Advanced Structural Ceramics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

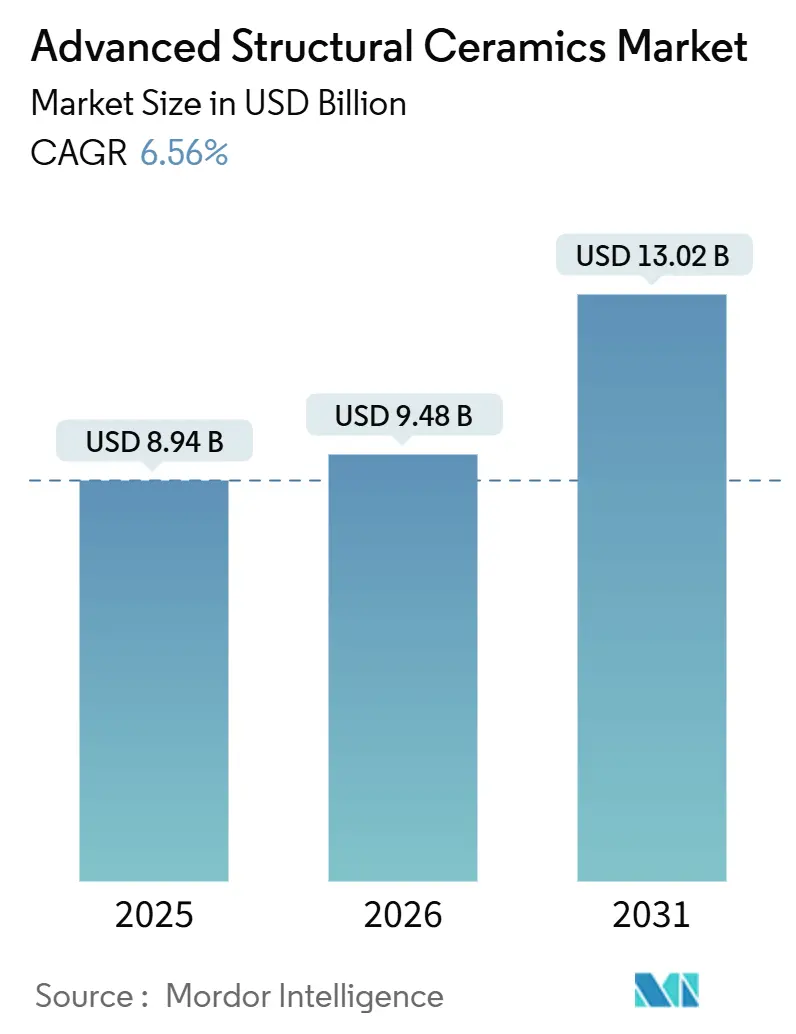

| Market Size (2026) | USD 9.48 Billion |

| Market Size (2031) | USD 13.02 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Structural Ceramics Market Analysis by Mordor Intelligence

The Advanced Structural Ceramics Market size is projected to expand from USD 8.94 billion in 2025 and USD 9.48 billion in 2026 to USD 13.02 billion by 2031, registering a CAGR of 6.56% between 2026 to 2031. Rising performance thresholds in aerospace, electric vehicles, and high-frequency electronics are reshaping material specifications, shifting demand away from legacy metals toward ceramics that remain dimensionally stable above 1,800°C. Hypersonic-vehicle prototypes in the United States and China already specify ultra-high-temperature zirconium- and hafnium-based ceramics for leading-edge structures exposed to more than 2,000°C. In parallel, the transition to 800 V battery systems in premium EVs is normalizing the use of aluminum nitride heatsinks and silicon carbide power modules, which dissipate five times more heat than copper at comparable weight. Semiconductor fabs are adopting low-loss ceramic substrates to preserve signal integrity above 28 GHz, while dental laboratories favor yttria-stabilized zirconia for its fracture toughness and esthetics.

Key Report Takeaways

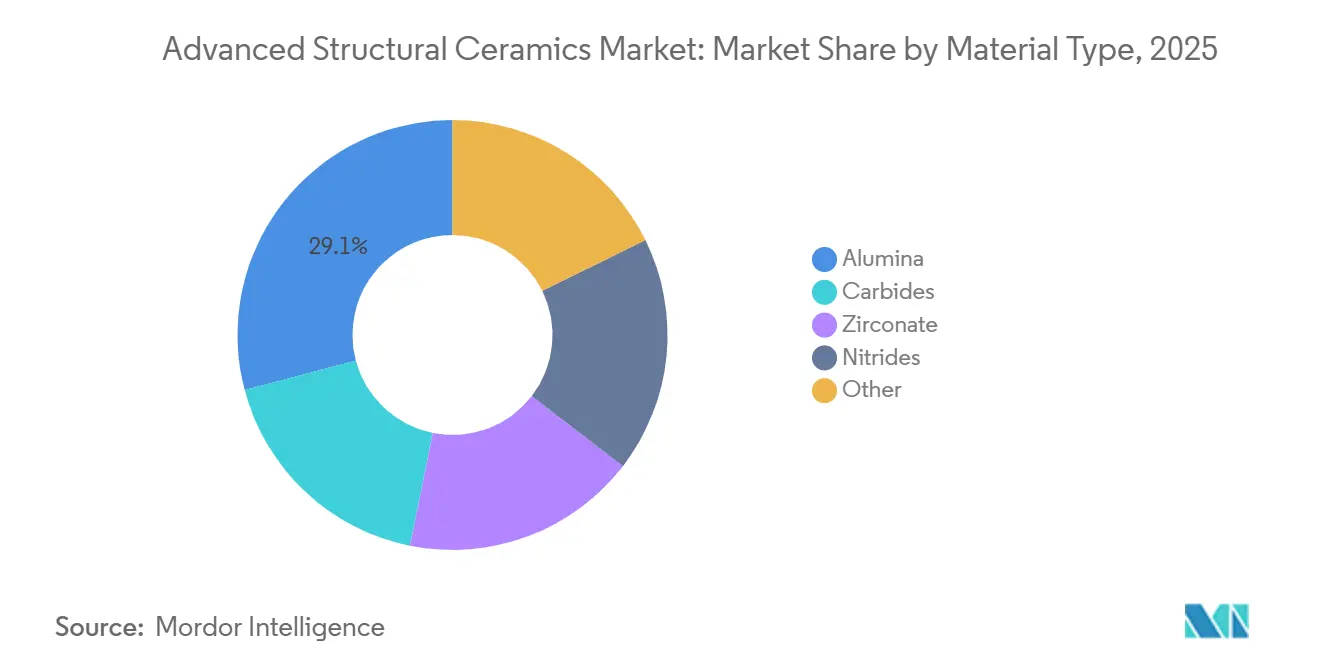

- By material, alumina held 29.12% of the Advanced Structural Ceramics market share in 2025, whereas zirconate is expanding at an 8.64% CAGR during the forecast period (2026-2031).

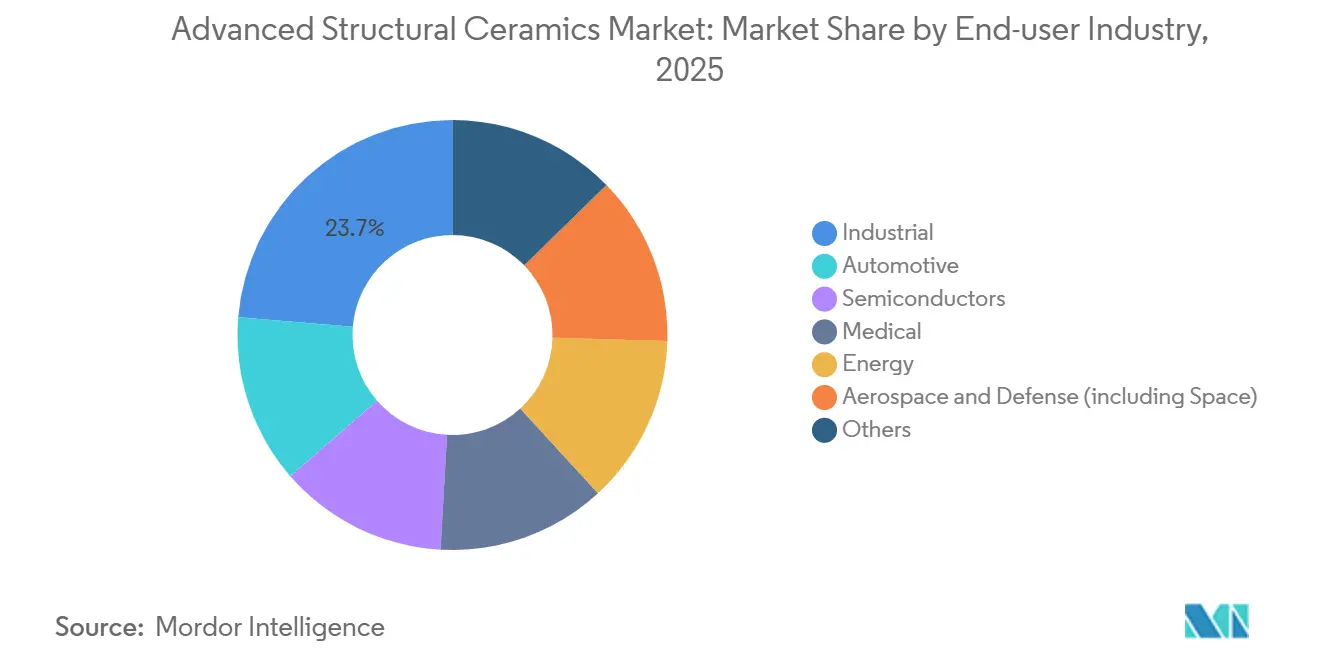

- By end-user industry, industrial applications led with 23.68% revenue share in 2025, while semiconductors record the highest projected CAGR at 7.15% during the forecast period (2026-2031).

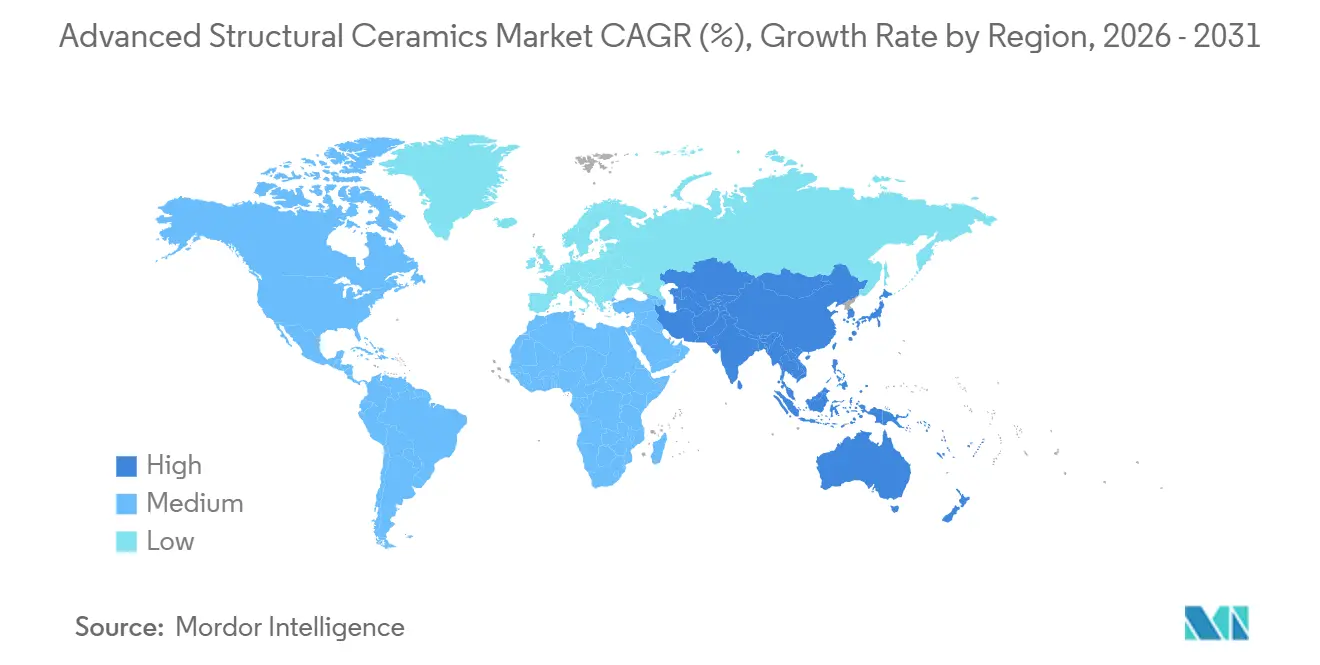

- By geography, Asia-Pacific accounted for 53.91% of 2025 revenue and will advance at a 7.11% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Structural Ceramics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for lightweight, high-temperature materials in aerospace and defence | +1.2% | North America, APAC (China, India), Europe | Medium term (2-4 years) |

| Electrification of powertrains boosting ceramic thermal-management in EVs | +1.5% | Global, with APAC and Europe leading adoption | Short term (≤ 2 years) |

| Rising 5G and advanced-node semiconductor deployment requiring low-loss ceramic substrates | +1.3% | APAC core (South Korea, Taiwan, Japan), spill-over to North America | Short term (≤ 2 years) |

| Rapid adoption of biocompatible ceramic implants in orthopaedics and dentistry | +0.9% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Hypersonic-vehicle programmes accelerating need for ultra-high-temperature advanced ceramics | +0.8% | United States, China, Russia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweight, High-Temperature Materials in Aerospace and Defense

Hypersonic flight programs require nose-cone and leading-edge structures that survive continuous exposure above 2,000°C, a threshold unattainable for nickel superalloys without active cooling. Zirconium-diboride and hafnium-diboride composites sintered with silicon carbide additives now retain flexural strength above 500 MPa after rapid thermal cycling[1]Oak Ridge National Laboratory, “ZrB2-SiC Composites,” ornl.gov. In 2025, the United States Department of Defense allotted USD 1.2 billion to accelerate the qualification of reusable ceramic matrix composites for flight tests scheduled in 2027. Partnerships between prime contractors and vertically integrated ceramic suppliers are shrinking certification lead-times, reinforcing domestic supply chains. European agencies are replicating this model to ensure sovereign access to ultra-high-temperature ceramics by 2030.

Electrification of Powertrains Boosting Ceramic Thermal-Management in EVs

Silicon carbide power electronics cut switching losses by 60%, but heat flux densities above 200 W/cm² oblige substrates with thermal conductivity higher than 150 W/m·K[2]IEEE, “High-Power SiC Modules,” ieee.org. CeramTec’s automotive-grade aluminum nitride, launched in 2024, delivers 180 W/m·K while weighing one-third as much as copper and sustaining junction temperatures to 175°C. Volkswagen specified these heatsinks for its unified cell platform in late 2025, signaling mainstream adoption across Europe. New ceramic coatings such as Zircotec’s ElectroHold reflect 85% of radiant heat, simplifying battery-pack insulation strategies. Automakers project compound cost savings from mass reduction and simplified cooling loops during the 2026–2031 design cycle.

Rising 5G and Advanced-Node Semiconductor Deployment Requiring Low-Loss Ceramic Substrates

Millimeter-wave base stations demand substrates with dielectric loss tangents below 0.001 at 28 GHz to avoid signal attenuation that undermines coverage. Low-temperature co-fired ceramic (LTCC) modules integrate embedded passives, trimming insertion loss by 1.5 dB and delivering 12% higher effective radiated power per antenna element. Murata expanded its LTCC (Low Temperature Co-fired Ceramic (LTCC)) capacity by 25% in 2025 to meet contracts with Ericsson and Nokia. Extreme-ultraviolet lithography tools also rely on yttrium-aluminum-garnet optics whose thermal-expansion match to silicon must remain within ± 0.5 ppm/K. Sustained semiconductor capital spending suggests a multi-year tailwind for ceramic components.

Rapid Adoption of Biocompatible Ceramic Implants in Orthopedics and Dentistry

Yttria-stabilized zirconia implants achieve a 98.2% ten-year survival rate, outperforming porcelain-fused-to-metal restorations. Germany’s 2024 S3 guidelines now list monolithic zirconia crowns as the preferred solution for posterior teeth. Additive manufacturing compresses implant lead times from three weeks to five days, enabling same-visit dentistry and higher reimbursement in private clinics. Plasma-sprayed calcium-phosphate coatings raise bone-implant contact above 75% within 12 weeks. In 2025, the United States FDA (Food and Drug Administration) cleared 14 new ceramic implant designs, doubling the previous year’s total.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High processing cost versus engineered metals and polymers | -1.1% | Global, acute in cost-sensitive automotive and industrial segments | Short term (≤ 2 years) |

| Brittleness limiting design flexibility in dynamic applications | -0.7% | Automotive, industrial machinery, consumer electronics | Medium term (2-4 years) |

| Volatile yttria/boron supply chain elevating raw-material risk | -0.9% | Global, concentrated impact on zirconia and boride producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Processing Cost Versus Engineered Metals and Polymers

Sintering temperatures of 1,600-1,800°C consume three to five times more energy per kilogram than aluminum casting, while diamond grinding to ±10 µm adds USD 15-25 per part. Hot-isostatic pressing ties up furnaces for up to 12 hours per batch, capping weekly output near 200 pieces. Binder-jet additive manufacturing cuts lead times from 12 weeks to three, but green-body strength constraints still require generous safety factors. Automotive tier-2 suppliers report ceramic valve guides priced at USD 8 each versus USD 2.50 for sintered steel, a premium accepted only in exhaust zones exceeding 900°C.

Brittleness Limiting Design Flexibility in Dynamic Applications

Ceramics’ tensile strength averages 30-40% of compressive strength, leaving parts susceptible to impact-induced microcracks. Silicon-nitride bearings deliver tenfold wear improvement over steel yet fail after a single 50-joule debris strike, prompting automakers to add redundant sealing that costs USD 12 per unit. Transformation-toughened zirconia lifts fracture toughness to about 10 MPa·m½ but loses that benefit above 800°C. Fiber-reinforced ceramic matrix composites display pseudo-ductility, yet oxidation above 1,200°C degrades interphase coatings, narrowing their temperature envelope. Designers often oversize ceramic parts by up to 30%, eroding the weight advantage that originally justified substitution.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Zirconate Builds Momentum as a Thermal-Barrier Workhorse

Alumina delivered 29.12% of 2025 revenue, anchored in wear parts, ballistic armor, and semiconductor wafer handling, supported by a hardness of 9 on the Mohs scale and resistivity above 10¹⁴ Ω·cm. Zirconate is projected to compound at 8.64% during the forecast period (2026-2031), driven by yttria-stabilized zirconia crowns and turbine thermal-barrier coatings whose 2.5 W/m·K thermal conductivity balances nickel-superalloy expansion. Carbides, mainly silicon and tungsten carbide, serve cutting tools and power electronics, while nitrides, such as silicon nitride and aluminum nitride, fill high-frequency substrates and bearings. Binder-jet lattice structures in alumina now cut heat-exchanger weight by 40%, yet 96% relative density imposes an 8% thermal-resistance penalty. Tungsten-carbide tools blended with 6-12% cobalt trade 10% hardness for 50% greater impact resistance in interrupted cutting. Gradient-doped zirconia concentrates toughening at the surface while preserving insulation in the core.

The advanced ceramics market size for zirconate applications is projected to reach USD 3.4 billion by 2031, reflecting its role in gas turbines and restorative dentistry. Alumina’s entrenched share in semiconductor equipment stabilizes its revenue base despite slower growth. Carbides and nitrides collectively benefit from 5G and EV momentum, but their higher raw-material costs temper margin expansion. Overall, material diversification aligns with OEM risk-mitigation strategies against raw-material volatility, a factor increasingly factored into long-term supply agreements.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Semiconductor Revenue Outpaces the Industrial Core

Industrial uses accounted for 23.68% of 2025 revenue, led by pump seals, valve seats, and refractory linings that endure corrosive slags at 1,600°C. Semiconductor demand is forecast to grow at a 7.15% CAGR during the forecast period (2026-2031) as EUV lithography requires yttrium-aluminum-garnet chucks with ±2 µm flatness, and each tool consumes 18 such parts. Automotive applications stretch from oxygen sensors to silicon-nitride turbocharger rotors capable of cold starts down to -40°C. Medical devices use zirconia hip joints and alumina spinal cages that show superior radiolucency in postoperative imaging. Energy applications include solid-oxide fuel cells whose yttria-stabilized electrolytes enable 60% electrical efficiency.

The advanced ceramics market share held by semiconductors is expected to climb by 2031 on the back of continued capex cycles and 3 nm process adoption. Industrial demand grows steadily but yields some share to sectors with higher value per part, notably medical and electric vehicles. Defense spending on hypersonic applications will further tilt the revenue mix toward ultra-high-temperature composites by the end of the forecast window.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific controlled 53.91% of 2025 revenue and is poised to advance at a 7.11% CAGR during the forecast period (2026-2031). China’s expansion of rare-earth refining in Hunan shortened zirconia lead times from 16 weeks to nine, underpinning regional dental-ceramic growth. Japan and South Korea continue to dominate multilayer ceramic capacitor feedstocks and electrostatic chucks, leveraging co-location with Samsung, SK Hynix, and Murata. India’s Gujarat and Tamil Nadu corridors are on track for 15% annual growth as import substitution takes hold under an 18% tariff regime.

North America's market share in 2025 was anchored by defense programs that require domestic sourcing under ITAR rules. CoorsTek’s Golden, Colorado, expansion of military-grade alumina will double armor-tile capacity by 2027. Canada focuses on alumina-toughened zirconia wear parts for oil-sands slurry pumps, achieving 18-month service life versus six months for high-chrome steel. Mexico’s oxygen-sensor cluster in Querétaro benefits from USMCA (United States–Mexico–Canada Agreement) content rules that favor North American material in EV power-trains.

Europe 2025 revenue, driven by Germany’s automotive ceramics and France’s nuclear-grade silicon-carbide cladding. CeramTec invested EUR 95 million (USD 102 million) in Plochingen to raise medical-grade zirconia output by 35%. France’s Orano qualified accident-tolerant SiC fuel cladding for commercial reactors in December 2024. South America and the Middle East & Africa together held very less market share in 2025, with Brazil’s refractory demand tied to steel output and South Africa’s alumina supporting mining operations.

Competitive Landscape

The Advanced Structural Ceramics market is moderately fragmented. Kyocera, CoorsTek, and Morgan Advanced Materials maintain cost advantages through powder synthesis, pressing, and machining under single ownership, enabling 25% lower conversion costs than merchants. Patent trends illustrate strategic thrusts. 3M filed 14 ceramic-matrix-composite patents in 2025 aimed at oxidation-resistant fiber coatings. Start-ups exploiting laser-based metal-ceramic joining have attracted more than USD 80 million in venture funding since 2025, targeting 30% assembly-cost reductions.

Advanced Structural Ceramics Industry Leaders

Saint-Gobain

CeramTec GmbH

CoorsTek, Inc.

KYOCERA Corporation

Morgan Advanced Materials plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nigeria inked a USD 1.3 billion investment agreement with the Africa Finance Corporation (AFC). The deal aims to establish an alumina refinery and bolster mineral exploration across the nation.

- October 2025: OSG unveiled the DIA-MXD, a carbide drill tailored for machining ceramics and glass. With its cutting-edge strength, the DIA-MXD ensures stability and durability, making it ideal for these materials.

Global Advanced Structural Ceramics Market Report Scope

Advanced structural ceramics (ASCs) are high-tech, engineered materials designed for superior mechanical strength, hardness, and thermal resistance in extreme environments where metals fail. They are essential for aerospace, automotive, and industrial applications, offering durability under high-stress, corrosive, or high-temperature conditions.

The Advanced Structural Ceramics market is segmented by material type and end-user industry. By material type, the market is segmented into alumina, carbides, zirconate, nitrides, and other. By end-user industry, the market is segmented into automotive, semiconductors, medical, energy, industrial, aerospace and defense (including space), and others. The market report also covers market sizing and forecasts for 18 countries across regions in value (USD).

| Alumina |

| Carbides |

| Zirconate |

| Nitrides |

| Other |

| Automotive |

| Semiconductors |

| Medical |

| Energy |

| Industrial |

| Aerospace and Defense (including Space) |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Alumina | |

| Carbides | ||

| Zirconate | ||

| Nitrides | ||

| Other | ||

| By End-User Industry | Automotive | |

| Semiconductors | ||

| Medical | ||

| Energy | ||

| Industrial | ||

| Aerospace and Defense (including Space) | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the advanced ceramics market in 2031?

The advanced ceramics market size is forecast to reach USD 13.02 billion by 2031.

Which material segment is growing fastest through 2031?

Zirconate ceramics, particularly yttria-stabilized zirconia, are expected to expand at an 8.64% CAGR on the back of dental and turbine-coating demand.

Why are advanced ceramics critical for 800 V electric-vehicle systems?

Their high thermal conductivity and electrical insulation allow silicon-carbide power modules to operate at junction temperatures up to 175°C without derating.

How much revenue share did Asia-Pacific hold in 2025?

Asia-Pacific accounted for 53.91% of global revenue in 2025 due to integrated rare-earth supply chains and precision MLCC manufacturing.

Which end-user industry shows the fastest revenue growth through 2031?

Semiconductors are projected to post a 7.15% CAGR, outpacing industrial and automotive segments.

Page last updated on: