PVC Stabilizers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

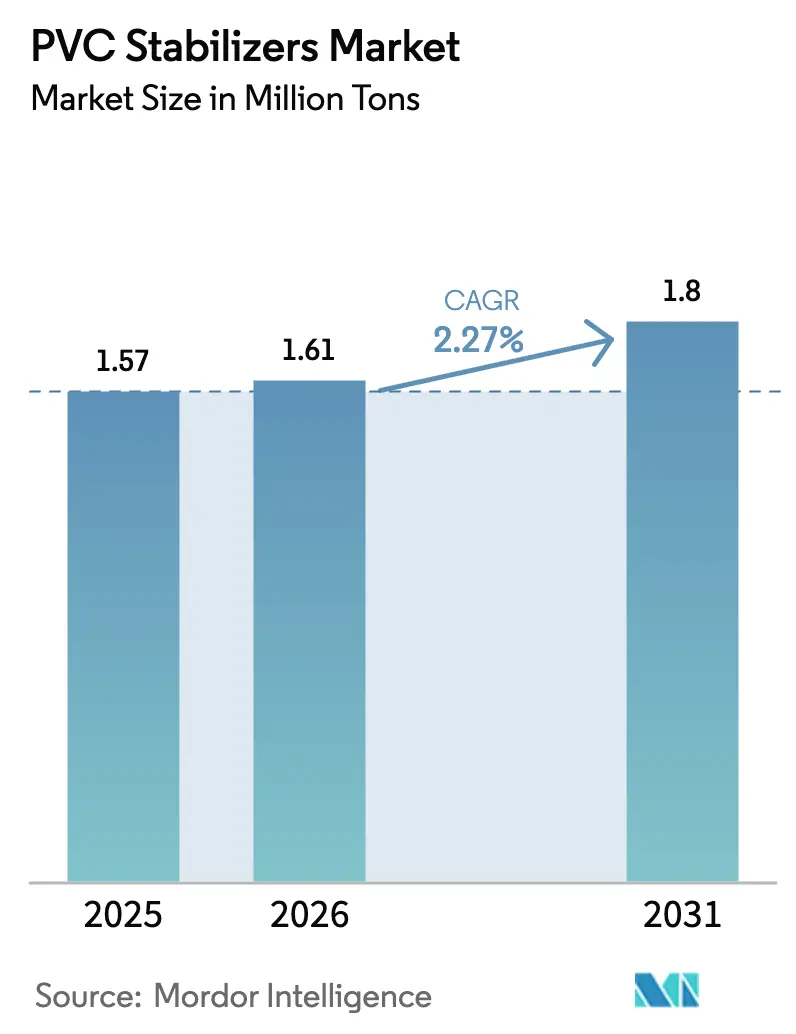

| Market Volume (2026) | 1.61 Million tons |

| Market Volume (2031) | 1.8 Million tons |

| Growth Rate (2026 - 2031) | 2.27% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PVC Stabilizers Market Analysis by Mordor Intelligence

The PVC Stabilizers Market size is expected to grow from 1.57 Million tons in 2025 to 1.61 Million tons in 2026 and is forecast to reach 1.8 Million tons by 2031 at 2.27% CAGR over 2026-2031. Regulatory mandates rather than headline volume growth now set the competitive bar, especially the European Union’s REACH and RoHS directives that continue to accelerate the global pivot away from lead-based additives. High-performance calcium-zinc and emerging organic systems allow access to export markets, medical-grade devices, and premium pipe projects but carry a higher per-kilogram cost that crimps margins when resin prices soften. Asia-Pacific overcapacity—1.9 million tons commissioned in 2025 and another 600,000 tons in 4Q 2025—drove Southeast Asian import prices to 17-year lows, further squeezing stabilizer spreads even as absolute consumption rose. Tin volatility (USD 14.20 per pound in 2024, +13% YoY) widened the cost gap between organotin grades and mixed-metal alternatives, hastening substitution in pipe, cable, and flooring applications. Recycled PVC streams promoted by VinylPlus now require 15-25% higher stabilizer loadings to offset thermal degradation, creating a secondary growth vector for premium blends.

Key Report Takeaways

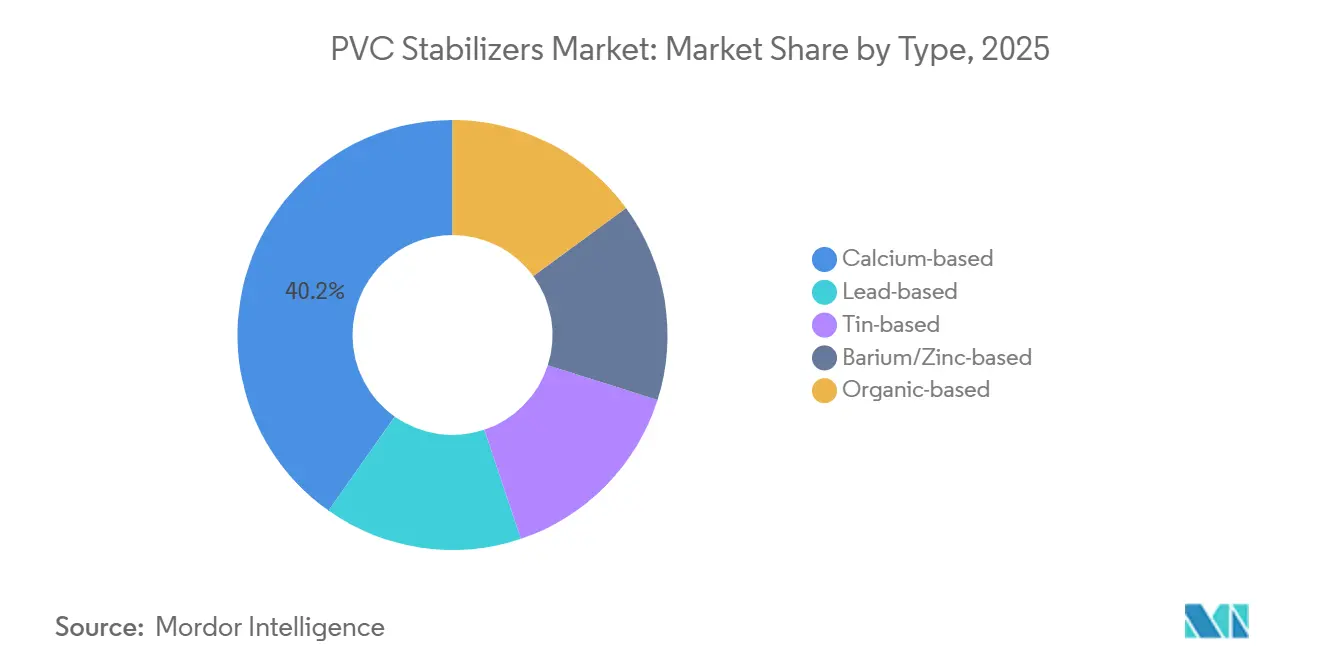

- By type, calcium-based led with 40.22% of PVC stabilizer market share in 2025, while organic-based are forecast to post the fastest growth at a 2.77% CAGR through 2031.

- By form, solid accounted for 69.59% of PVC stabilizer market size in 2025; liquid show a 2.35% CAGR to 2031.

- By application, pipes and fittings held 37.99% volume in 2025, whereas flooring and wall coverings will advance at 2.51% CAGR through 2031.

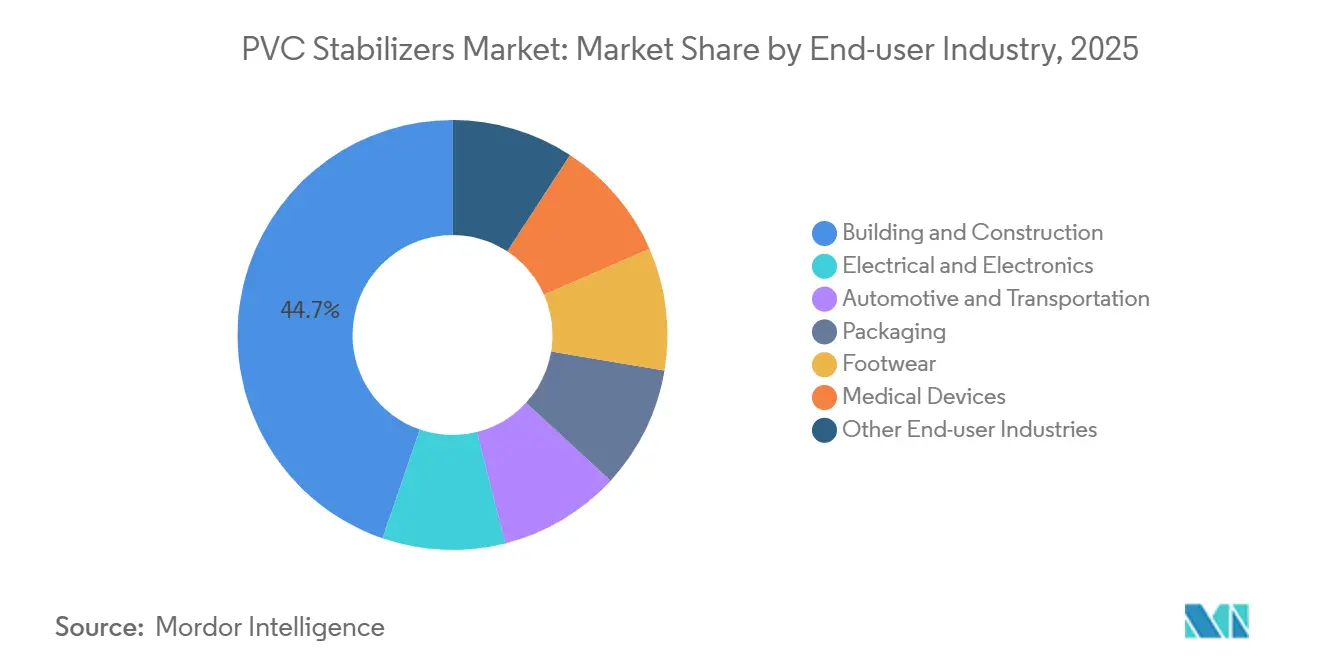

- By end-user industry, building and construction dominated with 44.72% in 2025; medical devices record the highest projected CAGR at 2.59% to 2031.

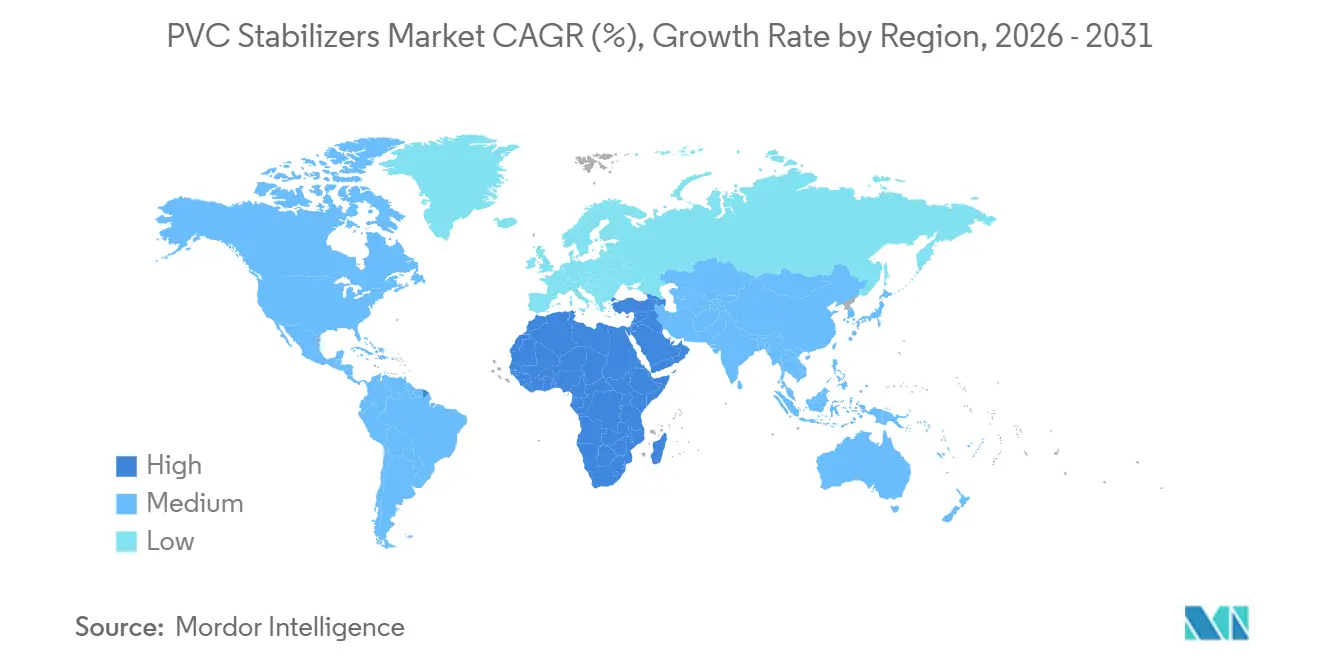

- By geography, Asia-Pacific led with 51.56% in 2025; while Middle-East and Africa record the highest projected CAGR at 2.36% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PVC Stabilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand Surge from PVC Pipes and Fittings | +0.8% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Regulatory Shift to Ca/Zn Stabilizers | +0.6% | Europe and North America, cascading to export-oriented Asia producers | Long term (≥ 4 years) |

| Rising PVC Use in Lightweight Automotive Parts | +0.3% | North America, Europe, China | Medium term (2-4 years) |

| Construction Boom in Emerging Economies | +0.5% | Asia-Pacific, Middle-East and Africa, South America | Medium term (2-4 years) |

| Recycled PVC Requires Higher Stabilizer Loadings | +0.2% | Europe core, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand Surge from PVC Pipes and Fittings

Water-infrastructure modernization across India, Thailand, Qatar, and Egypt is lifting stabilizer volumes faster than base-resin demand. Qatar Vinyl’s 350,000 tpa line, commissioned in 2025, focuses on irrigation and desalination pipe that needs UV-resistant calcium-zinc or organotin blends capable of withstanding 50 °C ambient temperatures. Egyptian Petrochemicals’ 120,000 ton expansion due January 2026 underpins North African pipe demand certified to ISO 1452 pressure standards. Regional supply gaps position localized stabilizer compounders to capture share as freight and lead-time advantages outweigh marginal cost premiums. The pivot from lead to calcium-zinc adds 5-8% to stabilizer cost but unlocks potable-water approvals that command 10-15% price premiums in municipal tenders.

Regulatory Shift to Ca/Zn Stabilizers

EU REACH Annex XVII and RoHS 2011/65/EU effectively barred lead stabilizers by 2024, forcing global producers to redesign portfolios or exit legacy lines. China’s export-oriented converters adopted Ca/Zn to preserve market access, while domestic pipes still rely on barium-zinc blends, creating a dual-track supply chain. North American manufacturers face softer federal rules, yet Proposition 65 labeling and Vinyl Institute commitments mirror European pressure with a 3-5-year lag. The U.S. FDA still allows organotin for food contact under 21 CFR 178.2650, maintaining a niche for methyltin in medical films. Long development cycles (18-24 months) and pilot extrusion investments raise barriers for fast followers contemplating Ca/Zn or metal-free alternatives.

Rising PVC Use in Lightweight Automotive Parts

Corporate Average Fuel Economy targets and Euro 7 emission rules push automakers to substitute metal with polymers. PVC content averaged 32 lb per vehicle in 2023, and electric models carry 450 lb of plastics, driving demand for low-smoke, zero-halogen wire harnesses. REACH phthalate limits accelerate trials of Ca/Zn and organic stabilizers that curb fogging per ISO 6452. Avient’s 2024 non-PFAS LubriOne launch exemplifies market pull toward PFAS-free processing aids that still fit 200 °C PVC windows. Chinese EV production above 9 million units in 2025 fuels local validation of magnesium-molybdenum-phosphorus stabilizers achieving UL 94 V-0 without bromine. These shifts favor suppliers able to bundle heat, UV, and flame performance in a single additive pack.

Construction Boom in Emerging Economies

National Infrastructure Pipeline (USD 1.4 trillion through 2025) allocates 15% to water and sanitation, directly lifting rigid-pipe demand in India[1]Ministry of Jal Shakti, “Jal Jeevan Mission Progress,” india.gov.in . Vision 2030 mega-projects such as NEOM specify PVC piping for non-potable flows at 60 °C, pushing formulators toward high-loading Ca/Zn-lanthanum blends. Brazil’s Minha Casa, Minha Vida relaunch drives window-profile and conduit demand, though tin tariffs encourage domestic Ca/Zn adoption. Southeast Asian housing starts above 3% annual growth favor luxury vinyl tile, adding pull for liquid stabilizers that assure tight color tolerances in printed films.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Bans on Lead and Phthalate Additives | -0.4% | Europe and North America, cascading to export-oriented Asia | Long term (≥ 4 years) |

| Price Volatility of Tin and Barium Feedstocks | -0.3% | Global, acute in Asia-Pacific tin-stabilizer producers | Short term (≤ 2 years) |

| Formulation Challenges for Medical-Grade Recycled PVC | -0.1% | North America and Europe medical device hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Bans on Lead and Phthalate Additives

REACH Entry 63 and RoHS 0.1% thresholds removed lead stabilizers from European electrical and construction use by 2024. Switching to Ca/Zn raises raw-material outlay USD 200-400 per ton, a burden that small regional compounders struggle to offset in price-sensitive pipe markets. Phthalate restrictions spanning DEHP, DBP, BBP, and DIBP oblige co-development of non-phthalate plasticizer packs, stretching product-development cycles by up to two years. U.S. state rules (Prop 65, Safer Products WA) compound inventory-management complexity for distributors shipping nationwide. Even organotin grades, still FDA-cleared for food contact, face mounting toxicology scrutiny that incentivizes an early shift toward metal-free or Ca/Zn alternatives.

Price Volatility of Tin and Barium Feedstocks

Myanmar ore bans cut China’s import share from 80% pre-2023 to about 25% in 2025, while Indonesia’s export curbs kept refined tin above USD 14 per lb in 2024[2]U.S. Geological Survey, “Mineral Commodity Summary: Tin 2025,” usgs.gov . Solder accounts for 48% of tin demand and is projected to rise 25% by 2030, intensifying the scrap for limited feedstock. PT Timah’s 10,000 tpa methyltin unit exemplifies vertical integration but cannot hedge global tightness. Barium carbonates sourced from Guizhou and Shaanxi endure winter-season shutdowns, swinging prices 10-20% intra-year. Such volatility forces formulators to stock costly safety inventory or redesign recipes around Ca/Zn, raising working-capital needs and slowing innovation.

Segment Analysis

By Type: Calcium Dominance Masks Organic Upswing

Calcium-based held 40.22% of PVC stabilizer market share in 2025 thanks to dual REACH/RoHS compliance and attractive USD 1,800-2,200 per-ton pricing. Lead systems are now relegated to niche battery separators with virtually no 2026-2031 growth. Tin stabilizers keep a foothold in clarity-critical medical films but face cost pressure from metal spikes. Barium-zinc secures demand through balanced cost and electric-insulation performance yet is hostage to Chinese feedstock disruptions. Organic stabilizers will post the fastest 2.77% CAGR by 2031 as medical and food-contact converters push metal-free formulations that hold leachables below 1 ppm.

Demand for metal-free benzotriazole and hindered-amine packages shows in IKA’s 2024 GreenStab release, which fetched 15-20% price premiums. Clariant’s 2026 portfolio realignment further signals the migration toward high-value phosphorus-based systems. Such moves expand the absolute PVC stabilizer market size for organics despite higher unit costs, carving out defensible niches against commodity calcium blends.

Note: Segment shares of all individual segments available upon report purchase

By Form: Liquids Chip Away at Solid Hegemony

Solid stabilizers controlled 69.59% of the PVC stabilizer market in 2025 because twin-screw lines and dry-blend feed systems are ubiquitous. They remain the default in pipe, window profiles, and wire insulation where dosing accuracy and dust reduction matter. Yet each hopper changeover extends downtime by 45 min and complicates color consistency.

Liquid grades, growing at 2.35% CAGR, win share in flooring, automotive films, and specialty sheets. One-shot dosing through peristaltic pumps trims labor 20-30% and tightens ΔE variation to ±0.5, critical for wood-grain LVT and dashboard skins. Baerlocher’s 2025 liquid Ca/Zn launch and BYK’s plate-out-free additives underscore momentum. As printers migrate to digital inks that reveal even minor shade drift, liquid systems’ share will keep edging upward, adding incremental PVC stabilizer market demand despite higher per-kilo costs.

By Application: Flooring Outpaces Pipes on Growth Rate

Pipes and fittings absorbed 37.99% of stabilizers in 2025 and will keep the largest slice through 2031, anchored by water and gas networks across Asia-Pacific and GCC. Calcium-zinc at 2-4 phr remains standard given 50-year service life claims.

Florring and wall coverings are the fastest at 2.51% CAGR. Retail and hospitality retrofits favor LVT’s lower installed cost and acoustic performance over ceramic. Liquid stabilizers aid one-shot dosing and suppress plate-out, lifting yield 3-5 pp and expanding the PVC stabilizer market size for these visuals-critical products. Films, sheets, cables, and niche goods fill the balance, each tugged by sector-specific safety or clarity needs.

By End-user Industry: Medical Devices Sprint Ahead

Building and construction retained 44.72% share in 2025 as urbanizing nations pour capex into housing and water grids. Electrical and electronics take roughly one-fifth, underpinned by low-smoke, zero-halogen wire harnesses.

Medical devices, however, exhibit the quickest 2.59% CAGR. Single-use IV bags, dialysis sets, and tubing surge across India and ASEAN hospitals, demanding USP VI-compliant stabilizers that survive gamma sterilization without yellowing. Organotin and premium Ca/Zn-lanthanum blends fetch margins 20-25% above commoditized pipe grades, boosting the PVC stabilizer market’s value component. Automotive and packaging round out demand but tap differentiated packages—flame-retardant or high-clarity—to meet evolving OEM scorecards.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated with 51.56% of global volume in 2025, propelled by China’s 3 million-ton PVC exports and India’s climb toward 5.5 million tons of domestic resin by FY 2026-27 as new Adani and Reliance capacity cuts import dependence. Regional oversupply depressed Southeast Asian prices to 17-year lows, pressuring margins yet stimulating Ca/Zn adoption in value-added pipes. Thailand’s 906,000-ton output still leaves it a net importer, favoring local compounders, while Sekisui’s CPVC capacity hike in 2026 validates hot-water pipe demand across ASEAN. Mature Japan and South Korea emphasize recycled-content blends that need 15-25% more stabilizer, propping volumes despite static construction activity.

In North America, U.S. residential re-roofing and vinyl siding, plus expanding EV harness output, keep baseline growth intact. FDA acceptance of organotin in food contact preserves a niche, while Prop 65 nudges Ca/Zn share higher. Canada’s CSA B137 cold-climate pipe codes and Mexico’s USMCA localization rules steer compounders toward domestic stabilizer sourcing, widening prospects for U.S. producers.

In Europe, lead bans are complete, and phthalate curbs bite further into flexible-film volumes, tempering overall growth. Germany champions recycled-content PVC under EU Packaging Waste rules, requiring stabilizers that tolerate 50% regrind without losing weatherability. Eastern Europe plant closures tighten regional resin, favoring imported stabilizer volumes through distributors. Scandinavia’s indoor-air standards and Southern Europe’s cost sensitivity add complexity, demanding a menu from low-emission organics to bare-bones Ca/Zn.

The Middle-East and Africa represent the fastest regional CAGR at 2.36%. Qatar Vinyl and Saudi Vision 2030 megaprojects scale PVC pipe demand that calls for UV-robust stabilizers able to handle 50-60 °C service. South Africa and Nigeria rely heavily on imports, offering market entry for regional formulators.

South America leans on Brazil’s Minha Casa, Minha Vida housing program and its two-million-unit backlog. Currency gyrations and tin tariffs accelerate Ca/Zn substitution, yet limited local tin-chemical capacity sustains import flows from Indonesia and China. Argentina’s fiscal constraints cap upside, while Colombia’s pipe upgrades provide a steady, if modest, pull-on stabilizer supply.

Competitive Landscape

The PVC stabilizer market remains moderately fragmented. The top 5 players—Baerlocher, Valtris, Arkema, Avient, and Adeka—command about 55-60% of global volume, leaving space for regional specialists. Baerlocher’s footprint across 13 nations and both solid and liquid portfolios enables global OEMs to one-stop source formulations compliant with divergent regional norms. Clariant’s 2026 strategic refocus on AddWorks and Exolit signals a pivot toward higher-margin organic stabilizers that support circular claims. Arkema’s renewable-power pledge for U.S. plants and mass-balance feedstocks positions it for carbon-footprint sensitive bids.

Avient’s 2024 launch of non-PFAS and PTFE-free LubriOne formulations shows agility in meeting automotive sustainability criteria. PT Timah leverages upstream tin to boost methyltin stabilizer margins via its BANKASTAB MT line, tripling the metal’s value when converted to chemicals. Mitsui Chemicals’ pyrolysis-oil cracker and RePLAYER blockchain capabilities offer downstream stabilizer makers cradle-to-gate transparency at a price premium. Emerging disruptors probe bio-derived Ca/Zn alternatives using tall-oil fatty acids and lignin phenolics, but need scale above 5,000 tpa to dent incumbent share.

Competitive differentiation now hinges less on raw capacity and more on regulatory foresight, circularity credentials, and application-specific technical service. Suppliers able to validate formulations under USP VI, ISO 4892, and UL 94 V-0 while documenting recycled or bio-attributed inputs stand to win the highest-margin contracts, especially in medical, automotive, and LVT flooring niches.

PVC Stabilizers Industry Leaders

Adeka Corporation

Baerlocher GmbH

Valtris Specialty Chemicals

Arkema

Avient Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SONGWON and Altek International FZE partnered to distribute high-performance PVC stabilizers across the Middle-East. The collaboration leveraged Altek's network in the construction and packaging industries to enhance Altek's supply of specialty chemicals and strengthen SONGWON's market presence in the region.

- October 2023: Baerlocher GmbH inaugurated a large-scale manufacturing plant in Madhya Pradesh, India, which focused on producing calcium-based PVC stabilizers. This represented the Baerlocher Group's largest investment outside Germany, emphasizing its commitment to sustainable additives in the Indian market.

Global PVC Stabilizers Market Report Scope

PVC (polyvinyl chloride) stabilizers enhance the performance and longevity of PVC products. These additives combat degradation from heat, light, and chemicals, preserving the material's physical and mechanical integrity. Industries such as automotive, construction, and electronics extensively utilize PVC stabilizers.

The PVC stabilizers market is segmented by type, form, application, end-user industry, and geography. By type, the market is segmented into calcium-based, lead-based, tin-based, barium/zinc-based, and organic-based. By form, the market is segmented into solid and liquid. By application, the market is segmented into pipes and fittings, cables and wires, profiles and frames, films and sheets, flooring and wall coverings, and other applications. By end-user industry, the market is segmented into building and construction, electrical and electronics, automotive and transportation, packaging, footwear, medical devices, and other end-user industries. The report also covers the sizes and forecasts for the PVC stabilizers in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Calcium-based |

| Lead-based |

| Tin-based |

| Barium/Zinc-based |

| Organic-based |

| Solid |

| Liquid |

| Pipes and Fittings |

| Cables and Wires |

| Profiles and Frames |

| Films and Sheets |

| Flooring and Wall Coverings |

| Other Applications |

| Building and Construction |

| Electrical and Electronics |

| Automotive and Transportation |

| Packaging |

| Footwear |

| Medical Devices |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Calcium-based | |

| Lead-based | ||

| Tin-based | ||

| Barium/Zinc-based | ||

| Organic-based | ||

| By Form | Solid | |

| Liquid | ||

| By Application | Pipes and Fittings | |

| Cables and Wires | ||

| Profiles and Frames | ||

| Films and Sheets | ||

| Flooring and Wall Coverings | ||

| Other Applications | ||

| By End-user Industry | Building and Construction | |

| Electrical and Electronics | ||

| Automotive and Transportation | ||

| Packaging | ||

| Footwear | ||

| Medical Devices | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected demand for PVC stabilizers by 2031?

Global consumption is forecast to reach 1.80 million tons by 2031, expanding at a 2.27% CAGR from 2026-2031.

Which stabilizer type will grow the fastest over the forecast period?

Organic-based are expected to post a 2.77% CAGR through 2031 as medical and food-contact applications tighten leachable limits.

Why are liquid stabilizers gaining share in flooring applications?

One-shot liquid dosing cuts color variation to ±0.5 ΔE and shortens changeovers, crucial for luxury vinyl tile lines where visual uniformity drives acceptance.

How do recycled PVC streams influence stabilizer usage?

Mechanical recycling degrades polymer chains, requiring 15-25% more stabilizer per ton to recover melt stability and long-term color, especially in Europe’s circular-content mandates.