Liquid Crystal Polymer (LCP) Films And Laminates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

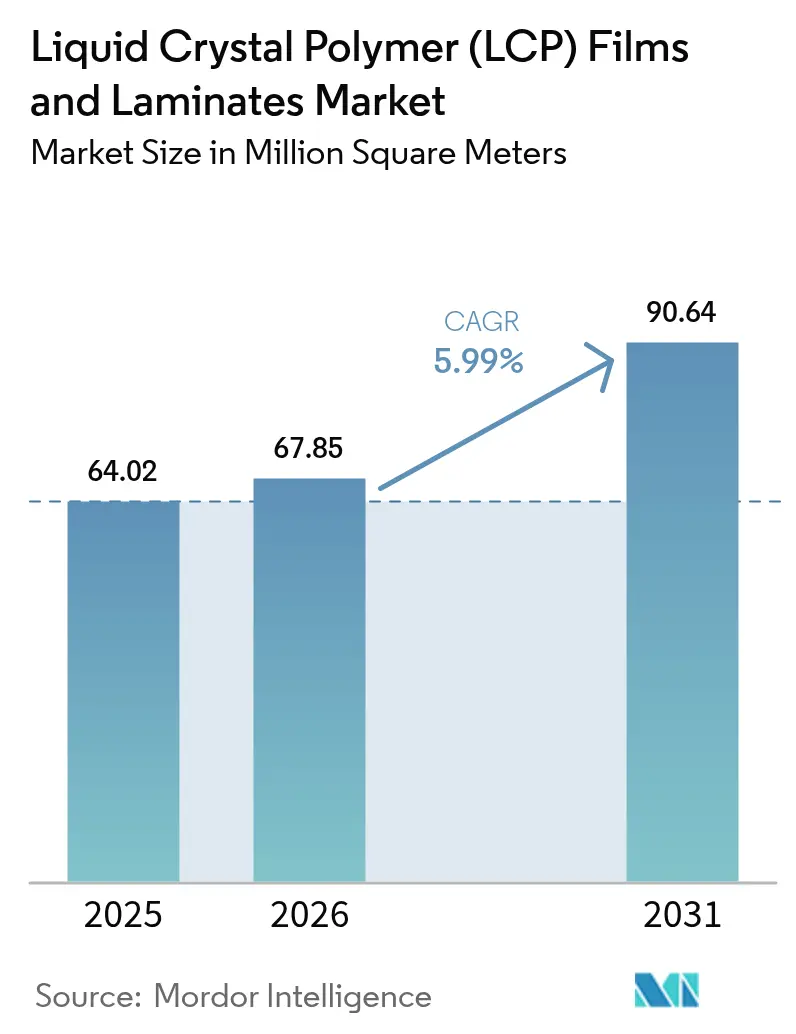

| Market Volume (2026) | 67.85 Million square meters |

| Market Volume (2031) | 90.64 Million square meters |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

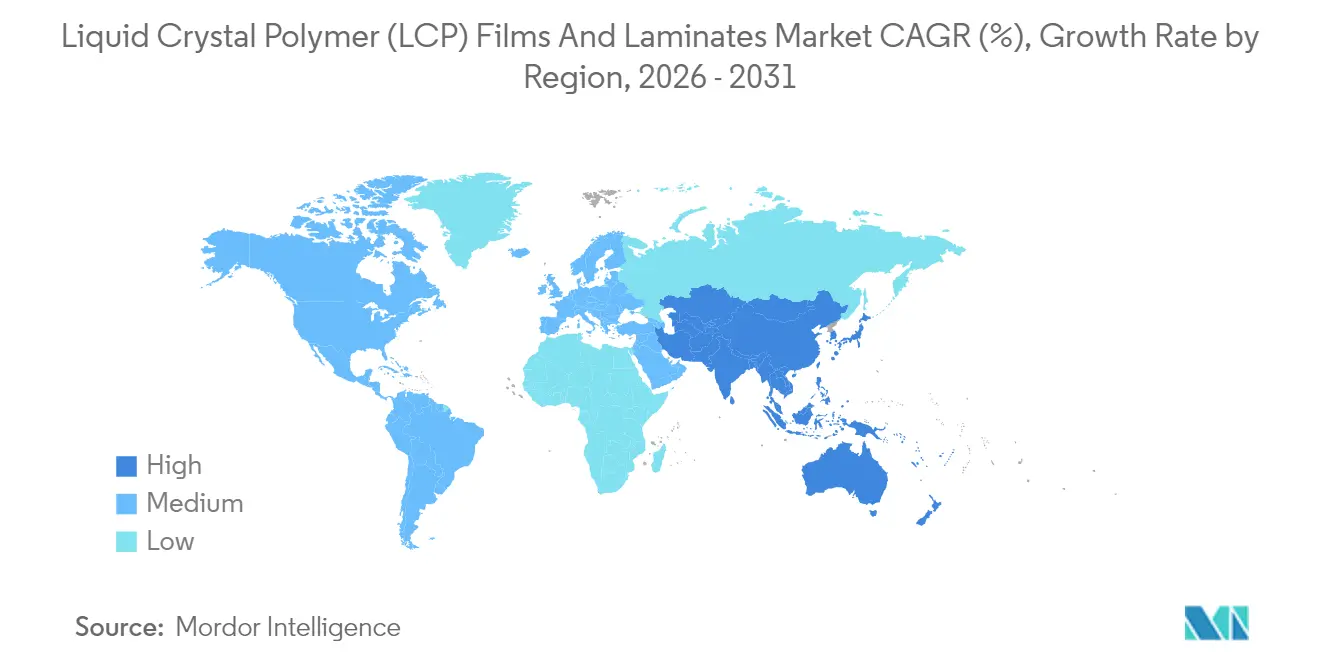

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liquid Crystal Polymer (LCP) Films And Laminates Market Analysis by Mordor Intelligence

Liquid Crystal Polymer (LCP) Films And Laminates Market size in 2026 is estimated at 67.85 million square meters, growing from 2025 value of 64.02 million square meters with 2031 projections showing 90.64 million square meters, growing at 5.99% CAGR over 2026-2031. Momentum stems from 5G infrastructure, foldable device form factors, and automotive imaging radar, which together reinforce demand resilience despite raw material volatility. Manufacturers continue to migrate away from polyimide and PTFE substrates because Liquid Crystal Polymer (LCP) Films and Laminates market materials maintain a 2.9 – 3.5 dielectric constant and <0.004 dissipation factor across millimeter-wave bands, preserving signal integrity even in high-humidity climates. Localization of capacity in East Asia now shortens lead times for handset and base-station customers, while sustainability-driven mass-balance grades create a new premium niche. Cost headwinds linger in Europe and North America where elevated energy tariffs inflate processing expenses, yet incremental productivity gains from ultra-high-flow grades and adhesiveless laminates temper margin pressure. Competitive strategy centers on vertical integration, patent-protected monomer routes, and regional technical support centers that expedite design-in cycles for advanced antenna modules.

Key Report Takeaways

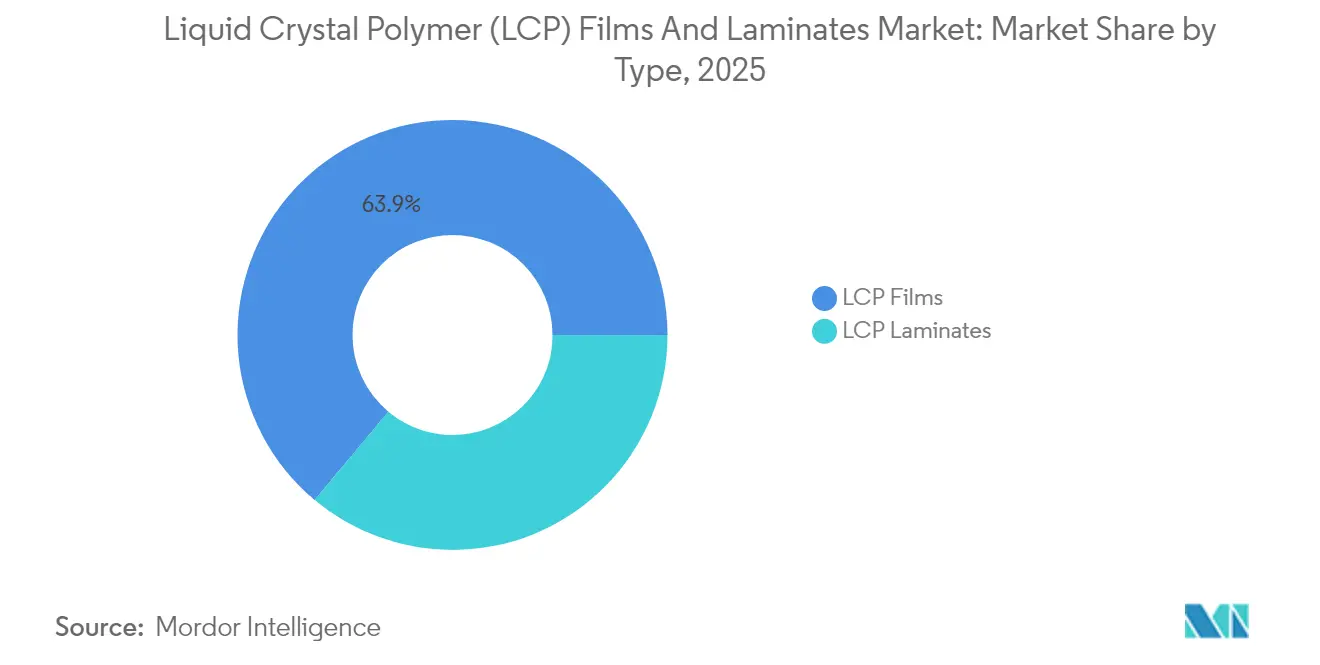

- By type, LCP films captured 63.92% of Liquid Crystal Polymer (LCP) Films and Laminates market share in 2025, while laminates are poised to expand at a 6.05% CAGR through 2031.

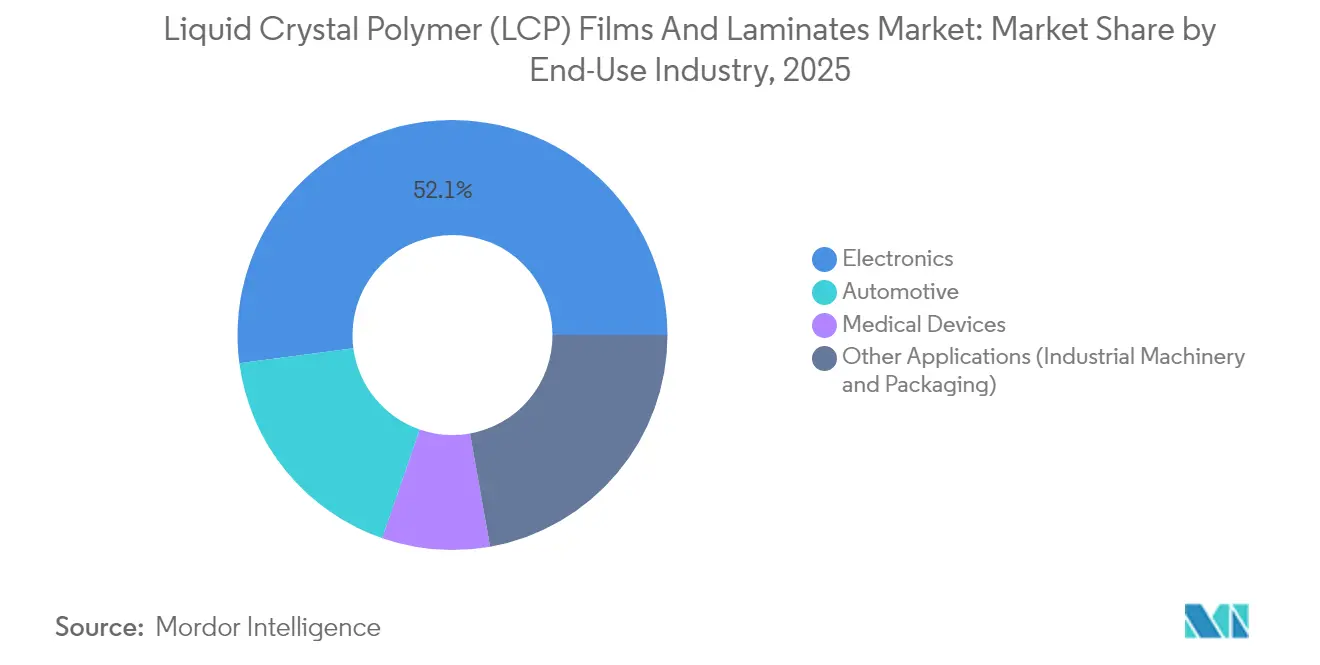

- By end-use industry, electronics accounted for 52.10% of Liquid Crystal Polymer (LCP) Films and Laminates market size in 2025 and is forecast to grow at 6.62% CAGR to 2031.

- By geography, Asia-Pacific contributed 63.10% of 2025 volume; the region will outpace global growth at a 6.41% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Crystal Polymer (LCP) Films And Laminates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization of electronic and electrical components | +1.8% | Global, concentrated in APAC consumer electronics hubs (Shenzhen, Seoul, Tokyo) | Medium term (2–4 years) |

| Surge in 5G / high-frequency communication infrastructure | +2.1% | Global, led by China, South Korea, U.S. metro markets; spillover to India, Brazil by 2027 | Short term (≤ 2 years) |

| Lightweighting and thermal-management needs in EV/ADAS | +1.2% | North America, Europe, China EV corridors; limited uptake in cost-sensitive markets | Long term (≥ 4 years) |

| Growing demand for minimally-invasive medical devices | +0.5% | North America, Western Europe; regulatory-driven adoption in Japan | Long term (≥ 4 years) |

| Flex-CCL adoption for mmWave antenna modules | +1.4% | APAC (China, South Korea, Taiwan); early adoption in North America 5G small cells | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Electronic and Electrical Components

Wearables and foldable phones now require interconnect pitches below 50 µm, a threshold at which polyimide flex circuits exhibit copper-adhesion failures under cyclic bending. Liquid Crystal Polymer (LCP) Films and Laminates market substrates dispense with adhesive layers, trimming total stack thickness by up to 20 µm and sustaining more than 100,000 bend cycles[1]Royal Society of Chemistry, “Adhesiveless LCP Flex Circuit Reliability Improvements,” rsc.org. The design win cadence accelerated in 2024 when flagship Android models adopted adhesiveless LCP antennas to fit sub-0.1 mm z-height constraints. Industrial IoT sensors deployed in rail and wind-turbine environments mirror this migration, citing 10-year durability with no delamination events. Suppliers respond by scaling plasma and chemical-etch surface treatments that raise copper-peel strength beyond 1.2 N/mm, closing historical reliability gaps against polyimide.

Surge in 5G / High-Frequency Communication Infrastructure

Millimeter-wave deployments in the 24–29 GHz range reveal the high insertion losses of FR-4 and standard polyimide. Liquid Crystal Polymer (LCP) Films and Laminates market laminates, with <0.003 dissipation factor in the n258 band, enable beam-forming architectures that extend cell radius without heavier ceramic substrates. China Mobile’s 2024 procurement of LCP-based flexible transmission modules for pole-mounted microcells highlights volume traction, while open-RAN disaggregation necessitates rugged, low-CTE interconnects that tolerate outdoor temperature swings from –40°C to +70°C. Accelerated spectrum auctions in India and Brazil suggest spill-over demand within two years.

Lightweighting and Thermal-Management Needs in EV/ADAS

Automotive radar moving to 4D imaging across 76 – 81 GHz requires dielectric stability over broad bandwidths. Liquid Crystal Polymer (LCP) Films and Laminates market grades satisfy this window, whereas optimized polyphenylene ether substitutes plateau at 0.002 dissipation factor only at center frequency. Rogers Corporation’s AMB power-substrate design win with an Asian EV OEM signals broader busbar-insulation adoption, leveraging LCP’s 0.3 W/m·K thermal conductivity to shed heat in compact battery packs[2]Rogers Corporation, “Q3 2024 Earnings Release,” rogerscorp.com.

Growing Demand for Minimally-Invasive Medical Devices

MRI-guided cardiology and neurovascular interventions rely on metal-free guidewires to avoid imaging artifacts. LCP monofilament offers a tensile strength of over 150 MPa and radiolucency, anchoring a niche but profitable segment where per-kilogram pricing triples that of electronics-grade film. Celanese’s VECTRA MT targets wearable injector housings that must survive gamma sterilization without dimensional creep. Lengthy 510(k) cycles dampen startup enthusiasm, yet large device OEMs continue to spec LCP for MRI-compatibility mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing and processing costs | -1.5% | Global, most acute in Europe and North America where labor and energy costs are elevated | Short term (≤ 2 years) |

| Competition from lower-cost high-frequency polymers (PI, PPE) | -1.0% | Global, strongest in automotive and mid-tier consumer electronics | Medium term (2–4 years) |

| Supply-chain concentration in specialty diacids and biphenols | -0.6% | Global, with acute exposure in Japan and Europe dependent on single-source monomers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing and Processing Costs

Extruding LCP films requires melt temperatures exceeding 300 °C and corrosion-resistant twin-screw lines, which can cost upwards of USD 5 million, deterring new entrants. Trim waste can reach 12% because low melt viscosity causes edge beading, resulting in twice the scrap compared to polyimide lines. Energy consumption is 40% higher than that of polyimide due to prolonged cooling cycles, and European tariffs exacerbate the gap. Celanese’s Zenite 16236(N) lowers processing temperatures to 280°C, reducing utility use; however, the step change still leaves LCP above standard molding ceilings, compelling converters to maintain dedicated cells.

Competition from Lower-Cost High-Frequency Polymers (PI, PPE)

Ester-ether polyimides now exhibit dissipation of 0.0015 – 0.0024 at 10 GHz, which is adequate for sub-6 GHz radios, and cost roughly half that of comparable LCP material. PPE blends capture 77 GHz radar substrates when range requirements stay under 200 m, supported by an established injection-molding infrastructure that Liquid Crystal Polymer (LCP) Films and Laminates market lacks. Sustainability differentials narrow as PPE suppliers adopt chemically recycled feedstocks, challenging LCP’s nascent bio-balanced grades and compressing its premium positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Films Retain Volume Lead while Laminates Accelerate on Integration Demand

LCP films claimed 63.92% of the 2025 volume in the Liquid Crystal Polymer (LCP) Films And Laminates Market, underscoring their foundational role in antenna-in-package circuits that dominate flagship smartphone architectures. Stable spot pricing near USD 180/kg throughout 2024 signals that capacity expansions in Japan and South Korea largely matched handset demand cycles. Laminates, although smaller, are forecast to outgrow films at a 6.05% CAGR through 2031, as integrated antenna modules favor copper-clad substrates that simplify assembly flows. Murata’s adhesiveless laminate qualification cut module reduced the z-height by 30 µm and improved thermal cycling reliability, illustrating why Liquid Crystal Polymer (LCP) Films and Laminates market customers are pivoting toward laminate solutions. Plasma-etched laminate surfaces now achieve a peel strength of over 1.2 N/mm, solving the surface-energy hurdle that once limited widespread adoption. Geographically, North American orders skew towards laminates for aerospace and defense, where pre-qualified stacks simplify certification, while APAC handset hubs still drive over 70% of film uptake.

Second-order dynamics suggest that thicker laminate formats (75 – 125 µm) are suitable for base-station antenna feeds, while thinner films (<50 µm) are more suitable for foldable devices, enabling regional suppliers to specialize. Chinese entrants such as Shenzhen WOTE tout next-generation grades with elevated glass-transition temperatures to capture local 5G infrastructure business . Concurrently, Japanese incumbents protect premium niches through patent-reinforced monomer syntheses that yield ultra-low ionics required for high-reliability aerospace boards.

By End-Use Industry: Electronics Dominate while Automotive Continues to Lag

Electronics accounted for 52.10% of the 2025 volume and are expected to remain the fastest-growing user, with a 6.62% CAGR to 2031, as Liquid Crystal Polymer (LCP) Films and laminates become indispensable market substrates for millimeter-wave smartphone antennas. Wi-Fi 7 routers, data-center optical transceivers, and smartwatches extend the demand base, each leveraging LCP’s moisture resistance to mitigate performance drift in humid home-network environments. Base-station flexible transmission modules further widen the scope, a shift underscored by tier-one OEM qualification pipelines logged in 2025.

The automotive sector maintained an 17.60% volume share in 2025, as PPE substrates meet current 77 GHz radar cost targets. Adoption momentum rises post-2027 with the introduction of 4D imaging radar, where frequency stability from 76 to 81 GHz propels LCP to the forefront. Battery-management-system busbars represent a parallel opportunity, leveraging the thinness of LCP laminates to reduce pack weight while safeguarding 800 V architectures. Medical devices, roughly 8.10% of demand, benefit from price inelasticity as MRI-guided catheter makers prioritize biocompatibility over resin cost. Other industrial uses, including high-temperature connectors in renewable-energy inverters, round out the Liquid Crystal Polymer (LCP) Films and Laminates market landscape.

Geography Analysis

Asia-Pacific held 63.10% of 2025 volume in Liquid Crystal Polymer (LCP) Films And Laminates Market, a dominance aligned with the region’s dense handset assembly clusters and its vertically integrated LCP supply chain. Kuraray, Toray, and Sumitomo Chemical maintain technology leadership in film extrusion, while Celanese’s 2024 Nanjing plant added 15% to global resin capacity, bringing resin synthesis closer to Chinese EV and 5G customers. South Korea focuses on laminate conversion for foldable-display antennas, where ultra-thin films enable 1.5 mm bend radius hinges. India’s first wave of 5.5 G base-stations, set for 2027, should lift regional demand as spectrum auctions conclude, maintaining a 6.41% CAGR through 2031.

North America's demand is concentrated in aerospace radar arrays, medical implants, and data-center interconnects. Rogers Corporation decided in October 2024 to locate its next power-substrate plant in China, aiming to service Asian EV customers, as it faces cost hurdles on US soil. Still, defense budgets sustain local laminate demand, insulating the region from the cyclicality of consumer electronics. Mexico’s emerging electronics assembly corridors may gradually replace some Asia-bound imports if near-shoring incentives deepen.

Europe faces eroded price competitiveness due to high electricity tariffs. German institutes investigate end-of-life LCP recycling under EU circular-economy mandates, potentially offsetting carbon costs and bolstering regional appeal. Eastern-European EMS plants show tentative interest in LCP flex boards for industrial IoT gateways, yet scale remains small. South America and the Middle East & Africa share the remaining <10%, with rollout pace tied directly to sovereign 5G capital-expenditure timetables.

Competitive Landscape

The Liquid Crystal Polymer (LCP) Films And Laminates Market is moderately consolidated. Japanese incumbents defend positions with patent-protected monomer chemistries, deterring Western entrants, while Chinese challengers develop alternative synthetic paths that skirt existing IP claims. Celanese introduced 60% renewable-content Zenite ECO-B in April 2024, targeting OEMs that confront Scope 3 emission targets despite a 20% price premium. Polyplastics’ biomass-balanced LAPEROS bG-LCP, slated for commercial release in 2025, aims for similar adoption in sustainability-minded markets.

Liquid Crystal Polymer (LCP) Films And Laminates Industry Leaders

-

Celanese Corporation

-

KURARAY CO. LTD.

-

Polyplastics Co. Ltd.

-

Sumitomo Chemical Advanced Technologies

-

TORAY INDUSTRIES INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sumitomo Chemical Co., Ltd. acquired a liquid crystal polymer (LCP) neat resin business from Belgium's Syensqo SA/NV. With the integration of Syensqo's products and technology, Sumitomo aims to bolster its offerings and expand its LCP business, especially targeting ICT and mobility applications.

- January 2025: Biesterfeld, an international distributor, bolstered its strategic partnership with Celanese Corporation, a manufacturer of engineering plastics. As part of this collaboration, Biisterfeld added two new LCP product families, Vectra and Zenite, to its portfolio.

Global Liquid Crystal Polymer (LCP) Films And Laminates Market Report Scope

Liquid crystal polymer (LCP) is an engineering plastic with a combination of high strength, modulus, and impact properties, flame retardance, resistance to a wide range of aggressive chemicals, shallow and tailorable coefficients of thermal expansion (CTE), excellent dimensional stability, thin-wall flowability, and unique processability.

The Liquid Crystal Polymer (LCP) Films And Laminates Market is segmented by type, application, and geography. By type, the market is segmented into LCP films and LCP laminates. By application, the market is segmented into automotive, electronics, medical devices, and other applications (industrial machinery, packaging, etc.). The report also covers the market size and forecasts for the liquid crystal polymer (LCP) films and laminates market in 22 countries across major regions. For each segment, the market sizing and forecasts have been done based on Volume (million square meter).

| LCP Films |

| LCP Laminates |

| Automotive |

| Electronics |

| Medical Devices |

| Other Applications (Industrial Machinery, Packaging) |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | LCP Films | |

| LCP Laminates | ||

| By End-Use Industry | Automotive | |

| Electronics | ||

| Medical Devices | ||

| Other Applications (Industrial Machinery, Packaging) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of Liquid Crystal Polymer (LCP) Films and Laminates in 2031?

The market is forecast to reach 90.64 million m² by 2031, rising from 67.85 million m² in 2026.

How fast is demand for LCP laminates expected to grow?

Laminates are projected to register a 6.05% CAGR through 2031 as antenna-in-package modules become standard.

Which region leads consumption of LCP films and laminates?

Asia-Pacific held 63.10% of 2025 volume and is set to expand faster than any other region through 2031.

Why are LCP substrates preferred for millimeter-wave 5G devices?

LCP maintains a <0.004 dissipation factor and low moisture absorption that preserve signal quality above 24 GHz.

What is the main restraint limiting wider LCP adoption in automotive radar?

Premium resin cost and adequate performance from lower-cost PPE substrates delay LCP penetration until 4D imaging radar ramps after 2027.

Page last updated on: