Pulp And Paper Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

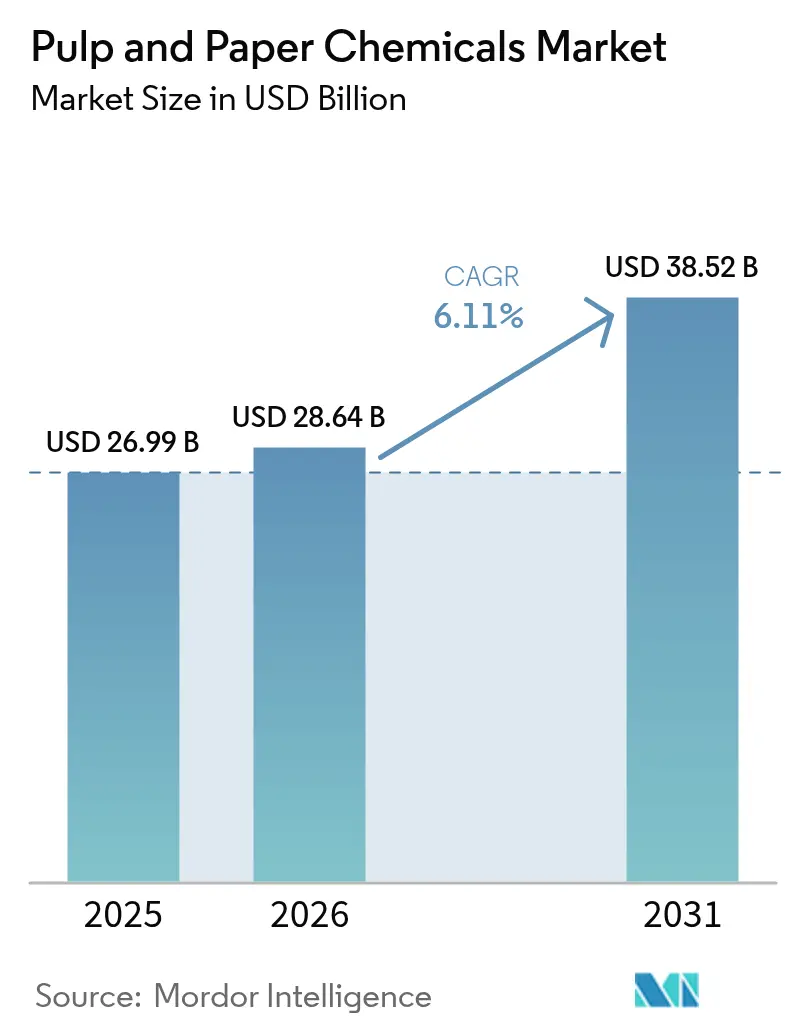

| Market Size (2026) | USD 28.64 Billion |

| Market Size (2031) | USD 38.52 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

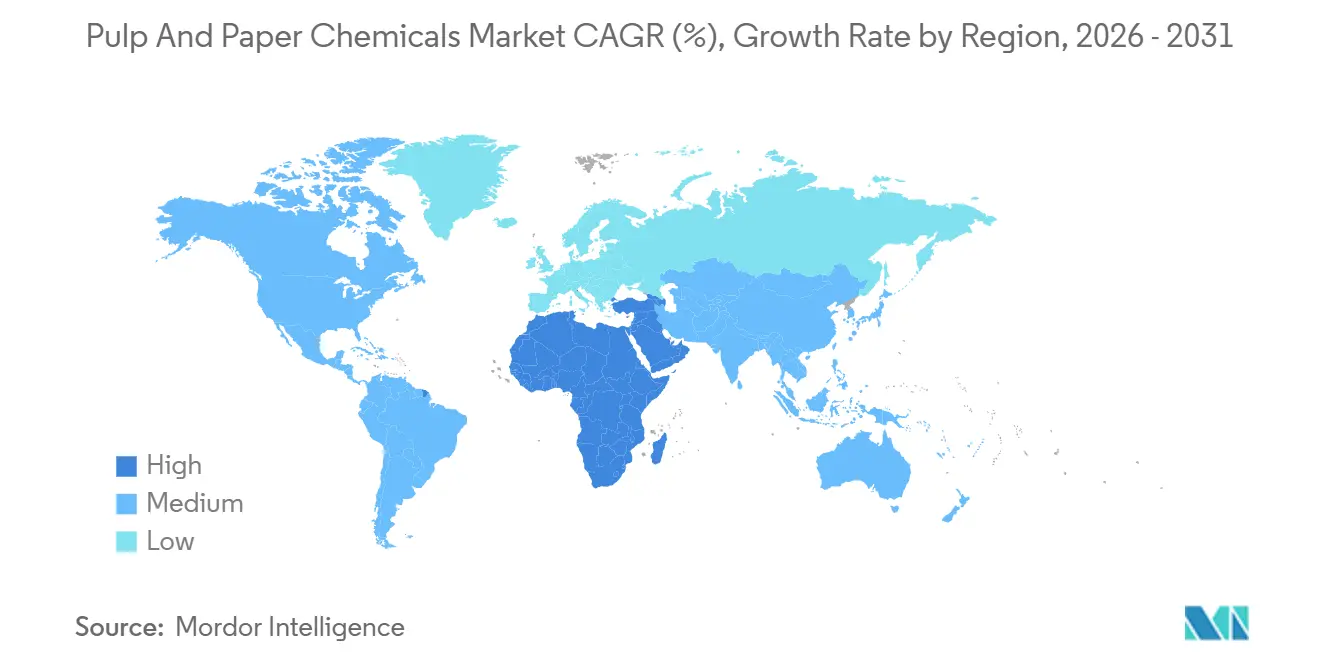

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulp And Paper Chemicals Market Analysis by Mordor Intelligence

The Pulp And Paper Chemicals Market size is expected to increase from USD 26.99 billion in 2025 to USD 28.64 billion in 2026 and reach USD 38.52 billion by 2031, growing at a CAGR of 6.11% over 2026-2031.

A decisive shift toward recycled-fiber furnish, enzyme-enabled processing, and bio-based formulations is anchoring structural growth while shrinking environmental footprints. Bleaching Agents remain the single largest revenue contributor, yet Sizing Agents are scaling faster as mills chase fluorine-free water repellency that satisfies incoming per- and polyfluoroalkyl substance curbs. Global demand also reflects tighter discharge norms that reward oxygen, ozone, and enzymatic sequences over chlorine derivatives. Suppliers are building local capacity next to new mills, which lowers logistics costs and embeds technical service inside process-control loops. Performance guarantees tied to measurable outcomes such as lower adsorbable organic halides or reduced steam per tonne now define contract renewals and margin prospects.

Key Report Takeaways

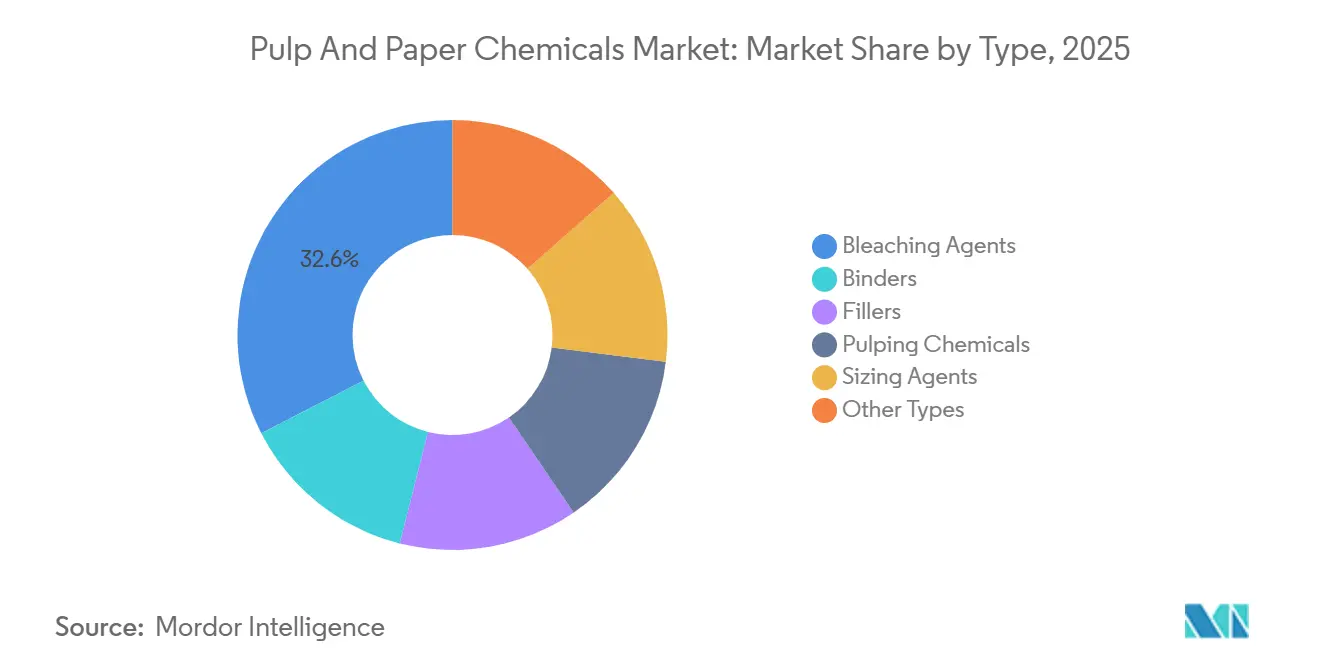

- By type, bleaching agents led the pulp and paper chemicals market with a 32.56% market share in 2025. Sizing agents are forecast to expand at a 6.35% CAGR through 2031.

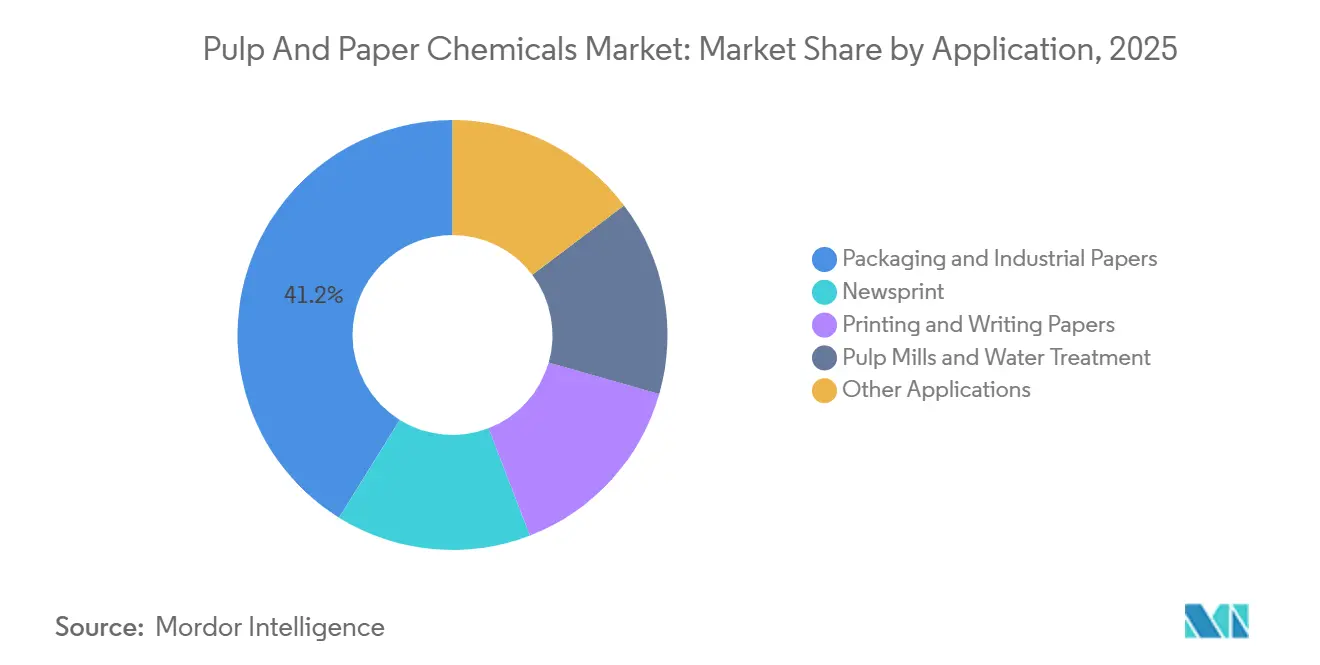

- By application, the packaging and industrial papers segment accounted for a 41.15% share of the pulp and paper chemicals market size in 2025. Pulp mills and water treatment activities are advancing at a 6.31% CAGR through 2031.

- By geography, Asia-Pacific held 46.93% of the Pulp and Paper Chemicals market share in 2025. The Middle East and Africa region is projected to post the fastest growth rate of 6.15% till 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pulp And Paper Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of packaging-grade paper capacity in Asia | +1.8% | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Surge in recycled-fiber furnish adoption | +1.5% | Global, with intensity in Europe and North America | Long term (≥4 years) |

| Water-free enzymatic bleaching breakthroughs | +1.2% | North America and Europe early adopters, Asia-Pacific scale-up | Long term (≥4 years) |

| Carbon-negative bio-based sizing agents | +0.9% | Europe and North America regulatory-driven, Asia-Pacific cost-driven | Medium term (2-4 years) |

| E-commerce led SKU proliferation driving specialty chemicals | +0.7% | Global, concentrated in urban logistics hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of Packaging-Grade Paper Capacity in Asia

Between 2024 and early 2026, China, India, and Indonesia saw the launch of new packaging-grade capacity. This surge has significantly boosted the demand for retention aids, wet-strength resins, and optical brighteners. In August 2026, Kemira launched a sizing plant in Thailand. This facility produces alkyl ketene dimer and alkenyl succinic anhydride grades, aligning with the pace of next-generation corrugators. By localizing chemical production, lead times are shortened for converters catering to cross-border e-commerce hubs. India's 2024 launch of a production-linked incentive program for paper and packaging ensures guaranteed offtake and mitigates greenfield risks. Given that new mills frequently set up in water-stressed areas, they are turning to membrane bioreactors and advanced oxidation, leading to increased spending on coagulants and flocculants. Collectively, these developments provide a multi-year boost to the Pulp and Paper Chemicals market throughout Southeast Asia.

Surge in Recycled-Fiber Furnish Adoption

Recycled fiber now exceeds 60% of global furnish, driven by extended producer responsibility in the European Union and voluntary brand pledges. This migration increases the need for deinking agents, flotation surfactants, and enzyme blends that maintain fiber length while suppressing chemical oxygen demand. Clariant launched Ceridust 1310 in April 2025, a bio-based deinking aid derived from renewable fatty acids, reflecting substitution away from ethoxylates[1]Clariant, “Clariant Launches Ceridust 1310 Bio-Based Deinking Aid,” clariant.com. Mills using recycled pulp consume more retention chemistry per tonne because shorter fibers complicate sheet formation. Although chemical intensity rises, the recycled route remains cost-competitive given high virgin pulp prices and landfill fees on reject streams. The driver keeps the Pulp and Paper Chemicals market aligned with circular economy narratives.

Water-Free Enzymatic Bleaching Breakthroughs

Enzymatic bleaching platforms, operating at moisture levels below 40%, eliminate the need for multi-stage washes. This innovation trims mill water usage significantly and reduces steam demand. In January 2025, Buckman inaugurated a pilot plant in Memphis. The plant successfully validated brightness targets for xylanase and laccase systems, achieving results without the use of chlorine dioxide or hypochlorite. In water-stressed areas of northern China, western India, and the southwestern United States, local tariffs on industrial water have surged. As a result, these regions perceive the technology as a valuable hedge. Currently, early adopters focus on premium printing and tissue grades, which can justify the existing cost premiums. However, the broader adoption in the long run hinges on the scale of enzyme fermentation and the feasibility of modular retrofits in existing bleach plants.

Carbon-Negative Bio-Based Sizing Agents

Sizing agents derived from tall oil, lignin, or algal lipids can achieve net-negative carbon footprints when feedstock sequestration is factored in, as per ISO 14067 protocols. In 2025, Kemira bolstered its Nanjing unit for alkenyl succinic anhydride, introducing a bio-feedstock line tailored to meet Scope 3 criteria, catering to global brand owners. While these agents command a price premium, converters willingly absorb the increase to validate their climate commitments on corrugated shipping boxes. Most packaging grades demonstrate performance parity, though heavy industrial papers still grapple with hydrophobia during aggressive converting. This advancement aligns with the European Union's initiative to limit fluorinated chemistries, propelling the transition to bio-derived alternatives in the Pulp and Paper Chemicals market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening AOX and COD discharge norms | -1.1% | Europe and North America regulatory leaders, Asia-Pacific lagging adoption | Medium term (2-4 years) |

| High energy intensity vis-à-vis alternative substrates | -0.8% | Global, acute in regions with carbon pricing | Long term (≥4 years) |

| Volatility in elemental chlorine prices | -0.6% | North America and Asia-Pacific chlor-alkali dependent regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightening AOX and COD Discharge Norms

In late 2024, the European Union updated its Best Available Techniques Reference Document, tightening the limit on adsorbable organic halides to permissible levels per air-dried tonne[2]European Commission, “Revised Best Available Techniques Reference Document for Pulp and Paper,” ec.europa.eu . Upgrading to ozone stages or extended delignification now demands significant capital investments per line. Mills that can't afford these upgrades face the risk of losing their permits post the 2027 compliance deadline. In 2025, several U.S. states rolled out matching bills, underscoring a global shift towards chlorine-free bleaching. While the regulatory change boosts the demand for alternatives like oxygen, ozone, and enzymes, it also pressures short-term margins, influencing the trajectory of the Pulp and Paper Chemicals market.

High Energy Intensity Versus Alternative Substrates

Traditional pulp and paper operations require significant thermal energy. This is approximately double the energy needed for molded-fiber packaging derived from agricultural residues and three times that of corrugated plastic equivalents. In jurisdictions with carbon pricing, the cost adds to the paper's variable expenses. Brands in the logistics and consumer electronics sectors are now exploring molded pulp and mycelium cushions, steering clear of chemical-intensive sizing. The Pulp and Paper Chemicals market faces constraints, particularly in regions burdened with high carbon fees, due to ongoing energy exposure.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bleaching Agents Lead, Sizing Agents Accelerate

In 2025, Bleaching Agents accounted for 32.56% of the market value, highlighting their pivotal role in achieving brightness targets for both printing and tissue applications. While sodium chlorate, hydrogen peroxide, and chlorine dioxide dominate in volume, there's a notable uptick in peroxide-heavy flows as mills adapt to AOX caps. In response to regional demand, Kemira ramped up its sodium chlorate production in Brazil during Q4 2024. Sizing Agents, despite their smaller volume, are on a rapid ascent, boasting a 6.35% CAGR that surpasses all other categories. The focus is on alkyl ketene dimer and alkenyl succinic anhydride, both of which offer water resistance without the drawbacks of fluorine. Driven by trends in lightweight packaging and digital print grades, the market size for Sizing Agents in Pulp and Paper Chemicals is projected to see steady growth through 2031.

Binders and Fillers, accounting for nearly a quarter of total sales, play a crucial role in coating lines, enhancing both opacity and print gloss. Pulping Chemicals have reached maturity, as new capacities lean towards recycled materials rather than virgin digester builds. Other Types, including defoamers, biocides, and corrosion inhibitors, grow in tandem with overall tonnage. However, they offer a margin advantage, especially where low dosages yield high performance. Arkema, having finalized its acquisition of Dow’s paper-additives assets in January 2025, is now strategically cross-selling specialty emulsion binders. These binders cater to coating rooms, prioritizing low-volatile organic compound formulations. Looking ahead, the Pulp and Paper Chemicals market is steadily shifting focus from traditional commodity tonnage to integrated performance additives, emphasizing technical service and lifecycle metrics.

By Application: Packaging Papers Dominate, Water Treatment Gains Traction

Packaging and Industrial Papers absorbed 41.15% of chemical input in 2025, riding on e-commerce logistics that favor lightweight corrugated boxes. Wet-strength resins, retention aids, and advanced sizing agents secure board integrity while shaving basis weight. Pulp Mills and Water Treatment, though smaller volumes, deliver a 6.31% CAGR that is the application pacesetter as mills install zero-liquid-discharge systems and membrane bioreactors that necessitate premium coagulants, antiscalants, and dispersants. The Pulp and Paper Chemicals market share for these applications is projected to widen further as regulations mature.

Printing and Writing Papers endure secular decline, yet premium art, security, and label grades still demand optical brighteners and surface chemistries that enhance color fidelity. Newsprint contracts in absolute tonnes but increases chemical intensity because higher recycled content requires extra deinking and drainage aids. Tissue and toweling register modest growth as changing hygiene habits offset some substitution from air-dry hand dryers. Modular chemical dosing systems from Ecolab allow large packaging mills to shift recipes in minutes, slashing waste during grade transitions. Divergent growth arcs imply that service models must flex across high-volume cost-sensitive products and technically intensive niches within the overall Pulp and Paper Chemicals market.

Geography Analysis

Asia-Pacific accounted for 46.93% of the 2025 value. China has bolstered its packaging capacity, while India's incentive scheme mitigates financing risks for emerging mills. Kemira's new sizing unit in Thailand enhanced just-in-time deliveries for Southeast Asian converters. Japan and South Korea, albeit at a slower pace, are prioritizing enzyme-based bleaching and bio-sizing upgrades to reduce Scope 3 emissions. Facing scrutiny over deforestation, Indonesia's export-driven pulp producers are turning to chemical vendors for traceability audits, ensuring their feedstocks are sustainable. Collectively, these developments solidify Asia-Pacific's dominance in the Pulp and Paper Chemicals market.

North America and Europe are pushing for carbon-negative sizing and water-free enzymatic bleaching, driven by tighter AOX and COD regulations. Arkema allocated resources to decarbonize its French facilities, aiming to provide low-carbon binders for mills targeting corporate net-zero objectives. Canadian pulp operations are capitalizing on affordable hydroelectric power to safeguard their profit margins. Fluctuating costs of elemental chlorine are prompting experiments with peroxide-ozone methods, which lessen halogen exposure, despite the financial strain of retrofitting. While growth is steady, the regions' innovative spirit ensures their continued influence in shaping the Pulp and Paper Chemicals market.

South America, primarily driven by Brazil's eucalyptus-based kraft pulp industry, underscores its belief in the enduring demand for bleach. Upgrading its facility in Brazil, Nouryon integrated regional technical services. While Argentina and Chile offer specialized grades, logistical challenges have allowed local blenders to capture a larger market share. The Middle East and Africa boast the fastest 6.15% CAGR forecast through 2031. Greenfield mills in Saudi Arabia, Egypt, and South Africa are adopting advanced techniques like oxygen delignification and peroxide sequences from their inception. Turkey, leveraging its strategic logistics position, is channeling investments into high-specification surface sizing to diversify its export routes. These regional disparities fuel a multi-speed growth trajectory in the Pulp and Paper Chemicals market.

Competitive Landscape

The Pulp and Paper Chemicals market is fragmented. Contracts now hinge on verified sustainability metrics such as lower adsorbable organic halides, reduced steam per tonne, and certified bio content. Biotechnology startups are entering with directed evolution enzyme cocktails and lignin-derived sizing agents. Larger incumbents answer with open innovation labs and supply guarantees that bundle process control sensors. Patent filings around algal lipid emulsions suggest near-term competitive skirmishes, though industrial scale may not arrive before 2028. Supplier qualification now almost always invokes ISO 14067 lifecycle audits, favoring players with dedicated sustainability teams and third-party verification budgets. These factors reinforce disciplined yet innovative rivalry inside the Pulp and Paper Chemicals market.

Pulp And Paper Chemicals Industry Leaders

Kemira

BASF

Solenis

Ashland Inc.

Buckman

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kemira announced an investment in multiple production line expansions of strength chemical agents for paper, board, and tissue in Thailand. The implementation of the expansion project is scheduled to begin in 2026.

- March 2025: Nouryon unveiled Eka HP Puroxide, a hydrogen peroxide product boasting a low carbon footprint. This innovation supports Nouryon's clients in the pulp and paper, mining, and water treatment sectors, enabling them to make substantial reductions in their Scope 3 greenhouse gas emissions.

Global Pulp And Paper Chemicals Market Report Scope

Pulp and paper chemicals are the raw materials required to produce paper. These chemicals are mixed with paper pulp to produce paper.

The Pulp and Paper Chemicals Market is segmented by type, application, and geography. By type, the market is segmented into binders, bleaching agents, fillers, pulping chemicals, sizing agents, and other types. By application, the market is segmented into newsprint, packaging and industrial papers, printing and writing papers, pulp mills and water treatment, and other applications. The report offers market size and forecasts for 20 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD).

| Binders |

| Bleaching Agents |

| Fillers |

| Pulping Chemicals |

| Sizing Agents |

| Other Types |

| Newsprint |

| Packaging and Industrial Papers |

| Printing and Writing Papers |

| Pulp Mills and Water Treatment |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Type | Binders | |

| Bleaching Agents | ||

| Fillers | ||

| Pulping Chemicals | ||

| Sizing Agents | ||

| Other Types | ||

| By Application | Newsprint | |

| Packaging and Industrial Papers | ||

| Printing and Writing Papers | ||

| Pulp Mills and Water Treatment | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which chemical type is expanding fastest across paper mills?

Sizing Agents show the quickest growth with a 6.35% CAGR through 2031, driven by fluorine-free water repellency needs.

Which region contributes the largest spend on pulp and paper chemicals today?

Asia-Pacific leads with 46.93% of the 2025 value, thanks to ongoing packaging capacity buildouts in China, India, and Indonesia.

How strict AOX limits influence chemical selection?

Lower AOX caps push mills to adopt oxygen, ozone, and enzymatic bleaching systems, trimming reliance on chlorine derivatives.

Why are water-free enzymatic bleaching systems gaining traction?

They cut mill water use and steam consumption, which lowers utility costs and eases discharge compliance.

What is the current global demand for pulp and paper chemicals market and its expected growth by 2031?

Global consumption is USD 28.64 billion in 2026 and is projected to reach USD 38.52 billion by 2031, reflecting a 6.11% CAGR.

Page last updated on: