High Speed Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

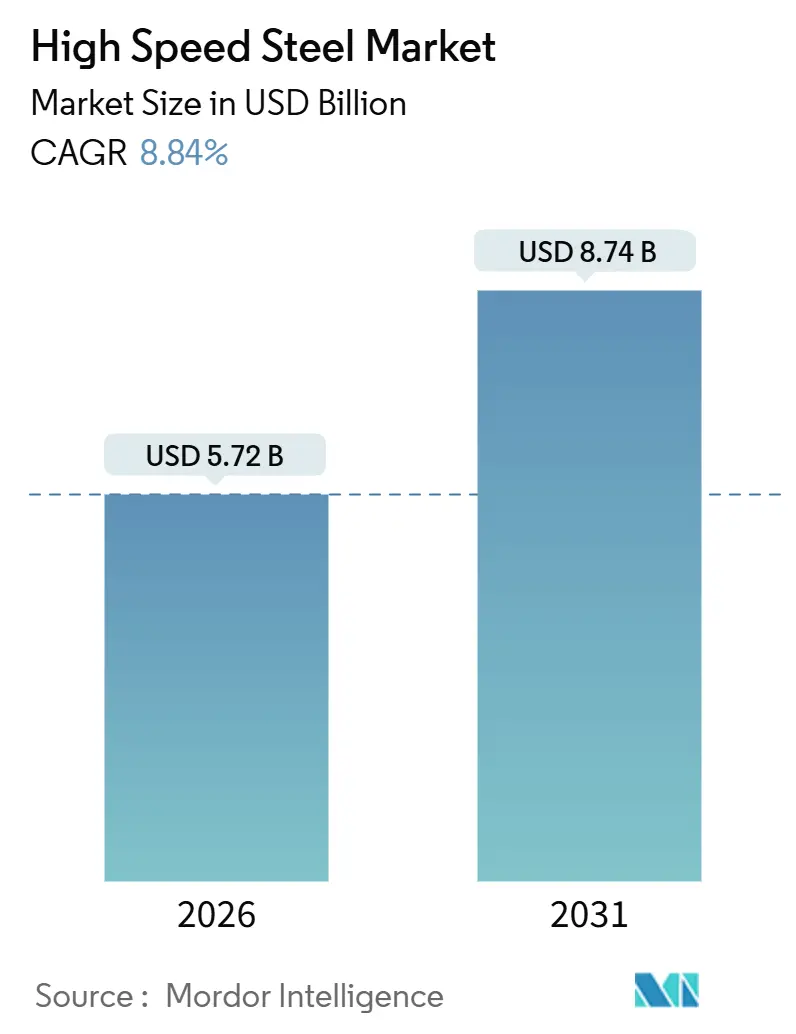

| Market Size (2026) | USD 5.72 Billion |

| Market Size (2031) | USD 8.74 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Speed Steel Market Analysis by Mordor Intelligence

The High Speed Steel Market size is estimated at USD 5.72 billion in 2026, and is expected to reach USD 8.74 billion by 2031, at a CAGR of 8.84% during the forecast period (2026-2031). Robust procurement linked to electric-vehicle component machining, sustained aerospace engine production, and the rapid spread of Industry 4.0 automation continue to amplify tool-consumption rates. Manufacturers favor molybdenum-rich compositions because they retain hot hardness above 600 °C while avoiding the price swings attached to tungsten, helping the high-speed steel market preserve a cost-performance edge in medium-speed operations. Surging demand for powder-metallurgy grades that extend tool life further protects the share against carbide encroachment. A parallel push for closed-loop tungsten recycling adds supply security benefits that resonate with buyers exposed to input-cost volatility.

Key Report Takeaways

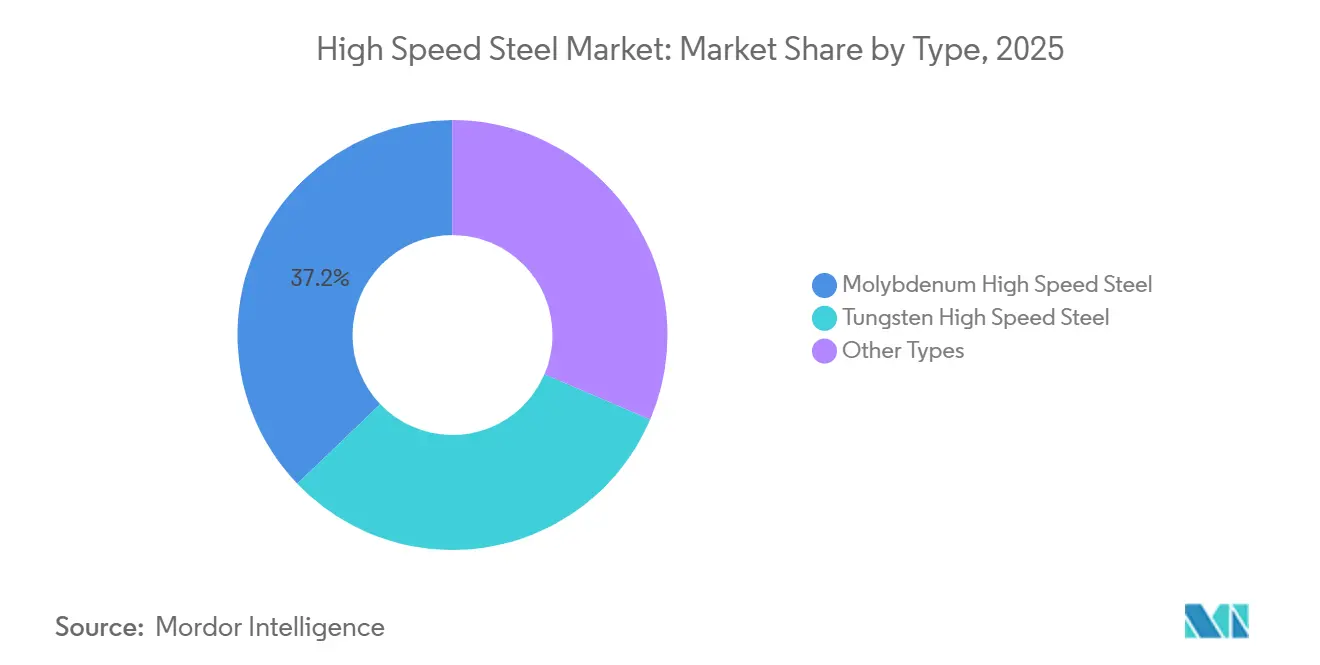

- By type, molybdenum grades captured 37.16% of 2025 revenue and are advancing at a 9.43% CAGR, the fastest across all compositions, within the high-speed steel market.

- By product type, metal cutting tools led with 53.76% of 2025 revenue, while the segment is expanding at a 9.59% CAGR, the quickest among product groups.

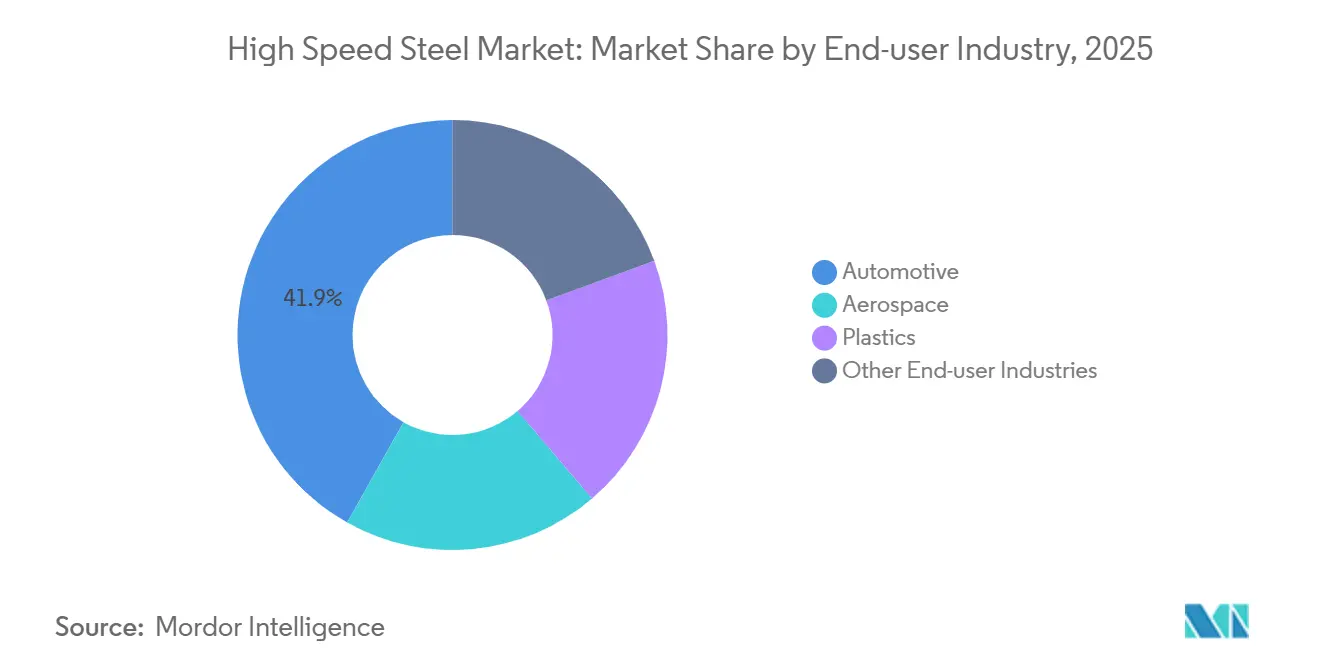

- By end-user, automotive machining held 41.85% of 2025 demand and is growing at a 9.38% CAGR, the highest among consuming industries.

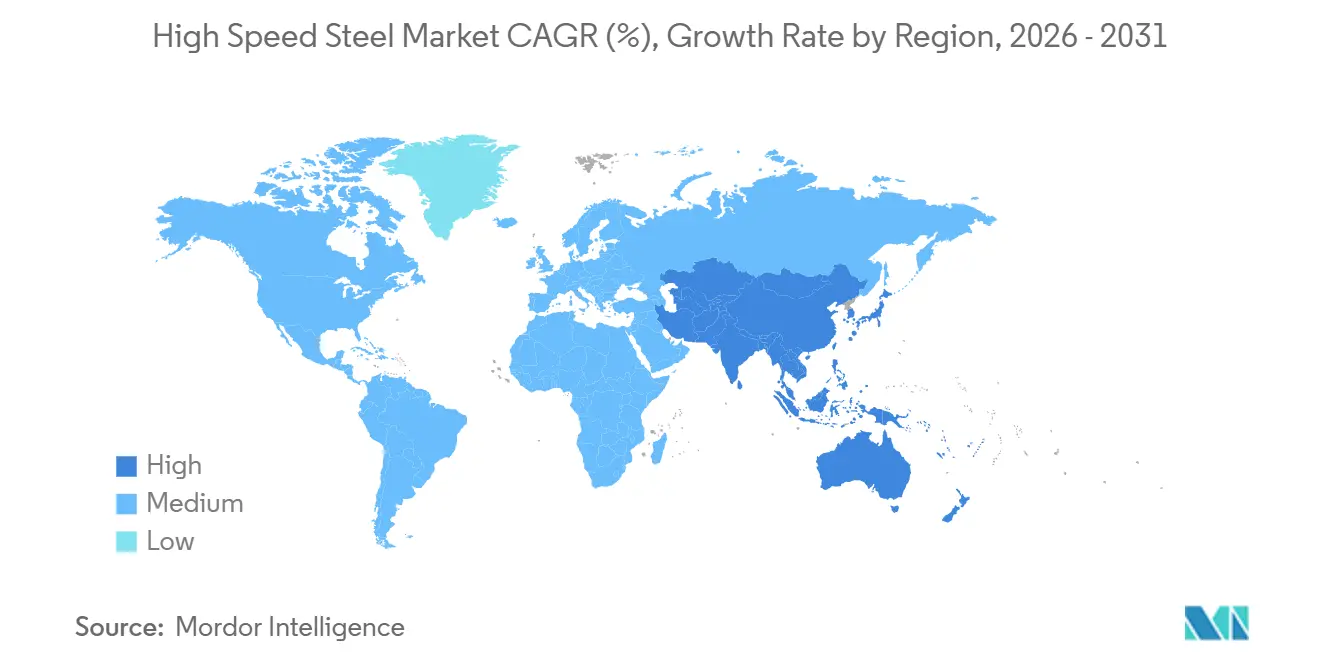

- By geography, Asia-Pacific commanded 64.28% of global revenue in 2025 and is expanding at a 9.34% CAGR, outpacing every other regional cluster.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Speed Steel Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of EV-driven automotive machining demand | +2.3% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rising aerospace engine and air-frame tooling needs | +1.8% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Automation and Industry 4.0 boosting tool-change frequency | +2.1% | Global, led by Germany, Japan, South Korea | Short term (≤ 2 years) |

| Powder-metallurgy HSS grades extending tool life | +1.6% | Global, concentrated in advanced manufacturing hubs | Medium term (2-4 years) |

| Circular-economy push for tungsten recycling | +1.0% | North America and EU, regulatory-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of EV Driven Automotive Machining Demand

As battery-electric vehicle production surges, tolerance bands are tightening below 50 µm. This shift leads to quicker tool wear and a significant uptick in drill and end-mill turnover. In tandem, Tesla ramped up its cutting tool procurement during its plant expansions in Texas and Berlin[1]Tesla Inc., “Annual Report 2025,” ir.tesla.com. Meanwhile, the Chinese Ministry of Industry and Information Technology reported an increase in new-energy vehicle production. Such production volumes favor molybdenum grades, which maintain hardness at 550–600 °C without incurring the cobalt premium. This preference bolsters the continuous growth of the high-speed steel market.

Rising Aerospace Engine and Air Frame Tooling Needs

Boeing reported a commercial backlog in its 2025 filing, while Airbus announced it has orders pending delivery. The high-speed steel market remains resilient against a complete shift to carbide, as secondary drilling and reaming on titanium shells still depend on the toughness of high-speed steel. Pratt & Whitney, citing the heightened risk of carbide fractures under vibratory loads, continues to use high-speed steel form tools for finishing fir-tree slots.

Automation and Industry 4.0 Boosting Tool Change Frequency

Operators, using predictive maintenance systems in connected machining centers, boosted tool-change counts, replacing cutters before any dimensional drift occurred. In 2025, Germany’s Federal Economic Ministry reported widespread adoption of Industry 4.0 among medium-sized manufacturers, highlighting real-time tool monitoring as a leading application. Japanese CNC builders noted increased tool consumption per output unit compared to 2023, creating expanded opportunities in the high-speed steel market, particularly for predictable powder-metallurgy grades.

Powder Metallurgy High Speed Steel Grades Extending Tool Life

Erasteel announced that its new PM grades, Rockwell C 67–69, offer a longer lifespan than their ingot-cast counterparts. Academic studies highlighted that nitrogen-alloyed PM high-speed steel boasts superior transverse rupture strength compared to M2. Sandvik, by combining PM substrates with AlCrN coatings, realized an extension in mold-steel milling life. Such advancements bolster buyer loyalty, especially those weighing cost against uptime in the high-speed steel market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward carbide and ceramic substitutes | -1.9% | Global, concentrated in aerospace and high-speed machining | Short term (≤ 2 years) |

| Volatile tungsten and molybdenum input prices | -1.2% | Global, acute in regions dependent on Chinese supply | Medium term (2-4 years) |

| 3D-printed carbide tools shortening HSS life-cycle | -0.8% | North America and Europe, early adoption phase | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Carbide and Ceramic Substitutes

In 2024 trials, ceramic inserts outlasted coated high-speed steel when milling Inconel 718[2]International Journal of Machine Tools and Manufacture, “Ceramic Insert Performance in Superalloy Machining,” sciencedirect.com . GE Aerospace's 2025 supplier guide has eliminated high-speed steel from many aerospace operations, mandating carbide or CBN for all primary cuts. Sandvik revealed growth in carbide insert sales in 2024, underscoring a notable shift in market share.

Volatile Tungsten and Molybdenum Input Prices

In 2024-2025, tungsten prices on the London Metal Exchange fluctuated, compressing producer margins. Molybdenum oxide prices swung significantly within a year, forcing higher raw-material inventory carries that pressured smaller mills. China still manages more than 80% of global tungsten refining capacity, and environmental audits in 2024 curtailed Jiangxi output, adding price risk for high-speed steel market participants.

Segment Analysis

By Type, Molybdenum Grades Outperform

Molybdenum compositions held 37.16% of 2025 revenue, and the cohort is set for a 9.43% CAGR through 2031. This positions molybdenum grades as the fastest-growing segment in the high-speed steel market, outpacing all rival alloys. Buyers remain loyal, drawn by cost advantages over tungsten blends and consistent performance up to 600 °C. The powder-metallurgy processing technique, which disperses fine carbides, enhances toughness and grindability. While tungsten grades maintain a niche for temperatures exceeding 650 °C, their rising prices limit broader adoption. Meanwhile, cobalt-enriched alloys find their place in high-speed gear hobbing and broaching, where they offer added red-hardness for intermittent loads.

In response to price fluctuations in tungsten during 2024-2025, OEMs shifted their focus to molybdenum variants. Proterial's M42 cobalt-molybdenum product achieved high Rockwell C hardness, boasting a significant cost advantage over the tungsten-rich T15. Meanwhile, Chinese producer Tiangong recorded notable sales growth in molybdenum high-speed steel in 2024, predominantly catering to automotive tiers in China and India, solidifying its leadership in the high-speed steel arena.

Note: Segment shares of all individual segments available upon report purchase

By Product Type, Metal Cutting Tools Dominate

Metal cutting tools secured 53.76% of 2025 revenue and will climb at a 9.59% CAGR, the swiftest among product groups. This share equates to the largest slice of the high-speed steel market size in value terms. Electric-vehicle battery enclosures require dense drilling patterns and repeated reaming, lifting twist-drill turnover. ISO 3685 tool-life standardization simplifies procurement comparisons, prompting buyers to balance unit cost against cycle time. Cold working tools, spanning punches and shear blades, benefit from PM microstructures that extend die life. Other product types, such as gear hobs, remain niche yet vital for precision transmission manufacturing.

As Industry 4.0 takes hold, metal-cutting consumption sees a significant uptick. Sandvik highlighted that in Mexico and Thailand, suppliers using automatic tool changers consumed more high-speed steel drills for each vehicle produced, compared to their semi-automated counterparts. Additionally, cold-working tools are benefiting from advanced carbides, which can withstand high press tonnage without chipping, proving advantageous for appliance and HVAC stamping.

By End-User, Automotive Remains in Front

Automotive machining accounted for 41.85% of 2025 demand and will advance at a 9.38% CAGR. The market share of high-speed steel in the automotive sector remains unparalleled, driven by an increase in machining intensity due to battery-electric architectures. In 2025, China rolled out a substantial number of new-energy vehicles, with consumption heavily centered in the Jiangsu and Zhejiang clusters. The aerospace sector continues to prioritize toughness over peak speed in its secondary titanium operations. In plastics processing, high-speed steel molds face challenges in tool life due to abrasion from fillers. Meanwhile, the mining sector utilizes hybrid HSS-carbide bits, capitalizing on the toughness of the HSS shank and the hardness of carbide edges.

Tesla's expansion in 2025 and its European EV rollout spurred a notable year-on-year increase in tooling demand at each plant, underscoring the close relationship between EV production and the growth of the high-speed steel market. Demand in the aerospace sector is bolstered by substantial backlogs at Boeing and Airbus, coupled with ramped-up production from Pratt & Whitney engines, ensuring a steady flow of tooling despite pressures from carbide sources.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific generated 64.28% of global revenue in 2025 and is forecast to grow at a 9.34% CAGR to 2031. As a result, the high-speed steel market in Asia-Pacific is set to outpace all other regions in growth. In 2024, China, primarily from its Jiangsu and Zhejiang hubs, was responsible for a substantial portion of global cutting tool production. Meanwhile, India drew in considerable foreign manufacturing investments in 2025, directing a significant portion of these orders to local tool suppliers. Japan continues to lead in precision, and South Korea's machine-tool output surged in 2025, driven by investments in semiconductors and automotive sectors, further solidifying the region's dominance.

North America and Europe together accounted for a notable share of the 2025 market value. Boeing's substantial backlog, alongside Pratt & Whitney's turbine initiatives, underscores the stronghold of high-speed steel in secondary aerospace applications. In 2025, Germany boasted a robust machine-tool output, with a notable uptick in cutting-tool consumption. The EU's Critical Raw Materials Act, aimed at boosting tungsten recycling, saw voestalpine successfully recover a significant amount from scrap in 2024, bolstering the region's supply chains.

South America, along with the Middle East and Africa, accounted for the remaining share of the market. In 2025, Vale invested heavily in upgrading mine equipment, which prominently featured machining centers utilizing high-speed steel tooling. Saudi Arabia's Public Investment Fund, in 2025, allocated substantial resources towards advanced manufacturing projects, including a joint venture eyeing domestic high-speed steel production. Despite facing import competition, South Africa's vehicle production in 2025 bolstered the demand for local cutting tools.

Competitive Landscape

The high-speed steel market is partially fragmented. Powder-metallurgy know-how and closed-loop tungsten recycling separate leaders from regional mills. Emerging challengers leverage additive manufacturing. Smaller regional players win on agility through rapid regrind services and custom profiles, particularly for niche aerospace fixtures and specialized mining tools. Consolidation remains selective, focusing on specialty alloys and distribution networks rather than large-scale mergers, indicating the importance of technology differentiation and customer proximity.

High Speed Steel Industry Leaders

Sandvik AB

ArcelorMittal

voestalpine BÖHLER Edelstahl GmbH & Co KG

Proterial, Ltd.

CRS Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Erasteel acquired select Crucible Industries assets to expand powder-metallurgy high-speed steel production in the United States, strengthening its local tooling and aerospace customer base.

- June 2024: Erasteel secured Environmental Product Declaration certification for conventional and recycled high-speed steel grades, the first in the sector to achieve verified life-cycle transparency.

Global High Speed Steel Market Report Scope

High-speed steel (HSS) is an alloy steel that incorporates tungsten and the alloying element vanadium for enhanced strength. High-speed steel is frequently used for metal cutting and woodturning because of its high wear resistance, hard work, and shock absorption, making it durable and precise.

The high-speed steel (HSS) market is segmented by type, product type, end-user industry, and geography. By type, the market is segmented into tungsten high-speed steel, molybdenum high-speed steel, and other types (cobalt high-speed steel, chromium high-speed steel, and vanadium high-speed steel). By product type, the market is segmented into metal-cutting tools, cold-working tools, and other product types (milling tools, drilling tools, etc.). By end-user industry, the market is segmented into automotive, aerospace, plastics, and other end-user industries (mining, manufacturing, tool making, etc). The report also covers the market size and forecasts in 27 countries across major regions. For each segment, market sizing and forecasts were made on the basis of value (USD).

| Tungsten High Speed Steel |

| Molybdenum High Speed Steel |

| Other Types (Cobalt High-Speed Steel, Chromium High-Speed Steel, and Vanadium High-Speed Steel) |

| Metal Cutting Tools |

| Cold Working Tools |

| Other Product Types (Milling Tools, Drilling Tools, etc.) |

| Automotive |

| Aerospace |

| Plastics |

| Other End-user Industries (Mining, Manufacturing, Tool Making, etc) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Qatar | |

| Egypt | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Type | Tungsten High Speed Steel | |

| Molybdenum High Speed Steel | ||

| Other Types (Cobalt High-Speed Steel, Chromium High-Speed Steel, and Vanadium High-Speed Steel) | ||

| By Product Type | Metal Cutting Tools | |

| Cold Working Tools | ||

| Other Product Types (Milling Tools, Drilling Tools, etc.) | ||

| By End-user Industry | Automotive | |

| Aerospace | ||

| Plastics | ||

| Other End-user Industries (Mining, Manufacturing, Tool Making, etc) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Qatar | ||

| Egypt | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the high-speed steel market by 2031?

The market is forecast to reach USD 8.74 billion by 2031 based on an 8.84% CAGR, from USD 5.72 billion in 2026.

Which alloy type is expanding the fastest?

Molybdenum grades are growing at a 9.43% CAGR through 2031 due to a favorable cost-performance balance.

Why does Asia-Pacific dominate demand?

The region hosts the majority of cutting tool production and large EV and electronics manufacturing bases, driving 64.28% of 2025 revenue.

How is Industry 4.0 influencing tool consumption?

Predictive maintenance raises tool-change frequency, increasing demand for predictable powder-metallurgy grades.

What supply risks affect producers?

Price volatility tied to tungsten and molybdenum, and concentration of tungsten refining in China, pressure margins, and planning.