Concrete Repair Mortar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

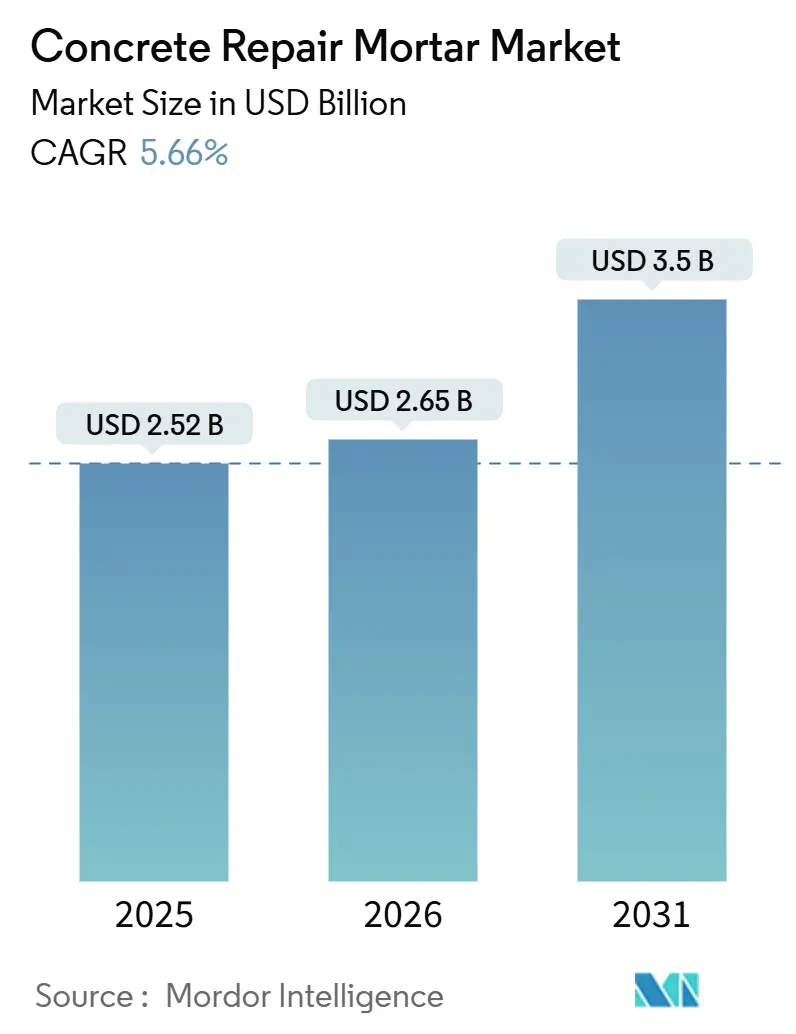

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concrete Repair Mortar Market Analysis by Mordor Intelligence

The Concrete Repair Mortar Market size was valued at USD 2.52 billion in 2025 and is estimated to grow from USD 2.65 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 5.66% during the forecast period (2026-2031). Aging infrastructure across developed economies, sizable public-sector rehabilitation budgets, and wider acceptance of polymer-modified formulations are steering the shift from reactive patching to planned life-cycle management. Regulatory pressure is mounting as Europe now mandates annual renovation of 3% of public buildings, while U.S. bridge owners tap the USD 40 billion Bridge Formula Program to fund rapid-setting overlay systems. Suppliers that bundle repair mortars with IoT-enabled sensors are capturing early mover advantage because asset owners value real-time carbonation data that extends inspection intervals.

Key Report Takeaways

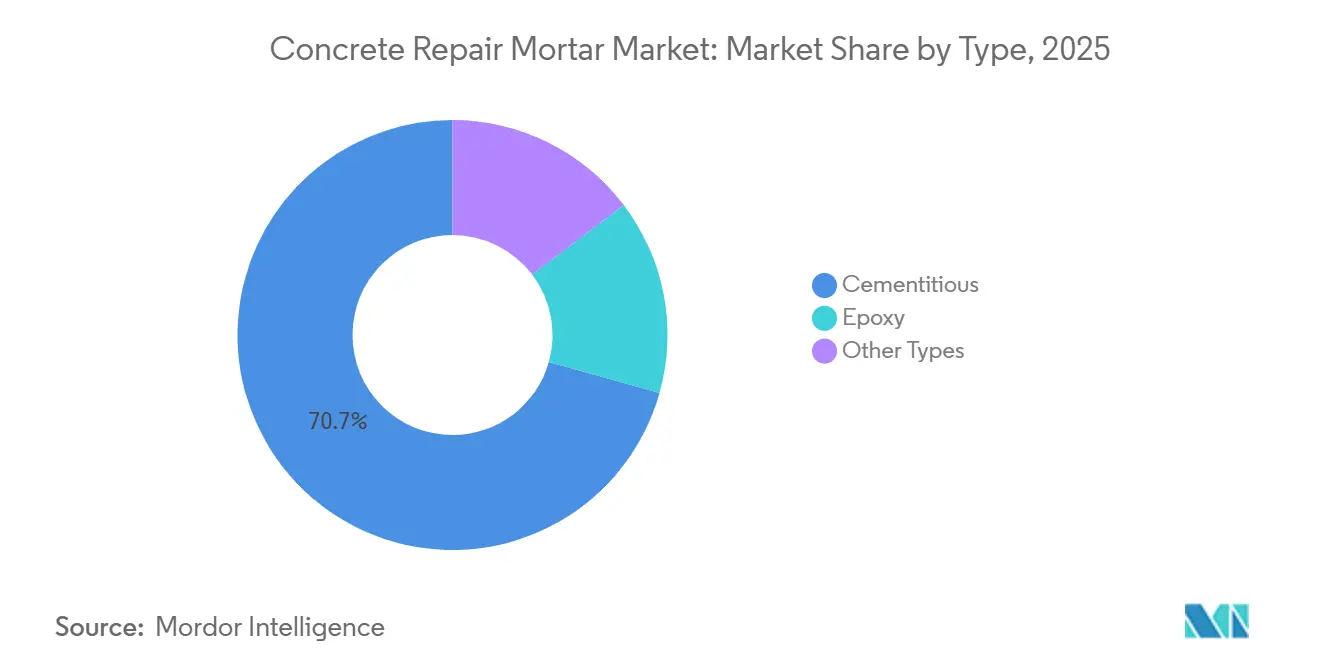

- By type, cementitious led with 70.65% concrete repair mortar market share in 2025 and is expanding at a 5.84% CAGR through 2031.

- By application method, spraying accounted for 61.44% of the concrete repair mortar market size in 2025 and is advancing at a 6.07% CAGR through 2031.

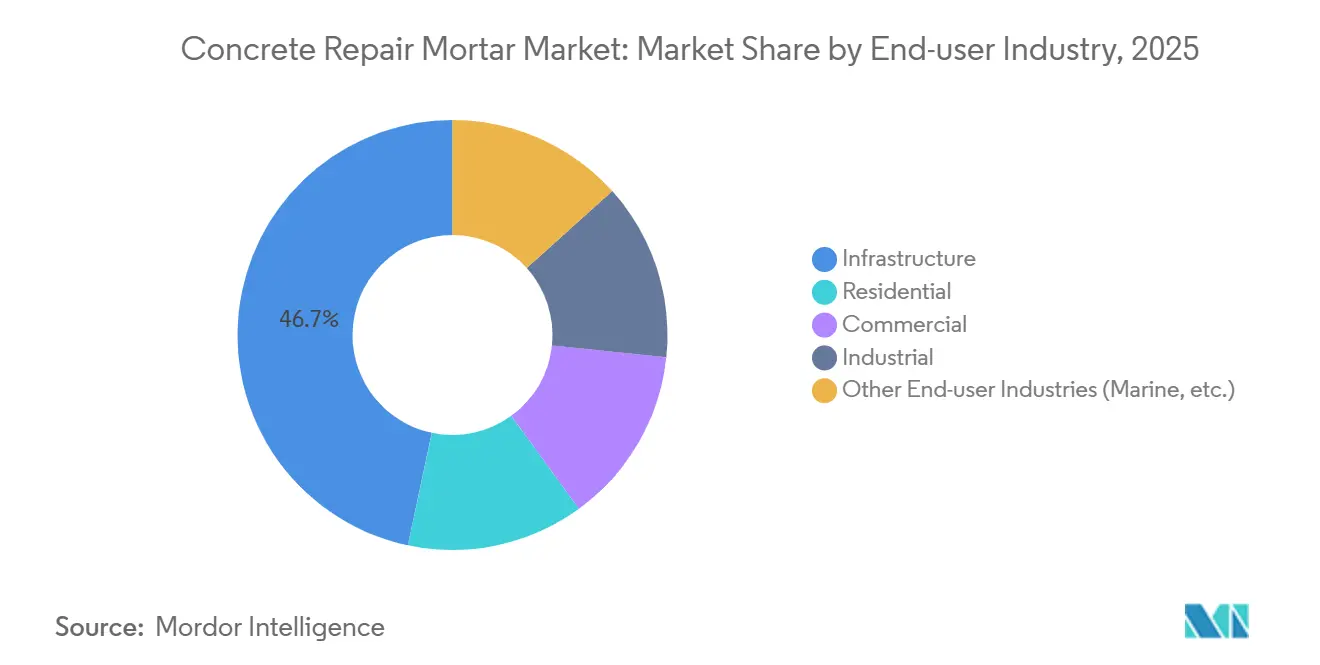

- By end-user industry, infrastructure captured 46.69% of the concrete repair mortar market size in 2025 while recording the fastest growth at a 5.91% CAGR through 2031.

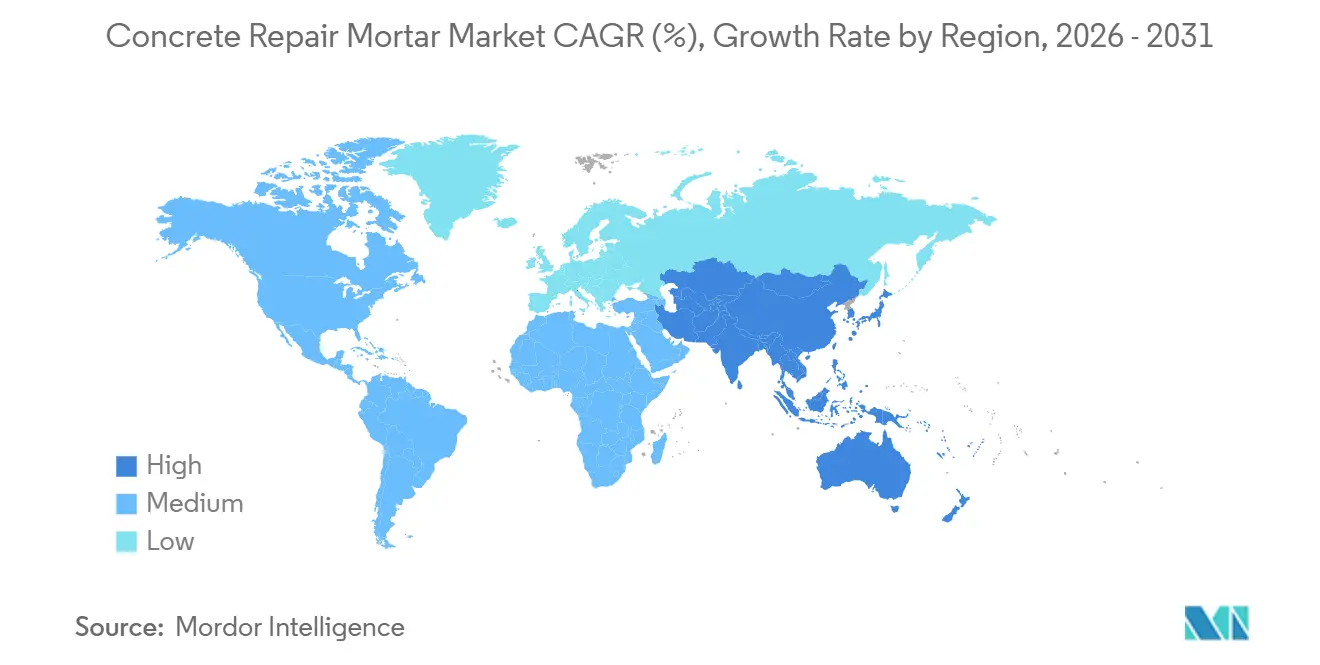

- By geography, Asia-Pacific held a 37.65% of the concrete repair mortar market share in 2025 and is projected to post a 6.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Concrete Repair Mortar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging transport infrastructure stock in Europe and North America | +1.5% | North America, Europe | Long term (≥ 4 years) |

| Expanding rehabilitation budgets for bridges and tunnels | +1.3% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of polymer-modified and fiber-reinforced repair mortars | +1.0% | Global | Medium term (2-4 years) |

| Stringent building-safety codes mandating periodic maintenance | +0.8% | North America, Europe, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Demand for ultra-low-carbon alkali-activated repair mortars in net-zero projects | +0.6% | Europe, select North America municipalities, early adopters in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Transport Infrastructure Stock in Europe and North America

Over 42,000 U.S. bridges now carry a structurally deficient rating, pushing owners toward high-performance overlays that add 15–25 years of service life without full replacement. Germany faces a similar backlog on 25,000 autobahn bridges erected before 1985, and EUR 2 billion a year is earmarked for polymer-modified rehabilitation[1]German Federal Ministry for Digital and Transport, “Bridge Rehabilitation Funding,” bmdv.bund.de . Condition-based inspection, enabled by ground-penetrating radar and half-cell mapping, lets owners intervene early, creating a steadier demand curve for suppliers. This diagnostic-driven model is widening the concrete repair mortar market because interventions occur before ratings slip below closure thresholds. Contractors consequently schedule work more predictably, smoothing labor deployment across seasons.

Expanding Rehabilitation Budgets for Bridges and Tunnels

The Infrastructure Investment and Jobs Act alone directs USD 40 billion to the Bridge Formula Program, and early grants favor rapid-setting polymer-modified mortars that keep traffic flowing overnight. New York State supplemented federal dollars with USD 450 million green bonds that specify low-carbon repair mixes for thruway structures to meet climate mandates. Europe’s Connecting Europe Facility dedicates EUR 33.7 billion through 2027, with tunnel upgrades consuming a rising share as fire-resistant linings become mandatory. Multi-year public budgets are underwriting long visibility for materials suppliers, though execution risk persists because labor shortages lengthen lead times.

Rapid Adoption of Polymer-Modified and Fiber-Reinforced Repair Mortars

Latex-modified cementitious mortars lower water-cement ratios, lifting bond strength 40–60% and allowing 5 mm thin-section repairs. Sika’s 2024 purchase of Kwik Bond Polymers delivered macro-synthetic fiber technology that replaces steel mesh, shrinking overlay labor by 30% and material weight by 15%. MAPEI’s Planitop range adds migrating corrosion inhibitors that double re-application intervals in chloride-rich settings. Hybrid microfiber–macrofiber blends now satisfy seismic energy-dissipation rules in California and Japan. Although polymer content raises material cost by up to 40%, payback occurs within five years on high-traffic assets because lane-closure penalties drop.

Stringent Building-Safety Codes Mandating Periodic Maintenance

The International Building Code 2021 requires facade inspections every ten years, with New York City and Miami-Dade imposing even tighter windows following high-profile failures. Miami-Dade’s 40-year recertification law has generated a queue of 1,200 towers needing polymer-modified repairs that promise 50-year durability. California seismic rules target 3,500 non-ductile concrete buildings for retrofit by 2025, spurring demand for fiber-reinforced mortars that restore shear capacity. Europe’s EN 1504 durability classes likewise push specifiers toward accredited products, filtering out low-compliance imports.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of cement, epoxy resins and specialty admixtures | -0.7% | Global | Short term (≤ 2 years) |

| Stringent VOC and dust-emission regulations on job sites | -0.4% | North America, Europe, developed Asia-Pacific markets | Medium term (2-4 years) |

| Shortage of certified concrete-repair applicators and high labor costs | -0.5% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Cement, Epoxy Resins, and Specialty Admixtures

Concrete-block prices jumped 5.8% quarter-over-quarter in Q2 2024 as kiln fuel costs and freight tariffs rose. Epoxy resins tracked crude oil, swinging 15–20% in Asia when cracker turnarounds tightened supply, forcing North American formulators to hold larger inventories. A 2024 fire that sidelined 12% of European capacity for calcium-nitrite inhibitors led to allocation regimes favoring long contracts, squeezing small buyers. Public owners on fixed multi-year budgets sometimes downgrade specifications when bids spike, risking long-term durability.

Stringent VOC and Dust-Emission Regulations on Job Sites

California’s Rule 1113 caps primers at 250 g/L VOC, nudging formulators to water-based chemistries that cure more slowly in humidity and raise labor time by 15%. Texas proposes parallel limits for 2027 that would phase out solvent-rich epoxies across Dallas–Fort Worth and Houston. OSHA silica limits require wet-cutting and respiratory gear, pushing contractors toward wet-mix shotcrete that satisfies dust rules but demands higher pump horsepower[2]Occupational Safety and Health Administration, “Crystalline Silica Final Rule,” osha.gov. Compliance costs add USD 50,000–100,000 in equipment per site, accelerating consolidation among contractors that can amortize outlays.

Segment Analysis

By Type: Cementitious Anchor Market Share Through Substrate Compatibility

Cementitious captured 70.65% revenue in 2025, demonstrating the highest concrete repair mortar market share because they bond seamlessly with Portland-cement substrates and meet installer familiarity thresholds. Within this category, latex additives slash permeability and enable 5 mm thin reinstatement layers on bridge decks. In contrast, epoxy systems, though smaller, command premiums above USD 15/kg in chloride-rich or chemical-spill settings where impermeability matters. Moisture-insensitive epoxies have recently widened their application window to damp substrates, a breakthrough that could lift epoxy’s portion of the concrete repair mortar market size by 2031.

Other chemistries remain niche. Methyl-methacrylate mortars reach 3,000 psi in two hours and suit overnight highway patches in dense corridors like the Washington Beltway. Magnesium-phosphate mixes cure below -10 °C, crucial for Canadian winter repairs. Regulatory filters are tightening: the EU’s REACH limits certain amines while California Proposition 65 spurs silica-free blends. Suppliers prepared with compliant formulations are better placed to defend or grow their concrete repair mortar market share across regulated geographies.

Note: Segment shares of all individual segments available upon report purchase

By Application Method: Spraying Captures Vertical and Overhead Repairs

Spraying delivered 61.44% revenue in 2025 and will expand at 6.07% as robotic rigs cut labor by half and generate consistent compaction. Field data show waste drops 30% when flow meters and automatic nozzles govern mix efficiency. Dry-mix variants still dominate mountainous or remote jobs lacking ready-mix access. Precision pouring remains the choice for horizontal floors where self-leveling mortars exceed FF50 flatness for automated warehouses, controlling 25% of the concrete repair mortar market size in slab remediation.

Manual troweling persists in low-value residential facade patches but is losing share because labor rates inflate. Dust rules pressure dry-mix adoption; wet-spray meets OSHA silica standards without costly tenting. Consequently, North American infrastructure projects now specify wet-mix on over 65% of bridge soffits, nudging spraying to further elevate its concrete repair mortar market share through 2031.

By End-user Industry: Infrastructure Drives Predictable Repair Cycles

Infrastructure accounted for 46.69% demand in 2025 and leads growth at 5.91% because bridge-management systems now trigger repairs once chloride ions reach 0.2% weight of cement or half-cell readings slip under -350 mV. The U.S. Bridge Formula Program ensures annual funding, letting departments award multi-year overlay contracts that stabilize volumes for suppliers.

Residential spikes stem from facade ordinances such as Miami-Dade’s 40-year rule, whereas commercial asset owners act when due diligence audits highlight deferred maintenance. Industrial plants want fast-cure, chemically resistant mortars; petrochemical floors demand sulfonic acid tolerance, while food processors need USDA clearance. Marine and wastewater jobs push chloride-diffusion below 2 × 10⁻¹² m²/s, favoring specialized vendors. These sub-sectors diversify concrete repair mortar market revenue streams even as infrastructure dominates volume.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 37.65% of 2025 revenue, with a 6.32% CAGR forecast, making it the fastest contributor to the concrete repair mortar market. China’s highway network exceeds 177,000 km and many expressway bridges built before 2010 now reach first major rehab windows; provincial owners prefer polymer-modified mortars that extend cycles by 20 years and reduce lifecycle cost 30%. India’s National Infrastructure Pipeline allocates USD 1.4 trillion, 19% for urban rail that specifies fiber-shotcrete linings rated for 100-year durability. Indonesia’s 3,200-km Trans-Java tollway and Malaysia’s MRT spur Southeast Asian growth. Japan’s seismic mandates drive shrinkage-compensated mortars for 72% of bridges soon crossing 50-year age.

North America offers steady expansion anchored by the Infrastructure Investment and Jobs Act. The U.S. National Bridge Inventory lists 42,000 deficient bridges, and layer-funding with toll revenues secures a multiyear concrete repair mortar market. Canada channels CAD 33.5 billion through the Investing in Canada plan, emphasizing cold-weather mixes that hydrate at below 5 °C. Mexico’s near-shoring industrial corridor upgrades will add incremental demand once assets enter maintenance.

Europe shows regulatory-led divergence. The Energy Performance of Buildings Directive compels 3% annual renovation of public stock, steering specifications toward alkali-activated binders with 80% lower emissions. Germany pours EUR 2 billion yearly into autobahn bridge overlays, while the UK’s carbon tool penalizes high-emission mortars on the Lower Thames Crossing. Southern Europe struggles with fiscal constraints, yet private owners in Spain and Italy comply with balcony-safety rules that favor epoxy injections.

South America’s concrete repair mortar market is tied to Brazilian and Chilean highway concessions that impose strict International Roughness Index limits and require six-hour reopening mixes. Argentina’s lithium brine plants demand sulfate-resistant mortars for ponds cycling -10 °C to 40 °C. Colombia’s 4G infrastructure program enters its first rehab phase, signaling fresh demand as tropical humidity accelerates joint wear.

Middle-East and Africa add lumpy yet high-margin opportunities. Saudi Arabia’s NEOM and Red Sea mega-projects need UV-resistant mortars tolerating 50 °C swings, while UAE rail extensions specify epoxy track-bed repairs for 200-ton freight loads. Qatar’s performance contracts penalize premature failures, incentivizing fiber blends with 20-year warranties. South Africa’s ZAR 198 billion road-rehab backlog is price sensitive, nudging the use of locally blended cementitious mixes.

Competitive Landscape

Competition is moderately concentrated: the five largest producers—Sika, MAPEI, Saint-Gobain, ARDEX GmbH, and The Euclid Chemical Company—generate 45–50% of global revenue. To differentiate, multinationals vertically integrate into admixtures and digital monitoring. Sika’s 2024 Kwik Bond Polymers buy unlocked proprietary macro-fibers and cross-selling lifted bundled sales; management targets a 15% revenue bump by 2027. MAPEI expanded Indonesian and Vietnamese plants to capture Southeast Asian demand while marketing Planitop low-carbon formulations eligible for LEED points. Saint-Gobain’s Weber unit commercialized 70% recycled alkali-activated mortars that meet France’s RE2020 caps.

White-space innovation centers on self-healing systems using bacteria encapsulation; early trials show 0.5 mm cracks seal autonomously and trim lifetime maintenance 25%. Flexcrete and Kryton inhabit marine niches, supplying chloride-resistant epoxy screeds over USD 15/kg under multi-year port contracts. Euclid Chemical’s patent on calcium-sulfoaluminate cements that hit 3,000 psi in four hours earned royalty deals with regional producers, creating high-margin recurring income. Robotics partnerships by BASF and Sika embed quality sensors into shotcrete rigs, countering skilled-labor shortages and appealing to contractors on lump-sum jobs.

Concrete Repair Mortar Industry Leaders

Sika AG

Saint-Gobain

MAPEI S.p.A.

ARDEX GmbH

The Euclid Chemical Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: MC-Bauchemie introduced Nafufill RM 10 Rapid, a fast-setting repair mortar designed for quick concrete and masonry restoration. It cured sufficiently for recoating in approximately 30 minutes, offering high strength and frost resistance for both indoor and outdoor applications, including resurfacing and creating covings.

- September 2024: Mapei S.p.A. introduced "The Zero Line," a range of construction products aimed at achieving carbon neutrality by reducing environmental impact while maintaining high performance and durability. This range comprised over 230 products, including concrete repair mortars, adhesives, and waterproofing membranes, with residual CO₂ emissions fully offset through certified environmental credits supporting reforestation and biodiversity protection initiatives.

Global Concrete Repair Mortar Market Report Scope

Concrete repair mortars are designed specifically to replace or restore the original profile and functionality of the damaged concrete. This mortar helps repair concrete defects, enhances its look, regains structural integrity, improves durability, and extends the life of the building.

The concrete repair mortar market is segmented by type, application method, end-user industry, and geography. By type, the market is segmented into cementitious, epoxy, and other types. By application method, the market is segmented into spraying, pouring, and manual. By end-user industry, the market is segmented into infrastructure, residential, commercial, industrial, and other end-user industries (marine, etc.). The report also covers the market size and forecasts for the concrete repair mortar in 26 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Cementitious |

| Epoxy |

| Other Types |

| Spraying |

| Pouring |

| Manual |

| Infrastructure |

| Residential |

| Commercial |

| Industrial |

| Other End-user Industries (Marine, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Cementitious | |

| Epoxy | ||

| Other Types | ||

| By Application Method | Spraying | |

| Pouring | ||

| Manual | ||

| By End-user Industry | Infrastructure | |

| Residential | ||

| Commercial | ||

| Industrial | ||

| Other End-user Industries (Marine, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the concrete repair mortar market?

The concrete repair mortar market stands at USD 2.65 billion in 2026 and is forecast to reach USD 3.50 billion by 2031 at a 5.66% CAGR.

Which region shows the fastest growth for concrete repair mortars?

Asia-Pacific leads with a projected 6.32% CAGR through 2031, buoyed by highway and metro-rail rehabilitation in China, India, and Southeast Asia.

Why are polymer-modified mortars gaining share?

Latex or acrylic modifiers improve bond strength, cut permeability, and allow thin repairs, delivering payback within five years on high-traffic assets.

How do VOC regulations affect product selection?

Caps such as California’s 250 g/L limit shift demand toward water-based or low-solvent epoxies, lengthening cure times but ensuring regulatory compliance.