Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.21 Billion |

| Market Size (2031) | USD 16.71 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

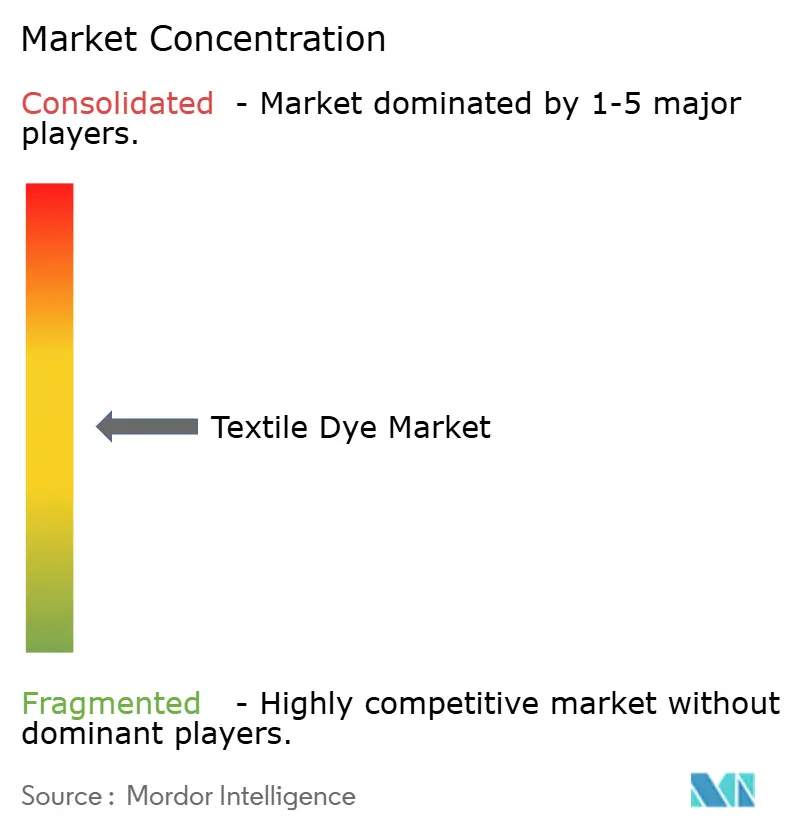

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Dye Market Analysis by Mordor Intelligence

The Textile Dye Market size is projected to be USD 12.65 billion in 2025, USD 13.21 billion in 2026, and reach USD 16.71 billion by 2031, growing at a CAGR of 4.81% from 2026 to 2031. Robust demand for polyester-rich fast-fashion garments, stricter sustainability mandates in North America and the European Union, and the rapid adoption of digital textile printing collectively sustain an above-trend growth path for the textile dyes market. Dispersive chemistries strengthen their position because polyester dyeing requires lower process water and shorter cycles than cotton, while brands increasingly choose synthetics to meet water-reduction targets under California’s AB 405 legislation. Asia-Pacific remains the epicenter of capacity additions as Vietnam and India court foreign direct investment for dyeing and finishing facilities, offsetting the gradual relocation of production from the Chinese mainland. Technical textile applications, from antimicrobial medical fabrics to flame-retardant automotive interiors, widen the addressable opportunity beyond apparel and underpin long-term stability despite fashion’s cyclical swings. Ongoing volatility in aniline and benzene feedstocks, however, demands backward integration or long-term supply contracts to defend margins in the textile dyes market.

Key Report Takeaways

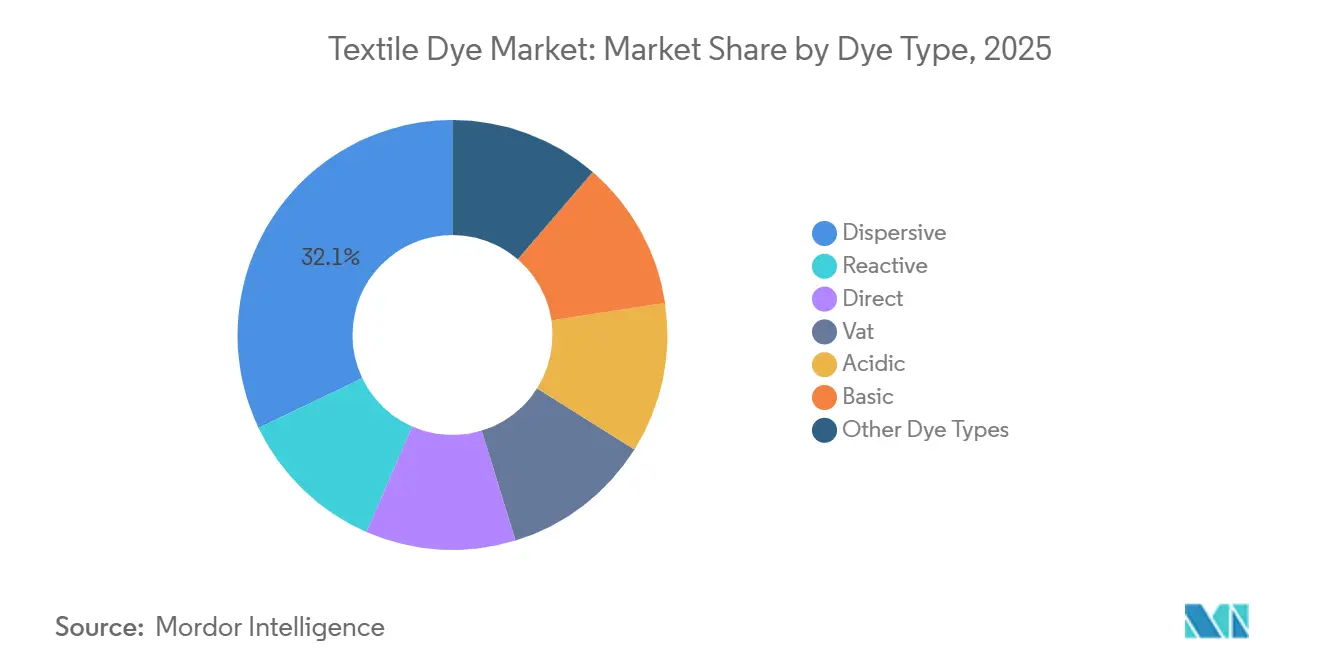

- By dye type, dispersive grades led with 32.11% revenue share in 2025 and are expanding at a 5.61% CAGR through 2031.

- By fiber, polyester captured 50.14% of the textile dyes market share in 2025, and is expanding at a 5.37% CAGR through 2031.

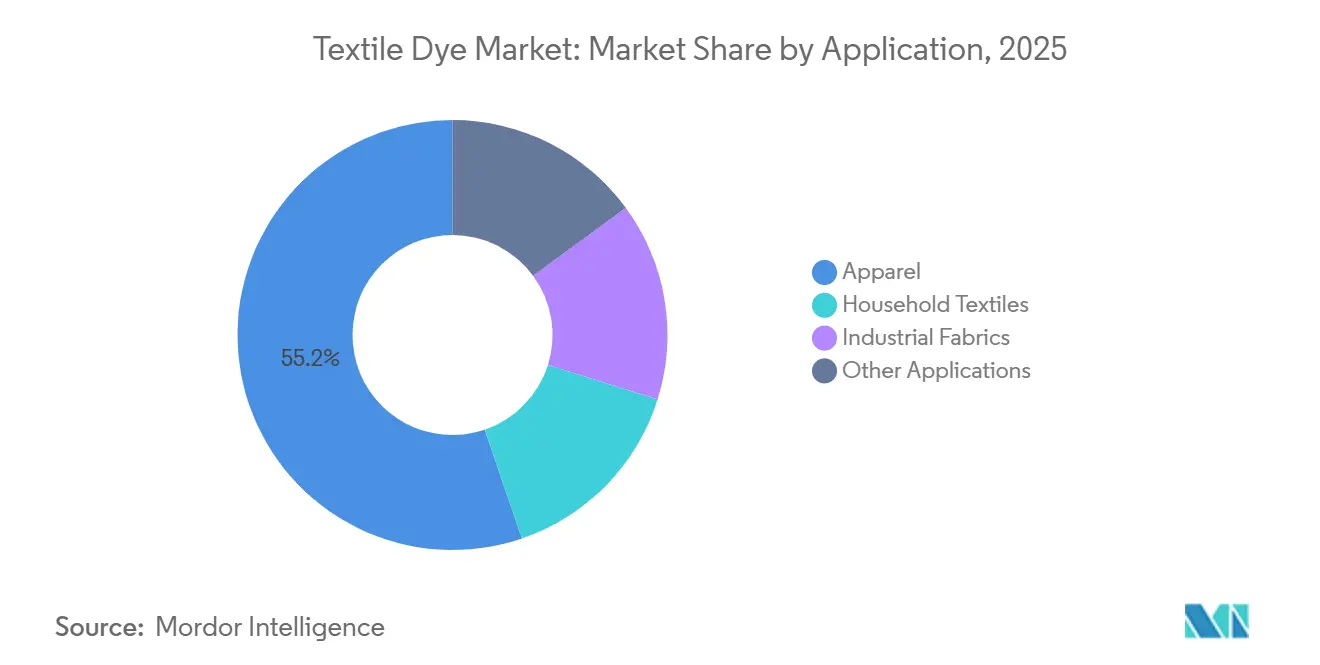

- By application, apparel commanded 55.23% share of the textile dyes market size in 2025 and is projected to grow 5.20% CAGR to 2031.

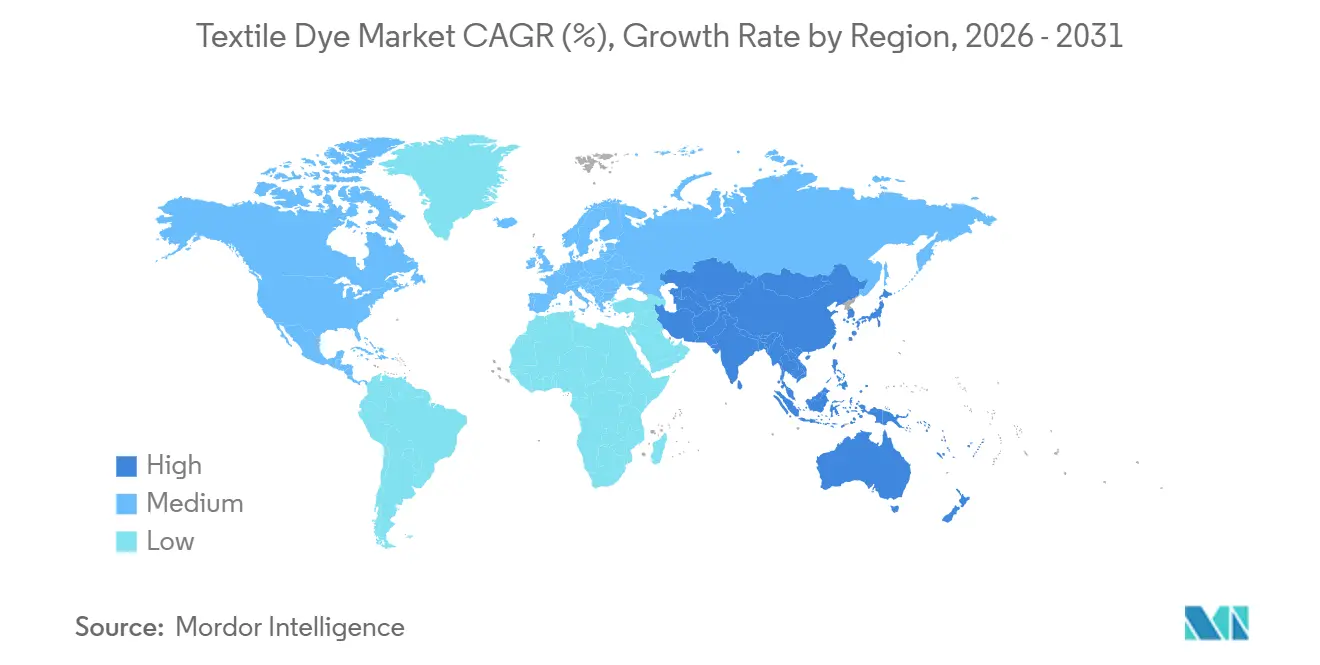

- By geography, Asia-Pacific held a 49.85% share in 2025 and is forecasted to register the fastest 5.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Textile Dye Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Fast-Fashion Output in Emerging Economies | +1.2% | APAC core (Bangladesh, Vietnam, India), spill-over to North Africa | Medium term (2-4 years) |

| Expansion of On-Demand Digital Textile Printing | +0.9% | Global, with early adoption in North America & EU | Short term (≤ 2 years) |

| Growth in Technical & Protective Textile Usage | +0.7% | North America, EU, APAC industrial hubs | Long term (≥ 4 years) |

| Retail Brand Sustainability Mandates (Bio-Based Dyes) | +0.6% | North America & EU, selective adoption in APAC | Medium term (2-4 years) |

| E-commerce Led Rise in Small-Lot Apparel Orders | +0.8% | Global, concentrated in urban metro areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Fast-Fashion Output in Emerging Economies

Bangladesh exported USD 47.4 billion in ready-made garments in 2025, a 12% rise over 2024, and polyester-blend fabrics represented 68% of those shipments[1]World Trade Organization, “World Apparel Trade 2025,” wto.org. Vietnam attracted USD 3.2 billion in textile foreign direct investment during 2025, mainly in dyeing and finishing plants serving near-shoring strategies of Western retailers. India’s Production-Linked Incentive program committed USD 1.44 billion through 2029 to upgrade technical-textile capacity, spurring installations of effluent-treatment units that comply with Zero Discharge of Hazardous Chemicals (ZDHC) protocols. Polyester dyeing consumes 30-40 liters of water per kilogram of fabric compared with 80-100 liters for cotton, lowering energy costs by close to 20% and reinforcing the long-term growth of the textile dyes market. Shorter lead times, from 45 days to 21 days, are now standard for global fast-fashion chains, making the rapid-cycle advantages of dispersive chemistries indispensable.

Expansion of On-Demand Digital Textile Printing

Global digital textile printing capacity increased 28% in 2025, buoyed by 1,847 industrial printer shipments from Kornit Digital, up 28% year on year[2]Kornit Digital, “FY 2025 Investor Presentation,” kornit.com. On-demand printing slashes inventory waste by 35-40% because brands can trial micro-collections without committing to 5,000-unit minimums. Reactive dyes remain dominant in inkjet formulations for cotton because of their covalent bonding, which delivers ISO 105-C06 Grade 4 wash-fastness without extra processing. Pigment-based solutions are gaining traction on polyester but still face color-gamut limitations that constrain their penetration in fashion lines driven by vibrant shades. As printer droplet sizes shrink to 10 picoliters, dye suppliers must reformulate products for viscosity control, drying speed, and nozzle anti-clogging performance.

Growth in Technical & Protective Textile Usage

Protective textiles generated USD 13.5 billion in 2024 revenue and are forecast to grow at 7.25% to 2029 on rising healthcare and automotive demand. Vat dyes occupy 62% of flame-retardant applications because their insoluble pigment structure withstands industrial laundering at 90 °C without color loss. Automotive original-equipment manufacturers specified OEKO-TEX Standard 100 compliance for 89% of interior fabrics in 2025, pushing dye houses to eliminate carcinogenic azo compounds. Acidic dyes hold a share in nylon filtration and geotextiles, where ISO 105-B02 Grade 7 lightfastness is obligatory for 10- to 15-year outdoor exposure. High qualification costs and long testing cycles keep margins resilient in this portion of the textile dyes market.

Retail Brand Sustainability Mandates (Bio-Based Dyes)

California’s AB 405 extended-producer-responsibility rule obliges apparel brands to design for recyclability starting January 2026, spotlighting dye chemistry as a determinant of fiber reuse. The European Union’s Ecodesign Regulation will mandate digital product passports by 2027, further escalating traceability demands. BASF introduced its Indigo Vat 40% bio-based grade in 2025, targeting denim mills that serve Levi’s and VF Corporation. Archroma’s EarthColors line, derived from food-industry waste, won adoption by 14 brands but carries a 15-20% cost premium that tempers mass-market penetration. Enzymatic processes now achieve roughly 80% yield versus 92-95% for petrochemical routes, underscoring the cost hurdle to scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Effluent Discharge Norms | -0.9% | APAC (China, India, Bangladesh), EU | Medium term (2-4 years) |

| Volatility in Petro-Derived Dye Intermediates | -0.7% | Global, acute in regions without petrochemical integration | Short term (≤ 2 years) |

| Competitive Threat from Naturally-Colored Cotton | -0.3% | North America & EU organic-certified segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Effluent Discharge Norms

China’s January 2025 wastewater revision cut allowable chemical oxygen demand to 50 mg/L, forcing 127 dye houses in the Yangtze River Delta to suspend operations pending upgrades. The ZDHC Manufacturing Restricted Substances List added 18 azo dyes in 2024, prompting audits across 11 countries. Installing closed-loop water systems costs USD 2.8-5.1 million per plant, a burden that eliminated roughly one-quarter of smaller facilities in 2025 and drove regional consolidation. Bangladesh’s Department of Environment issued 89 closure notices in 2025, disrupting 15-18% of polyester-blend capacity used by Western brands. Stricter norms disproportionately affect reactive and direct dyes with higher biochemical oxygen demand, nudging consumption toward dispersive formulations aligned with polyester growth.

Volatility in Petro-Derived Dye Intermediates

Aniline prices oscillated between USD 1,420 and USD 1,890 per metric ton in 2025 on crude oil swings and Chinese plant shutdowns. Benzene touched USD 920 per metric ton in Q2 2025 during refinery maintenance in South Korea and India. Margin compression reached 180-240 basis points for producers lacking backward integration, whereas Zhejiang Longsheng’s captive aniline shielded profitability. Three Indian dye projects deferred commissioning to 2027 amid feedstock uncertainty, shrinking spot-market liquidity, and amplifying volatility. Smaller firms that cannot hedge against 25-30% quarterly price spikes face existential risk, hastening industry consolidation and reinforcing the bargaining power of vertically integrated suppliers in the textile dyes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dye Type: Dispersive Chemistries Extend Their Lead

Dispersive dyes secured 32.11% of 2025 revenue, while the segment’s 5.61% CAGR forecast to 2031 exceeds the overall textile dyes market. Polyester’s share of global fiber use underpins that trajectory because dispersive formulations bond effectively without auxiliary reducing agents, trimming process time by up to 25%. Reactive dyes will trail at sub-4% growth as cotton’s environmental scrutiny intensifies. Direct dyes, valued for economical coloration of cellulosic home textiles, contribute 12-14% but face substitution in regions tightening effluent rules.

Huntsman’s supercritical CO₂-compatible dispersive range, commercialized in seven East Asian mills during 2025, eliminates water completely, aligning with regulatory pressures and bolstering premium pricing. Vat dyes retain a lucrative slice through durable outdoor and workwear applications, while acidic dyes keep a foothold in nylon and wool. Basic dyes and niche chemistries round out the remainder, with growth limited by declining acrylic fiber use. Collectively, these shifts will keep the textile dyes market share of dispersive dyes on an upward course through 2031.

By Fiber Type: Polyester Dominance Reshapes Purchasing Patterns

Polyester absorbed 50.14% of 2025 dye volumes and is forecast to expand at 5.37% to 2031 as athleisure demand climbs 9.2% annually and recycled PET adoption accelerates. Cotton’s slice will contract gradually because dyeing 1 kilogram of cotton consumes more than double the water required for polyester, a disparity spotlighted by policymakers in drought-exposed California. Nylon maintains its share as performance sportswear and hosiery applications grow in emerging Asia, delivering premium margins due to specialized acidic dye requirements.

Wool remains a niche luxury and technical-outdoor fiber, sustaining acidic-dye demand that prioritizes colorfastness over cost. Acrylic’s decline mirrors the ascent of polyester fleece in winter garments, capping growth for basic dyes. Viscose and eco-friendly bast fibers, although hailed for biodegradability, together account for a very less share of dye usage because production footprints and technical dyeing hurdles moderate adoption. The textile dyes market size allocated to polyester is thus set to widen, reinforcing investment in dispersive and recycled-polyester-oriented reactive chemistries.

By Application: Apparel’s Micro-Trend Clock Continues to Tick

Apparel contributed 55.23% of the 2025 market value and is predicted to post a 5.20% CAGR through 2031 as direct-to-consumer labels introduce 15-20 micro-collections each year. Brands such as Zara unveiled 12,000 new designs in 2025, a 50% jump over 2020, driving color palette expansion and higher per-garment dye spend. Household textiles are buoyed by emerging-market income gains; India’s home-textile exports grew 14% year-on-year to USD 4.7 billion in 2025. Industrial fabrics hold value where qualification cycles lasting up to three years anchor long-term supply contracts and stabilize revenues.

Other uses, leather, paper, and wood, are being pressured by synthetic substitutes in footwear and automotive interiors. Athleisure’s moisture-management needs push disperse formulations with hydrophobic tweaks that resist perspiration bleed, while modest-fashion growth in Muslim-majority economies escalates demand for high-concentration dark shades. These concurrent trends sustain a diverse chemistry mix, securing a broad base for the textile dyes market through 2031.

Geography Analysis

Asia-Pacific commanded 49.85% of global value in 2025 and is on track for a 5.75% CAGR to 2031. Bangladesh delivered 12% garment-export growth to USD 47.4 billion, Vietnam’s USD 3.2 billion 2025 FDI inflows targeted dyeing facilities, and India’s USD 1.44 billion incentive budget accelerated effluent-treatment adoption. China remains the largest single country, but ceded 180 basis points of share in 2025 as brands diversify for geopolitical resilience. Japan and South Korea, with stringent OEKO-TEX adoption, fulfill specialty-dye demand in automotive and electronics textiles. Indonesia and Thailand benefit from wage arbitrage yet rely heavily on imported intermediates, exposing them to feedstock volatility.

North America’s market share is aided by near-shoring to Mexico, whose 2025 textile FDI totaled USD 890 million. California’s AB 405 places end-of-life recyclability at the forefront, prompting investment in bio-based and easily de-inkable dyes suitable for fiber-to-fiber recycling streams. Canada’s cold-climate outdoor sector continues to specify vat and acidic dyes with extreme colorfastness, while the United States remains import-reliant for 75-plus % of its dye needs.

Europe is constrained by the 2024 REACH ban on 34 azo dyes and the pending Ecodesign passports by 2027. Germany, Italy, and France compose more than half of regional demand, leveraging premium positioning to pass through sustainability-driven cost uplifts. The United Kingdom contends with 4.5% import tariffs post-Brexit, and Russia’s sanctions-impacted sector struggles with specialty-intermediate shortages. South America, led by Brazil is driven by a 214-million-consumer domestic apparel base, while the Middle East and Africa, anchored by Egypt’s USD 3.1 billion export milestone and Saudi Arabia’s Vision 2030 investments.

Competitive Landscape

The textile dye market exhibits moderate fragmentation. Regional specialists such as Kiri Industries, Atul Ltd, and Colourtex secure an 18-22% share through deep backward integration into intermediates that buffer against aniline and benzene swings. White-space opportunities revolve around dyes that maintain color yield on recycled polyester, where a 12-15% loss currently hampers uptake, and around digital-printing formulations that achieve high wash-fastness without energy-intensive post-baking.

Textile Dye Industry Leaders

Archroma

Huntsman International LLC

BASF

Kiri Industries Ltd

Zhejiang Longsheng Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Deven Supercriticals inaugurated India's inaugural commercial-scale supercritical CO₂ dyeing plant. This facility is the world's pioneer in dyeing a diverse range of fabrics, from cotton and nylon to viscose and their blends, using conventional dyes. Such groundbreaking advancements are poised to elevate the demand for textile dyes.

- April 2024: Archroma invested USD 750,000 to expand its South Carolina site, adding six jobs and boosting regional dyeing capacity.

Global Textile Dye Market Report Scope

Dyes are used for coloring fabrics applied to the fiber by diffusion, absorption, or bonding. Dyes can be of two types, which include natural and synthetic dyes. Natural dyes can be derived from plants, minerals, and others. However, synthetic dyes are prepared in the laboratory.

The textile dye market is segmented by dye type, fiber type, application, and geography. By dye type, the market is segmented into reactive, dispersive, direct, vat, acidic, basic, and other dye types. By fiber type, the market is segmented into cotton, polyester, nylon, wool, acrylic, viscose, and other fiber types. By application, the market is segmented into apparel, household textiles, industrial fibers, and other applications. The report also covers the market size and forecasts for the market in 18 countries across the globe. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Dye Type

| Reactive |

| Dispersive |

| Direct |

| Vat |

| Acidic |

| Basic |

| Other Dye Types |

By Fiber Type

| Cotton |

| Polyester |

| Nylon |

| Wool |

| Acrylic |

| Viscose |

| Other Fiber Types |

By Application

| Apparel |

| Household Textiles |

| Industrial Fabrics |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Dye Type | Reactive | |

| Dispersive | ||

| Direct | ||

| Vat | ||

| Acidic | ||

| Basic | ||

| Other Dye Types | ||

| By Fiber Type | Cotton | |

| Polyester | ||

| Nylon | ||

| Wool | ||

| Acrylic | ||

| Viscose | ||

| Other Fiber Types | ||

| By Application | Apparel | |

| Household Textiles | ||

| Industrial Fabrics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the textile dyes market be by 2031?

It is projected to reach USD 16.71 billion in 2031, growing at a 4.81% CAGR from 2026.

Which dye type is expanding the fastest?

Dispersive dyes are forecast to grow at 5.61% CAGR through 2031, buoyed by polyester’s rising share in apparel.

Why is Asia-Pacific so dominant in dye consumption?

The region hosts nearly half of global value because Bangladesh, Vietnam, India, and China anchor the world’s garment manufacturing and attract continuous capacity additions.

What is driving interest in bio-based textile dyes?

California’s AB 405 and the EU’s forthcoming digital product passports incentivize brands to switch to bio-based chemistries that simplify recycling and meet traceability goals.

How are feedstock price swings affecting dye producers?

Fluctuations in aniline and benzene trimmed margins by up to 240 basis points in 2025, pushing non-integrated producers toward long-term contracts or backward integration.

Page last updated on: