Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The High Temperature Sealant Market Report is Segmented by Chemistry (Silicone, Epoxy, Other Chemistries), End-User Industry (Electrical and Electronics, Automotive and Transportation, Chemical and Pharmaceutical, Building and Construction, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

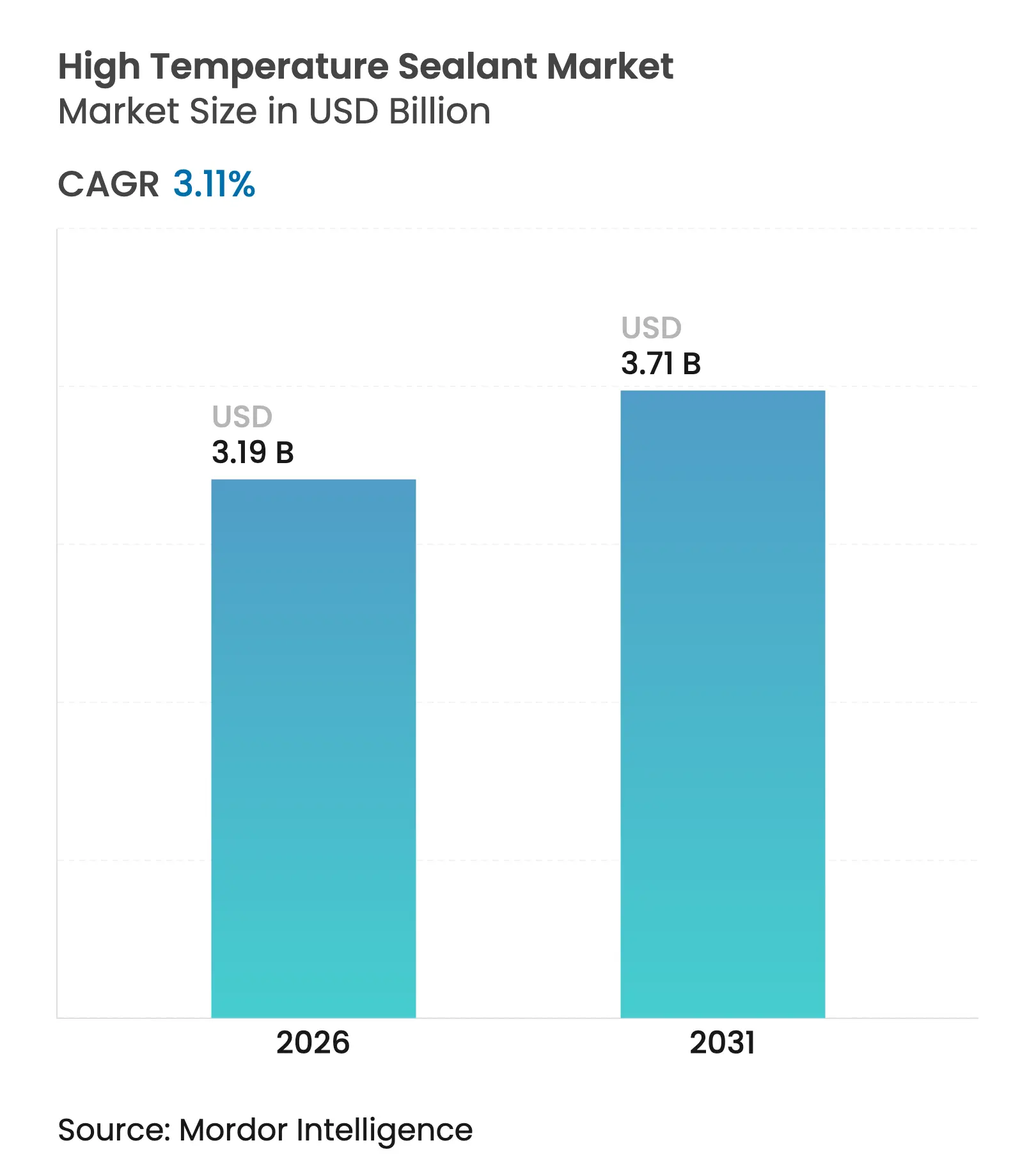

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 3.11 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The High Temperature Sealant Market size was valued at USD 3.09 billion in 2025 and estimated to grow from USD 3.19 billion in 2026 to reach USD 3.71 billion by 2031, at a CAGR of 3.11% during the forecast period (2026-2031). Stable demand from electric-vehicle battery packs, concentrated solar-power receivers, and advanced electronics assemblies keeps the high temperature sealant market on a steady growth path. Silicone remains the anchor chemistry thanks to unmatched thermal stability, while polyimide, epoxy, and acrylic systems gain ground in mission-critical niches that push operating temperatures beyond the silicone comfort zone. Growth momentum is strongest in Asia-Pacific, where dense manufacturing clusters in China, Japan, and India continue to scale output of power electronics and automotive components. Concurrently, North American and European producers focus on low-VOC reformulations and specialty grades that address strict environmental statutes. Supply-chain vulnerability around high-purity quartz after Hurricane Helene and ongoing energy-transition capital spending both shape procurement and R&D agendas across the high temperature sealant market.

Key Report Takeaways

*Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Demand from Electrical and Electronics Assemblies

Growing Demand from Electrical and Electronics Assemblies

| +1.5% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.5%

|

Geographic Relevance

:

Global, with concentration in Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Accelerating EV and Hybrid-Vehicle Thermal-Management

Needs

Accelerating EV and Hybrid-Vehicle Thermal-Management

Needs

| +0.8% | North America, Europe, China | Short term (≤ 2 years) | |||

Expansion of Aerospace and Defence High-Temp Applications

Expansion of Aerospace and Defence High-Temp Applications

| +0.6% | North America, Europe | Long term (≥ 4 years) | |||

Scheduled Refinery / Petrochemical Turnaround Cycles

Scheduled Refinery / Petrochemical Turnaround Cycles

| +0.3% | Global, with emphasis on Middle East, North America | Medium term (2-4 years) | |||

Adoption In Concentrated Solar-Power Receiver Seals

Adoption In Concentrated Solar-Power Receiver Seals

| +0.2% | Middle East, North Africa, Southwest USA | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Demand from Electrical and Electronics Assemblies

Higher power density chips now run at junction temperatures well above 200 °C, so packaging houses rely on thermally conductive silicone sealants for die-attach, underfill, and lid seal operations. Wide-bandgap semiconductors such as silicon-carbide and gallium-nitride exacerbate heat load, while 5G radios and edge servers push even more wattage into smaller footprints[1]Mihai Banu, “Thermal Interface Materials for GaN Devices,” MDPI, mdpi.com. These pressures elevate thermal-cycling stress, making durable sealing indispensable in Asia-Pacific megafabs that dominate global output. Consistent product quality, automated dispensing, and rapid cure profiles position specialty silicones as the default choice across this part of the high temperature sealant market.

Accelerating EV and Hybrid-Vehicle Thermal-Management Needs

Battery packs typically integrate up to 5 liters of thermal interface material, and each cubic centimeter of that material must stay intact from −40 °C to 85 °C while resisting electrolyte exposure. The shift toward 800 V powertrains and faster charging sharpens thermal gradients, so automakers specify silicone sealants with thermal conductivity of 3 W/m·K or higher. Adhesion must also endure vibration and torsion, especially in skateboard chassis designs. China, Europe, and the United States therefore remain priority markets for new high temperature sealant market introductions targeting e-mobility assembly lines.

Expansion of Aerospace and Defence High-Temp Applications

Modern turbofan cores operate hotter to raise efficiency, creating exhaust zones that approach 982 °C. Sealants must keep elasticity and chemical integrity in the presence of aviation fuels, hydraulic fluids, and missile exhaust plumes. Hypersonic vehicle prototypes impose even harsher profiles, pushing development of ceramic-filled silicone and polyimide systems capable of service beyond 1,500 °C. North American and European defense budgets sustain this demand, ensuring long-term support within the high temperature sealant market.

Scheduled Refinery / Petrochemical Turnaround Cycles

Turnarounds occur every three to five years and involve wholesale gasket and seal replacement on units running at 427 °C and 2,000 psi. Operators seek reliable materials that minimize unscheduled outages, especially when processing heavier crude grades. Refineries in the Middle East and Gulf Coast allocate sizeable budgets to high-temperature sealing kits, locking in predictable, counter-cyclical revenue streams for suppliers.

*Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent VOC and Hazardous-Substance Regulations

Stringent VOC and Hazardous-Substance Regulations

| -0.4% | North America, Europe | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

North America, Europe

|

Impact Timeline

:

Short term (≤ 2 years)

|

Cost Pressure from Lower-Temp Alternative Chemistries

Cost Pressure from Lower-Temp Alternative Chemistries

| -0.6% | Global, with emphasis on cost-sensitive markets | Medium term (2-4 years) | |||

Supply

Volatility of High-Purity Silica and Specialty Polymers

Supply

Volatility of High-Purity Silica and Specialty Polymers

| -0.3% | Global, with concentration in North America, Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent VOC and Hazardous-Substance Regulations

California’s Rule 1168 caps VOC content in many sealant lines at 250 g/L, forcing formulators to adopt 100% solids or water-borne systems. The European Union’s REACH framework adds labeling and preregistration costs, favoring large producers with robust regulatory teams. Reformulating high temperature products without sacrificing thermal stability poses technical hurdles, particularly for solvent-borne chemistries.

Cost Pressure from Lower-Temp Alternative Chemistries

Polyurethane and acrylic compounds rated to 200 °C cost 20–40% less than premium silicone. In construction or consumer appliances, engineers increasingly downgrade to these moderate-temperature options to save unit cost. Hybrid systems that blend acrylic bulk with high-temperature fillers now encroach on parts of the high temperature sealant market once considered silicone strongholds, creating margin compression for premium suppliers.

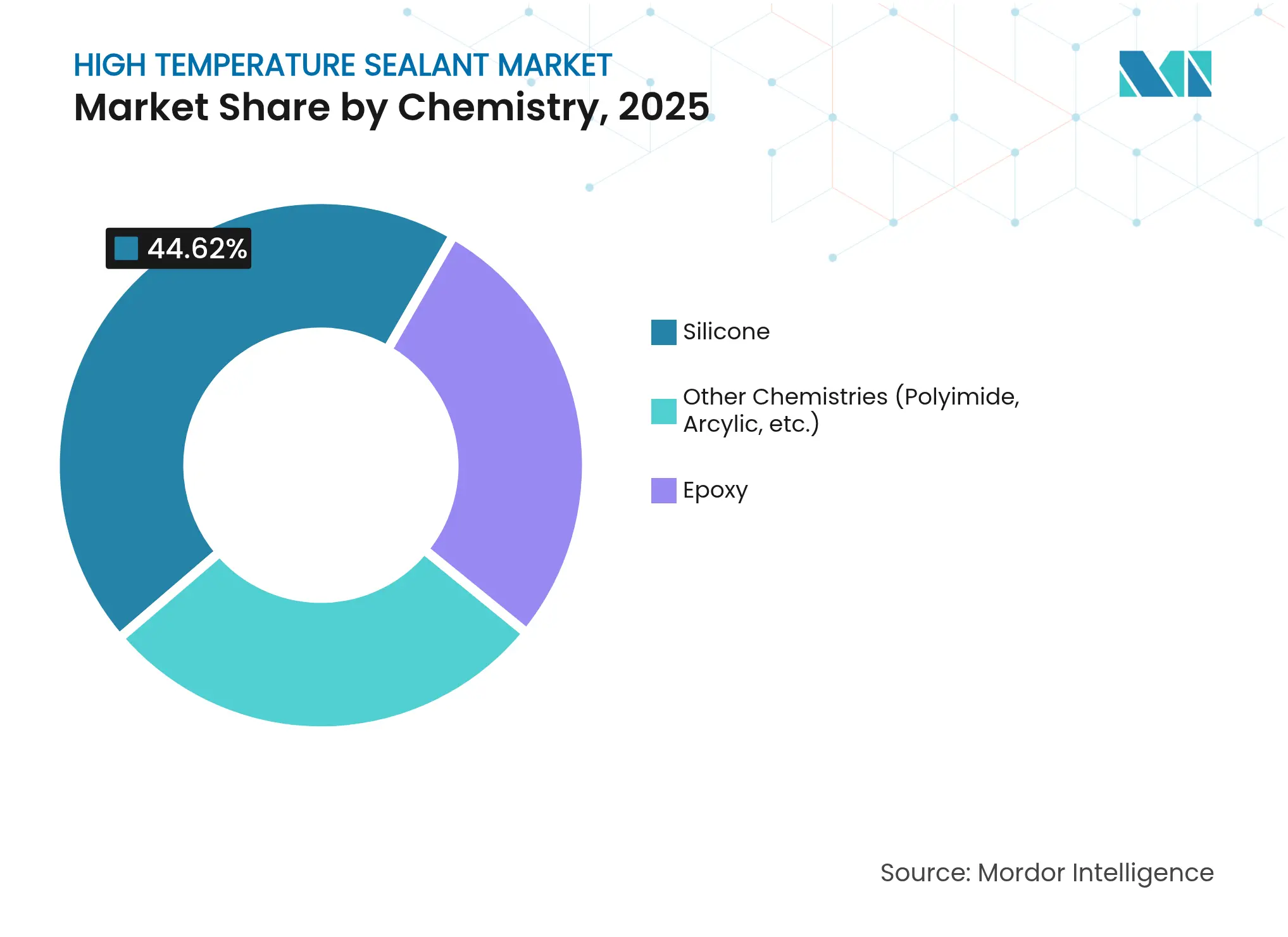

By Chemistry: Silicone Dominance Faces Specialty Competition

Silicone captured 44.62% of high temperature sealant market share in 2025, supported by proven stability from −65 °C to 300 °C and compatibility with automated dispensing. Phenyl-modified grades push upper service limits to 478 °C while silver-coated glass fillers introduce electrical conductivity for heat-spreader attach lines. This technology depth keeps silicone at the core of the high temperature sealant market despite new contenders.

Polyimide, epoxy, and specialty acrylic chemistries together are forecast to grow at 3.93% CAGR, reflecting escalating requirements beyond silicone’s upper threshold. Polyimide excels in jet-engine nacelles, while epoxy grades dominate in electronics potting where rigidity and chemical resistance trump flexibility. The overall high temperature sealant market size for these alternatives is projected to expand steadily as aerospace, defense, and niche renewable segments outsource higher operating-temperature envelopes.

Note: Segment shares of all individual segments available upon report purchase

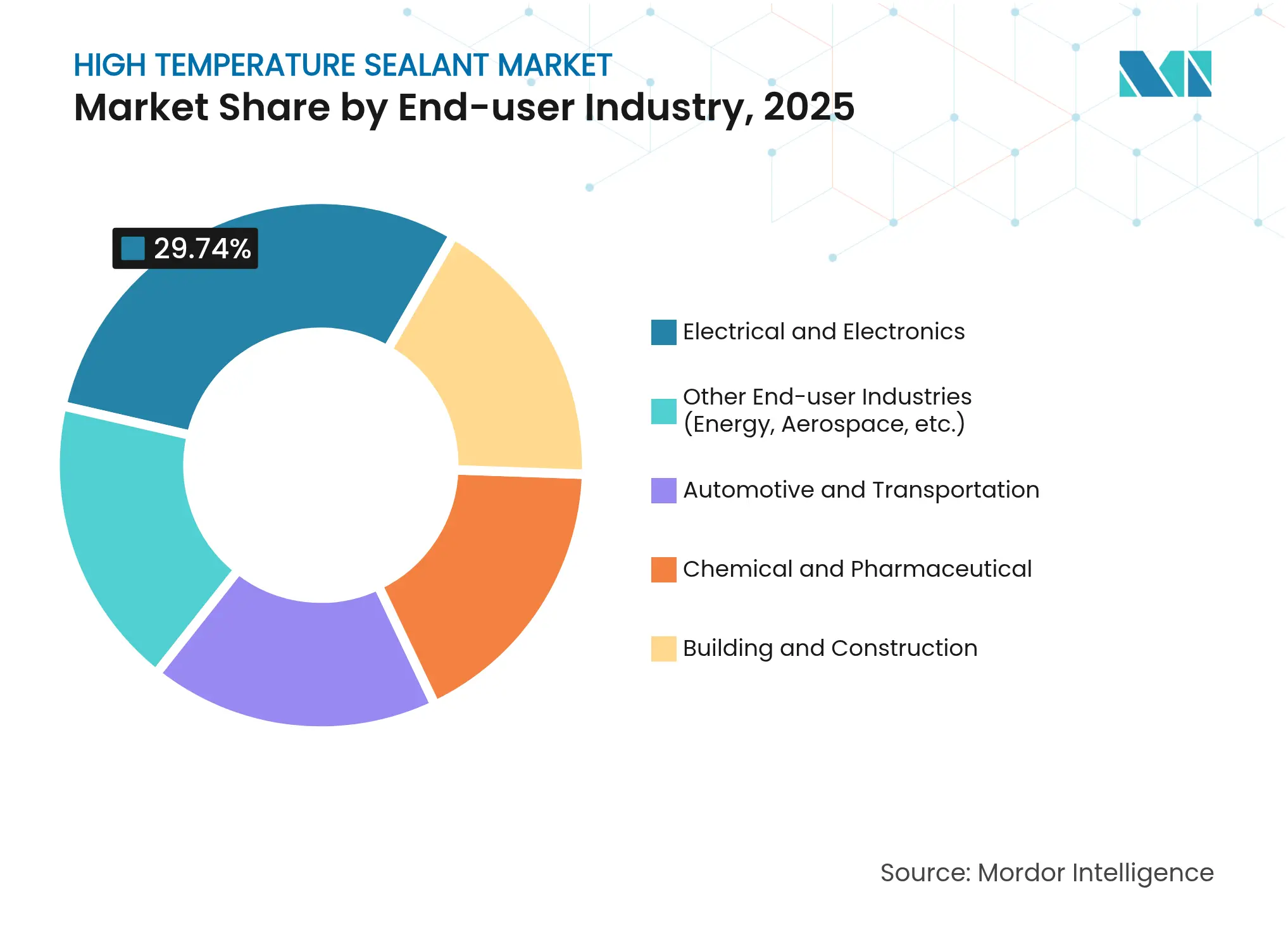

By End-User Industry: Electronics Leadership Amid Diversification

Electrical and electronics absorbed 29.74% of the high temperature sealant market size in 2025 as shrinking die footprints concentrated heat flux across solder bumps and underfills. Power-converter modules in wind turbines and solar inverters use silicone gels to manage differential expansion while protecting wire bonds at 175 °C junction temperatures. Emerging 3D-chiplet packaging further reinforces demand for resilient sealants.

Aerospace, new-energy, and other specialized sectors are projected to grow at 4.09% CAGR. Electric-vehicle battery-pack sealing, hydrogen electrolyzer stacks, and concentrated solar receiver flanges all require materials capable of spanning hundreds of degrees while resisting hydrocarbons or molten salts. These newer outlets diversify revenue and insulate the high temperature sealant market from cyclical swings in single sectors.

Note: Segment shares of all individual segments available upon report purchase

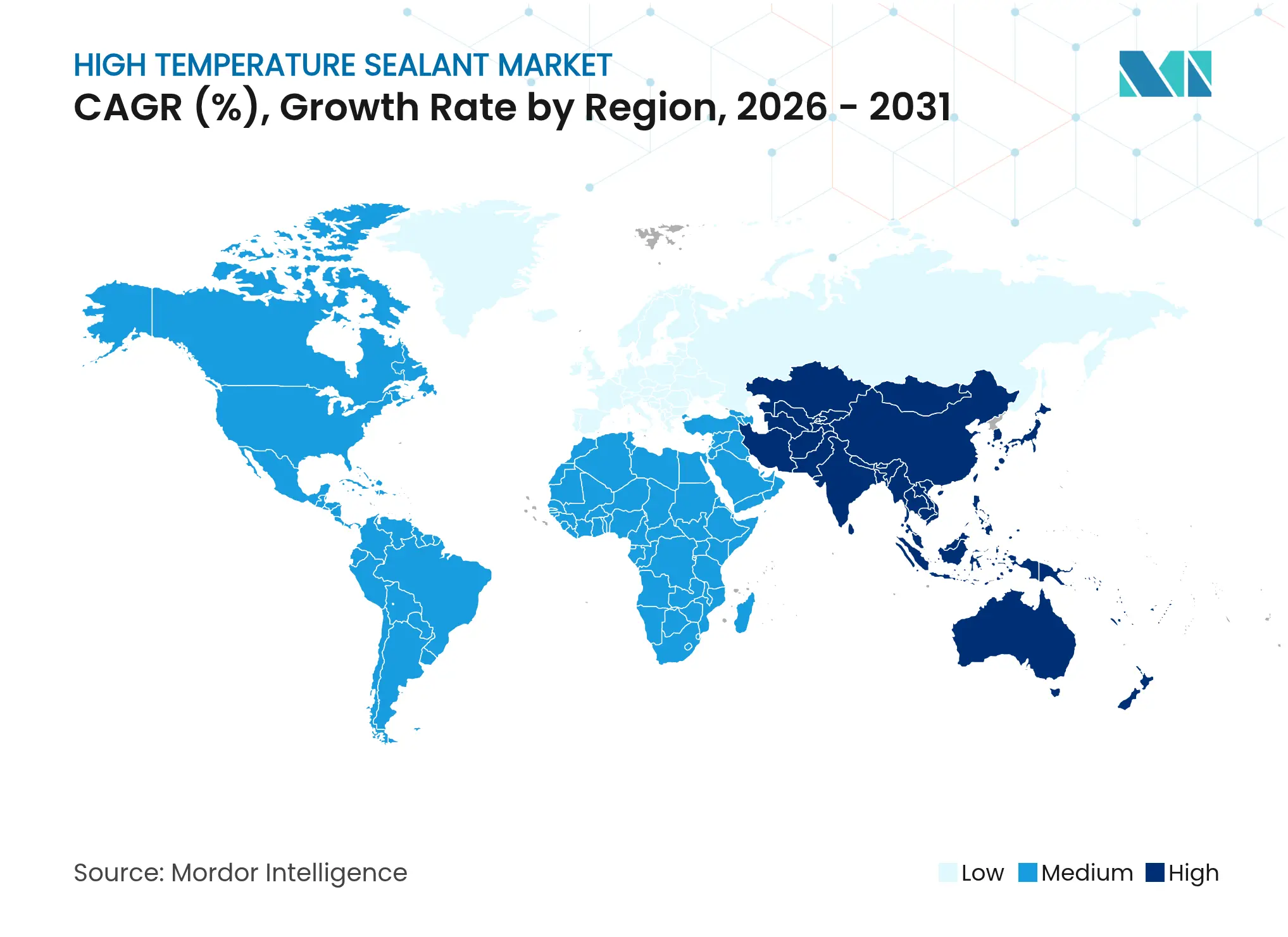

Asia-Pacific leads the high temperature sealant market with 41.35% share in 2025, driven by technology clusters spanning Beijing to Bengaluru. China’s semiconductor buildup raises demand for thermally conductive silicone pastes in flip-chip lines, while Japanese automakers adopt high-voltage battery designs that elevate service temperatures. India’s pharmaceutical reactors also rely on polyimide gaskets tested to 300 °C. Emerging ASEAN hubs such as Thailand attract investment, evidenced by Sekisui’s 8 billion yen film plant in Rayong that anchors local specialty material demand.

North America remains pivotal for specialty aerospace and defense applications that specify ultra-high-temperature sealants above 500 °C. The Gulf Coast refinery corridor triggers predictable turnaround cycles and sizable orders for graphite-packed expansion joints. Mexico’s role as an EV assembly base adds incremental demand, especially for battery and power-electronics sealing.

Europe emphasizes sustainability and regulation. German Tier-1 automotive suppliers require REACH-compliant silicones that still pass fire-safety norms, while the United Kingdom’s civil-aerospace sector validates every batch of polyimide adhesive against flammability and compression-set criteria. Southern Europe’s concentrated solar-power pipeline, notably in Spain, deploys sodium-silicate sealants capable of daily cycling between ambient and 700 °C. Collectively, these dynamics ensure that the high temperature sealant market continues evolving across the continent in line with green-deal policy goals.

Market Concentration

The high temperature sealant market features moderate fragmentation yet visible consolidation momentum. Global majors such as Arkema, Henkel, and Dow combine multi-plant scale with application engineering teams that embed products at the design phase. Sika lifted 2024 revenue 7.4% in local currencies by integrating recent roofing and building-sealant acquisitions, thereby widening cross-selling potential for its heat-resistant lines[2]Sika AG, “Acquisition Strategy and Market Expansion,” Sika.com. Henkel launched UV-curable potting compounds that pass immediate high-pressure testing, shortening customer production cycles. Dow broadened photovoltaic offerings with the DOWSIL PV platform that secures frames at sustained temperatures near 150 °C.

Midsize players pursue regional footholds through ceramic-filled specialty offerings tailored for hypersonic flight, molten-salt valves, and lithium-ion fire barriers. Supply-chain resilience ranks high on procurement scorecards after raw-material shocks in 2024, steering OEMs toward partners with backward-integrated quartz or siloxane monomer assets. Digital formulation tools, additive manufacturing, and automated dispensing equipment round out the competitive differentiators reshaping the high temperature sealant market.

Start-up innovators look to bio-based silicone analogues and energy-efficient curing methods, aligning product roadmaps with circular-economy targets in Europe. Meanwhile, Asian conglomerates continue to boost in-house sealant production that supports captive electronics and automotive operations. Across all tiers, the constant thread is investment in testing laboratories that certify performance above 400 °C, reflecting customer intolerance for thermal failure in electrified, mission-critical equipment.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The high temperature sealant market report include:

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.