3D Concrete Printing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

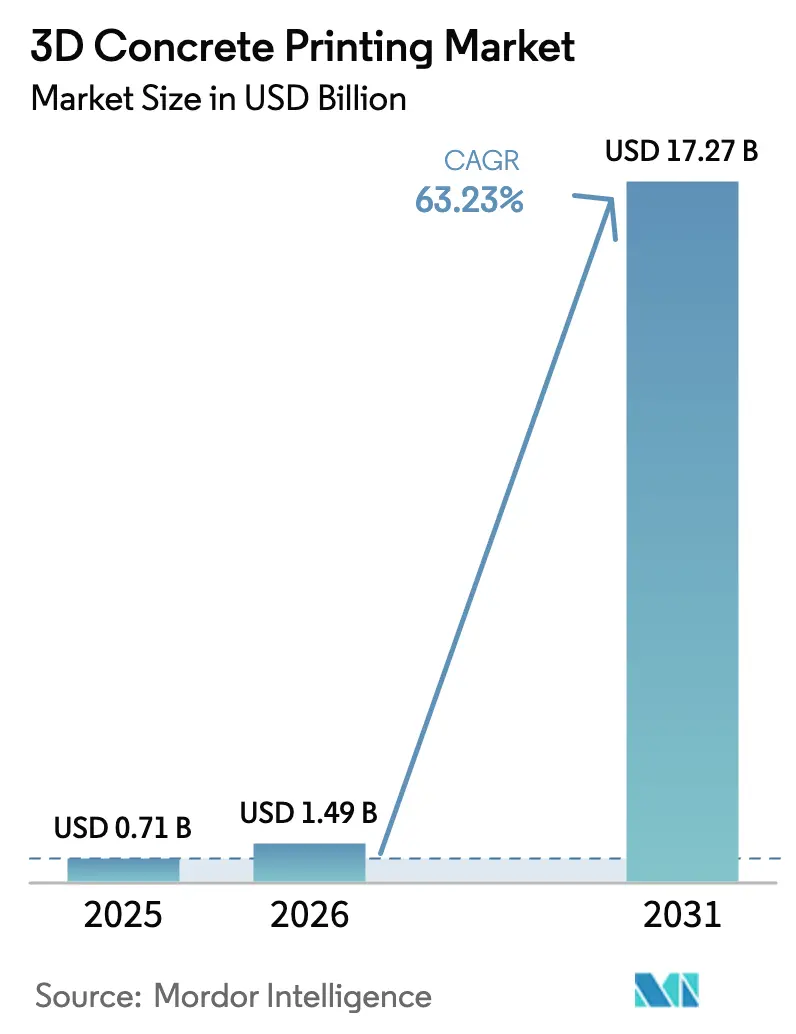

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 17.27 Billion |

| Growth Rate (2026 - 2031) | 63.23% CAGR |

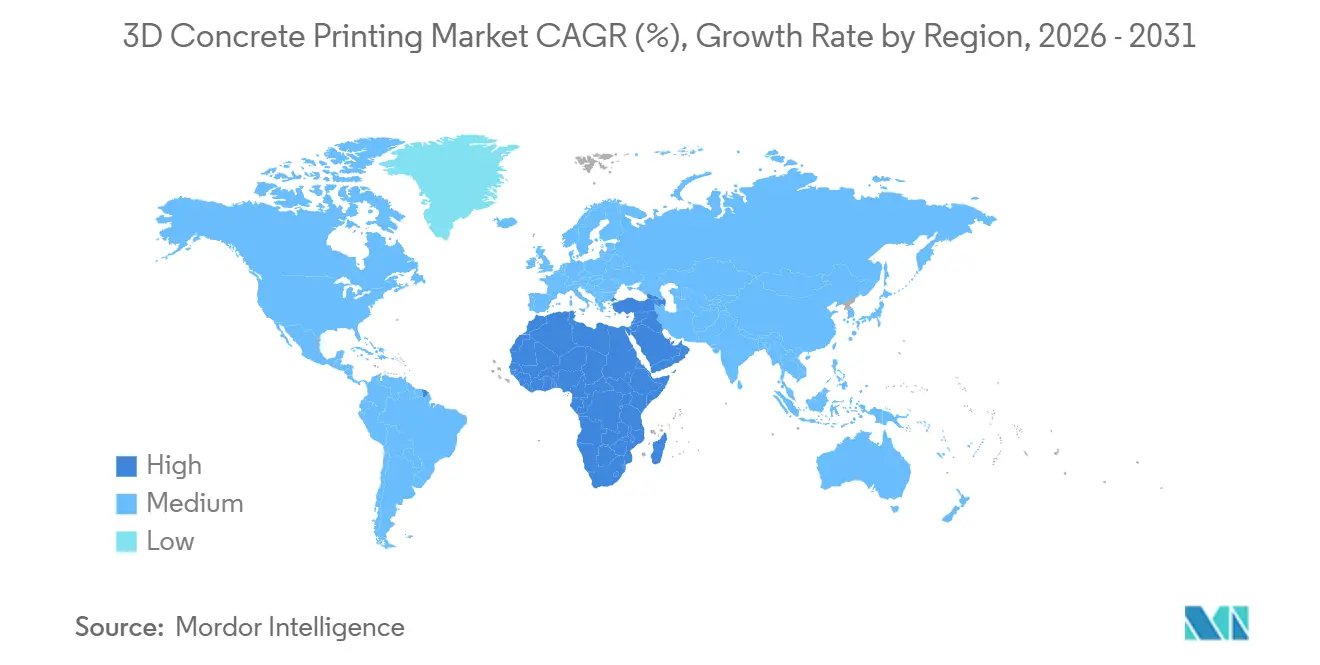

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Concrete Printing Market Analysis by Mordor Intelligence

The 3D Concrete Printing Market size is expected to grow from USD 0.71 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 17.27 billion by 2031 at 63.23% CAGR over 2026-2031. Robust momentum comes from the first mainstream building-code pathways, rapid material-science progress, and urgency to trim project cycle times. The ICC’s AC509 criteria and UL’s 3401 evaluation standard eliminated the need for case-by-case approvals, unlocking commercial financing and insurance coverage. Demonstrations such as the U.S. Army Corps of Engineers’ 46 m² barracks printed in under 40 hours showed labor savings of 75% and negligible waste. Asia-Pacific leads adoption as China’s prefabrication mandates and India’s affordable-housing targets converge with skilled-labor shortages. Meanwhile, architects worldwide are shifting to high-performance mixes that achieve compressive strengths above 100 MPa, enabling thinner shells and cantilevered facades without formwork. Equipment cost remains a drag, yet hybrid factory-printed panels combined with on-site assembly are broadening the addressable customer base.

Key Report Takeaways

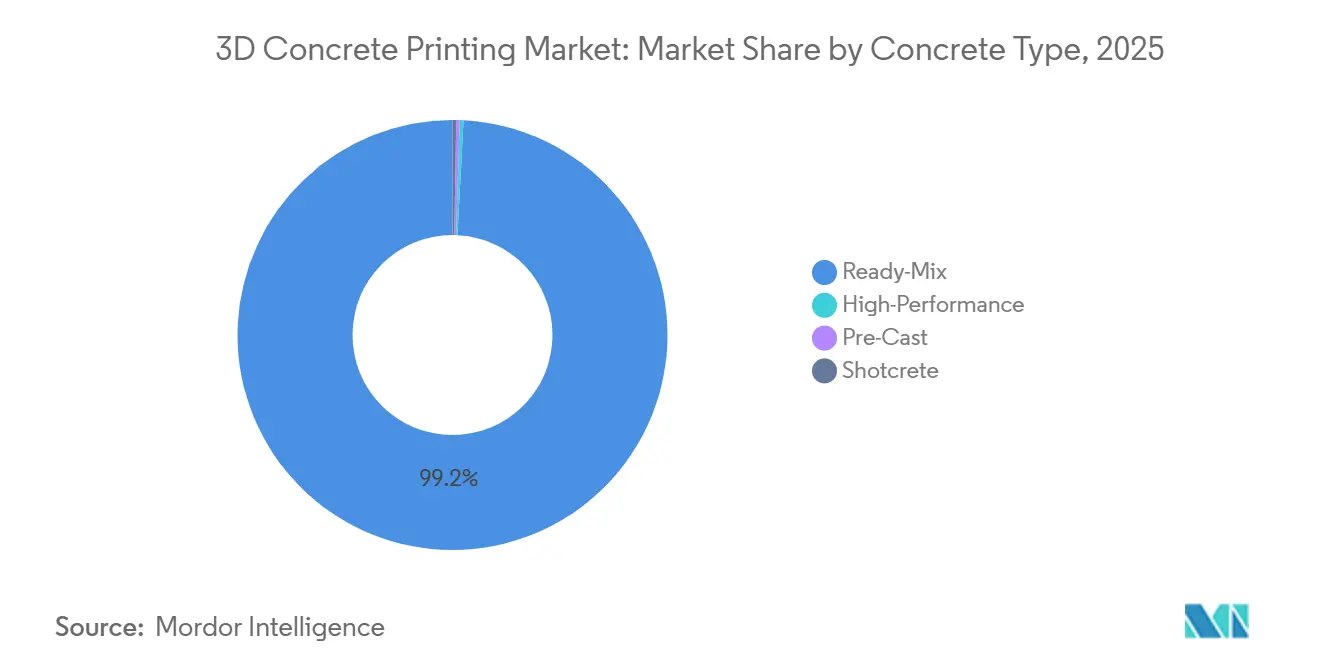

- By concrete type, ready-mix held 99.20% of the 3D concrete printing market share in 2025. High-performance mixes are forecast to expand at a 78.77% CAGR between 2026 and 2031.

- By product type, panels and lintels captured 65.94% of 2025 revenue in the 3D concrete printing market size and are advancing at a 74.78% CAGR through 2031.

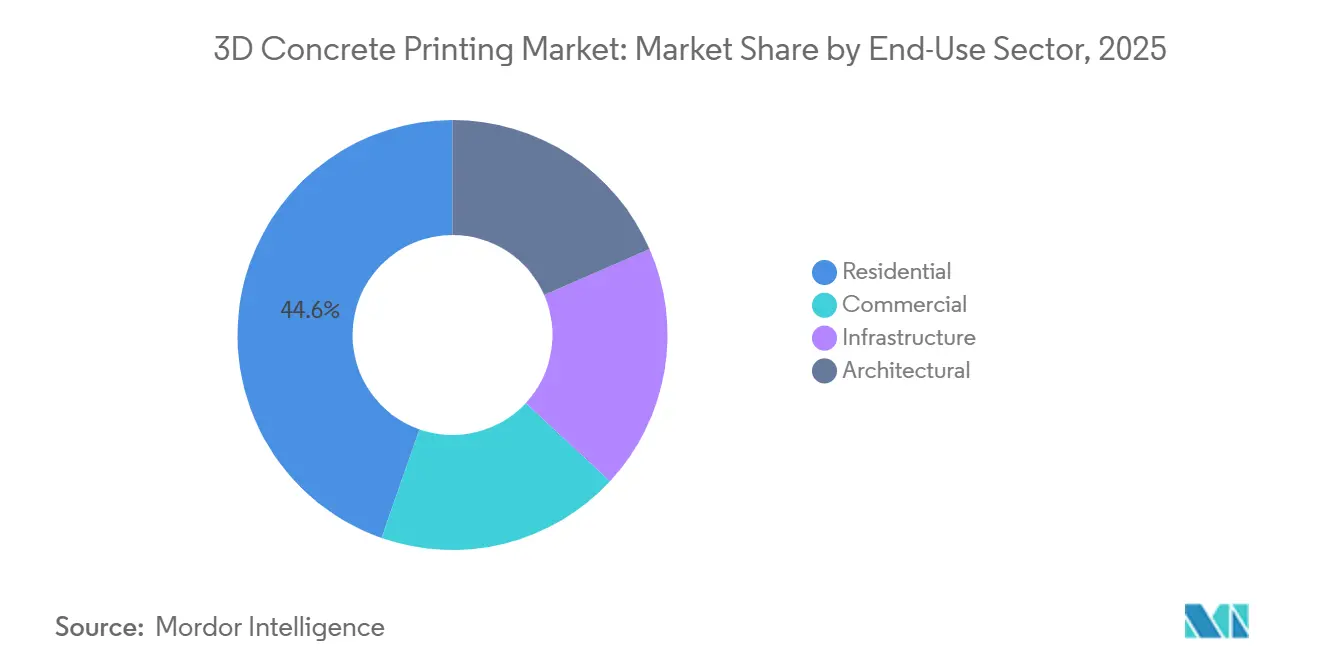

- By end-use, residential accounted for 44.64% of 2025 demand, while architectural applications are growing at a 72.05% CAGR.

- By geography, Asia-Pacific commanded a 55.54% 3D concrete printing market share in 2025. Whereas the Middle-East and Africa are growing at a 77.64% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 3D Concrete Printing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost- and time-efficient automated construction | +18.5% | Global, with early concentration in North America, APAC urban corridors | Short term (≤ 2 years) |

| Infrastructure boom and affordable-housing demand in Asia-Pacific | +15.2% | APAC core (China, India, ASEAN), spill-over to MEA | Medium term (2-4 years) |

| Sustainability push for low-waste/low-carbon building | +12.8% | Europe, North America, APAC (Japan, South Korea) | Long term (≥ 4 years) |

| Defense and disaster-relief adoption of printed shelters | +8.4% | North America (DoD), Europe (NATO), disaster-prone APAC regions | Medium term (2-4 years) |

| Regulatory breakthroughs (ICC-ES AC509, UL 3401 ESRs) | +6.9% | North America, gradual adoption in Europe and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost- and Time-Efficient Automated Construction

While labor productivity in construction has remained stagnant for decades, additive systems are revolutionizing the industry. These systems not only eliminate the need for formwork but also significantly reduce labor hours and minimize waste. A prime example is ICON’s 100-home project at Wolf Ranch in Texas, which showcases a streamlined approach: a two-day wall printing followed by conventional roofing and MEP fit-out. Military assessments echo these economic benefits, demonstrating that four-person teams can set up robust shelters in just 48 hours for expeditionary bases[1]U.S. Marine Corps Systems Command, “Expeditionary Advanced Base Operations,” marcorpsyscom.marines.mil. Such efficiencies are particularly crucial in markets like Japan, which experienced a workforce decline between 2015 and 2025.

Infrastructure Boom and Affordable-Housing Demand in Asia-Pacific

India's ambitious Pradhan Mantri Awas Yojana targets new urban homes by 2030. However, current capacities reveal a shortfall. In Chennai, Tvasta's printed prototype achieved a reduction in build time. By 2027, China is set to require prefabricated components to make up tier-1 residential projects, leading to a surge in bulk orders for factory-printed slabs. Meanwhile, the Asian Development Bank's robust infrastructure pipeline underscores a consistent demand for printed pedestrian bridges and culverts.

Sustainability Push for Low-Waste/Low-Carbon Building

Concrete is a major contributor to global CO₂ emissions. However, innovative techniques are emerging to mitigate this impact. Additive layering can significantly reduce concrete volume and is compatible with clinker-reduced binders. Heidelberg Materials has developed a printable mix that reduces clinker content, resulting in a lower embodied carbon footprint[2]Heidelberg Materials, “i.tech 3D Sustainability Report 2025,” heidelbergmaterials.com. Starting in 2026, Europe’s Carbon Border Adjustment Mechanism will incentivize the use of domestic low-carbon components. Meanwhile, LC3 technology, a brainchild of ETH Zurich, substitutes a portion of traditional Portland cement with calcined clay and limestone. This not only maintains the essential thixotropy for layer adhesion but also achieves a commendable reduction in embodied carbon.

Defense and Disaster-Relief Adoption of Printed Shelters

In its FY 2024 budget, the U.S. Department of Defense allocated funds for field-deployable printers. NATO's Arctic exercise in 2025 confirmed that command posts could be printed in sub-zero temperatures within a swift timeframe. Meanwhile, pilots conducted by UNHCR in Jordan demonstrated the ability to print shelters quickly, underscoring the urgency of humanitarian needs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for printers and ancillaries | -4.2% | Global, most acute in emerging markets with limited access to equipment financing | Short term (≤ 2 years) |

| Non-standardized printable-mix formulations and codes | -3.1% | Global, with fragmentation highest in APAC and Latin America | Medium term (2-4 years) |

| Urban-site logistics limits for large gantry systems | -2.6% | Dense urban centers in APAC, Europe, select North American metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Printers and Ancillaries

Purchasing a COBOD BOD2 gantry, which boasts a 14.6 m span, comes with a significant price tag. However, to fully equip it with essential pumps, mixers, and generators, an additional investment is required. The leasing market for such equipment is limited, and those who do venture into it face a steep interest rate. This is largely due to financiers' lack of depreciation data. Furthermore, in India, duties on imported robotics can accumulate to a hefty percentage, posing a significant challenge in the emerging market.

Non-Standardized Printable-Mix Formulations and Codes

Despite using identical recipes, labs experience a variation in layer adhesion, highlighting differences in mixing and humidity conditions. Consequently, each project allocates a budget for site-specific rheology tests. In Japan and India, printed structures are still deemed non-conventional, necessitating ministerial-level approvals and causing delays in project starts.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Concrete Type: Ready-Mix Dominance Masks High-Performance Surge

Ready-mix secured 99.20% of the 3D concrete printing market in 2025, riding on ubiquitous supply chains and contractor familiarity. Most sites adapt local ready-mix with viscosity-modifying admixtures dosed on site. High-performance concrete, however, is accelerating at a 78.77% CAGR as compressive strengths above 100 MPa enable 50 mm-thick walls that free valuable floor area. ACI studies show that ultra-high-performance formulations cut material volume while meeting identical load ratings. In many low-rise applications, fiber reinforcement has replaced the need for rebar. However, when fiber content exceeds a certain threshold, nozzle clogging becomes an issue, necessitating iterative testing.

The diversification continues: geopolymer mixes activated by sodium silicate offer near-zero embodied carbon but require 60 °C curing, limiting them to factory settings. Pre-cast workflows leverage factory control to print wall panels and floor slabs, minimizing weather delays prevalent in on-site printing. Shotcrete variants are entering tunnel-repair use cases where rapid setting and adhesion matter most. These trends signal a gradual migration from commodity to engineered mixes as second-wave adopters prioritize design freedom and sustainability.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Panels and Lintels Lead Modular Shift

Panels and lintels delivered 65.94% of 2025 revenue in the 3D concrete printing market and are expanding at a 74.78% CAGR as developers favor hybrid construction. Factory-printed wall panels, featuring embedded conduits, have reduced on-site assembly time to just four hours per unit. Meanwhile, lintels with hollow cores have significantly cut formwork costs.

While floors and roofs have been slower to adopt, they are now gaining momentum. Using suspended-nozzle techniques, they are able to print ceiling layers without the need for elaborate falsework. Helical staircases have carved out a profitable niche, especially after CyBe managed to print a spiral staircase at a cost lower than precast alternatives. Additionally, architectural street furniture—ranging from planters and benches to acoustic baffles—has introduced a premium design segment to the market. Given that inspectors and insurers view factory-printed modules as lower risk, modular workflows are seeing faster approval times, leading to broader adoption beyond just the early adopters.

By End-Use Sector: Residential Scale Meets Architectural Ambition

Residential projects held 44.64% of 2025 demand as national housing programs in India, China, and Saudi Arabia specified aggressive unit counts and timelines. ICON demonstrated 48-hour wall printing for single-family homes, beating wood-frame workflows on speed even before accounting for waste reduction.

Infrastructure and architectural segments, though smaller in volume, are the fastest-growing. The architectural sub-segment is advancing at a 72.05% CAGR as museums and transit hubs commission doubly-curved facades and acoustically graded panels impossible with standard casts. The Smithsonian’s Hirshhorn renovation tuned reverberation across galleries using variable-porosity printed panels. Dubai’s Museum of the Future employed stainless-steel-reinforced printed concrete to achieve its torus-shaped skin. Infrastructure use cases, such as pedestrian bridges, validated long-term durability; the Netherlands’ 2017 printed bridge still shows no structural degradation.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific maintained 55.54% of global 3D concrete printing market share in 2025. China's push for a prefabrication mandate by 2027 is fueling a surge in factory orders. Meanwhile, WinSun's successful five-story apartment block in Suzhou has validated the feasibility of mid-rise constructions. With an urban housing deficit, India is turning to 3D printing as a cost-effective solution. Japan, grappling with a dwindling labor force, is hastening the adoption of robotic printing, enabling two-person teams to complete detached homes. In 2024, South Korea allocated a substantial amount for public-housing pilot projects. Additionally, the ASEAN region's ongoing infrastructure projects are bolstering the demand for printed culverts and bus shelters.

North America is capitalizing on its early regulatory advantages. The introduction of AC509 and UL 3401 has eliminated uncertainties in permitting, enabling swift approvals from lenders and insurers. In 2024, a significant funding round for ICON facilitated the expansion of its Vulcan printer, catering to residential, military, and commercial sectors. To tackle the challenges of northern climates, Canada has set up a cold-weather test facility in Ottawa, focusing on freeze-thaw durability. In Tabasco, Mexico, INFONAVIT is making strides by printing homes at an impressive rate, achieving rapid build times.

Europe's embrace of 3D concrete printing is largely influenced by stringent carbon policies and a precast industry keen on integrating this new technology. Germany's endorsement of PERI's printed walls has set a precedent, guiding other EU nations. Heidelberg Materials is proactively aligning its clinker-reduced mix with the EU's impending carbon tariffs, set to roll out in 2026. France and the Netherlands are at the forefront, championing major infrastructure initiatives like XtreeE's Paris footbridge, designed to endure heavy traffic. While the UK is making strides in standardization through its Construction Innovation Hub, it's evident that its pace lags behind its continental counterparts.

South America's journey in 3D concrete printing is still in its infancy. Brazil is taking a step forward with a pilot project in São Paulo, aiming to produce homes under its social-housing initiative. On the other hand, Argentina grapples with economic challenges; its fluctuating inflation and currency instability have stymied significant capital investments. As a result, most activities are confined to university laboratories, where researchers are delving into experiments with recycled-plastic fibers.

The Middle-East and Africa post the fastest continental growth at a 77.64% CAGR. Saudi Arabia's ROSHN has ambitious plans, targeting printed units by 2030, with a swift production cycle. Dubai is setting the pace with a mandate that a portion of all new constructions must adopt additive techniques by 2030. They've already showcased this commitment with a printed bus shelter, engineered to endure the region's extreme desert conditions and sandstorms. In South Africa, the CSIR is exploring innovative clay-based printable mixes, aiming to address housing challenges in informal settlements.

Competitive Landscape

The 3D concrete printing market is moderately consolidated. Construction giants are purchasing printers outright to secure internal capabilities, while mid-tier contractors rely on build-operate-transfer agreements to sidestep capital outlays. Patent activity is heating up. COBOD’s US 11407169 B2 covers multi-footprint gantry rails, cutting mobilization overhead for large sites. Sika’s EP 3898558 A1 extends printable-mix open times to four hours, vital for hot climates. Startups are targeting speed; Mighty Buildings’ light-stone composite cures under UV, printing ten times faster than cementitious mixes. Standards-body participation now forms a strategic moat, as companies that shape test protocols embed preferences for their proprietary chemistries and hardware.

3D Concrete Printing Industry Leaders

COBOD International A/S

ICON Technology Inc.

Apis Cor

Heidelberg Materials AG

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ICON Technology closed a USD 56 million Series C led by Norwest and Tiger Global, lifting total capital to USD 543 million and accelerating scale-up beyond the 95-home Wolf Ranch community.

- October 2024: COBOD introduced the BOD3 printer with a 14.6 m span and suspended-nozzle mode, enabling floor and roof printing on the same setup.

Global 3D Concrete Printing Market Report Scope

3D concrete printing (3DCP) is defined as an additive manufacturing construction technique that utilizes a computer-controlled nozzle to extrude cementitious materials layer-by-layer, enabling the creation of complex structures without the need for traditional formwork. This automated process enhances design flexibility, minimizes material waste, and accelerates construction timelines.

The 3D concrete printing market is segmented by concrete type, product type, end-use sector, and geography. By concrete type, the market is segmented into ready-mix, high-performance, pre-cast, and shotcrete. By product type, the market is segmented into walls, floors and roofs, panels and lintels, staircases, and other product types. By end-use sector, the market is segmented into residential, commercial, infrastructure, and architectural. The report also covers the market size and forecasts in 14 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Ready-Mix |

| High-Performance |

| Pre-Cast |

| Shotcrete |

| Walls |

| Floors and Roofs |

| Panels and Lintels |

| Staircases |

| Other Product Types |

| Residential |

| Commercial |

| Infrastructure |

| Architectural |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | GCC Countries |

| South Africa | |

| Rest of Middle-East and Africa |

| By Concrete Type | Ready-Mix | |

| High-Performance | ||

| Pre-Cast | ||

| Shotcrete | ||

| By Product Type | Walls | |

| Floors and Roofs | ||

| Panels and Lintels | ||

| Staircases | ||

| Other Product Types | ||

| By End-Use Sector | Residential | |

| Commercial | ||

| Infrastructure | ||

| Architectural | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | GCC Countries | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global demand for 3D concrete printing and its expected growth by 2031?

Worldwide consumption is USD 1.49 billion in 2026 and is projected to reach USD 17.27 billion by 2031, reflecting a 63.23% CAGR.

How fast can 3D concrete printers complete a single-family home today?

Demonstrations such as ICON’s 100-home Wolf Ranch project show wall systems printed in 48 hours, cutting total construction labor by 60%.

Which concrete mix trends will shape adoption over the next five years?

High-performance and LC3 clinker-reduced mixes are scaling quickly, offering compressive strengths above 100 MPa and embodied-carbon cuts of 40%.

How do recent regulations affect permitting timelines in the United States?

ICC’s AC509 criteria and UL 3401 standards allow standard plan checks, trimming permitting lead times by up to 12 months and cutting legal fees.

Why are panels and lintels dominating current product-type revenues?

Factory-printed panels and lintels eliminate costly formwork, integrate conduits and insulation, and shorten on-site assembly to a few hours per unit.

Which region is projected to grow the fastest through 2031?

The Middle-East and Africa region records a 77.64% CAGR driven by Saudi Arabia’s 30,000-unit ROSHN initiative and Dubai’s 25% additive-construction mandate.