Polyester Staple Fiber (PSF) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 36.18 Billion |

| Market Size (2031) | USD 45.56 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyester Staple Fiber (PSF) Market Analysis by Mordor Intelligence

The Polyester Staple Fiber Market size is expected to increase from USD 34.67 billion in 2025 to USD 36.18 billion in 2026 and reach USD 45.56 billion by 2031, growing at a CAGR of 4.72% over 2026-2031. Cost-performance advantages over cotton, soaring demand for non-woven hygiene products, and an accelerating pivot to lightweight automotive acoustics continue to reinforce the economic case for PSF. Recycled volumes are scaling yet remain feedstock-constrained, keeping virgin fiber dominant even as global brands commit to circularity targets. Asia-Pacific’s integrated PTA-to-fiber chains anchor global cost leadership, but environmental regulations in Europe and North America are reshaping trade flows toward locally produced, low-shedding, and chemically recycled grades. Competitive intensity is rising as China’s top producers, Reliance Industries, and integrated recyclers expand capacity and push downstream into specialty segments.

Key Report Takeaways

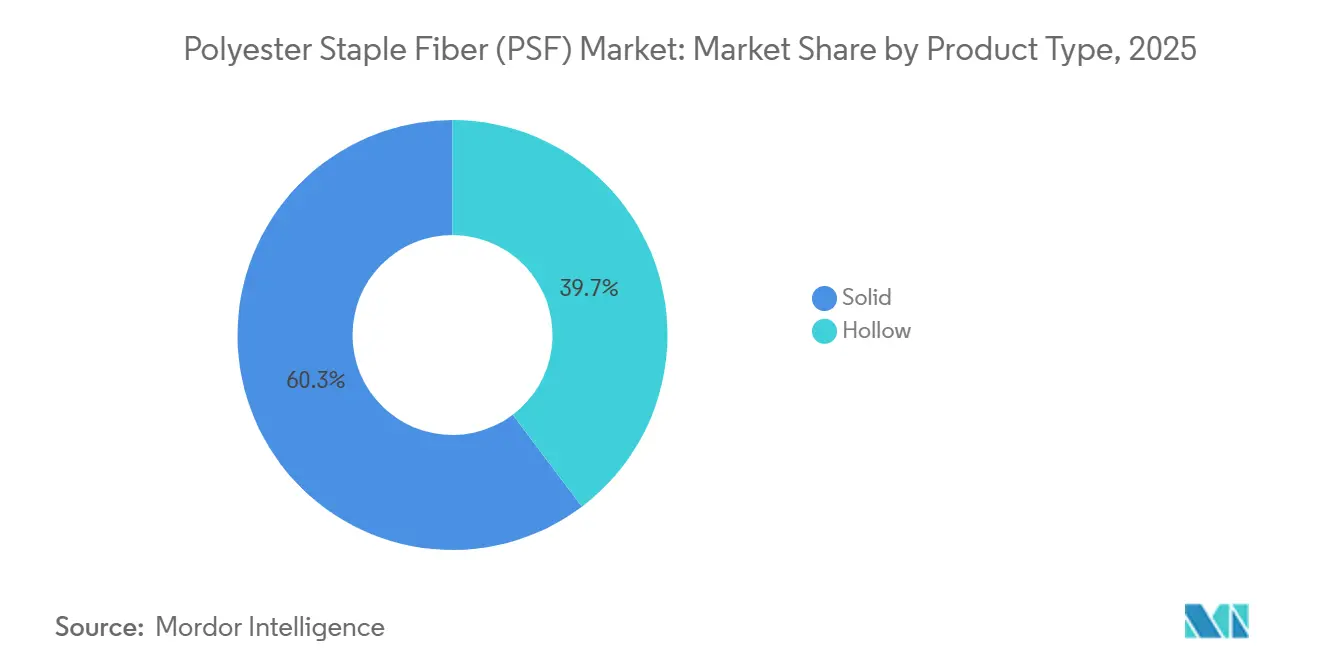

- By product type, solid fibers held 60.28% of the polyester staple fiber market share in 2025, while hollow fibers are forecast to expand at a 5.86% CAGR through 2031.

- By origin, virgin grades accounted for 63.44% of the polyester staple fiber market size in 2025; recycled grades are the fastest-growing segment at a 4.92% CAGR between 2026-2031.

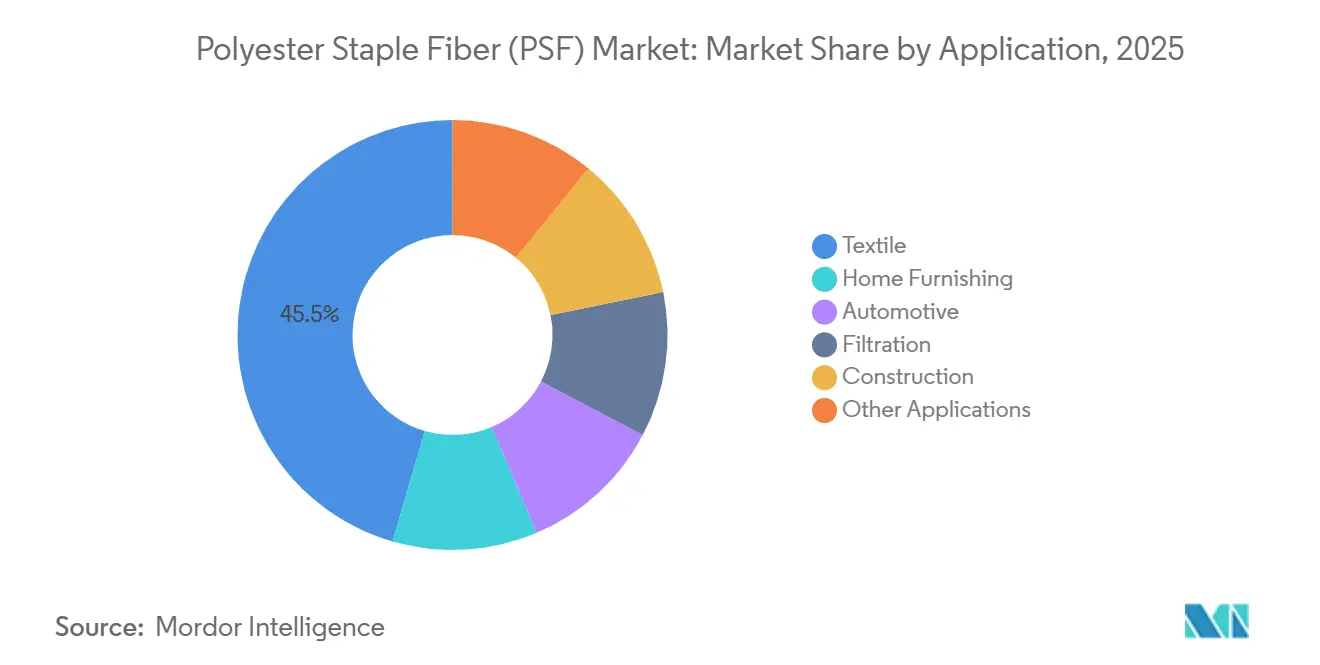

- By application, textiles dominated with a 45.51% share in 2025; automotive uses are projected to grow at a 5.35% CAGR to 2031.

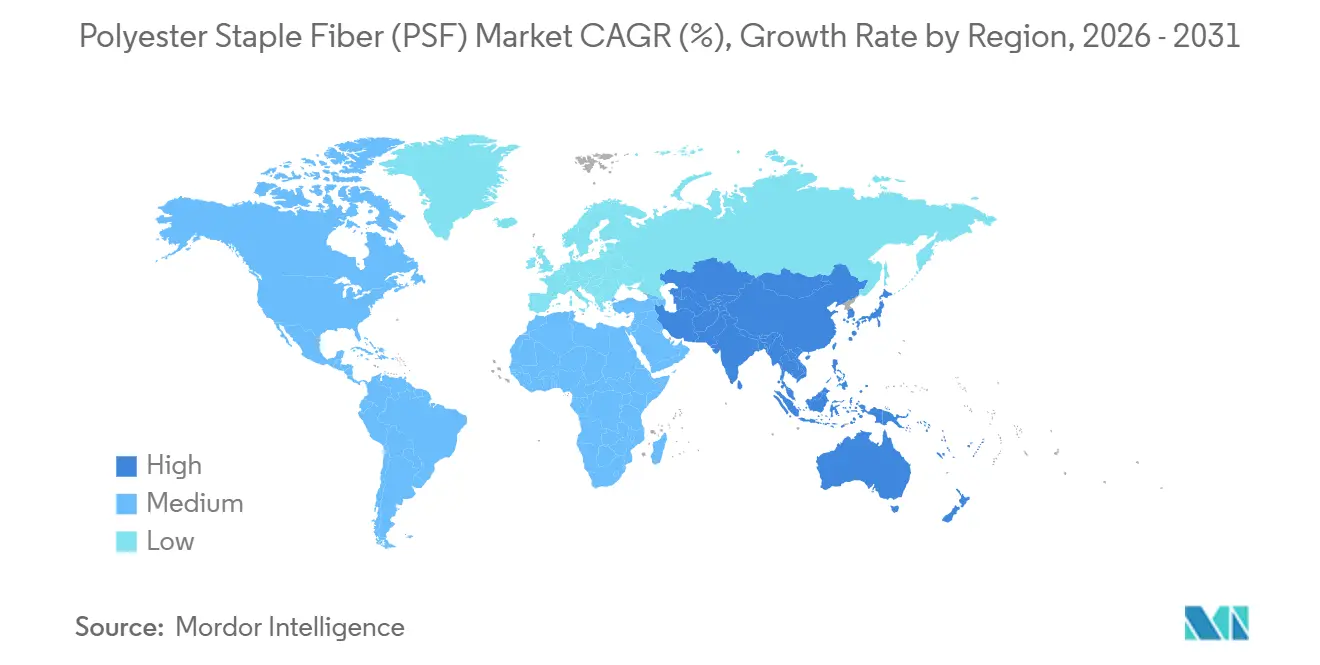

- By geography, Asia-Pacific commanded 73.65% of global volume in 2025 and is expected to register the highest regional CAGR of 5.44% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyester Staple Fiber (PSF) Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for recycled PSF from fast-fashion brands | +1.2% | Global, concentrated in Europe, North America, and Asia-Pacific brand supply chains | Medium term (2-4 years) |

| Expansion of non-woven hygiene capacity in Southeast Asia | +0.9% | ASEAN core (Vietnam, Indonesia, Thailand), spill-over to South Asia | Short term (≤ 2 years) |

| Substitution of cotton with polyester amid raw-cotton price volatility | +0.8% | Global, acute in South Asia and China textile hubs | Medium term (2-4 years) |

| Lightweight, low-noise NVH components boost automotive PSF use | +0.7% | North America, Europe, China EV manufacturing clusters | Long term (≥ 4 years) |

| Rapid growth of fiber-reinforced 3D printed concrete panels | +0.3% | North America, Europe, Middle East construction markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Recycled PSF from Fast-Fashion Brands

Brand commitments to boost recycled content are now solidifying into multi-year contracts, with rPSF prices sitting higher than virgin fiber[1]Textile Exchange, “Recycled Polyester Guidelines v1.0,” TextileExchange.org. H&M, hitting recycled polyester in 2024, backed Syre with an investment to scale up chemical recycling. Far Eastern Group expanded its rPET capacity, but with most of its recycled input sourced from bottles, it's facing heightened competition from the packaging sector for feedstock. Indorama's collaboration with Jiaren Chemical is set to introduce additional capacity for textile-to-textile processing, underscoring the growing importance of depolymerization in achieving a closed-loop system. Meanwhile, new guidelines from ZDHC in 2024 tighten controls on wastewater and chemicals, creating steeper capital challenges for smaller recyclers and favoring market consolidation among integrated players.

Expansion of Non-Woven Hygiene Capacity in Southeast Asia

Non-woven investments are shifting from coastal China to Vietnam, Indonesia, and Thailand, driven by lower labor costs, preferential trade corridors, and increasing regional diaper penetration[2]Office of Industrial Economics Thailand, “Industrial Economics Status 2024 and Outlook 2025,” Oie.go.th. Thailand's output of man-made fibers saw growth in 2024. Meanwhile, Sinopec Yizheng's benchmark zero-VOC melt-direct line is setting the standard for new plants in ASEAN. Data from EDANA and INDA highlight that hygiene non-wovens now represent a significant portion of the global volume. Additionally, the tensile strength and absorbency of PSF make it the preferred fiber for both core and acquisition layers. With India’s diaper market on the rise, local off-take is bolstered, paving the way for double-digit capacity expansions until 2027. Furthermore, logistics savings from avoiding long-haul exports enhance project economics, solidifying ASEAN's position as the emerging hub for hygiene-grade PSF.

Substitution of Cotton with Polyester Amid Raw-Cotton Price Volatility

In 2023, cotton's market share dipped, while polyester dominated with a commanding share of global fiber production. Weather-related harvest disruptions and dwindling stocks have led to price surges, squeezing spinner margins and hastening the industry's pivot towards polyester-rich blends for their cost predictability. India's Production-Linked Incentive scheme is now backing man-made fiber capacity, accelerating the shift to Polyester Staple Fiber (PSF) in both spinning and weaving. Polyester's superior moisture regain and dimensional stability make it the preferred choice for technical textiles, outshining cotton. With the expansion of integrated PTA-MEG complexes, the unit cost of polyester is on a downward trajectory, further amplifying the price disparity and solidifying its dominance in both apparel and home textiles.

Lightweight, Low-Noise NVH Components Boost Automotive PSF Use

Hollow PSF is helping automakers achieve both cabin quietness and weight reduction. These air cores cut density, reducing mass significantly, and achieve noise-reduction coefficients above 0.6 in the 500–2,000 Hz band. In electric vehicles, every kilogram saved not only extends the range but also offsets battery costs. Hailide, a Chinese supplier with a significant global share in tire-cord fabric, is using OEM certifications to promote its hollow NVH grades. Their low-melting-point variants allow for quick thermoforming of interior composites in under 60 seconds, perfectly suiting the fast-paced EV production cycles. With sustained EV adoption in the U.S., Europe, and China, there is a steady demand for performance PSF grades.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price swings linked to crude-oil volatility | -0.9% | Global, acute in import-dependent regions (Europe, Southeast Asia) | Short term (≤ 2 years) |

| Anti-dumping duties on PSF in the United States and EU | -0.5% | North America, Europe; affects exporters in China, India, Vietnam | Medium term (2-4 years) |

| Tightened EU microplastic shedding legislation | -0.4% | Europe, with compliance spillover to global brands sourcing EU-bound textiles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Swings Linked to Crude-Oil Volatility

In 2025, as crude-linked paraxylene costs surged faster than fiber prices, PTA and MEG margins took a sharp hit. This led to the closure of several PTA units in China. Europe and ASEAN, both heavily reliant on imports, grappled with higher feedstock prices compared to China's integrated refineries. This disparity not only diminished their competitiveness but also hastened a wave of rationalization. In response to the shifting market dynamics, Indorama closed its Canadian PTA plant, and Alpek paused its Cedar Creek rPET operations, both actions taken as profit spreads turned negative. While China's Ministry of Industry has advocated for capacity discipline, the global landscape tells a different story: with a significant nameplate capacity for PET, a structural oversupply looms large. Furthermore, the erratic nature of feedstock costs casts a shadow over long-term contracts, complicating capital-planning visibility throughout the PSF chain.

Anti-Dumping Duties on PSF in the United States and EU

U.S. duties on PSF imports from China and India are steering buyers away from these low-cost Asian sources. Instead, they're turning to regional suppliers or opting for pricier alternatives. Meanwhile, the European Commission is probing into Vietnamese PET imports, and there's a possibility that tariffs could be extended to staple fiber. Such a move would disrupt current re-export channels that have been sidestepping Chinese levies. Exporters are now at a crossroads, deliberating whether to invest in local production or absorb losses from tariffs. Notably, industry giants Reliance and Indorama are making strategic moves, expanding their footprint in North America and Europe. Additionally, there's a noticeable shift: more Chinese fiber is now finding its way to Africa and Latin America. These markets, however, come with their own challenges, boasting lower purchasing power and different specification levels. As trade frictions intensify, they're not just raising inventory risks but also complicating global sourcing strategies for converters downstream.

Segment Analysis

By Product Type: Hollow Fiber Gains Traction in Mobility and Insulation

In 2025, solid Polyester Staple Fiber (PSF) commanded a 60.28% share of the market, primarily driven by its applications in apparel, home furnishings, and hygiene non-wovens, where its tenacity and colorfastness are highly valued. Solid fibers, known for their resistance to pilling and prolonged compression, have seen sustained demand in blended polyester-cotton fabrics and upholstery, outpacing their natural counterparts. Meanwhile, hollow grades are climbing at a 5.86% CAGR, fueled by automakers, outdoor apparel brands, and insulation providers who prioritize weight savings and thermal efficiency. Academic studies highlight hollow polyester's thermal conductivity at approximately 0.04 W/m·K, on par with fiberglass, but without the downsides of skin irritation and moisture retention. Automotive OEMs are now turning to low-melting-point hollow variants for door-panel composites, enabling rapid vacuum-forming and aligning with electric vehicle production targets. In the construction sector, hollow batts are gaining traction, offering advantages like easier handling and mold resistance over traditional mineral wool. With the surge of electric vehicle platforms and green construction standards, the appeal of hollow PSF is set to soar, even as solid fiber maintains its volume lead through 2031.

By Origin: Recycled Volumes Rise Despite Feedstock Bottlenecks

In 2025, Virgin PSF commanded a 63.44% share of the Polyester Staple Fiber market, leveraging China's mega-complexes that benefit from integrated PTA and MEG, ensuring unmatched conversion costs. While smaller in scale, recycled variants are rising by 4.92% CAGR as brands secure long-term supply contracts to meet 2030 sustainability targets. Notably, bottle-derived rPET accounts for the majority of inputs, creating tension with the beverage industry. This dynamic has driven spot rPET premiums in Europe and North America to surpass those of virgin counterparts. Meanwhile, chemical depolymerization initiatives are striving to reduce reliance on bottles by tapping into textile waste. However, their progress is hampered by significant capital expenditures and the fluid nature of certification protocols. Blended PSF, which combines both virgin and recycled streams, serves as a cost-effective intermediary. This is particularly appealing to mid-tier apparel brands, where consumers appreciate sustainability labels but are hesitant to pay full price premiums. Looking ahead, while virgin fiber remains the go-to for performance-centric segments, recycled grades are steadily capturing a larger share of consumer spending, driven by mounting regulatory and reputational pressures.

By Application: Automotive Outpaces a Maturing Textile Base

In 2025, textiles accounted for a 45.51% share of revenue, but their volume growth is slowing due to a saturated apparel market and rising compliance costs from EU microplastic regulations. In contrast, the automotive sector is set to lead with 5.35% CAGR growth, fueled by global EV sales crossing a notable threshold and new, stringent interior noise regulations. Hollow and low-melting-point PSF grades, known for their acoustic dampening and quick thermoformability, are replacing heavier glass and PU foams. In filtration, polyester non-wovens are achieving high capture rates for PM2.5 with acceptable pressure drops, gaining market share from traditional cellulose and glass media. Thanks to infrastructure stimulus efforts in Asia and the Middle East, construction applications like geotextiles and fiber-reinforced 3D-printed concrete are on the rise. While niches such as rope, cordage, and specialty yarns are smaller, they remain significant due to polyester's inherent abrasion resistance and UV stability. As a result, the automotive sector stands out as the primary growth driver, providing a buffer against challenges faced by the textile industry.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific cemented 73.65% market share in 2025 and is on track for a 5.44% CAGR through 2031. China's polyester capacity solidifies the region's cost leadership. However, with PTA margins compressing in 2025, the government has intervened with "anti-involution" measures to prevent over-building. In India, bolstered by Production-Linked Incentives and the MITRA mega-parks, the addition of man-made spinning lines is projected to elevate the country's Polyester Staple Fiber market size over the forecast period. Meanwhile, Thailand, Vietnam, and Indonesia are capitalizing on non-woven hygiene investments, shifting from pricier China. They benefit from lower energy tariffs and trade corridors with ASEAN-U.S./EU, ensuring robust offtake. Japan and South Korea are honing in on high-performance fibers, as evidenced by Toray's capex in Korea, signaling a shift towards premium-margin carbon and aramid grades over the commodity PSF.

North America, under the protective umbrella of anti-dumping measures, is reshaping its supply chain. While these shields bolster domestic producers, they also create a dependency, necessitating PET imports annually to meet demand. In a strategic move, Reliance Industries and Indorama have both rolled out debottlenecking programs in the U.S., aiming to leverage tariff-induced import substitution. Across the Atlantic, Europe grapples with tightening environmental regulations. With microplastic legislation nudging buyers towards low-shedding grades and recycling innovations, local producers face pressures from soaring energy costs. Yet, Alpek's revival of its Wilton PET line, adding capacity, remains on edge due to fluctuations in paraxylene prices.

While South America and the combined regions of the Middle-East and Africa account small portion of the global volume, burgeoning infrastructure pipelines and demographic trends hint at a potential for above-average growth. In Saudi Arabia, NEOM is setting the stage, and in Dubai, 3D-print building codes are igniting an early demand for PSF-reinforced concrete. Brazil, in a strategic shift, is turning to polyester blends to buffer against cotton's volatility, a move further supported by a depreciated currency enhancing its export competitiveness. Despite trailing in per-capita fiber consumption, these emerging regions are witnessing a multi-year uplift, fueled by fiscal stimulus and urbanization.

Competitive Landscape

The polyester staple fiber (PSF) market is moderately fragmented. Smaller, unintegrated spinners increasingly differentiate via bio-based PSF blends or contract tolling for specialty hollow grades, but rising research and development and compliance costs are squeezing margins. Digitalization—AI-based process controls and predictive maintenance—offers further scale advantages to large players, widening the productivity gap. Long-term, market power gravitates toward integrated chains with captive feedstock, recycling technologies, and specialty portfolios that satisfy OEM acoustic specs or EU microplastic limits. This convergence sets the stage for mergers and acquisitions as smaller assets consolidate under larger balance sheets capable of funding greenfield recycling plants, melt-direct lines, and advanced research and development.

Polyester Staple Fiber (PSF) Industry Leaders

Indorama Corporation

Reliance Industries Limited

SINOPEC YIZHENG CHEMICAL FIBRE LIMITED

TORAY INDUSTRIES, INC.

Alpek

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Indorama Ventures Public Company Limited, a global leader in sustainable chemicals, has expanded its dejaTM fiber and filament yarn portfolio to enhance sustainability. The portfolio includes PET filament and fiber, widely used in polyester staple fiber production, aimed at supporting circularity and reducing greenhouse gas emissions.

- January 2025: Ambercycle, Inc. and Hang Zhou Benma Chemfibre and Spinning Co.,Ltd. have partnered to scale cycora staple fiber production by combining their expertise in technology scale-up. This collaboration aims to meet the rising demand for sustainable fibers while reducing reliance on virgin resources. It also addresses textile waste challenges by integrating circular materials into the Chinese value chain.

Global Polyester Staple Fiber (PSF) Market Report Scope

Polyester staple fiber (PSF) almost includes the same properties as polyester fiber, manufactured directly from MEG or PET chips and PTA or recycled PET. Virgin PSF is made of PTA and MEG or PET chips, while recycled PSF is made with PET flakes that have been recycled. PSF that is 100% virgin is usually more expensive than recycled PSF and is often more hygienic. Polyester staple fiber is often used in spinning and non-woven weaving.

The market is segmented by product type, origin, application, and geography. By product type, the market is segmented into solid and hollow. By origin, the market is segmented into virgin, blended, and recycled. By application, the market is segmented into textile, home furnishing, automotive, filtration, construction, and other applications. The report also covers the market size and forecasts in 16 countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Solid |

| Hollow |

| Virgin |

| Blended |

| Recycled |

| Textile |

| Home Furnishing |

| Automotive |

| Filtration |

| Construction |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Solid | |

| Hollow | ||

| By Origin | Virgin | |

| Blended | ||

| Recycled | ||

| By Application | Textile | |

| Home Furnishing | ||

| Automotive | ||

| Filtration | ||

| Construction | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is demand for hollow PSF growing within automotive interiors?

Hollow grades dedicated to noise-vibration-harshness components are projected to register a 5.86% CAGR through 2031, outpacing overall market growth.

What share of global PSF consumption does Asia-Pacific hold?

Asia-Pacific accounted for 73.65% of global volume in 2025 and is forecast to maintain dominance through sustained 5.44% CAGR expansion.

How are EU microplastic regulations influencing fiber development?

Brands sourcing the EU market now demand low-shedding PSF grades, pushing producers to invest in surface treatments and process controls that smaller spinners cannot easily fund.

What is the current global demand for the polyester staple fiber market and its expected growth by 2031?

Global consumption is USD 36.18 billion in 2026 and is projected to reach USD 45.56 billion by 2031, reflecting a 4.72% CAGR.