Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.42 Billion |

| Market Size (2031) | USD 15.28 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

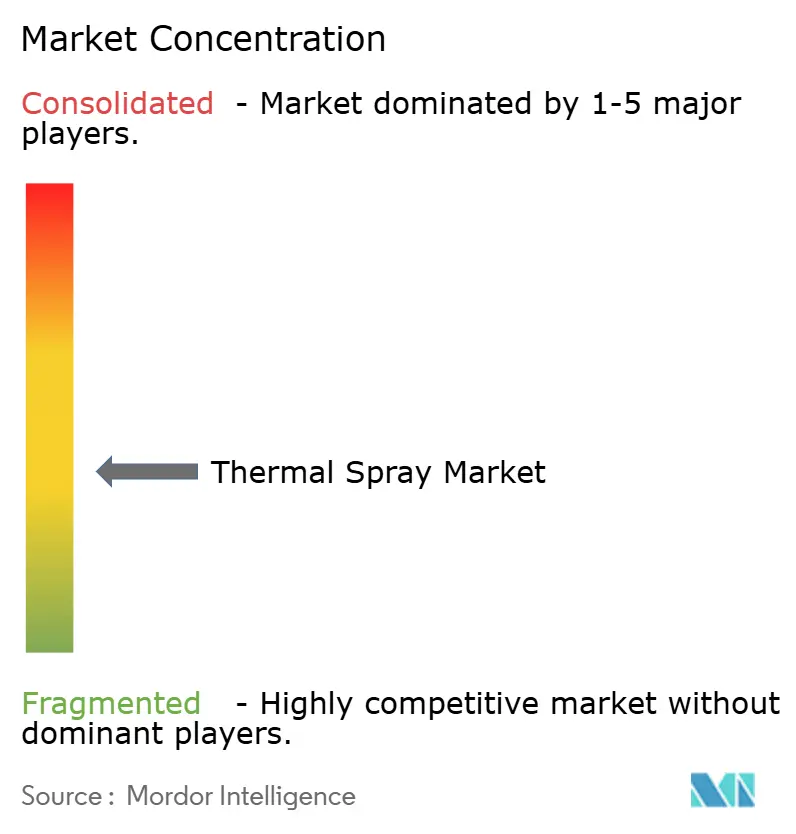

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermal Spray Market Analysis by Mordor Intelligence

The Thermal Spray Market size is expected to increase from USD 11.92 billion in 2025 to USD 12.42 billion in 2026 and reach USD 15.28 billion by 2031, growing at a CAGR of 4.22% over 2026-2031. Growth is underpinned by regulatory pressure to replace carcinogenic hexavalent chromium plating, surging turbine-engine demand for yttria-stabilized zirconia (YSZ) thermal-barrier coatings, and accelerating electronics adoption for power-module heat-sink metallization. Capital spending is shifting from electroplating lines to high-velocity oxygen-fuel (HVOF) and high-velocity air-fuel (HVAF) spray booths as aviation and hydraulic suppliers align with UK and EU REACH deadlines. Equipment vendors are benefiting from job-shop investments in portable cold-spray cells that support in-situ maintenance, repair, and overhaul (MRO) on aircraft, turbines, and offshore assets. Meanwhile, feedstock diversification is gathering pace after China’s 2024 export restrictions on tungsten and rare-earth processing technology, prompting Western OEMs to co-locate coating capacity near Asian supply chains.

Key Report Takeaways

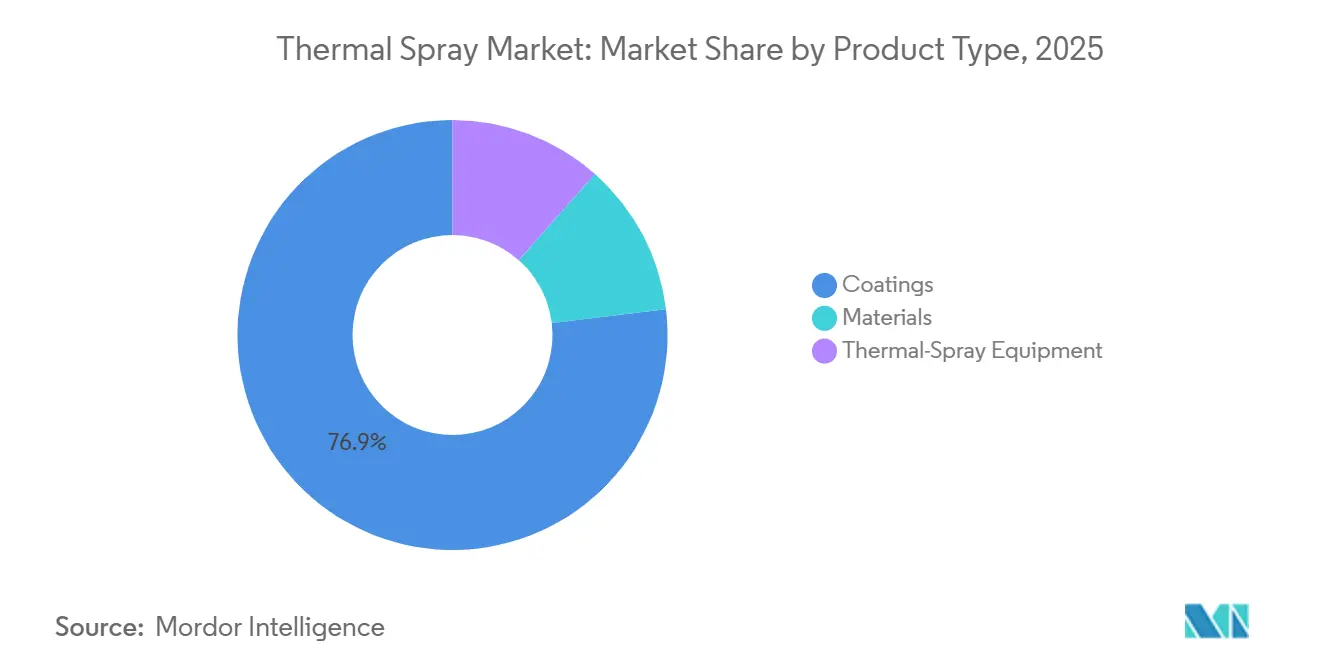

- By product type, coatings dominated with 76.92% of the thermal spray market share in 2025, while thermal-spray equipment is forecast to post the fastest 6.16% CAGR through 2031.

- By coating technology, combustion processes held 45.44% of the thermal spray market size in 2025, whereas electric energy methods are expected to expand at a 4.62% CAGR through 2031.

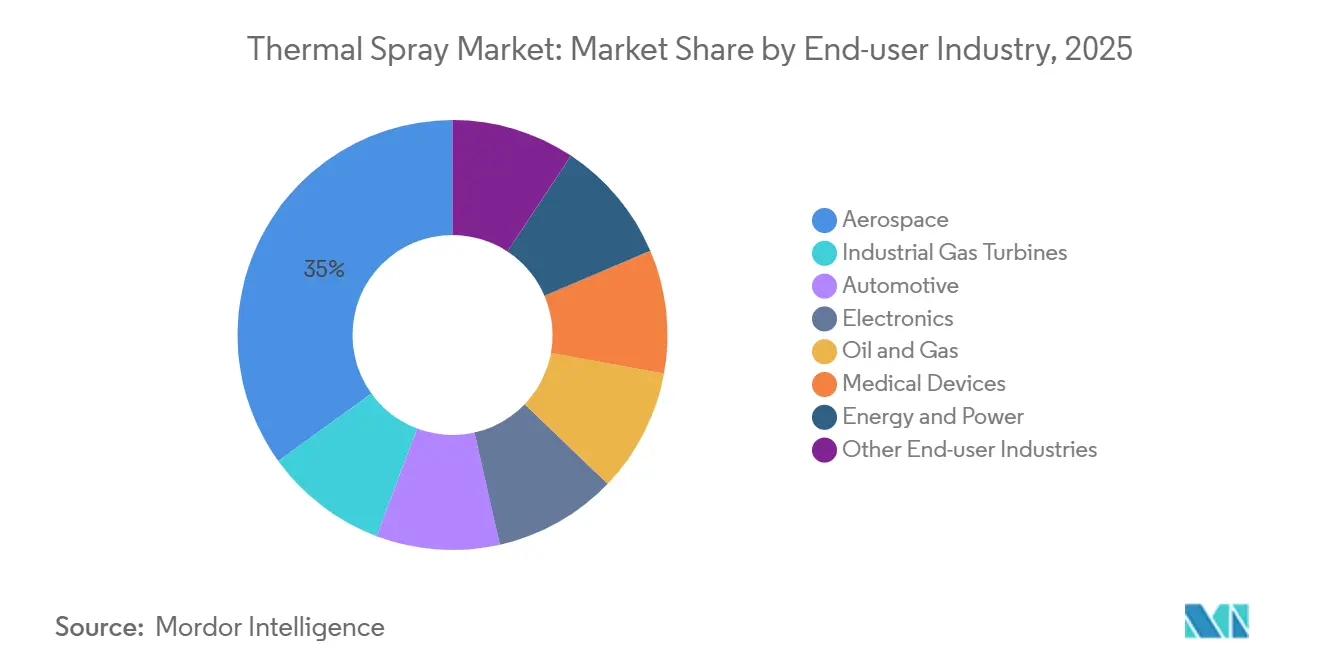

- By end-user industry, aerospace led with 34.96% revenue share in 2025; electronics is projected to register the highest 6.15% CAGR to 2031.

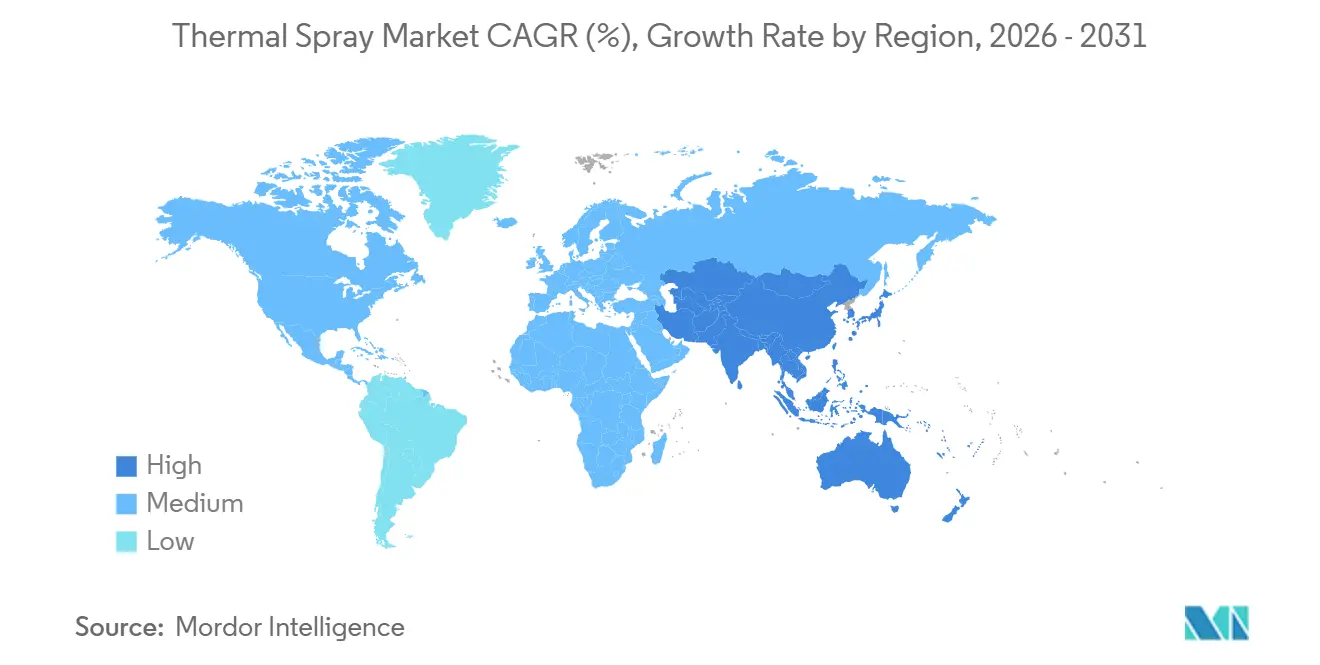

- By geography, Asia-Pacific accounted for 34.35% of global sales in 2025 and is advancing at the quickest 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermal Spray Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hard-chrome replacement across hydraulics | +0.9% | North America, Europe (UK, Germany, France) | Medium term (2-4 years) |

| Light-weight, high-temp alloys in narrow-body jet engines | +1.1% | Global, concentrated in North America, Europe, Asia-Pacific aerospace hubs | Long term (≥ 4 years) |

| Hydrogen ICE and e-powertrain cylinder bore wear solutions | +0.7% | Europe, Asia-Pacific (China, Japan, South Korea) | Medium term (2-4 years) |

| High-entropy alloy (HEA) coatings for geothermal and space probes | +0.4% | North America (NASA, DoE geothermal), Europe (ESA), niche Asia-Pacific | Long term (≥ 4 years) |

| Laser-assisted cold-spray for in-situ MRO | +0.8% | Global, early adoption in North America aerospace, spreading to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hard-Chrome Replacement Across Hydraulics

In 2024, the UK denied authorizations for chromium trioxide, prompting hydraulic-cylinder manufacturers to seek alternatives. They turned to HVOF and HVAF coatings, achieving wear resistance akin to hard chrome while sidestepping carcinogenic waste. In a notable shift, Airbus and Boeing, in 2025, revised their material specifications. They now permit deposits of up to 300 µm, either tungsten-carbide-cobalt or chromium-carbide-nickel-chromium, on landing-gear shafts. This change has ignited a surge in demand for retrofitting automated masking and sub-5 µm grinding systems. Meanwhile, North American OEMs have discovered that investing in spray cells yields a return within 18-24 months by sidestepping wastewater fees. Furthermore, the ISO 14917 certification has emerged as a pivotal procurement benchmark, leading to a wave of consolidation among coating job shops that can afford third-party audits.

Light-Weight, High-Temp Alloys in Narrow-Body Jet Engines

Next-gen turbofans, boasting pressure ratios exceeding 50:1, are pushing turbine-inlet temperatures beyond 1,500 °C. This surge in temperature necessitates the use of multilayer YSZ thermal-barrier coatings, complemented by rare-earth-doped bond coats, to effectively resist CMAS attacks[1]Michael Mauer, “Process Diagnostics and Control in Thermal Spraying,” Journal of Thermal Spray Technology, springer.com. Utilizing suspension plasma spray (SPS), manufacturers achieve columnar YSZ microstructures that boast lower thermal conductivity, resulting in an extended time-on-wing. Industry giants are turning to solution-precursor plasma spray (SPPS) for applying environmental-barrier coatings on their ceramic-matrix-composite shrouds. In a strategic move to mitigate rare-earth risks, engine OEMs are now stockpiling scandia- or dysprosia-doped feedstock. This decision, while safeguarding against supply chain vulnerabilities, has led to an inflation of working capital requirements, particularly challenging for smaller coaters.

Hydrogen ICE and E-Powertrain Cylinder Bore Wear Solutions

Hydrogen embrittlement causes bore wear in heavy-duty hydrogen engines. However, iron-based thermal-spray coatings help mitigate this issue by trapping hydrogen in controlled-porosity micro-voids[2]Daroonparvar M. et al., “Hydrogen Embrittlement Resistant Coatings: A Review,” coatings, mdpi.com. Daimler Truck and Volvo Group are in the process of qualifying arc-sprayed FeCrAlY coatings, targeting long-term durability. In response to Euro 7 brake-particle regulations, thermal-spray rotors have been developed that can reduce dust emissions significantly. Additionally, wire-arc systems, which deposit aluminum-bronze or molybdenum at a high rate, have managed to lower per-part costs sufficiently to rival traditional machining methods.

High-Entropy Alloy Coatings for Geothermal and Space Probes

High-entropy alloys from the CoCrFeNi family endure temperatures greater than 800 °C and resist corrosive brine. This resilience has led to geothermal tests, revealing that these alloys boast a significantly longer lifespan than Inconel 625. Recent laser-assisted cold-spray trials achieved near-dense CoCrFeNiTi repairs on rocket nozzles, showcasing minimal oxidation. However, with gas-atomized HEA powders remaining expensive, adoption faces hurdles. The challenge persists until additive suppliers can upscale directed-energy-deposition wire routes, effectively combining near-net printing with thermal-spray finishing.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-operator scarcity in Asian and LATAM job-shops | -0.6% | Asia-Pacific (Southeast Asia, India), South America (Brazil, Argentina, Colombia) | Short term (≤ 2 years) |

| Volatile WC-Co and rare-earth oxide supply chain | -0.8% | Global, acute in North America and Europe dependent on Chinese exports | Medium term (2-4 years) |

| Carbon-footprint pressure vs gas-fuelled spray booths | -0.5% | Europe (EU CSRD compliance), North America (voluntary ESG reporting) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Operator Scarcity in Asian and LATAM Job-Shops

Mastering thermal-spray proficiency typically requires several months. However, as vocational pipelines struggle to keep pace, many shops in Southeast Asia and Latin America face significant vacancies. Recently, fewer new Level II inspectors have received global certification compared to earlier years. Productivity continues to be affected as operators migrate to higher-wage markets in the GCC, and unreliable power grids destabilize plasma torches. Most shops, earning modest revenues, find it challenging to invest in robotic automation, especially with vision-guided cell costs remaining high.

Volatile WC-Co and Rare-Earth Oxide Supply Chain

In early 2025, a significant increase in tungsten-carbide prices followed China's 2024 prohibition on tungsten-processing technology. This move tightened profit margins for coaters in North America and Europe. While domestic powder plants, backed by the U.S. defense sector, are on the horizon, they are not expected to achieve full scale until later this decade. In 2025, fluctuations in spot prices for yttria and dysprosia added complexity to fixed-price contracts in the aerospace sector. Meanwhile, smaller job shops, lacking the capacity to secure multi-ton supply agreements, are increasingly outsourcing work to integrated competitors equipped with captive atomizers.

Segment Analysis

By Product Type: Equipment Growth Outpaces Coatings

Equipment revenue, forecast to climb at a 6.16% CAGR through 2031, is poised to surpass the broader thermal spray market. The industry's pivot towards in-situ MRO and stringent aerospace-grade quality checks has catalyzed a transition from traditional flame-spray rigs to advanced robotic HVOF and portable cold-spray platforms. Capital investments are further amplified by dust-collection retrofits and gravimetric feeders boasting precise powder-flow tolerance. Coatings, commanding a 76.92% share in 2025, anchor the recurring consumables demand, solidifying the thermal spray market's stature for service providers. The product lineup is rounded out with materials like ceramic powders featuring low oxygen content.

Equipment manufacturers have integrated predictive-maintenance software with subscription-based spare-parts packages, fostering annuity streams and curtailing unplanned downtimes. While portable spray guns, weighing less than 5 kilograms, cater to field technicians, challenges like nozzle clogging and inconsistent powder-feed have posed adoption barriers. Additionally, the thermal spray sector has witnessed a surge in orders for acoustic enclosures, essential for adhering to shop-floor noise limits and evolving occupational safety regulations.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Thermal Spray Coatings and Finishes: Electric Methods Gain Share

Combustion methods held 45.44% of 2025 revenue, yet plasma and arc spray are forecast to capture incremental share as manufacturers demand denser, hydrogen-embrittlement-free deposits. Atmospheric plasma spray has taken the lead in producing YSZ thermal barriers, achieving impressive thermal conductivities as low as 0.8 W/m·K. Electric energy forms a fast-growing niche that engine OEMs have qualified for ceramic composite shrouds, anchoring a 4.62% CAGR through 2031.

Arc spray, with its high throughput, remains a vital player in protecting bridges and wind towers from corrosion. Cold spray, especially with its laser-assisted variants, has made significant strides in aluminum airframe repairs, underscoring the thermal spray market's potential to broaden its horizons through related maintenance solutions. While detonation-gun equipment is costly and operates in batch mode, it continues to hold its ground in ultra-hard WC-Co coatings for drill bits, achieving high velocities. With the expansion of electric methods, the market share of plasma and arc systems in the thermal spray industry is expected to approach parity with combustion methods by 2031.

By End-User Industry: Electronics Surge Contrasts with Aerospace Maturity

Aerospace contributed 34.96% of 2025 revenue, but growth is leveling as engine backlogs normalize. Electronics, conversely, is on track for a 6.15% CAGR through 2031, fueled by 5G infrastructure and electric-vehicle inverter thermal management. Semiconductor fabs are enhancing thermal conductivity and increasing current density by applying aluminum or copper coatings on direct-bonded-copper substrates.

Industrial gas turbines, along with sectors like automotive, oil and gas, medical devices, and energy and power, make up the rest of the market. Medical OEMs are adopting plasma-sprayed hydroxyapatite orthopedic implants, compliant with FDA standards. Meanwhile, the Euro 7 brake-particle regulations are hastening the adoption of wire-arc aluminum-bronze rotors. Oil and gas operators are utilizing HVOF Inconel 625 overlays to combat sour-gas corrosion, achieving an impressive extension of service life. These diverse applications bolster the thermal spray market's resilience, even as traditional internal-combustion volumes wane.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific led with 34.35% 2025 revenue and is forecast to grow at a 5.12% CAGR from 2026 to 2031, the fastest region globally. China's restrictions on mineral exports have paradoxically spurred domestic coating investments, drawing in Western joint ventures keen on securing feedstock. In India, the hubs of Hyderabad and Bengaluru have become the go-to destinations for engine MRO, previously funneled through Singapore, thanks to enticing aviation incentives. Meanwhile, Japanese experts have been transferring their HVOF knowledge to Thailand and Indonesia, focusing on e-powertrain rotor-shaft production.

North America has seen the U.S. Air Force deploying portable cold-spray systems in the field, highlighting a strategic push for swift aircraft repairs. In Canada, thermal-spray erosion coatings are applied in oil sands, while Mexico's automotive sector has ramped up production of cylinder bores and brake rotors tailored for hydrogen and EV platforms. With backing from the U.S. defense sector, domestic powder-plant initiatives aim to reduce reliance on tungsten and rare-earth elements, although commercial production is not expected until 2028.

Europe is grappling with challenges from CSRD carbon accounting mandates and the REACH phase-out of hard chrome. As part of initiatives for hydrogen-ready turbines, Airbus and Safran have been trialing SPS environmental-barrier coatings on A320neo and A350 engines. Germany and France are actively retrofitting industrial gas turbines with coatings adept at handling hydrogen co-firing. South America and the Middle East-Africa see contributions from Brazilian offshore corrosion endeavors and Saudi Arabian desalination projects, though operator shortages and power-grid instabilities limit their output.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The thermal spray market is moderately fragmented. Vertical integration across powder atomization, equipment, and service delivery cushions feedstock volatility and enables turnkey contracts. Cold-spray capability is emerging as a key differentiator; NASA’s 2025 laser-assisted demonstration validated aircraft-field repairs that could displace weld rebuilds. Niche opportunities abound in high-entropy-alloy geothermal linings and hydrogen-ICE cylinder-bore coatings, areas requiring customized feedstocks beyond standard WC-Co or NiCr powders. Smaller shops leverage ISO 14917 and NADCAP certifications to secure aerospace and hydraulic contracts, while equipment vendors pivot to subscription models bundling consumables and remote diagnostics.

Thermal Spray Industry Leaders

BODYCOTE

Linde PLC

OC Oerlikon Management AG

Castolin Eutectic

Kennametal Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: Oerlikon and MTU Aero Engines began building a smart thermal spray factory to digitalize aerospace coating, integrating inline analytics for traceability.

- June 2024: Oerlikon Group opened an Advanced Coating Technology Center for turbine components, expanding research and development capacity.

Global Thermal Spray Market Report Scope

Thermal spraying is an industrial coating process where a consumable is applied as a spray of finely divided semi-molten or molten droplets to produce coatings and then deposit them onto a surface. It is a technology that improves or restores the surface of a solid material. Thermal spraying aids in applying coatings to various materials and components to resist wear, corrosion, cavitation, abrasion, or heat.

The thermal Spray market is segmented by product type, thermal spray coatings and finishes, end-user industry, and geography. By product type, the market is segmented into coatings, materials, and thermal-spray equipment. By thermal spray coatings and finishes, the market is segmented into combustion and electric energy. By end-user industry, the market is segmented into aerospace, industrial gas turbines, automotive, electronics, oil and gas, medical devices, energy and power, and other end-user industries. The report also covers the market sizes and forecasts for the thermal spray market in 27 countries across major regions. For each segment, the market size and forecast are provided based on revenue (USD).

By Product Type

| Coatings | |||

| Materials | Coating Materials | Powders | Ceramics |

| Metals | |||

| Polymers and Other Powders | |||

| Wires/Rods | |||

| Other Coating Materials | |||

| Supplementary Materials (Auxiliary Material) | |||

| Thermal-Spray Equipment | Thermal Spray Coating Systems | ||

| Dust Collection Equipment | |||

| Spray Guns and Nozzles | |||

| Feeder Equipment | |||

| Spare Parts | |||

| Noise-reducing Enclosures | |||

| Other Thermal Spray Equipment | |||

By Thermal Spray Coatings and Finishes

| Combustion |

| Electric Energy |

By End-user Industry

| Aerospace |

| Industrial Gas Turbines |

| Automotive |

| Electronics |

| Oil and Gas |

| Medical Devices |

| Energy and Power |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Coatings | |||

| Materials | Coating Materials | Powders | Ceramics | |

| Metals | ||||

| Polymers and Other Powders | ||||

| Wires/Rods | ||||

| Other Coating Materials | ||||

| Supplementary Materials (Auxiliary Material) | ||||

| Thermal-Spray Equipment | Thermal Spray Coating Systems | |||

| Dust Collection Equipment | ||||

| Spray Guns and Nozzles | ||||

| Feeder Equipment | ||||

| Spare Parts | ||||

| Noise-reducing Enclosures | ||||

| Other Thermal Spray Equipment | ||||

| By Thermal Spray Coatings and Finishes | Combustion | |||

| Electric Energy | ||||

| By End-user Industry | Aerospace | |||

| Industrial Gas Turbines | ||||

| Automotive | ||||

| Electronics | ||||

| Oil and Gas | ||||

| Medical Devices | ||||

| Energy and Power | ||||

| Other End-user Industries | ||||

| By Geography | Asia-Pacific | China | ||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Malaysia | ||||

| Thailand | ||||

| Indonesia | ||||

| Vietnam | ||||

| Rest of Asia-Pacific | ||||

| North America | United States | |||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| NORDIC Countries | ||||

| Turkey | ||||

| Russia | ||||

| Rest of Europe | ||||

| South America | Brazil | |||

| Argentina | ||||

| Colombia | ||||

| Rest of South America | ||||

| Middle-East and Africa | Saudi Arabia | |||

| Qatar | ||||

| United Arab Emirates | ||||

| Nigeria | ||||

| Egypt | ||||

| South Africa | ||||

| Rest of Middle-East and Africa | ||||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the thermal spray market in 2026?

It is valued at USD 12.42 billion in 2026.

What is the forecast CAGR for thermal spray between 2026-2031?

The market is projected to grow at a 4.22% CAGR, reaching USD 15.28 billion in 2031.

Which product type is expanding fastest?

Equipment sales are forecast to advance at a 6.16% CAGR to 2031.

Which end-user segment will grow quickest?

Electronics applications are expected to rise at a 6.15% CAGR through 2031.

Which region leads growth?

Asia-Pacific is projected to expand at a 5.12% CAGR, the fastest worldwide.