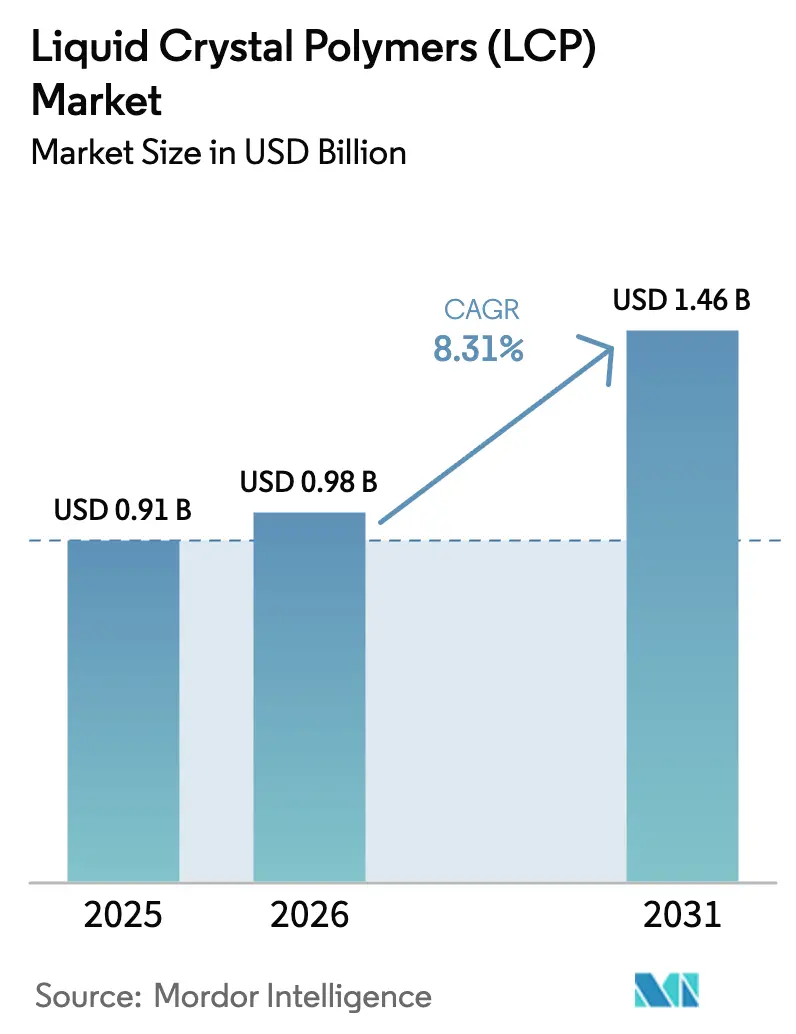

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

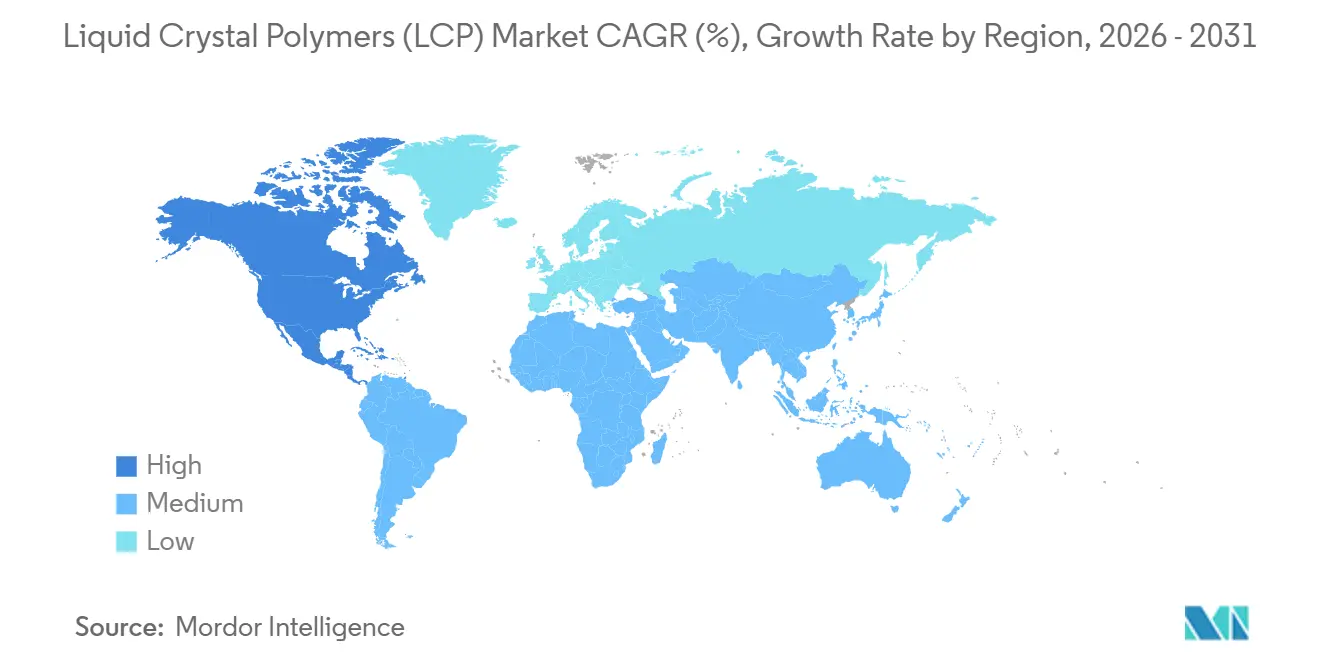

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Crystal Polymers (LCP) Market Analysis by Mordor Intelligence

The Liquid Crystal Polymers Market size was valued at USD 0.91 billion in 2025 and is estimated to grow from USD 0.98 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 8.31% during the forecast period (2026-2031). The upward trajectory reflects three concurrent technology shifts that intensify demand: shrinking radio-frequency (RF) components for 5G handsets, rising thermal loads in 800-volt electric-vehicle (EV) power electronics, and stricter biocompatibility needs for implantable medical sensors. Thermotropic grades dominate because they withstand reflow-solder profiles above 280 °C while fitting standard injection-molding lines, a combination that keeps tooling costs low for connector suppliers. In parallel, lyotropic grades are advancing in aerospace composites and ballistic fibers where solution processing delivers extreme molecular orientation and tensile strength. Regionally, the Liquid crystal polymers market remains anchored in Asia-Pacific, yet North America is accelerating as EV lightweighting and aerospace programs favor LCP in place of metals. Producers are moving beyond capacity races toward differentiated low-dielectric and bio-based chemistries, signaling a competitive turn that rewards formulation know-how more than sheer scale.

Key Report Takeaways

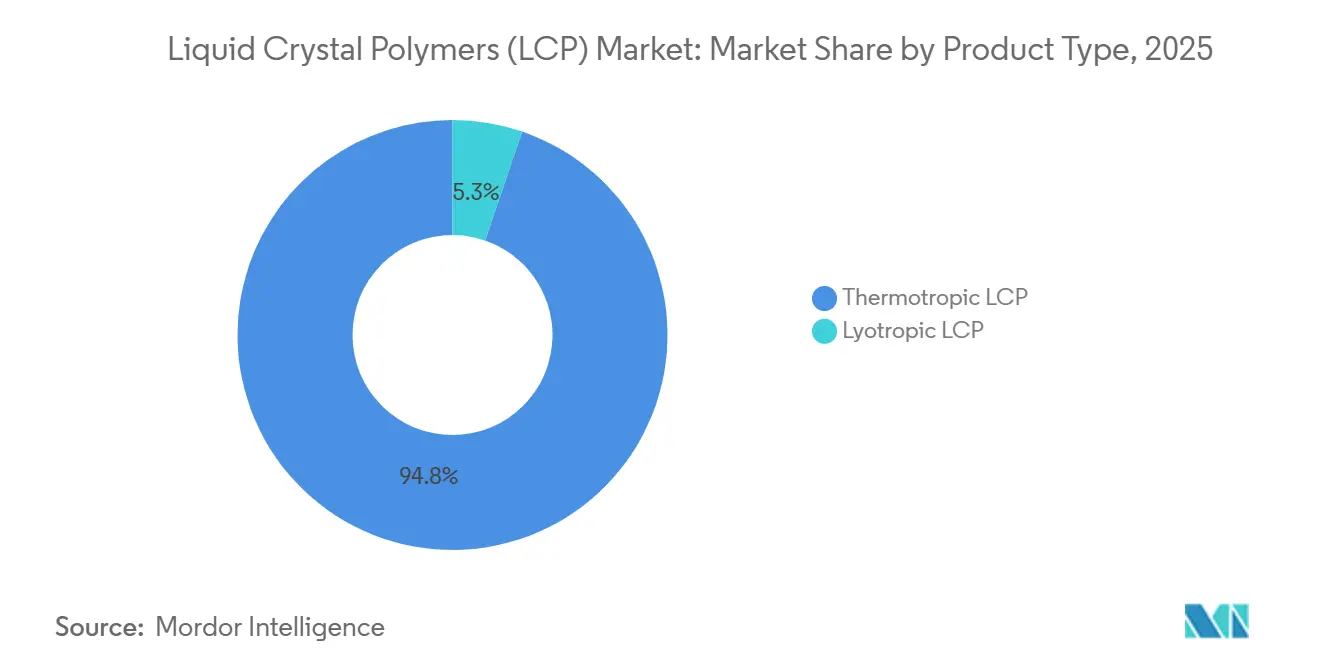

- By product type, thermotropic LCP held 94.75% of the liquid crystal polymers market share in 2025, while lyotropic LCP is expanding at a 9.27% CAGR through 2031.

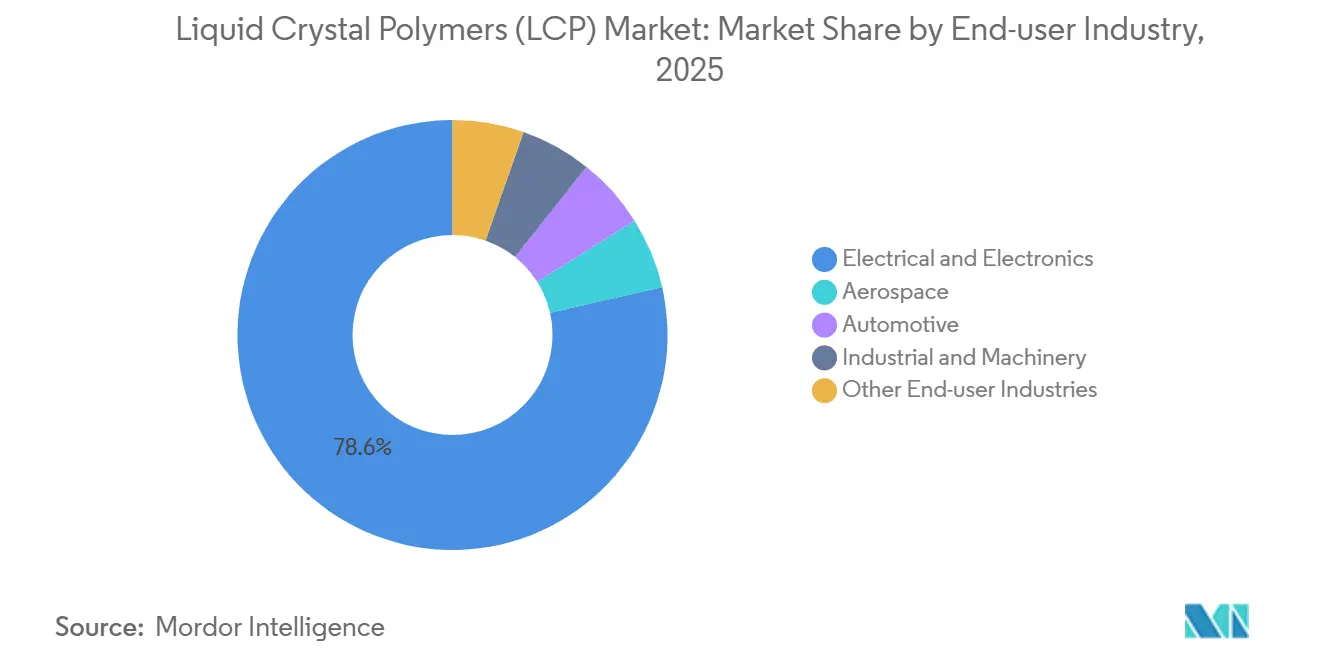

- By end-user industry, electrical and electronics captured 78.56% of the liquid crystal polymers market share in 2025, while aerospace is advancing at a 9.20% CAGR to 2031.

- By geography, Asia-Pacific led with 69.11% share of the Liquid crystal polymers market in 2025, while North America is forecast to rise at a 9.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Crystal Polymers (LCP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturisation of SMT Components and 5G RF Modules | +2.1% | Asia-Pacific core (China, Japan, South Korea), spill-over to North America | Short term (≤ 2 years) |

| Lightweight Substitution for Metals in EV Power Electronics | +1.8% | North America and Europe (automotive hubs), emerging in China | Medium term (2-4 years) |

| Surge in Demand for High-frequency Flexible Circuits | +1.9% | Global, with concentration in Asia-Pacific electronics manufacturing | Short term (≤ 2 years) |

| LCP Films for Wearable/Implantable Medical Sensors | +1.2% | North America and Europe (regulatory approval pathways), Japan | Medium term (2-4 years) |

| Adoption of LCP Membranes in PEM Fuel-cells and Green Hydrogen Electrolysers | +0.7% | Europe (hydrogen strategy), Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of SMT Components and 5G RF Modules

The shift to standalone 5G networks and millimeter-wave bands forces a wholesale rethink of RF front-end packaging, and dielectric constants of 2.9-3.5 combined with dissipation factors below 0.002 make LCP films the default substrate at 28 GHz and higher. Polyplastics broadened its LAPEROS LH and TF series in December 2025 to supply antenna-in-package modules that integrate multiple RF chains inside footprints under 10 mm. China’s Ministry of Industry and Information Technology confirmed the installation of 2.3 million 5G base stations by late 2025, a build-out that scales interconnect requirements for massive-MIMO arrays where conventional polyimide laminates introduce prohibitive signal loss[1]Ministry of Industry and Information Technology, “5G Infrastructure Progress Report 2025,” miit.gov.cn . Surface-mount devices now ship with 0.3 mm pitches, demanding plastic housings that stay within ±0.02 mm after 260 °C reflow. Because Liquid crystal polymers market formulations retain dimensional stability at those extremes, designers are culling legacy resins from spec sheets, cementing LCP as the material of record for next-generation RF modules.

Lightweight Substitution for Metals in EV Power Electronics

OEMs are moving to 800-V battery systems that push inverter housing temperatures beyond 200 °C. LCP maintains more than 80% tensile strength at 240 °C, enabling direct metal replacement in non-structural enclosures while slashing part mass by up to 50% and meeting UL 94 V-0 without halogens. Daicel’s FY 2026 interim report cited double-digit LCP shipment growth for server power modules, mirroring EV inverter heat-flux trends. Inflation Reduction Act credits that reward weight savings enhance the business case, and once an LCP grade clears the 24-36-month automotive qualification cycle, engrained tooling makes displacement unlikely. The Liquid crystal polymers market therefore benefits from regulatory pull and engineering push, with volume gains climbing as silicon-carbide switching surpasses 100 kHz.

Surge in Demand for High-frequency Flexible Circuits

Flexible copper-clad laminates using LCP are edging out polyimide in circuits working above 10 GHz because polyimide’s dissipation factor of 0.008-0.012 degrades signal integrity over 50 mm traces. Murata, Rogers, and UBE together controlled more than half of 2024 laminate revenue, underscoring high entry barriers to produce 50 µm films with copper peel strengths above 0.7 kg/cm. Foldable and rollable displays amplify usage; LCP substrates endure more than 200,000 bends at a 1 mm radius, four times polyimide endurance, a ratio that outweighs the 30-40% raw-material cost premium. As yields on foldable panels rise, tier-one smartphone brands lock-in LCP to avoid USD 150 warranty hits per failed unit, feeding sustained momentum for the Liquid crystal polymers market.

LCP Films for Wearable/implantable Medical Sensors

ISO 10993 biocompatibility studies show negligible inflammatory response after 12 months in vivo, validating LCP for long-term implants such as neural probes and continuous glucose monitors. Moisture uptake under 0.02% thwarts dielectric breakdown in miniaturized circuits immersed in body fluids. The U.S. FDA’s breakthrough-device pathway has shortened review cycles to under 24 months, expediting commercialization for med-tech start-ups. Wearable patches gain from 25 µm LCP films that flex with skin while keeping electrical pathways intact through perspiration and twisting. Japan’s aging population is accelerating adoption of continuous monitoring solutions, giving med-device makers another vector to expand the Liquid crystal polymers market beyond its electronics core.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Premium vs. High-temperature Nylons and PPS | -1.4% | Global, most acute in cost-sensitive automotive and industrial segments | Short term (≤ 2 years) |

| Weld-line Weakness and Anisotropic Shrinkage in Complex Molds | -0.9% | Global manufacturing, particularly in multi-cavity tooling applications | Medium term (2-4 years) |

| Concentrated Upstream Supply of Specialty Diacids/diols | -0.6% | Global, with supply concentration in Japan and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Premium vs. High-temperature Nylons and PPS

Liquid crystal polymers market grades trade at USD 16-18 per pound, around double high-temperature nylons such as PA6T. Celanese raised Vectra and Zenite list prices by up to USD 0.50/kg in March 2025 despite stable oil benchmarks, a move that underscores structural cost headwinds rooted in batch polymerization and specialty monomer sourcing. The gap steers cost-sensitive auto connectors toward glass-fiber PPS, whose global capacity tops 150 kt per year. Efforts to trim LCP cost run into chemistry barriers; stoichiometric precision and multi-hour reaction cycles constrain yield, limiting room for commodity-style scaling. Until bio-based monomers reach parity, high upfront resin prices will continue to moderate the Liquid crystal polymers market penetration in under-hood applications.

Weld-line Weakness and Anisotropic Shrinkage in Complex Molds

LCP exhibits tensile anisotropy up to 3:1 between flow and transverse directions, complicating designs that experience multi-axial loads. Weld lines in multi-gate tools retain only 40-60% of nominal strength, forcing heavier ribs or gate re-positioning, which undermines part cost targets. Shrinkage variance from 0.1% (flow) to 0.6% (cross-flow) triggers warpage in thin substrates, hampering first-pass yields required in high-volume electronics lines. Simulations help, yet liquid-crystalline rheology remains difficult to model, so molders face 6-12 months of learning curves when re-tooling from amorphous resins. These hurdles slow adoption tempo in new verticals, tempering near-term Liquid crystal polymers market uptake.

Segment Analysis

By Product Type: Thermotropic Dominance Anchors Volume Growth

Thermotropic LCP accounted for 94.75% of 2025 shipments, underscoring their entrenched position in fine-pitch connectors and antenna substrates. At USD 16-18 per pound, they remain costly, yet high-yield processing on conventional molding presses offsets some of that premium for mass electronics producers. Growth through 2031 is tied to millimeter-wave devices and data-center upgrades that require mold-in antenna structures with dimensional drift below 0.03 mm across reflow cycles.

Lyotropic LCP will grow at 9.27% through 2031, the quickest among all product groups, as fiber makers exploit solution processing to spin high-tenacity yarns for protective apparel and aerospace laminates. Pilot lines at Kuraray and Toray overcome solvent recovery challenges by deploying closed-loop systems that recapture more than 90% dimethylacetamide, trimming environmental footprints. If Sumitomo’s bio-aromatic building blocks reach commercial scale by 2027, lyotropic producers may secure feedstock optionality that could narrow cost gaps over the long term.

By End-user Industry: Electronics Dominance Masks Aerospace Velocity

Electrical and electronics absorbed 78.56% of total market share in 2025, reflecting smartphones, base-stations, servers, and consumer devices that all chase miniaturization and thermal resilience. Polyplastics’ Kaohsiung plant was expressly justified by AI server connector demand that must transmit 800 Gb/s without packet loss, a task that hinges on dielectric loss tangents under 0.002.

Aerospace advances at 9.20% CAGR through 2031, the fastest among user groups. Thermoplastic composites trimmed cabin interior assembly time by 30% versus thermoset panels on recent wide-body programs, and a 10% mass cut in galley monuments translates to USD 50,000 annual fuel savings per aircraft. The high margins offset small volumes, prompting Sumitomo and Toray to introduce flame-retardant, low-smoke LCP formulations that target FAA FAR 25.853 compliance. Automotive and industrial sectors trail because PPS and high-temperature nylons cover many requirements at half the polymer price, but EV inverter heat flux and chemical pump corrosion challenges will keep LCP on design shortlists.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific controlled 69.11% of 2025 sales, underpinned by a value chain that runs from monomer synthesis to final device assembly inside the Pearl and Yangtze delta clusters. China alone imported more than 40,000 tonnes of LCP pellets in 2025 to feed connector and flexible-circuit fabs, a figure confirmed by General Administration of Customs data[2]General Administration of Customs of the People’s Republic of China, “Plastics Import Statistics 2025,” customs.gov.cn . Japan is supplying high-purity grades for medical and automotive clients that prize domestic quality oversight. South Korea remains a net importer despite its strong electronics export profile because its sole domestic line is under 1,000 tonnes. Government subsidies, proximity to contract assemblers, and real-time technical service jointly reinforce regional dominance, ensuring that the Liquid crystal polymers market will remain heavily weighted to Asia, at least through the forecast window.

North America is the fastest climber, running at a 9.12% CAGR out to 2031. Celanese’s decision to build its newest plant in Nanjing rather than Texas highlights Asia’s gravitational pull, but the U.S. retains a technological edge in aerospace and medical devices, both high-margin niches that require ITAR-compliant supply chains. The CHIPS and Science Act provides tax credits for domestic advanced-material production, and several resin suppliers are evaluating debottleneck projects near existing acetyl complexes.

Europe grows more slowly, hamstrung by automakers squeezing costs amid competition from low-priced Chinese EVs. However, REACH compliance and the European Green Deal favour halogen-free and bio-based resins, allowing Sumitomo’s biomass LCP route to command a green premium. South America and the Middle-East and Africa together account for low demand, with most shipments arriving as finished connectors or flexible laminates assembled offshore. Telecommunications build-outs in Brazil, Nigeria, and Saudi Arabia will lift consumption, but not enough to alter the regional ranking in the Liquid crystal polymers market.

Competitive Landscape

The top five suppliers—Polyplastics, Celanese, and Sumitomo, Kuraray, and Toray—hold close to 77% of worldwide capacity, conferring moderate pricing power without absolute dominance. Polyplastics’ new Kaohsiung train pushed its share, yet Celanese’s 20,000-tonne Nanjing addition narrows the gap. Sumitomo is carving a technological niche with bio-derived monomers that lower carbon intensity by up to 40%; if scale economics improve, this route could disrupt the cost hierarchy. Chinese challengers Kingfa and WOTE benefit from preferential financing and feedstock incentives, undercutting imports by up to 15% on landed cost.

Product differentiation pivots on dielectric loss, flow length, and low-warpage performance. Celanese’s Vectra ultra-low-dk grades post dissipation factors of 0.0015 at 28 GHz, meeting IEEE 802.11be front-haul expectations. Polyplastics melds its own polymer backbone with compounding know-how to offer grades that retain tensile modulus after 200,000 bend cycles at 1 mm radius, targeting foldable devices. Vertical integration confers resilience: Celanese pulls acetic acid from its acetyl chain, while Daicel synthesizes specialty cellulose derivatives that could underpin bio-feedstock ventures.

Standards bodies indirectly shape rivalry. IEC TC 46 electrical tests, UL 94 flammability, and FDA ISO 10993 biocompatibility protocols funnel end-users toward high-performance resins. Suppliers that secure early listings on these standards lock in multi-year supply contracts, creating switching costs. Collaboration with OEMs on application-specific grades cements positions: for instance, Sumitomo co-developed low-outgassing resins for satellite optics with JAXA in 2025, an effort that requires five-year flight-qualification, effectively barricading the niche. The Liquid crystal polymers market, therefore, balances scale, chemistry innovation, and regulatory credentialing as primary levers of competitive advantage.

Liquid Crystal Polymers (LCP) Industry Leaders

Celanese Corporation

Sumitomo Chemical Co., Ltd.

KURARAY CO., LTD.

Polyplastics Co., Ltd.

TORAY INDUSTRIES, INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Polyplastics Co., Ltd. expanded its LAPEROS liquid crystal polymer (LCP) product line with the introduction of the LH and TF series. The LH series offered a balanced combination of flowability, mechanical properties, and heat resistance, while the TF series is designed for enhanced fluidity, enabling improved molding of complex geometries in smartphones and precision electronic components.

- June 2025: Sumitomo Chemical Co., Ltd. established mass production technology for liquid crystal polymer (LCP) using a monomer sourced from biomass materials. The company aimed to secure customer certification by the end of fiscal 2026 and to begin supplying the product from 2027.

Global Liquid Crystal Polymers (LCP) Market Report Scope

Liquid crystal polymers (LCP) are a type of aromatic thermoplastic polymer, typically derived from polyesters, that form highly ordered, rod-like structures even in their molten state. They are known for their high strength, outstanding dimensional stability, superior heat resistance, and excellent chemical resistance. These properties make them suitable for manufacturing thin-walled, small, and complex components used in electronics (such as connectors and sensors) and medical devices.

The Liquid crystal polymers (LCP) market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into thermotropic LCP and lyotropic LCP. By end-user industry, the market is segmented into electrical and electronics, aerospace, automotive, industrial and machinery, and other end-user industries. The report also covers the market size and forecasts for Liquid crystal polymers (LCP) in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Thermotropic LCP |

| Lyotropic LCP |

| Electrical and Electronics |

| Aerospace |

| Automotive |

| Industrial and Machinery |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Product Type | Thermotropic LCP | |

| Lyotropic LCP | ||

| By End-user Industry | Electrical and Electronics | |

| Aerospace | ||

| Automotive | ||

| Industrial and Machinery | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Market Definition

- End-user Industry - Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the liquid crystal polymer market.

- Resin - Under the scope of the study, virgin liquid crystal polymer resin in the primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms