Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Polyethylene Naphthalate Market Report is Segmented by Product Form (Film Grade, Fiber Grade, Resin/Pellet Grade), Application (Beverage Bottling, Packaging, Electronics, Rubber Tires, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

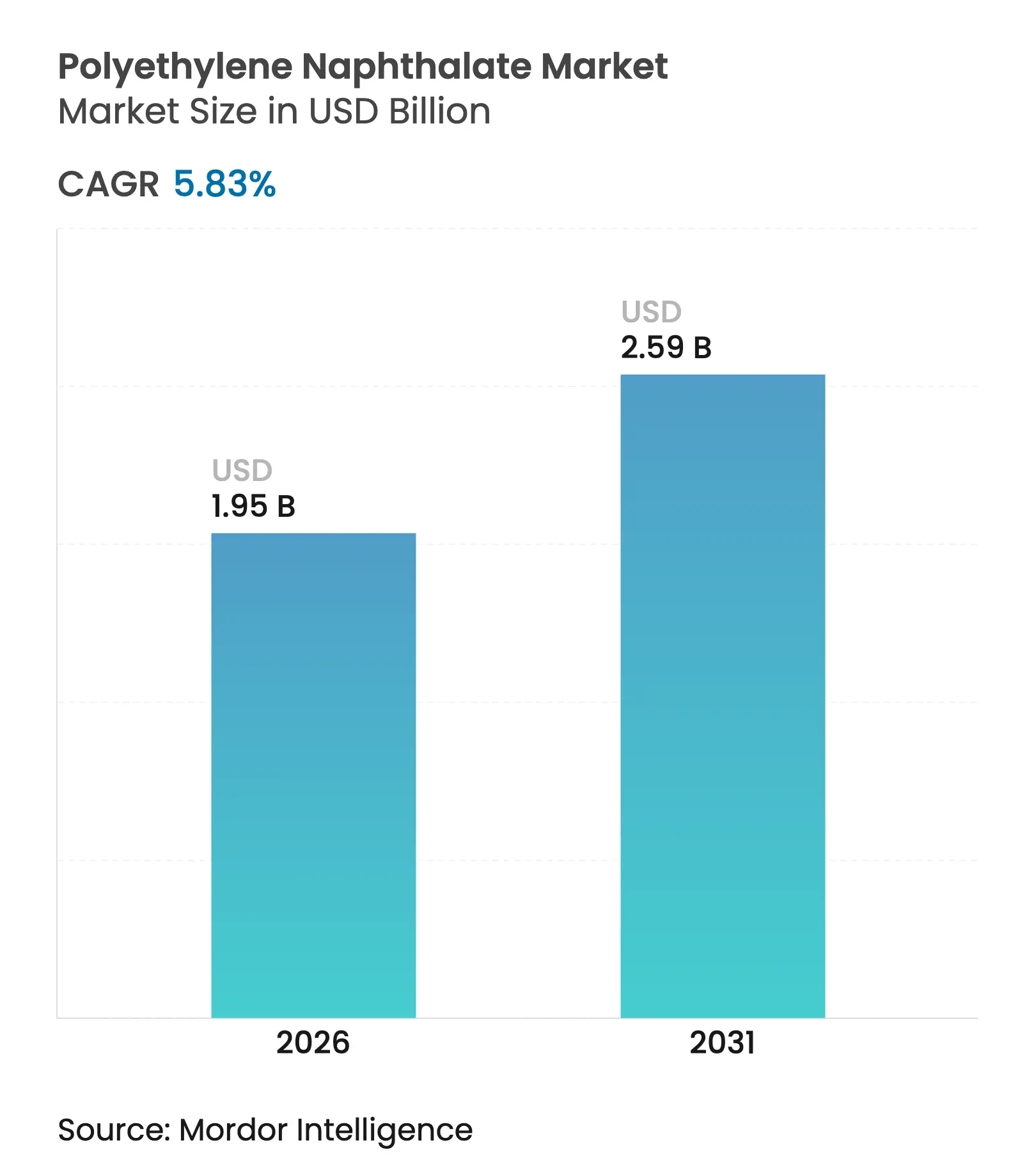

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 5.83 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Polyethylene Naphthalate Market size was valued at USD 1.84 billion in 2025 and estimated to grow from USD 1.95 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). Superior thermal stability, barrier performance against oxygen and moisture, and dimensional integrity up to 220°C continue to pull the polymer into advanced packaging, flexible electronics, and next-generation energy devices. OEMs in 5G infrastructure, wearable technology, and electric-vehicle (EV) battery systems increasingly specify PEN over PET because it withstands hot-fill, solder-reflow, and sterilization profiles without shrinkage, delamination, or loss of dielectric strength. Supply security remains a pivotal theme because only a handful of global producers convert 2,6-naphthalenedicarboxylic acid into PEN, creating both pricing leverage for incumbents and vulnerability to regional disruptions. Sustainability pressures from regulators and brand owners accelerate R&D in recyclable mono-material multilayer packaging and low-carbon bio-routes, adding a new dimension to competition.

Key Report Takeaways

*Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Barrier and thermal superiority in packaging

Barrier and thermal superiority in packaging

| +1.8% | North America and Europe, global roll-out | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

North America and Europe, global roll-out

|

Impact Timeline

:

Medium term (2-4 years)

|

PEN films for EV batteries and flex-electronics

PEN films for EV batteries and flex-electronics

| +1.5% | Asia-Pacific core, spill-over to North America | Short term (≤2 years) | |||

5G and wearable devices need stable circuits

5G and wearable devices need stable circuits

| +1.2% | Asia-Pacific and North America | Medium term (2-4 years) | |||

Substrates for perovskite and flexible PV

Substrates for perovskite and flexible PV

| +0.8% | Europe and Asia-Pacific | Long term (≥4 years) | |||

Shift to recyclable mono-material packaging

Shift to recyclable mono-material packaging

| +0.7% | Europe and North America, expanding worldwide | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Barrier and Thermal Superiority in Packaging

PEN’s glass-transition temperature of 120°C versus PET’s 80°C lets beverage producers execute hot-fill and pasteurization without panel collapse, taste ingress, or oxygen pickup, highlighting innovations in the polyethylene naphthalate industry. The material’s oxygen-transmission rate is one-tenth that of PET, extending shelf life for sensitive nutraceutical drinks and ready-to-drink coffees. Brand owners pursuing mono-material multilayer bottles use PEN as both core and tie-layer, enabling recycling streams free of foreign polymers. Recent pilot lines in Germany demonstrated 30% lighter bottles with equal carbonation retention, cutting logistics emissions. Equipment compatibility with legacy PET injection-stretch-blow machines reduces conversion hurdles, allowing quick scale-up at global fillers.

Demand Surge for PEN Films in EV Batteries and Flexible Electronics

Separator films made of PEN retain tensile strength above 175 MPa at 140°C, limiting shrinkage to less than 1% during thermal runaway events in lithium-ion cells, a key safety differentiator versus polyolefin alternatives within the polyethylene naphthalate market. Automotive OEMs specify the polymer for pouch and cylindrical formats to satisfy new UN 38.3 abuse-test thresholds. In flexible OLED displays, PEN substrates enable curvature radii below 2 mm while sustaining 85% optical transmittance. Asian panel makers report that roll-to-roll coating on PEN achieves defect densities 40% lower than on polyimide, accelerating yield learning curves for foldable smartphones.

5G and Wearable Devices Need Dimensionally Stable Flexible Circuits

High-frequency circuits in 5G radio units demand substrates with low dielectric loss and a stable coefficient of thermal expansion, and the polyethylene naphthalate industry is benefiting from this shift. PEN’s CTE of 13 ppm °C⁻¹ aligns well with copper traces, minimizing line-width variance after reflow. Direct lamination of graphene on PEN produces transparent antennas that retain 95% conductivity after 10,000 bend cycles. Wearable medical patches integrate PEN films with stretchable silver inks to enable multi-day biosignal capture under perspiration and body heat without delamination, supporting remote patient-monitoring protocols.

Emerging Use as Substrate in Perovskite and Flexible Solar Cells

Roll-to-roll processed perovskite modules on PEN endure 350 hours of damp-heat testing, quadruple the lifetime of PET-based counterparts. The polymer’s transparency above 92% in the visible spectrum sustains photon flux, while its thermal endurance allows sintering temperatures up to 180°C that are prohibitive for PET. European research consortia target building-integrated photovoltaics using PEN laminates that adhere directly to curved façades, reducing balance-of-system costs and installation time.

*Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High manufacturing cost of NDC

High manufacturing cost of NDC

| -1.4% | Global, price-sensitive markets | Short term (≤2 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global, price-sensitive markets

|

Impact Timeline

:

Short term (≤2 years)

|

Competition from bio-based alternatives

Competition from bio-based alternatives

| -0.9% | Europe and North America, expanding globally | Medium term (2-4 years) | |||

Feedstock concentration of naphthalate monomers

Feedstock concentration of naphthalate monomers

| -0.6% | Global, regional supply vulnerabilities | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

High Manufacturing Cost of NDC-Based Polymer

Production of 2,6-naphthalenedicarboxylic acid involves multi-stage oxidation of methyl naphthalene at 220°C and 30 bar, followed by complex purification, driving energy costs 25% above PTA levels[1]L D Lillwitz, “Production of Dimethyl-2,6-Naphthalenedicarboxylate,” sciencedirect.com[. Only three commercial plants operate at economies of scale, enabling suppliers to maintain price premiums of 45% over PET feedstock. Short-cycle price spikes correlate with capacity outages, causing downstream resin hikes that squeeze converters’ margins in consumer packaging. Cost pressure limits penetration into low-margin beverage segments, steering the polymer toward niches where performance trumps price.

Competition from Bio-Based Alternatives (PEF, PBS)

Polyethylene furanoate delivers oxygen-barrier performance equal to PEN at potentially lower greenhouse-gas footprints, attracting brand owners pursuing science-based targets and intensifying competitive dynamics within the polyethylene naphthalate market. Start-up producers in China have validated PEF bottle blow molding at commercial speeds, and recent scale-up announcements totaling 500 kt per year could undercut PEN pricing by 12% once fully utilized. If food-contact approvals converge by 2027, packaging converters may pivot toward PEF grades that promise drop-in recycling with existing PET streams.

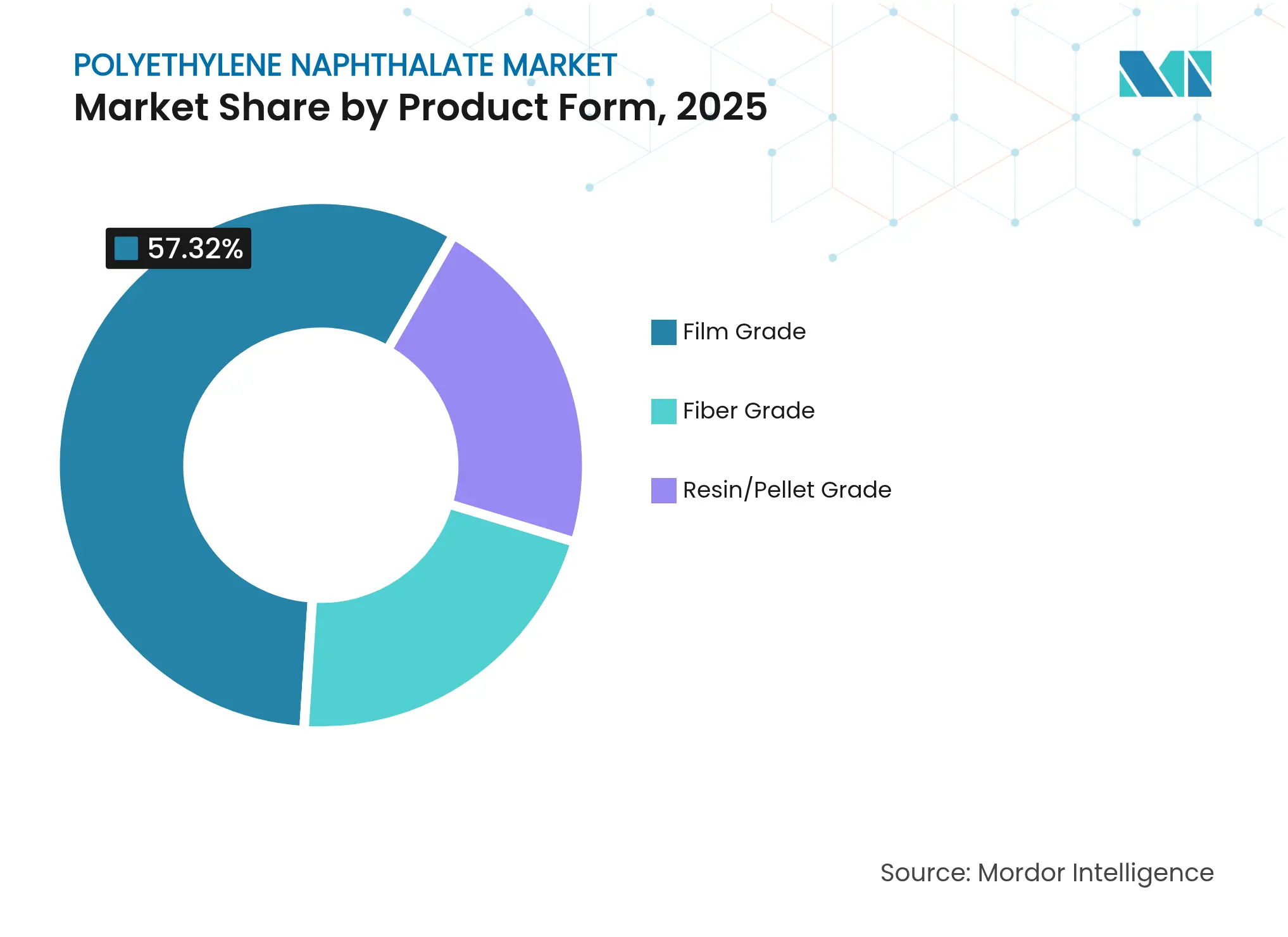

By Product Form: Film Grade Fuels Electronics Innovation

Film grade held 57.32% of the polyethylene naphthalate market share in 2025 thanks to its optical clarity, mechanical strength above 200 MPa, and dimensional stability up to 220°C, factors that allow film to replace glass or polyimide in applications such as foldable displays and camera modules. Film grade also posted the fastest 6.72% CAGR outlook, underpinned by demand from flexible printed circuits, battery separators, and transparent antennas. Electronics assemblers prefer PEN film because it matches copper’s thermal expansion, reducing warpage in multilayer substrates during lead-free solder cycles above 240°C. Processability on legacy PET coating and slitting lines minimizes capital expenditure, making the upgrade path economical.

Converters in advanced packaging rely on PEN film for multilayer pouches that block oxygen at 0.1 cc m ⁻² day ⁻¹ and water vapor at 0.05 g m ⁻² day ⁻¹. Barrier parity with aluminum foil while offering microwave transparency eliminates metal layers, enabling easier recycling. Fiber grade accounts for a solid but slower-growing niche in tire cord, conveyor belts, and fire-resistant textiles where stiffness and heat stability outperform PET. Resin or pellet grade mainly serves injection-molded hot-fill containers and precision components for aerospace ducts.

Note: Segment shares of all individual segments available upon report purchase

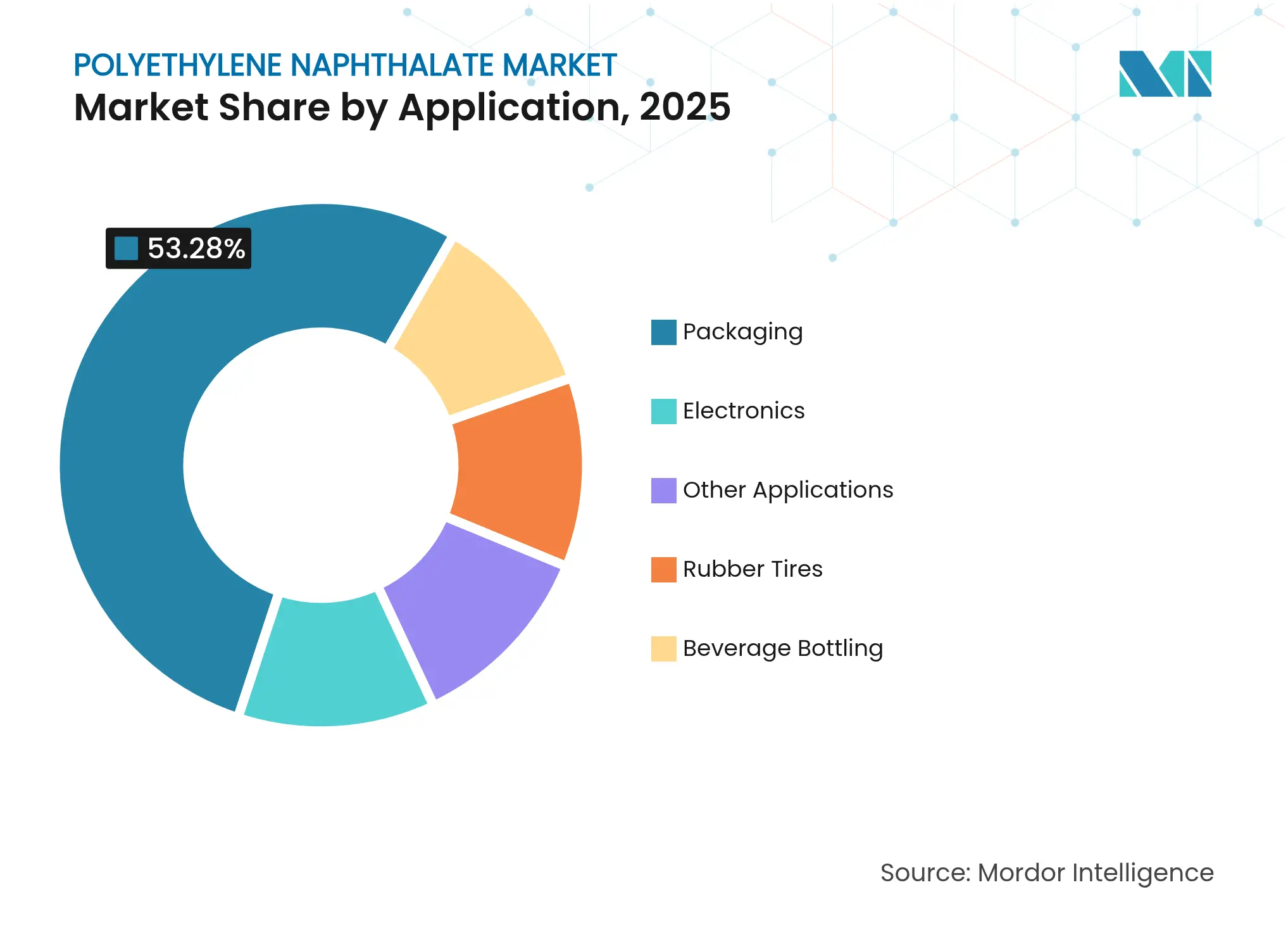

By Application: Electronics Growth Challenges Packaging Leadership

Packaging generated 53.28% of 2025 revenue because beverages, chilled foods, and hot-fill sauces exploit PEN’s high glass-transition temperature and superior gas barrier. Bottlers run pasteurization tunnels at 80°C without panel deformation, allowing shelf-stable vitamin drinks. However, electronics is on track for a 7.34% CAGR, the fastest among applications, as 5G radio boards, wearable sensors, and advanced batteries demand polymer substrates with consistent dielectric and mechanical performance.

Rubber tires use PEN fiber for cap-ply reinforcement that retains modulus at the 160°C peak temperatures seen during high-speed endurance tests, reflecting ongoing developments in the polyethylene naphthalate industry. Beverage bottling remains important, yet faces margin pressure from bio-based substitutes. Specialty optics, medical devices, and industrial films constitute the “other applications” basket, providing a steady but smaller revenue stream that benefits from the polymer’s radiation resistance.

Note: Segment shares of all individual segments available upon report purchase

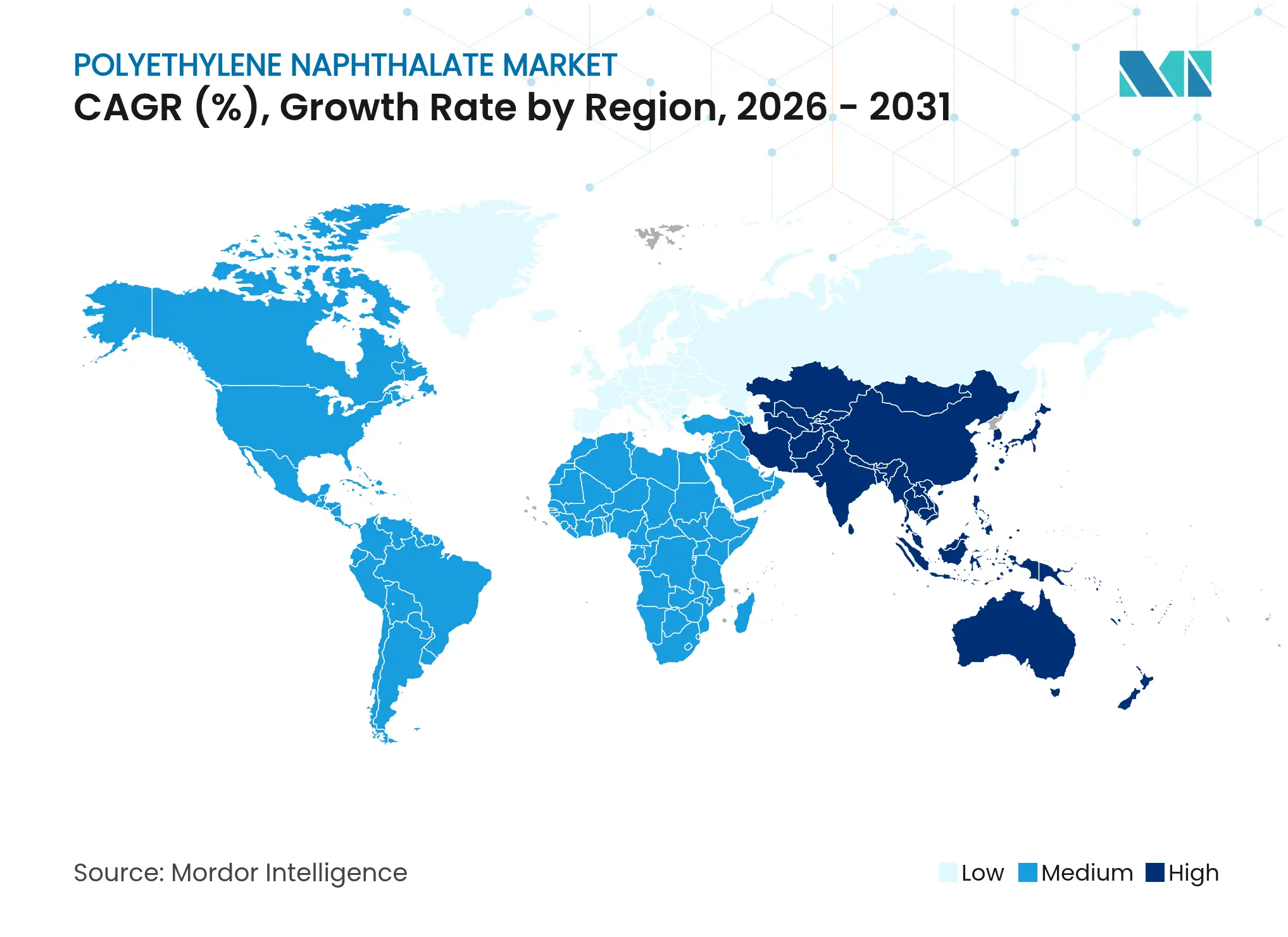

Asia-Pacific held 41.95% share of the polyethylene naphthalate market size in 2025 due to dense concentrations of display fabs, semiconductor packaging houses, and high-volume bottle converters. China’s “Made in 2025” program funds flexible OLED lines, each consuming up to 1,200 t of PEN film annually. Japan leverages the polymer’s dimensional stability in camera-module spacers essential for autonomous-driving sensors. Korea’s two largest battery makers qualified PEN separators for next-generation NCM cathodes, ensuring volume offtake through the decade.

Regional CAGR of 6.25% is driven by localization of EV supply chains and massive 5G small-cell roll-outs, reinforcing momentum within the polyethylene naphthalate market. However, over-reliance on two NDC feedstock plants located in Southeast Asia adds supply risk, prompting some OEMs to dual-source from North America. North America shows mature yet steady growth in aerospace ducts, military optical films, and hot-fill condiment bottles, reinforcing the expanding footprint of the polyethylene naphthalate market. FDA clearances encourage small-batch craft beverage producers to adopt PEN for niche carbonated energy drinks requiring pasteurization. Europe prioritizes sustainable packaging, with converters running pilot lines using chemically recycled PEN flakes to meet Extended Producer Responsibility fees, while FMCG leadership teams increasingly factor the polymer into plastic-tax avoidance strategies. South America and the Middle East & Africa remain nascent markets yet are gaining traction for solar modules that must withstand high ambient temperatures, where PEN delivers a distinct value proposition over glass.

Market Concentration

The top five producers—Teijin, SKC, Toyobo, Indorama Ventures, and SASA—controlled roughly 55% of global resin capacity in 2024, giving the polyethylene naphthalate market a moderate concentration profile. Teijin focuses on high-purity grades under the Teonex line targeting medical and aerospace. SKC integrates upstream to PTA and NDC, providing cost advantage in Asia-Pacific. Toyobo invests in ultrathin films below 10 µm for micro-display applications. Indorama Ventures leverages its PTA assets in Thailand to ensure backward-integrated cost positions, while SASA scales up bio-glycol routes to lower Scope 1 emissions.

Strategic moves include expanded 8-billion-yen interlayer-film capacity in Thailand by Sekisui Chemical for automotive head-up displays, reflecting rising innovation within the polyethylene naphthalate market. Indorama Ventures secured a USD 200 million IFC loan to boost PET and PEN recycling plants across India and Southeast Asia, elevating the company’s circular-economy credentials. Amcor’s partnership with Kolon Industries integrates PEF and recycled PEN into flexible packaging portfolios, positioning both firms for sustainability-focused bids at global CPG accounts. Patent landscapes reveal over 210 new filings since 2023 covering barrier-coated PEN films, indicating active innovation pipelines.

New entrants face barriers in proprietary catalyst know-how, stringent electronics qualification cycles, and the high capex of NDC synthesis within the polyethylene naphthalate market. Nevertheless, regional resin compounders experiment with blending recycled PEN with PCR-PET to dilute cost and ease adoption in mid-tier applications, a strategy that could shift competitive dynamics after 2028 if mechanical-property targets are met.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Polyethylene Naphthalate is a type of polyester that has properties such as oxygen barrier, hydrolytic stability, and tensile strength. It expands the application range of polyester into more demanding end uses such as rigid and flexible packaging, industrial fiber, and film for electrical, light management, data storage, and imaging applications due to its higher stiffness, moisture, gas, and light barrier, as well as thermal, electrical, and chemical resistance. The polyethylene naphthalate market is segmented by application and geography. By application, the market is segmented into beverage bottling, packaging, electronics, rubber tires, and others. The report also covers the market size and forecasts for the polyethylene naphthalate market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done in revenue (USD).

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Feasibility Analysis for FBO Services in East Africa

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.