Decorative Laminates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.88 Billion |

| Market Size (2031) | USD 10.30 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

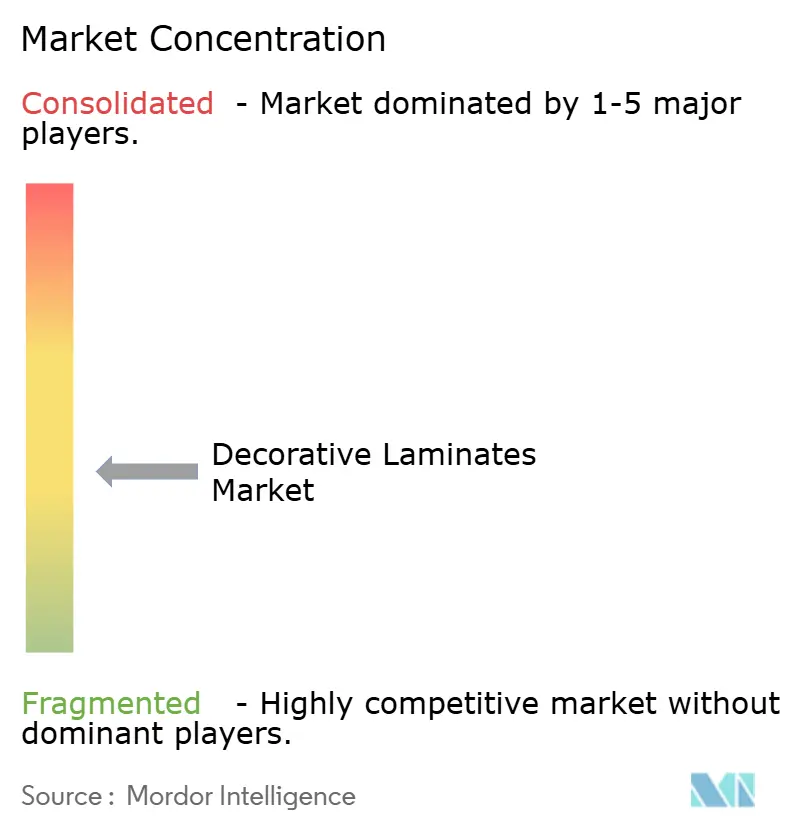

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decorative Laminates Market Analysis by Mordor Intelligence

The Decorative Laminates Market size was valued at USD 8.62 billion in 2025 and is estimated to grow from USD 8.88 billion in 2026 to reach USD 10.30 billion by 2031, at a CAGR of 3.01% during the forecast period (2026-2031). A tightening formaldehyde-emission ceiling in Europe, volatile new-build activity in Asia-Pacific, and substitution pressure from luxury vinyl tile (LVT) and engineered stone are reshaping sourcing strategies and capital allocation. Digital printing and emboss-in-register lines are scaling because they cut plate costs and support bespoke décor programs that mature rotogravure assets cannot deliver economically. Overlay papers are also displacing kraft cores as designers demand ultra-realistic textures that capture premium price points despite higher resin content. Finally, European anti-dumping duties on Chinese décor paper have accelerated vertical integration, forcing converters to internalize impregnation to protect margins.

Key Report Takeaways

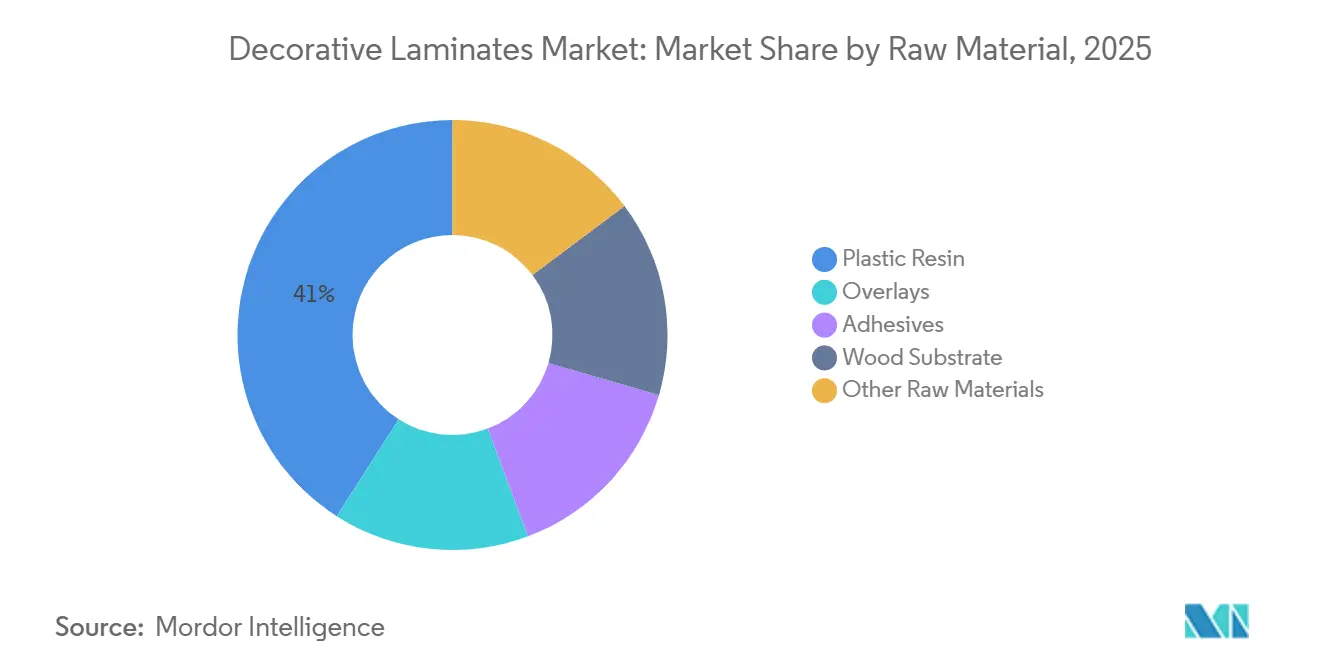

- By raw material, plastic resin held 40.96% of the Decorative Laminates market share in 2025. Overlays are advancing at the fastest CAGR of 3.43% CAGR through 2031.

- By application, furniture maintained a 53.14% revenue share of the Decorative Laminates market size in 2025. Wall panels are projected to expand at a 3.21% CAGR to 2031.

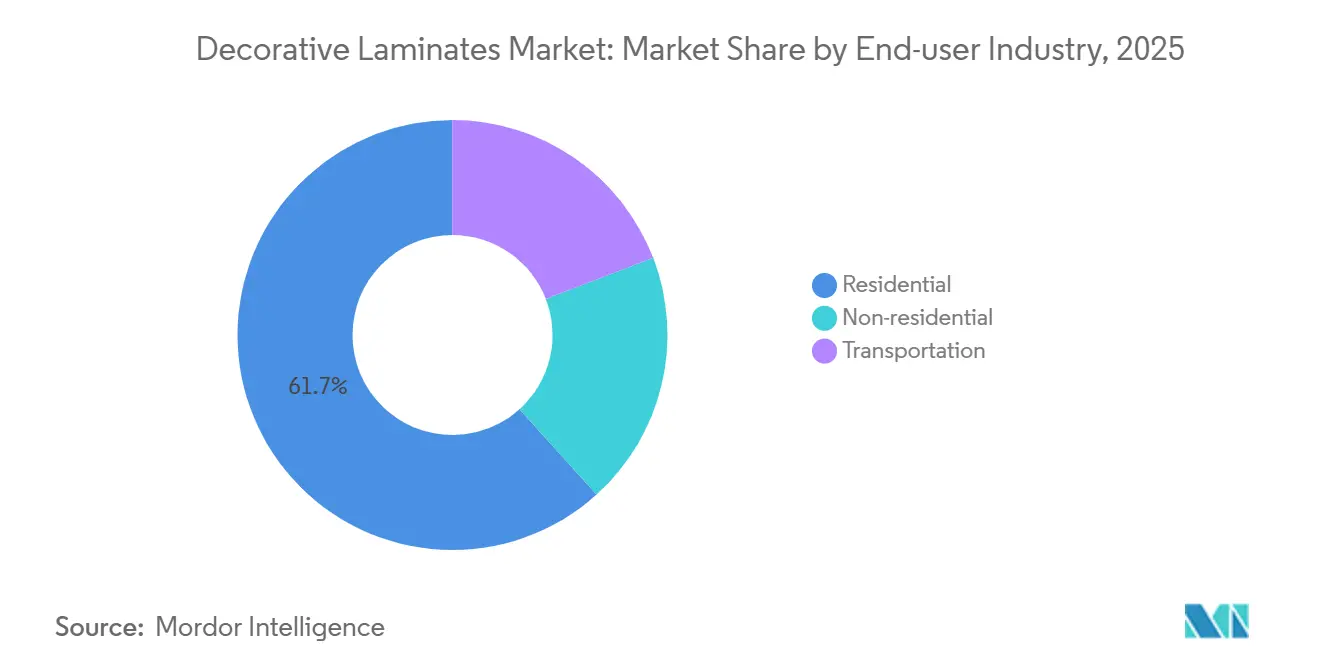

- By end-user industry, the residential segment accounted for 61.69% of the Decorative Laminates market size in 2025. Non-residential recorded the highest projected CAGR at 3.64% through 2031.

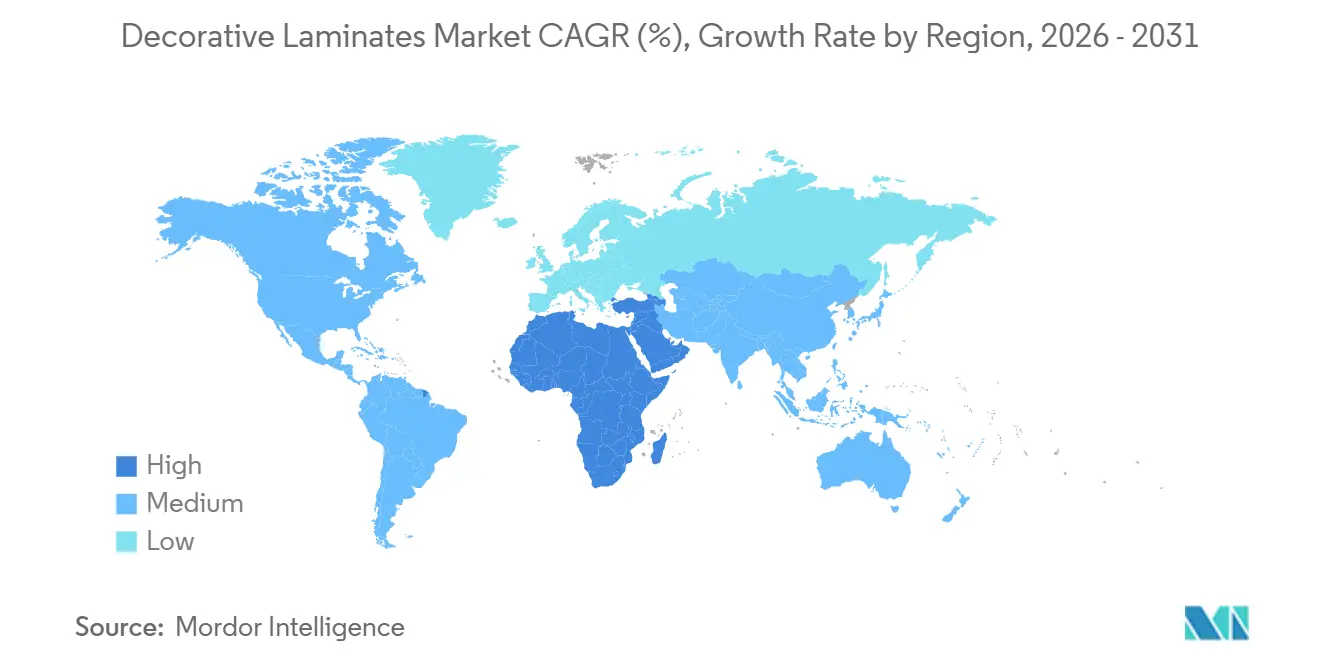

- By geography, the Asia-Pacific held the highest market share of 38.24% in 2025. However, the Middle East and Africa share is expected to grow the fastest with a CAGR of 3.49% through the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Decorative Laminates Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential construction surge in Asia-Pacific | +0.9% | India core, partial offset by China contraction; spillover to Southeast Asia | Medium term (2-4 years) |

| Cost-effective aesthetics fuelling renovation demand | +0.7% | Global, with concentration in Japan, North America, and Western Europe | Short term (≤ 2 years) |

| Advances in digital printing and emboss-in-register tech | +0.5% | North America and EU early adoption; Asia-Pacific manufacturing scale-up | Long term (≥ 4 years) |

| Prefab single-family housing with laminate-integrated panels | +0.4% | North America primary; nascent in Australia and Scandinavia | Medium term (2-4 years) |

| Tier-II/III city e-commerce DIY cut-sheet adoption | +0.3% | India and Southeast Asia core; limited penetration in China tier-III cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Residential Construction Surge in Asia-Pacific

India's residential market is growing. In H1 2025, premium-segment home sales surged, leading to increased demand for laminates in kitchens, wardrobes, and wall paneling. Conversely, China experienced a downturn: real-estate investments plummeted, and finished-home deliveries dropped, dampening the demand for laminates in the region[1]National Bureau of Statistics of China, “Real Estate Development and Sales Jan–Oct 2024,” stats.gov.cn. As a result, producers are reallocating their inventory, focusing on India's tier-I and emerging tier-II cities, while reducing their presence in the oversaturated coastal hubs of China. With record office leasing in India and a retail pipeline extending through 2028, opportunities in commercial fit-outs are expanding. Additionally, while Southeast Asian housing stimulus packages cast a positive light on the market, supply-chain fragmentation is moderating immediate volumes.

Cost-Effective Aesthetics Fueling Renovation Demand

In FY 2024, Japan's renovation expenditure underscored a trend where homeowners and developers lean towards refurbishing existing assets rather than embarking on new constructions, especially in light of the nation's aging demographic. Among wood-look surfaces, decorative laminates stand out for their cost-effectiveness, making them a favored choice in budget-sensitive remodeling endeavors. While DIY e-commerce platforms in India and Southeast Asia have begun shipping cut-to-size panels across the nation, their growth potential is hampered by a lack of installer training, leading to fewer repeat orders. North America's aging housing stock continues to drive remodeling activities. However, with mortgage rates set to rise in 2025, consumers are gravitating towards mid-tier laminate grades instead of premium ones. Western Europe exhibits a similar trend of thriftiness, but the push from landlord regulations on energy retrofits somewhat mitigates this down-trading.

Advances in Digital Printing and Emboss-in-Register Tech

Digital inkjet lines now replicate stone and textile motifs with a fidelity that was once the hallmark of luxury veneers. Meanwhile, emboss-in-register presses align texture and print seamlessly. Unilin's Lux 21 line integrates both functions in line. This innovation reduces the minimum economic order size and mitigates inventory risks. Koenig & Bauer's RotaJET platform has revolutionized make-ready times, cutting them down from hours to mere minutes. This efficiency is paramount for bespoke designs driven by architects. Due to the EU's anti-dumping duty on Chinese décor paper, feedstock costs have surged. In response, converters are now bringing impregnation processes in-house to safeguard their margins. With laminates already composed of biobased materials and post-consumer recycled fiber, digital workflows are playing a pivotal role in meeting the increasing demands for embodied-carbon disclosure.

Prefab Single-Family Housing with Laminate-Integrated Panels

North American prefab builders now specify laminate-clad cabinetry and wall panels at the factory stage, compressing on-site labor and waste. Orders come as bulk contracts, smoothing demand for suppliers but locking design weeks in advance. Adhesive systems must survive vibration and humidity swings during module transport, driving research and development in low-VOC chemistries. Australia and Scandinavia are piloting similar models, while Asia-Pacific sticks to bespoke site work that limits prefabricated panel adoption. Warranty exposure for transport damage forces producers to extend after-sales services, but the trade-off is higher line-run predictability.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by engineered stone, LVT and thermofoils | -0.6% | Global, with acute pressure in North America and Western Europe mid-tier residential | Short term (≤ 2 years) |

| European Union E1/E0 formaldehyde-emission compliance costs | -0.4% | EU core; ripple effect on exporters to EU from Asia-Pacific and North America | Medium term (2-4 years) |

| Supply-chain traceability costs for wood substrates | -0.3% | EU primary due to EUDR; North America secondary via FSC/PEFC certification pressure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution by Engineered Stone, LVT, and Thermofoils

Luxury vinyl tile now dominates moisture-prone floor zones because it resists water and installs quickly with click-lock systems. Engineered stone countertops capture upmarket kitchen and bath remodels where buyers view laminates as a resale compromise. Thermofoil doors create seamless edges that European buyers perceive as higher quality than edge-banded laminate fronts. To regain share, laminate producers bank on high-resolution prints and deep-textured embossing that narrows the aesthetic gap, but price parity remains elusive in volume segments. Developing markets still opt for laminates on cost grounds, softening global substitution pressure yet not reversing it.

European Union Formaldehyde-Emission Compliance Costs

Starting August 6, 2026, Regulation 2023/1464 will limit emissions from composite wood panels to 0.062 mg/m³. This mandates resin reformulation and ongoing monitoring[2]European Commission, “Regulation 2023/1464 Formaldehyde Limits,” ec.europa.eu. In anticipation of this regulation, a major plant has invested in capture systems and bio-based adhesives. Meanwhile, smaller converters grapple with the choice of consolidating or exiting the EU market. They face fixed overheads from accreditation, testing, and batch traceability. To engage EU buyers, exporters must obtain certifications per EN 16516 and EN 717-1. This requirement raises entry barriers, benefiting established players with operations across multiple countries. Additionally, the regulation boosts demand for E0-certified overlays and resins, pushing up input prices.

Segment Analysis

By Raw Material: Overlay Adoption Rises as Resin Volatility Persists

Plastic resin accounted for 40.96% of the decorative laminates market in 2025, reflecting its central role in melamine and phenolic bonding. Yet overlay papers are on track to post a 3.43% CAGR to 2031, the fastest in the raw-material mix. This trend is driven by architects' demand for high-definition prints and synchronized embossing, features that overlays provide without increasing thickness. In Asia-Pacific, where long-term contracts are uncommon, the pricing of plastic resin—tied to fossil feedstocks—necessitates careful cost pass-throughs.

The growth of overlays is further fueled by the EU's imposition of an anti-dumping duty on Chinese décor paper. This move has nudged European converters to adopt in-house impregnation methods, ensuring a steady supply. Meanwhile, adhesive suppliers are introducing bio-based, formaldehyde-free systems. These systems, while commanding a premium, assist producers in adhering to the stringent ceiling. Wood substrates continue to be vital, but the EU's Deforestation Regulation has escalated audit costs. However, mills boasting FSC or PEFC licenses are now positioned to capitalize on a pricing advantage. With an uptick in certified volumes, the segment of the decorative laminates market linked to recycled wood content is anticipated to outpace the growth of virgin-fiber volumes.

Note: Segment shares of all individual segments available upon report purchase

By Application: Wall Panels Gain Share as Furniture Matures

Furniture dominated demand at 53.14% in 2025, sustained by ready-to-assemble cabinets and modular workstations. However, wall panels are expected to outpace every other application, advancing at a 3.21% CAGR through 2031. Commercial fit-outs, particularly in India and the Gulf, specify laminate-clad partitions that stand up to high traffic and tight build schedules.

Hotel and retail designers are increasingly favoring emboss-in-register prints that replicate concrete, textile, and leather textures, leading to a shift away from traditional paint and wallpaper. While laminates once held a strong position in flooring, they're now losing ground to water-resistant LVT. In Europe, thermofoil fronts are making inroads into cabinet doors. Japan's non-residential renovation orders have redirected focus from flooring to decorative wall cladding. As a result, the market share of decorative laminates in wall panels is set for a steady ascent, especially as hospitality refurbishments prioritize quick-install, low-VOC surfaces.

By End-User Industry: Commercial Spaces Lead Future Growth

Residential buyers consumed 61.69% of volumes in 2025, yet office, retail, and hospitality fit-outs will be the growth engine, with non-residential demand forecast to rise at a 3.64% CAGR to 2031. This optimistic outlook is bolstered by strong office leasing activity in India for 2024, alongside a robust retail pipeline, signaling strong demand for items like reception desks, washroom cubicles, and display fixtures.

Japan's non-residential renovation expenditure highlights a trend in mature markets: a preference for capital expenditure on refresh cycles over new constructions. While transportation interiors carve out a niche, they prove to be lucrative; notably, automotive-grade laminates play a pivotal role in the lightweighting endeavors of electric vehicles. Although China's ongoing slump continues to weigh on global residential volumes, India's achievement in home completions for FY 2025 provides a noteworthy counterbalance. Furthermore, the decorative laminates market, catering to prefab factories, challenges conventional end-user distinctions, as these modules seamlessly incorporate cabinetry and wall panels prior to shipment.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 38.24% of revenue in 2025, but growth is bimodal. India is on the brink of a booming housing market, and with record commercial leasing, the country is witnessing a swift adoption of laminates in furniture and wall panels. In contrast, China is grappling with a significant drop in finished-unit deliveries from January to October 2024. This downturn has compelled suppliers to either pursue export orders or shift their focus to refurbishment niches. Meanwhile, Japan's substantial expenditure on renovations highlights a broader trend: a move away from new constructions towards upgrades. This trend is also evident in South Korea, where the aging housing stock is prompting similar shifts.

In North America, a stable market sees remodeling and prefab housing balancing out the slowdown in new builds. However, a spike in mortgage rates in 2025 has curtailed some discretionary upgrades. Europe is bracing for a formaldehyde cap in August 2026, impacting its decorative laminates market. A testament to the capital needed for compliance is EGGER's new production line in Germany. Additionally, anti-dumping duties on Chinese décor paper are putting pressure on converters across the continent, leading to heightened interest in local impregnation assets.

The Middle East and Africa are projected to post the fastest regional CAGR at 3.49% through 2031. In Saudi Arabia and the UAE, megaprojects are turning to laminate-clad interior solutions, emphasizing the need for tight delivery schedules. Concurrently, rising per-capita incomes are fueling a surge in residential refurbishments. While South America may contribute smaller volumes, urbanization trends in Brazil are providing a boost. Given the evolving regulatory landscapes and cyclical nature of construction, regional suppliers are finding themselves in a delicate dance: balancing the capital needed for compliance with the agility required for capacity deployment.

Competitive Landscape

The decorative laminates market is moderately fragmented. Smaller firms lacking emission-testing labs face either niche specialization or merger with larger peers before the August 2026 deadline. E-commerce-focused brands target India’s tier-II/III cities with cut-sheet packs but must solve installer scarcity to lock in repeat sales. FSC and PEFC certifications are becoming tender prerequisites in Europe and North America, adding to costs yet opening doors to public-sector projects. As capacity additions cluster in compliant plants, supply is likely to migrate from high-cost, sub-scale mills to regional hubs capable of multi-country servicing.

Decorative Laminates Industry Leaders

Wilsonart LLC

Greenlam Industries Limited

Broadview Holding

Kronoplus Limited

Egger

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rushil Decor Limited inaugurated a new manufacturing facility in Village Itla, Gujarat, and commenced commercial production of jumbo-sized decorative laminate sheets. The newly established unit is designed to produce approximately 1.2 million sheets annually (based on a 1 mm sheet) in its first phase.

- March 2025: Formica Corporation rebranded its DecoMetal laminates line to Homapal. Homapal, based in Herzberg am Harz, Germany, is a global real metal and magnetic laminate producer. The collection will now represent North America's architectural metal offerings.

Global Decorative Laminates Market Report Scope

Decorative laminates are defined as versatile surfacing materials composed of layers of kraft paper impregnated with plastic resins (phenolic and melamine), topped with a decorative paper, and bonded under high or low pressure to a wood-based substrate. They are widely used for furniture, cabinets, flooring, and wall panels, offering durable, aesthetic, and resistant finishes.

The market is segmented by raw material, application, end-user industry, and geography. By raw material, the market is segmented into plastic resin, overlays, adhesives, wood substrate, and other raw materials. By application, the market is segmented into furniture, cabinets, flooring, wall panels, and other applications. By end-user industry, the market is segmented into residential, non-residential, and transportation. The report also covers the market sizes and forecasts in 15 countries. For each segment, the market sizing and forecasts were made based on revenue (USD).

| Plastic Resin |

| Overlays |

| Adhesives |

| Wood Substrate |

| Other Raw Materials |

| Furniture |

| Cabinets |

| Flooring |

| Wall Panels |

| Other Applications |

| Residential |

| Non-residential |

| Transportation |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Plastic Resin | |

| Overlays | ||

| Adhesives | ||

| Wood Substrate | ||

| Other Raw Materials | ||

| By Application | Furniture | |

| Cabinets | ||

| Flooring | ||

| Wall Panels | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Non-residential | ||

| Transportation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current decorative laminates market size and projected growth?

It was USD 8.88 billion in 2026 and is forecast to reach USD 10.30 billion by 2031 at a 3.01% CAGR.

Which raw material segment will grow the fastest through 2031?

Overlay papers are expected to post a 3.43% CAGR, outpacing plastic resin and adhesives.

Why are wall panels gaining ground over furniture in laminate demand?

Commercial fit-outs and hospitality refurbishments favor quick-install, embossed wall panels that simulate stone or textile finishes.

Which region offers the highest forecast CAGR?

The Middle East and Africa are projected to grow at 3.49% annually through 2031, led by Saudi and UAE megaprojects.