Market Overview

| Study Period | 2021 - 2031 |

|---|---|

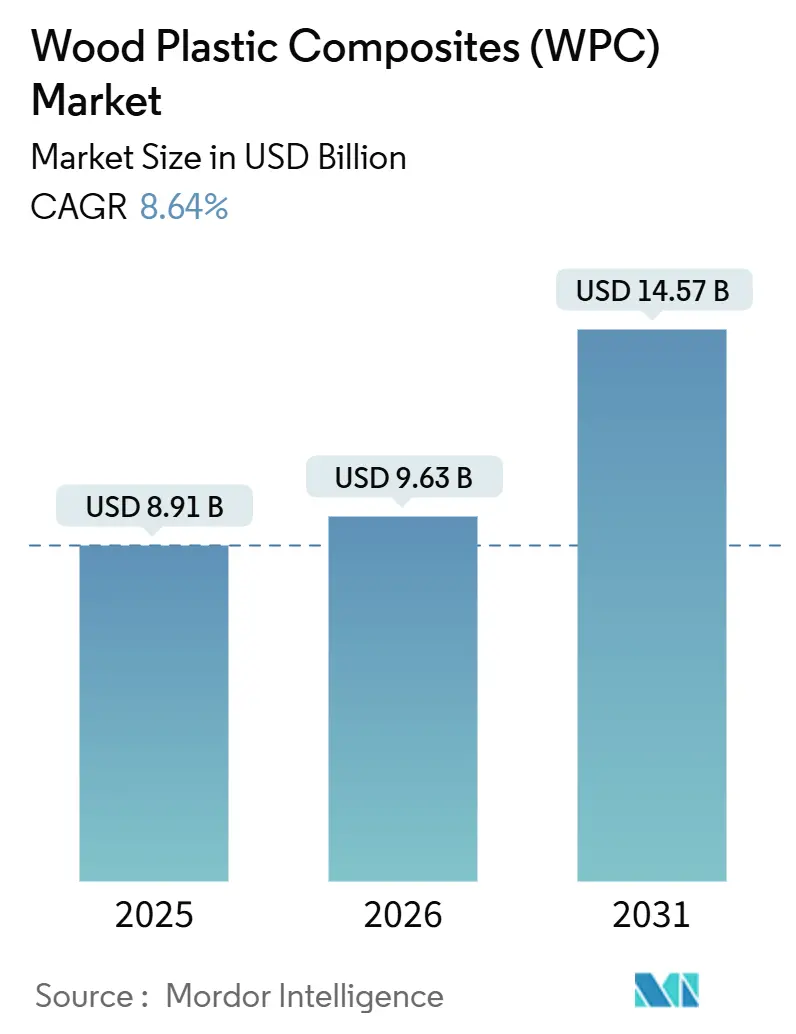

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 14.57 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

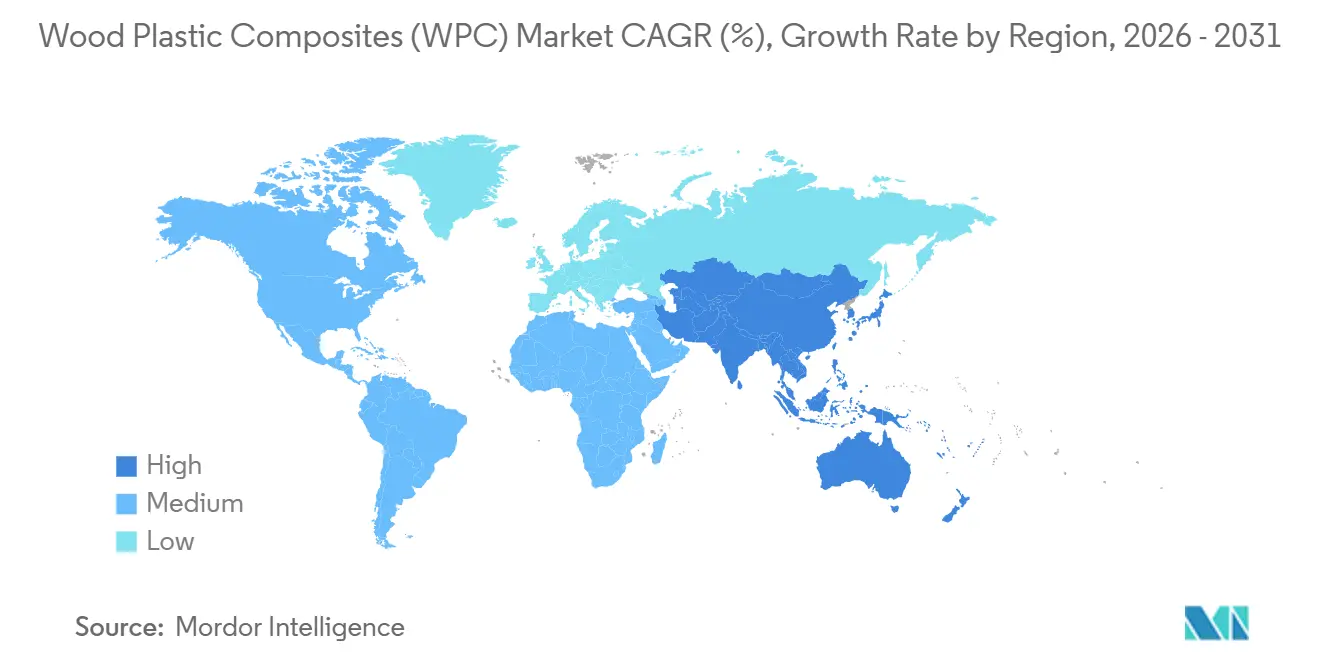

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Plastic Composites (WPC) Market Analysis by Mordor Intelligence

The Wood Plastic Composites Market size is projected to expand from USD 8.91 billion in 2025 and USD 9.63 billion in 2026 to USD 14.57 billion by 2031, registering a CAGR of 8.64% between 2026 to 2031. Mandatory wood-fiber-reuse targets in the European Union and China are transforming post-consumer wood from a disposal cost into valuable feedstock, easing raw-material pressure and anchoring demand for composite decking, fencing, and trim. Automotive lightweighting regulations in the European Union, United States, and China are accelerating polypropylene-based formulations, while co-extrusion technology is elevating capped profiles into a premium, maintenance-free option. Polymer-price volatility and fire-resistance certification hurdles remain key challenges, yet steady innovation in flame-retardant additives, glass-bubble fillers, and digital extrusion controls signals an industry pivot from commodity to engineered-material positioning. Competitive intensity stays moderate, with the five largest producers capturing roughly 38% revenue, leaving meaningful whitespace for regionally focused extruders and vertically integrated recyclers.

Key Report Takeaways

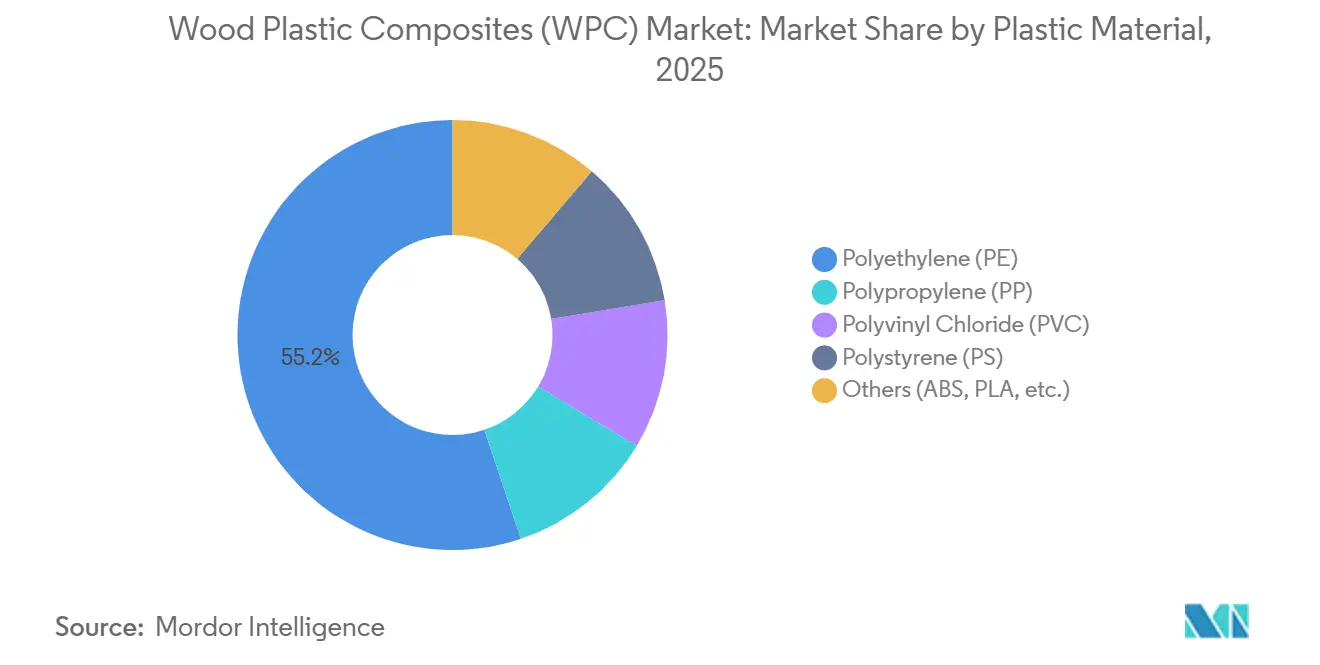

- By plastic material, polyethylene captured 55.16% of the wood plastic composite market share in 2025; polypropylene is projected to expand at a 9.26% CAGR between 2026 and 2031.

- By processing technology, extrusion commanded 70.36% of the wood plastic composite market size in 2025, while injection molding records the fastest projected CAGR at 9.15% through 2031.

- By product form, Uncapped (Conventional) WPC held 65.42% of 2025 revenue, whereas capped profiles will post a 9.56% CAGR to 2031.

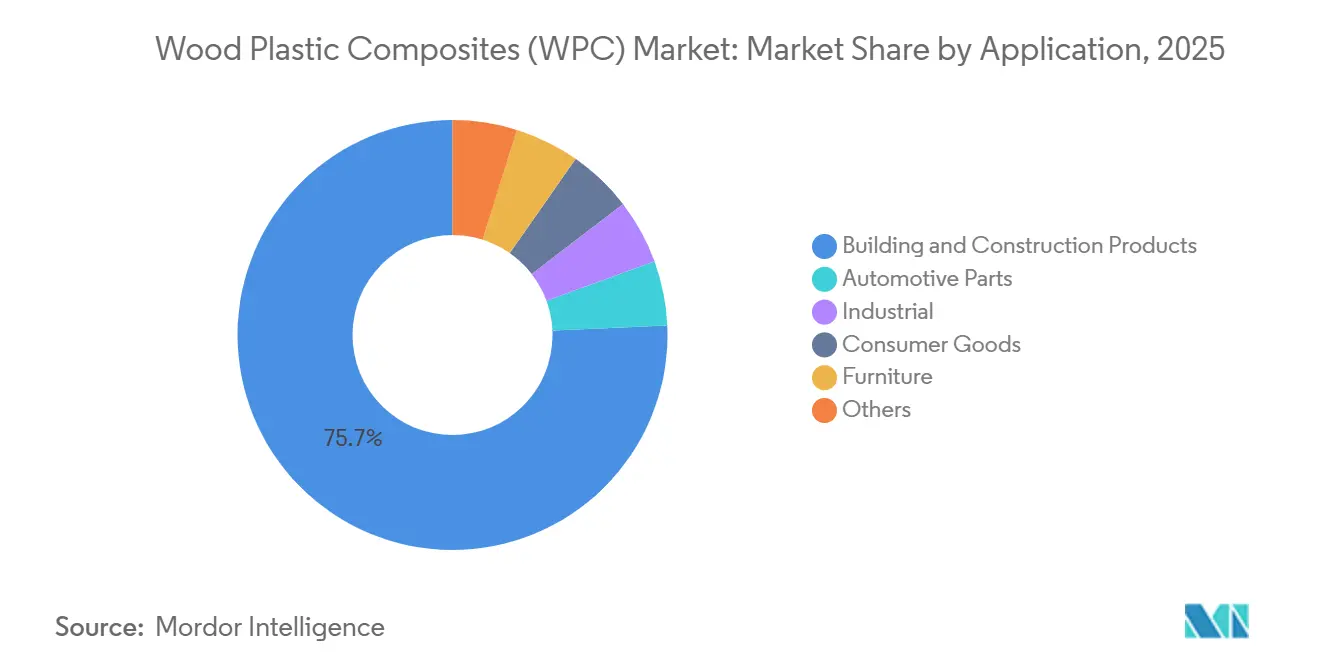

- By application, building and construction accounted for a dominant 75.71% of the wood plastic composite market size in 2025; automotive parts are advancing at a 9.42% CAGR to 2031.

- By geography, the Asia Pacific held 55.38% of the 2025 global revenue and is projected to sustain a 9.52% CAGR, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Plastic Composites (WPC) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in DIY home-improvement & outdoor-living projects | +2.1% | North America, Europe, APAC urban cores | Short term (≤ 2 years) |

| Mandatory wood-fiber-reuse targets | +1.8% | EU core, China, spill-over to ASEAN | Medium term (2-4 years) |

| Shift toward lead-free PVC-based indoor WPC in Asia | +1.5% | China, India, Southeast Asia | Medium term (2-4 years) |

| Lightweighting push for non-structural automotive parts | +1.3% | Global, concentrated in EU & China automotive hubs | Long term (≥ 4 years) |

| Growing demand for low-maintenance urban landscaping products | +1.0% | APAC tier-2/3 cities, Middle East, North America suburbs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in DIY Home-Improvement & Outdoor-Living Projects

Lock-in effects from pandemic remodeling have persisted, keeping US outdoor-project spending above USD 90 billion in 2026 and lifting composite-decking specification rates among national builders. Big-box retailers have increased the wood plastic composites market shelf space by 30% since 2023, pairing digital design tools with one-day pickup to remove perceived project complexity. Homes marketed with pre-installed composite decks are closing 15% faster than comparable wood-deck listings, underscoring resale-value recognition among buyers. E-commerce penetration sits near 12% today, but direct-to-consumer brands are shortening sample-delivery windows to forty-eight hours, intensifying pressure on dealer-based incumbents. The resulting traffic funnel continues to ratchet up brand loyalty, as customers who complete a first WPC project report a 67% likelihood of specifying composites on subsequent outdoor jobs.

Mandatory Wood-Fiber-Reuse Targets

The European Union Waste Framework Directive revision, effective January 2024, compels member states to recycle 65% of municipal waste by 2035, with a distinct carve-out for wood streams. China’s 14th Five-Year Plan similarly mandates a 60% utilization rate for bulk industrial solid waste by 2025, naming lumber residues as a priority feedstock[1]National Development and Reform Commission, “14th Five-Year Plan for Circular Economy,” ndrc.gov.cn. As municipalities divert demolition timber into material recovery channels, composite extruders are securing multi-year offtake agreements that undercut sawmill demand for virgin flake. Germany’s Hamburg Sanitation Department, for instance, signed a ten-year supply contract with a regional extruder covering 30,000 tonnes annually, swapping previous incineration routes for mechanical recycling. Compliance with the European Union Deforestation Regulation, live since June 2023, further tilts sourcing away from imported hardwood decking toward local composite profiles.

Shift Toward Lead-Free PVC-Based Indoor WPC in Asia

Updated Chinese standard GB 18580-2017 caps lead at 90 ppm in indoor decorative products, catalyzing adoption of calcium-zinc and organotin-stabilized PVC-WPC. Indian standard IS 15871 is on track for a 2026 ratification with comparable limits, propelling capex into new twin-screw lines across Gujarat and Maharashtra. Though lead-free stabilizers add 8-12% material cost, certified PVC-WPC now qualifies for green-building incentives in Singapore’s BCA Green Mark and the UAE’s Estidama Pearl schemes. Guangdong-based plants commissioned since 2024 have raised regional capacity by 200,000 tonnes per year, aiming at interior wall cladding, door frames, and modular furniture exports to Southeast Asia and the Gulf Cooperation Council.

Lightweighting Push for Non-Structural Automotive Parts

The European Union’s post-2025 passenger-car CO₂ limit of 95 g/km imposes a monetary penalty near EUR 95 per exceeded gram, pricing every kilogram shed at roughly EUR 2 in avoided fines[2] European Commission, “Directive 2008/98/EC on Waste,” europa.eu. Injection-molded WPC interior panels deliver 15–20% mass savings against glass-fiber-reinforced PP while maintaining comparable impact strength. Volkswagen Group’s 2025 supplier-scorecard revision allocates bonus points to parts exceeding 25% recycled or bio-based content, automatically elevating qualifying WPC bids. China’s dual-credit scheme for new-energy vehicles magnifies the incentive by awarding lightweighting credits convertible to revenue, accelerating platform-wide material transitions at BYD and Geely.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Temperature sensitivity & long-term wear/creep | -1.2% | Global, acute in high-temperature climates (Middle East, Southern U.S.) | Long term (≥ 4 years) |

| Volatility in recycled & virgin polymer prices | -0.9% | Global, most severe in regions dependent on imported resin (EU, India) | Short term (≤ 2 years) |

| Fire-resistance certification hurdles for high-rise construction | -0.7% | Urban centers with high-rise density (Asia-Pacific, Europe, North America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Temperature Sensitivity & Long-Term Wear/Creep

WPC’s coefficient of thermal expansion is 3–5 times that of lumber, leading to 6 mm board growth over a 3 m span in Riyadh summer highs, which installers must offset with expansion gaps. Long-term creep testing published in the Journal of Materials in Civil Engineering states 15–20% mid-span deflection growth after five years under constant load for uncapped beams. Capped co-extruded profiles moderate surface temperature by 10–15°F and resist moisture ingress but cost 25–35% more, curbing uptake in price-sensitive projects. Glass-bubble fillers are promising mitigations, yet add USD 0.20 per linear foot, pressuring margins against premium hardwoods such as ipe.

Volatility in Recycled & Virgin Polymer Prices

Crude oil-linked polyethylene prices fluctuated by 22% between Q1 2024 and Q4 2025. Recycled HDPE trades at a 15–25% discount to virgin resin but suffers inconsistent melt-flow and contamination, lifting cleaning costs. The EU Carbon Border Adjustment Mechanism adds EUR 50–80 per imported-polymer tonne starting 2026, steering European extruders toward domestic recyclate even as supply remains tight. Bio-based PE from Brazilian sugarcane commands a 20–30% premium but insulates buyers from crude swings, giving vertically integrated producers a hedge over spot-market purchasers.

Segment Analysis

By Plastic Material: Polypropylene Gains on Automotive Demand

Polyethylene retained 55.16% of 2025 volume, anchoring the wood plastic composites market through economy-grade decking and fencing. Polypropylene, however, is expanding at 9.26% CAGR on surging automotive applications where injection-molded WPC interior trim replaces glass-fiber reinforced PP, delivering 15% weight savings and improved recyclability. Polyvinyl chloride captures indoor wall and furniture niches, leveraging inherent fire resistance to command a 10–15% premium. Polystyrene remains confined to low-stress décor, whereas ABS and PLA occupy a small but fast-growing “others” slice as municipalities pursue compostable or bio-based credentials.

End-users perceive PP-WPC as an easy switch: it runs on existing automotive tooling, passes low-VOC cabin-air requirements in the European Union, and integrates seamlessly into circular supply chains seeking single-polymer stream recovery. HDPE’s supply-chain depth keeps it the first choice for commodity profiles, yet susceptibility to thermal expansion is steering premium lines toward capped co-extruded hybrids. Patent data show 31% of 2025 WPC filings involved co-extrusion die advancements, illustrating a shift from raw-material cost focus to process ingenuity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Processing Technology: Injection Molding Scales for Complex Geometries

Extrusion delivered 70.36% of 2025 output by virtue of low-cost, continuous-profile production suited to decking, siding, and fencing. Injection molding is growing at 9.15% CAGR as tier-1 suppliers install multi-cavity tools yielding six door panels per shot, slashing per-part cost to parity with glass-fiber PP. Over-molding fasteners inside WPC parts trims assembly labor by 12–15%, a decisive saving in labor-scarce European plants.

Compression molding and pultrusion remain specialized, servicing structural poles and pedestrian-bridge planking where longitudinal strength premiums outweigh slow cycle times. Capital outlays climb for co-extrusion lines, USD 2–3 million versus USD 1–1.5 million for single-layer extruders, favoring well-capitalized players and gradually consolidating capacity, a trend likely to lift average selling prices from 2027 onward.

By Product Form: Capped Profiles Take Premium Position

Un-capped profiles captured 65.42% of 2025 shipments, anchoring the wood plastic composites market share in price-sensitive residential and municipal projects. Capped co-extruded decking, however, is expanding at a 9.56% CAGR through 2031 as homeowners accept a 20–30% premium in exchange for reduced fading and easier cleaning. Performance tests published by ASTM International show capped boards retain 90% of original color after five years versus 70–75% for uncapped alternatives, making the upgrade an attractive life-cycle investment. Contractors report warranty claims drop by one-third when capped products are specified, easing service-call costs. Municipal buyers still favor uncapped grades for benches and boardwalks because initial outlay, not aesthetics, drives budget decisions.

Hybrid “partially capped” boards that coat only top and side surfaces entered volume production in 2025 and already hold 8% of segment demand, offering a middle ground between cost and durability. Large producers are capitalizing on higher margins: Trex noted that capped lines accounted for 68% of residential-decking revenue in its latest filing, lifting gross margin two points year over year. Smaller Asian extruders are catching up by licensing co-extrusion dies, but equipment costs of USD 2–3 million per line remain a barrier. As cap-layer pigment technology advances, color-matched railings and fascia boards are driving attachment sales, further enlarging the wood plastic composites market size attributable to premium systems.

By Application: Automotive Parts Break Out of Niche

Building and construction absorbed 75.71% of 2025 demand, reflecting entrenched use in decking, fencing, cladding, and trim across North America and Asia-Pacific. Within this umbrella, decking alone represented more than half of the installed volume, underpinned by a remodeling cycle that continues to favor low-maintenance materials. Fencing is the fastest riser in construction, gaining from privacy concerns in suburban housing and perimeter needs for schools and parks. Municipal landscaping products, benches, planters, and pergolas, are surging due to city mandates for water-saving and long-life assets, widening the installed footprint and pushing distributors to carry broader SKUs. Collectively, these uses keep construction central to the wood plastic composites market size at least through 2028.

Automotive parts are the standout growth pocket, projected to climb at a 9.42% CAGR as OEMs chase weight reduction to meet tightening fleet CO₂ limits. Door panels, trunk liners, and package trays molded from polypropylene-based WPC trim 15–20% mass versus glass-fiber PP while hitting low-VOC targets for cabin air, a decisive procurement metric in the European Union. BYD and Geely already deploy WPC interior trim on electric-vehicle platforms, gaining 2–3% range extensions that translate directly into consumer appeal. The segment’s momentum is also attracting aftermarket converters that retrofit conventional models with lighter panels, opening a secondary revenue stream for suppliers. As more tier-1 vendors lock in composite programs, automotive could lift its wood plastic composites market share from today’s mid-single digits to near 10% by the end of the decade.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific produced 55.38% of global revenue in 2025 and is set to compound at 9.52% through 2031, driven by China’s push to a 70% urban population share and India’s state-subsidized housing surge. Municipal bids in Hefei now require WPC park furniture in all new greenfield developments exceeding 3 ha, accelerating capex into capped-profile lines within Zhejiang and Anhui provinces. Southeast Asian markets, Vietnam, Thailand, Indonesia, absorb rising pallet and crate demand linked to export-manufacturing growth and ISPM-15 compliance, boosting industrial-grade WPC shipments.

North America held a significant portion of 2025 sales, owing to a USD 495 billion remodeling pool where outdoor projects remain the single fastest-growing spend category. Builders shifting away from chemically treated lumber favor composite decking for warranty and resale-value optics. Canadian provincial rebates for energy-efficient refurbishments indirectly benefit composite cladding and railing adoption. Mexico’s emergent extrusion corridor near Monterrey supplies US demand under USMCA tariff protections, shortening transit lead times.

Europe’s share trails its population weight but stands to climb as landfill bans on construction waste tighten in Germany, the Netherlands, and the Nordics. The EU’s Carbon Border Adjustment adds cost pressure to imported hardwoods, advantaging locally extruded composites certified under EN 15804 environmental-product declarations. Meanwhile, Middle East and South America exhibit pockets of double-digit growth, Dubai’s WPC park mandates, Brazil’s resort deck refurbishments, and Chile’s earthquake-resilient façade retrofits underscore latent potential once supply-chain hurdles ease.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Wood Plastic Composites (WPC) market exhibits moderate concentration. North American brand leaders wield extensive patent portfolios around co-extrusion and embossing, supporting gross margins near 40%. Scandinavian challenger PolyPlank leans on bio-based PLA to court municipal buyers fulfilling zero-landfill targets, a niche strategy but one enabling contract wins in Stockholm’s 2025 public-park overhaul. Achieving ISO 9001 and ASTM D7032 certification has become table stakes for public procurement, naturally filtering out under-capitalized entrants and nudging the sector toward gradual consolidation.

Wood Plastic Composites (WPC) Industry Leaders

Trex Company Inc.

The AZEK Company Inc.

UFP Industries, Inc.

Fiberon (Fortune Brands Innovations)

Oldcastle APG (CRH)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: The US Environmental Protection Agency (EPA) proposed revisions to multiple sections of 40 CFR Part 770, titled 'Formaldehyde Standards for Composite Wood Products', as part of the Toxic Substances Control Act (TSCA). This proposal was published in the Federal Register (91 FR 6161). This can impact the wood plastic composites (WPC) market.

- April 2025: CenturyPly unveiled its premium-quality louvers crafted from WPC (Wood-Plastic Composite). Initially debuting in the major cities of Delhi and Bangalore, CenturyPly has plans for a nationwide rollout. CenturyWPC harnesses high-quality raw material for enhanced strength, longevity, and eco-friendliness.

Global Wood Plastic Composites (WPC) Market Report Scope

Wood plastic composite is a lumber or panel product made from the amalgamation of wood fiber/shavings/flour and thermoplastic fibers. These composites exhibit improved thermal, mechanical, thermal, and processing characteristics compared to conventional plastic, treated lumber, and steel components, allowing them to extend their applications in highly contoured parts of building products, automotive, furniture, and other consumer products. Wood plastic composites are recognized as sustainable materials as they are often made using reused plastic and wood wastes.

The wood plastic composites (WPC) market is segmented by plastic material, processing technology, product form, application, and geography. By plastic material, the market is segmented into polyethylene, polypropylene, polystyrene, polyvinyl chloride, and other plastic materials. By processing technology, the market is segmented into extrusion, injection molding, and compression and pultrusion. By product form, the market is segmented into capped (Co-extruded) WPC and uncapped (Conventional) WPC. By application, the market is segmented into building and construction, automotive parts, industrial, consumer goods, furniture, and other applications. By geography, the market is segmented into Asia Pacific, North America, Europe, South America, and the Middle East and Africa. The report also covers the size and forecasts for the wood plastic composites (WPC) market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

By Plastic Material

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyvinyl Chloride (PVC) |

| Polystyrene (PS) |

| Others (ABS, PLA, etc.) |

By Processing Technology

| Extrusion |

| Injection Molding |

| Compression & Pultrusion |

By Product Form

| Capped (Co-extruded) WPC |

| Uncapped (Conventional) WPC |

By Application

| Building & Construction Products | Decking |

| Fencing | |

| Molding & Trimming | |

| Landscaping & Outdoor | |

| Automotive Parts | |

| Industrial | |

| Consumer Goods | |

| Furniture | |

| Others |

By Geography

| Asia | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Plastic Material | Polyethylene (PE) | |

| Polypropylene (PP) | ||

| Polyvinyl Chloride (PVC) | ||

| Polystyrene (PS) | ||

| Others (ABS, PLA, etc.) | ||

| By Processing Technology | Extrusion | |

| Injection Molding | ||

| Compression & Pultrusion | ||

| By Product Form | Capped (Co-extruded) WPC | |

| Uncapped (Conventional) WPC | ||

| By Application | Building & Construction Products | Decking |

| Fencing | ||

| Molding & Trimming | ||

| Landscaping & Outdoor | ||

| Automotive Parts | ||

| Industrial | ||

| Consumer Goods | ||

| Furniture | ||

| Others | ||

| By Geography | Asia | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will the wood plastic composites market be by 2031?

It is forecast to reach USD 14.57 billion by 2031, expanding at an 8.64% CAGR from 2026.

Which plastic resin is growing fastest inside composite formulations?

Polypropylene is rising at a 9.26% CAGR, propelled by automotive lightweighting mandates.

Are capped profiles really worth the price premium?

Yes, they retain 90% of initial color after five years and cut homeowner maintenance costs, justifying a 20–30% upcharge.

What region leads current demand?

Asia-Pacific accounts for 55.38% of global revenue and continues to outpace other regions.

Who are the leading manufacturers?

Trex Company, The AZEK Company, UFP Industries, PolyPlank Solutions, and Anhui Sentai collectively hold about 38% global share.