Calcium Oxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

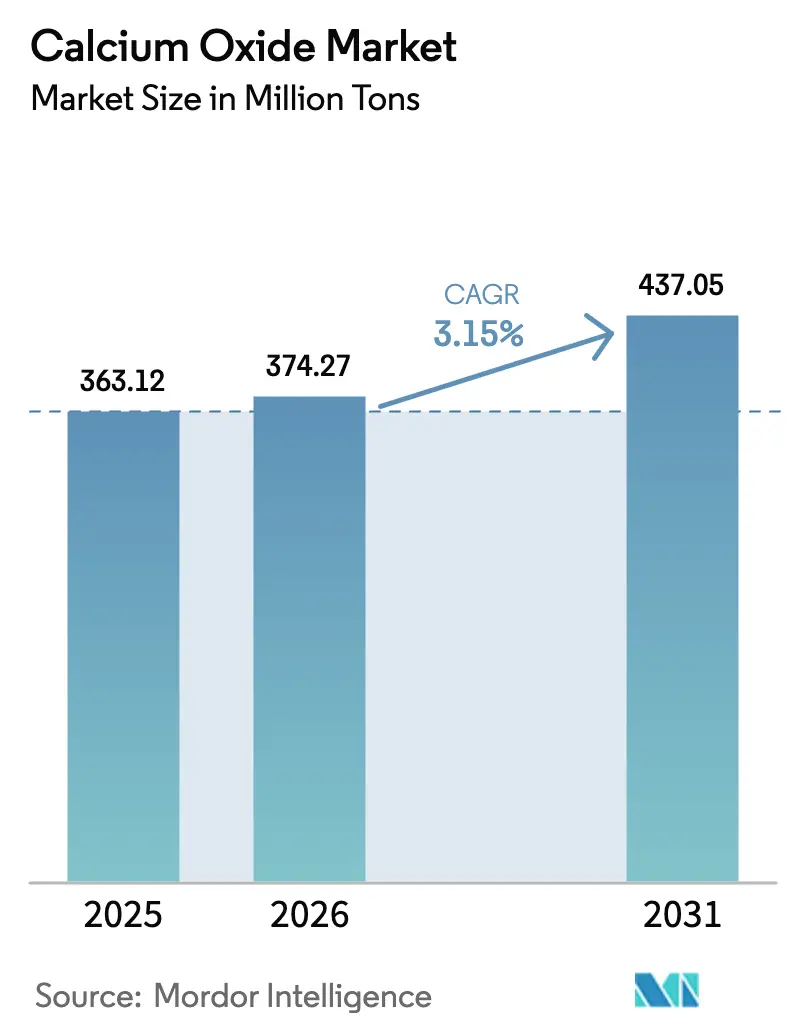

| Market Volume (2026) | 374.27 Million tons |

| Market Volume (2031) | 437.05 Million tons |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

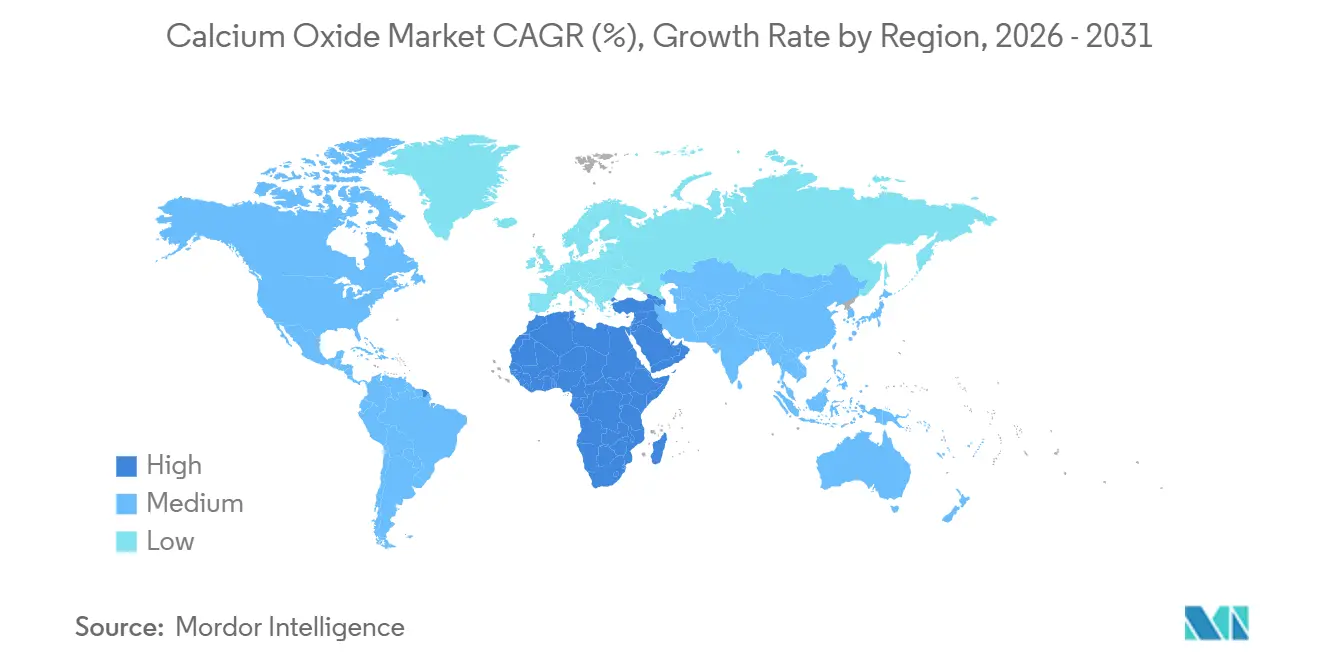

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Oxide Market Analysis by Mordor Intelligence

The Calcium Oxide Market size was valued at 363.12 Million tons in 2025 and is estimated to grow from 374.27 Million tons in 2026 to reach 437.05 Million tons by 2031, at a CAGR of 3.15% during the forecast period (2026-2031). Blast-furnace/basic-oxygen steelmaking continues to anchor demand, yet the gradual shift toward electric arc furnaces is lowering per-ton quicklime intensity even while absolute crude-steel tonnage remains high. Stricter sulfur-dioxide limits under the U.S. Clean Air Act and the EU Industrial Emissions Directive are compelling coal-fired utilities and cement kilns to retrofit flue-gas-desulfurization systems that rely on lime slurries, creating a stable compliance-driven demand pool. In parallel, low-carbon cement pilots across Europe and North America are lifting the premium segment for high-purity CaO, which trades 20-30% above commodity grades. Energy-price volatility and carbon-emission costs remain the principal headwinds, accelerating investment in carbon-capture-ready kilns and alternative fuels.

Key Report Takeaways

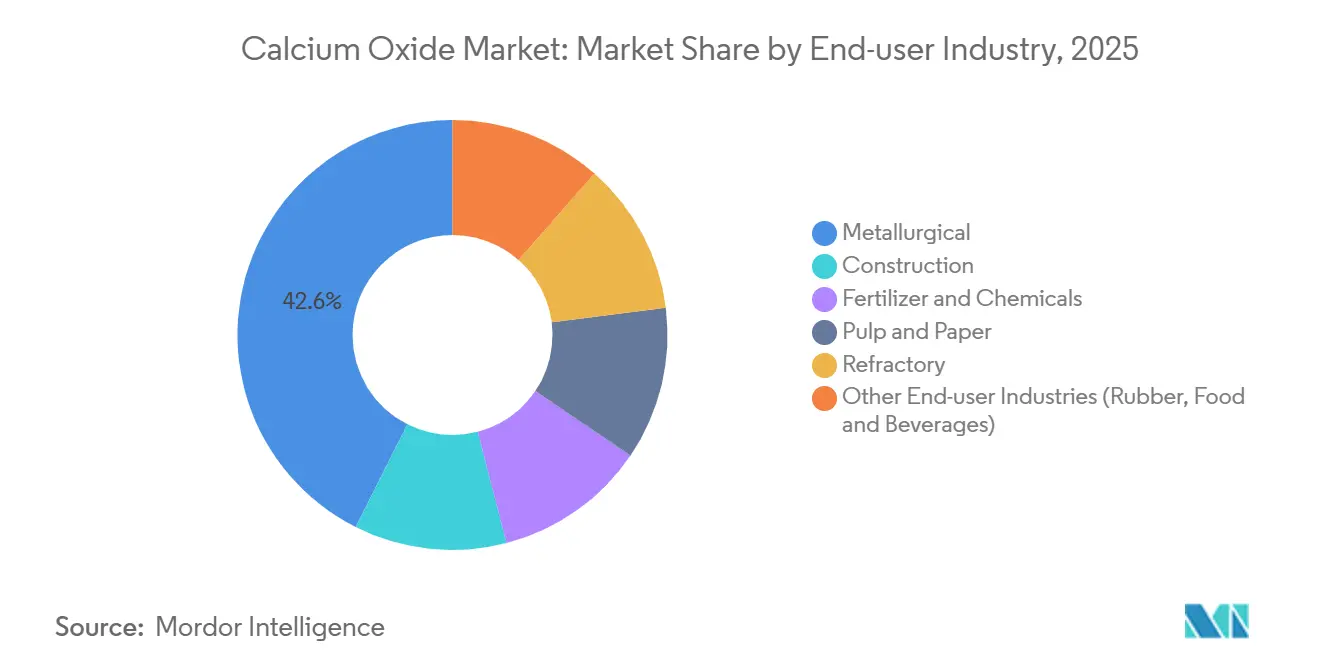

- By end-user industry, the metallurgical segment led with 42.57% of the calcium oxide market share in 2025, while the fertilizer and chemicals segment is forecast to expand at a 4.16% CAGR through 2031.

- By geography, Asia-Pacific captured 49.32% of the calcium oxide market share in 2025, while the Middle-East and Africa region is projected to post the fastest growth at 3.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Oxide Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global crude-steel output | +0.7% | APAC core (China, India, Japan), spill-over to Middle-East | Medium term (2-4 years) |

| Rapid infrastructure and cement demand in Asia-Pacific and Africa | +0.8% | APAC (India, ASEAN), Middle-East (Saudi Arabia, UAE), Sub-Saharan Africa | Long term (≥ 4 years) |

| Stricter emissions rules boosting CaO use in FGD and water treatment | +0.4% | Global, with concentration in North America, EU, and China | Short term (≤ 2 years) |

| Agricultural soil-health programs in emerging economies | +0.5% | Sub-Saharan Africa, Brazil, India, Argentina | Long term (≥ 4 years) |

| Low-carbon cement and carbon-looping technologies requiring high-purity CaO | +0.4% | EU, North America, early pilots in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Crude-Steel Output

Steel remains the single-largest consumer of calcium oxide, using 15-50 kilograms of quicklime per ton of crude steel, depending on furnace technology. China produced just over 1.0 billion tons of crude steel in 2024, a marginal decline yet still outsizing every other market. The OECD projects that 40.5% of new steel capacity through 2030 will continue to use the BF-BOF route, preserving lime intensity even as EAF penetration inches higher. India’s National Steel Policy targets 300 million tons of capacity by 2030, largely BF-BOF, effectively locking in sustained quicklime offtake. The International Energy Agency calculates that fluxes in steelmaking account for 0.3 gigatons of process CO₂ annually, underscoring the climate case for CCS-equipped kilns. Collectively, these factors underpin a demand floor for the calcium oxide market even under conservative steel-growth scenarios.

Rapid Infrastructure and Cement Demand in Asia-Pacific and Africa

Cement output reached 453 million tons in India during fiscal 2025, supported by a clinker-to-cement ratio near 0.75. Major ASEAN economies are plowing public budgets into rail, highways, and affordable housing, lifting regional cement production by 4-5% each year through 2030. Saudi Arabia’s Vision 2030 megaprojects require huge volumes of low-carbon concrete; a 5,000-ton-per-day clinker-free line at Yanbu showcases how high-purity CaO can substitute Portland clinker while cutting embodied carbon by up to 80%. In Sub-Saharan Africa, 32.7 million hectares of acid soils are depressing crop yields, spurring agricultural-lime programs that dovetail with construction growth. These converging infrastructure and agricultural initiatives reinforce a robust volume trajectory for the calcium oxide market.

Stricter Emissions Rules Boosting CaO Use in FGD and Water Treatment

Revised National Ambient Air Quality Standards in the United States and tighter SO₂ caps in the EU are forcing older coal units and cement kilns to install or upgrade lime-based scrubbers[1]U.S. Environmental Protection Agency, “Revised NAAQS for SO₂,” epa.gov . China’s Ministry of Ecology and Environment now mandates SO₂ concentrations below 50 mg/m³ for cement kilns, accelerating lime demand for desulfurization. Municipal utilities continue to rely on lime softening for pH control and phosphorus removal; the American Water Works Association notes dosing rates of 100-300 mg/L, volumes that move independently of construction and steel cycles. These regulatory levers create a relatively price-inelastic floor for the calcium oxide market.

Low-Carbon Cement and Carbon-Looping Technologies Requiring High-Purity CaO

The EU Regulation 2024/2620 recognizes mineral carbonates as permanent carbon sinks, enabling producers to claim credits when CaO reacts with CO₂ during curing. Lhoist’s EUR 250 million investment in a carbon-capture-ready dolime plant exemplifies the pivot toward CCS-equipped assets targeting one million tons of annual CO₂ sequestration by 2031. Carmeuse is piloting calcium-looping to capture kiln emissions by cycling CaO and CaCO₃ in separate reactors. All such technologies specify CaO purities above 90% to minimize inert buildup, opening a premium niche within the broader calcium oxide market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy and CO₂ costs, tightening kiln-emission limits | -0.3% | EU, North America, with emerging pressure in APAC | Short term (≤ 2 years) |

| Limestone and natural-gas price volatility | -0.2% | Global, acute in regions dependent on imported gas (EU, Japan, South Korea) | Medium term (2-4 years) |

| Alternative sorbents/fluxes gaining share in steel | -0.2% | Global steel markets, concentrated in China, EU, and North America EAF clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy and CO₂ Costs, Tightening Kiln-Emission Limits

Producing one ton of quicklime consumes 3.2-4.5 GJ of thermal energy, and natural gas can represent 60% of cash costs for gas-fired kilns. EU carbon prices near EUR 80 per ton of CO₂ translate into an additional EUR 60-70 per ton of quicklime for legacy kilns emitting roughly 0.8 tons CO₂ per ton product. Free-allowance reductions under ETS Phase IV intensify this burden each year. In the United States, emerging state-level programs and stricter New Source Performance Standards compel selective catalytic reduction and fabric-filter retrofits that raise capex without expanding capacity. Small, standalone producers find it increasingly difficult to finance such upgrades, feeding a consolidation trend in the calcium oxide market.

Limestone and Natural-Gas Price Volatility

High-grade (more than 95% CaCO₃) limestone reserves are becoming deeper and farther from transport nodes, raising haulage costs by up to 25% over the past five years[2]U.S. Geological Survey, “Mineral Commodity Summary: Lime 2025,” usgs.gov . Import dependence is acute in regions such as Japan, South Korea, and parts of the Middle-East, where freight premiums add USD 10-15 per ton to landed cost. LNG prices in Northeast Asia oscillated between USD 12 and USD 25 per MMBtu during 2024-2025, feeding unpredictable kiln costs. Alternative fuels such as biomass and hydrogen mitigate exposure but require expensive burner retrofits and, in hydrogen’s case, infrastructure that remains nascent. Volatility therefore suppresses margin visibility and slows project sanctioning in the calcium oxide market.

Segment Analysis

By End-user Industry: Metallurgical Dominance Faces Structural Headwinds

The Metallurgical segment accounted for 42.57% of calcium oxide market share in 2025, reflecting its critical function as a flux in BF-BOF steelmaking. Although the global shift toward EAF technology lowers lime intensity to 5-15 kg per ton of steel, India’s BF-centric expansion and persistent integrated capacity in China sustain absolute volume demand. Refractory-grade CaO for ladle linings commands price premiums, underpinned by quality certifications that limit new entrants.

Construction is energized by India’s 453-million-ton cement output and ASEAN’s infrastructure boom. Fertilizer and Chemicals is the fastest-expanding end-user industry, advancing at a 4.16% CAGR through 2031. Pulp and Paper mills retain stable quicklime usage of 80-120 kg per ton of pulp in kraft causticizing loops. Collectively, non-metallurgical industries provide diversification that cushions the calcium oxide market against steel-cycle volatility.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific led the calcium oxide market with 49.32% of 2025 volume, anchored by China’s massive steel and cement sectors and India’s accelerating infrastructure pipeline. Ultra-low-emission mandates for Chinese cement kilns are generating fresh demand for FGD-grade lime even as construction growth moderates. India’s government has allocated USD 1.4 trillion under its National Infrastructure Pipeline, sustaining cement capacity additions and farm-lime distribution across 10 million hectares of acid soils.

North America benefits from the Infrastructure Investment and Jobs Act, which funds highway resurfacing, bridge rehabilitation, and water-system upgrades, all of which employ CaO in asphalt modification and water-softening treatments. While the U.S. steel sector’s pivot toward EAF mini-mills reduces lime intensity, overall demand remains resilient due to automotive and appliance output. Mexico’s nearshoring-boosted construction growth prompted Grupo Calidra to expand Bajío capacity, reinforcing the regional calcium oxide market.

Europe operates under high energy costs and stringent carbon targets. Regulation 2024/2620 classifies mineral carbonates as permanent sinks, encouraging CCS-ready kilns and high-purity CaO for alkali-activated binders. Germany and France lead low-carbon cement trials, whereas Poland and Romania emphasize cost-competitive grades for steel. The Middle-East and Africa region, projected to grow at 3.98% CAGR, leverages Saudi Vision 2030 megaprojects and sub-Saharan soil-liming programs. South America’s demand hinges on Brazil’s Cerrado agriculture and Argentina’s lithium brine processing, both reliant on quicklime for pH moderation and impurity removal.

Competitive Landscape

The calcium oxide market is moderately concentrated: the top five suppliers—Lhoist, Carmeuse, Graymont, Minerals Technologies Inc., and Mississippi Lime—command roughly 45% of global capacity. Capital is flowing into carbon-abatement projects rather than greenfield tonnage. Lhoist has earmarked EUR 250 million for a carbon-capture-ready dolime plant in Belgium that will sequester one million tons of CO₂ annually once fully online in 2031. Carmeuse has partnered with a European cement major to pilot calcium-looping at a French kiln, targeting commercial rollout by 2028.

Regional challengers capitalize on logistics: CAO Industries exploits Malaysia’s proximity to ASEAN construction hubs, while Grupo Calidra leverages rail links to Mexico’s steel belt. Technology disruptors such as Hoffmann Green are licensing clinker-free cement that replaces Portland-clinker with high-purity CaO, shrinking embodied carbon by 80% and monetizing EU carbon credits. The European Patent Office registered 47 lime-decarbonization patents during 2024-2025, signaling intensified R&D race around electric kilns, oxyfuel designs, and microwave calcination. In this landscape, producers with integrated quarries, multi-fuel kilns, and early-stage CCS pilots enjoy structural cost and compliance advantages.

Calcium Oxide Industry Leaders

Carmeuse

Lhoist

Minerals Technologies Inc.

GRAYMONT

Mississippi Lime Company d/b/a MLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Pacific Lime and Cement Limited launched its calcium oxide business in Western Australia. The company provided mining customers with a high-quality and cost-effective solution, supported by an integrated supply chain delivering directly to the mine gate.

- June 2024: Grupo Calidra announced the commissioning of a new kiln at its La Laja plant in San Juan, Argentina. The kiln was the largest Maerz lime calcination kiln in the Southern Cone, with a daily production capacity of 600 tons of high-grade, high-reactivity calcium oxide, amounting to approximately 219,000 tons annually.

Global Calcium Oxide Market Report Scope

Calcium Oxide, also known as Quicklime, consists primarily of calcium and magnesium oxides. Quicklime is available in several sizes - ranging from lump and pebble lime to granular and pulverized lime.

The calcium oxide market is segmented by end-user industry and geography. By end-user industry, the market is segmented into metallurgical, construction, fertilizer and chemicals, pulp and paper, refractory, and other end-user industries (rubber, food and beverages). The report also covers the market size and forecasts for calcium oxide in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Metallurgical |

| Construction |

| Fertilizer and Chemicals |

| Pulp and Paper |

| Refractory |

| Other End-user Industries (Rubber, Food and Beverages) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By End-user Industry | Metallurgical | |

| Construction | ||

| Fertilizer and Chemicals | ||

| Pulp and Paper | ||

| Refractory | ||

| Other End-user Industries (Rubber, Food and Beverages) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the calcium oxide market?

The calcium oxide market stands at 374.27 million tons in 2026 and is projected to reach 437.05 million tons by 2031, with a 3.15% CAGR.

Which region contributes the most to global calcium oxide demand?

Asia-Pacific leads with 49.32% of 2025 volume thanks to China’s steel and India’s cement sectors.

What is driving the fastest growth in end-use demand?

Precision agriculture is lifting Fertilizer and Chemicals demand, projected to expand at 4.16% CAGR to 2031.

How are emission rules influencing calcium oxide consumption?

Stricter SO₂ caps in the U.S., EU, and China are spurring installations of lime-based flue-gas-desulfurization systems, creating a compliance-driven demand floor.