Bisphenol A (BPA) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

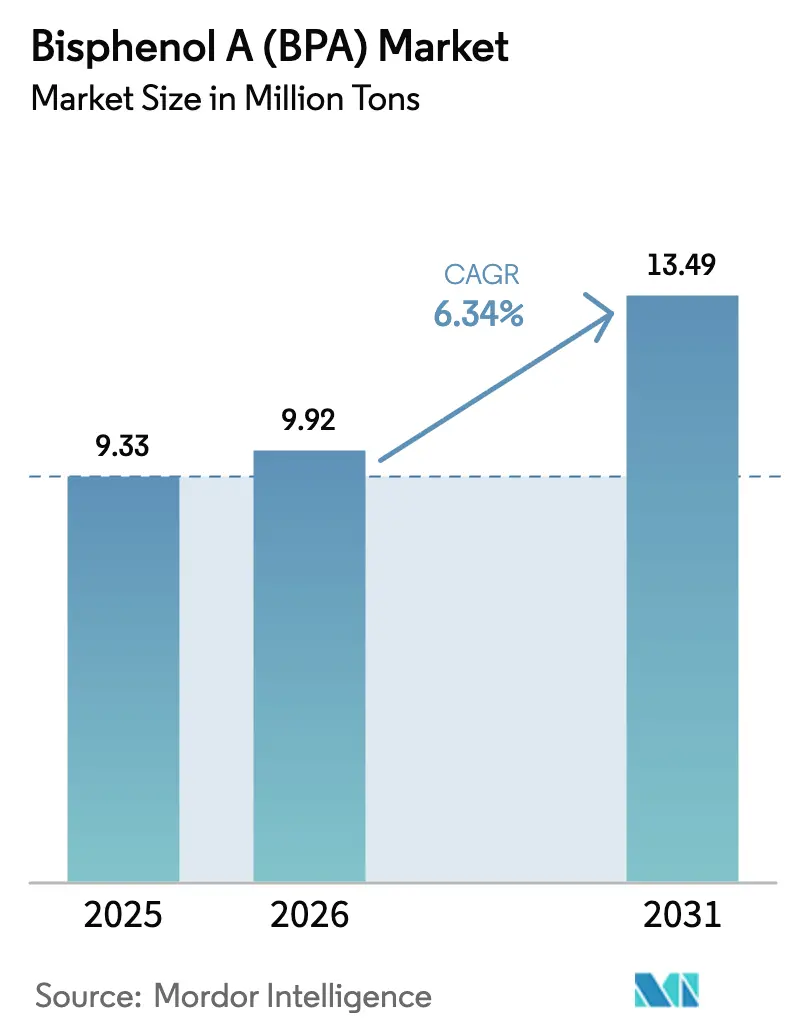

| Market Volume (2026) | 9.92 Million tons |

| Market Volume (2031) | 13.49 Million tons |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

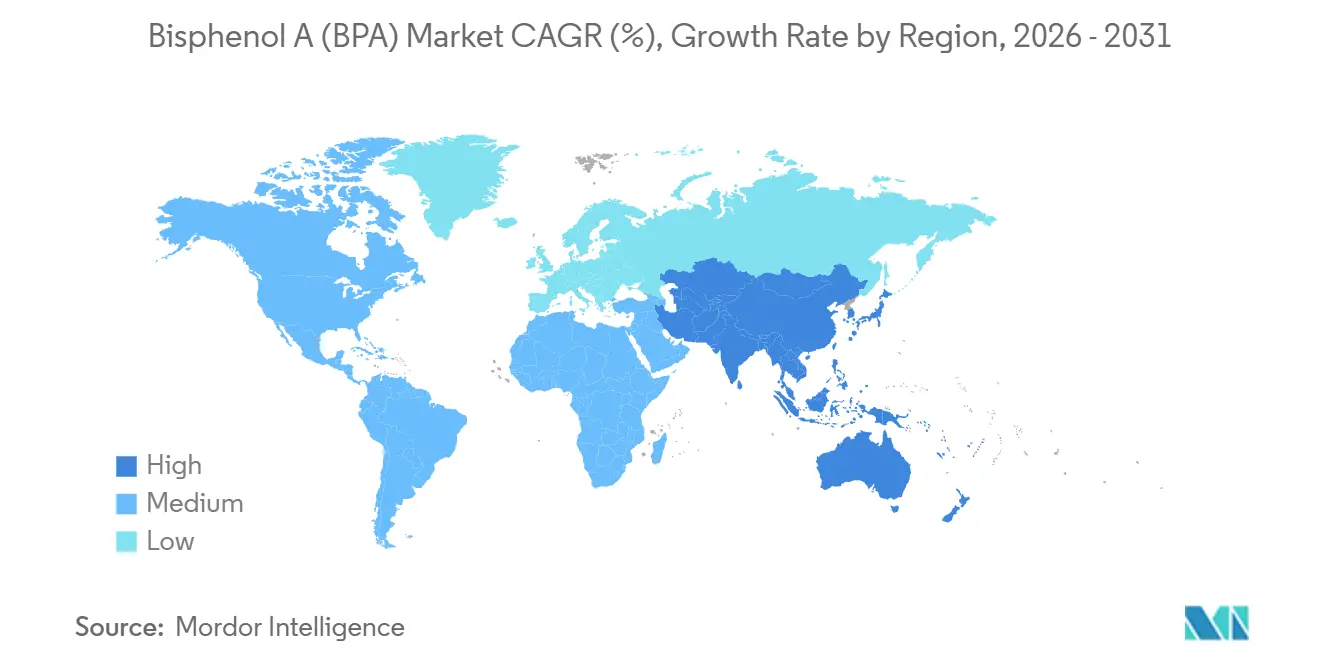

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bisphenol A (BPA) Market Analysis by Mordor Intelligence

The Bisphenol A Market size was valued at 9.33 million tons in 2025 and is estimated to grow from 9.92 million tons in 2026 to reach 13.49 million tons by 2031, at a CAGR of 6.34% during the forecast period (2026-2031). Polycarbonate continues to anchor volume because its impact strength, clarity, and flame retardancy are valued in consumer electronics and automotive glazing. Feedstock-cost gaps between Asia-Pacific and the West are widening, so integrated Chinese producers enjoy stronger cash margins than North American and European peers. Wind-energy rollout and aerospace composites are lifting epoxy-resin demand, giving high-purity BPA grades a growth pocket that is insulated from food-contact regulation. At the same time, closed-loop depolymerization pilots in Texas and Europe hint at future secondary supply streams that could temper virgin capacity needs without curbing overall Bisphenol A market momentum.

Key Report Takeaways

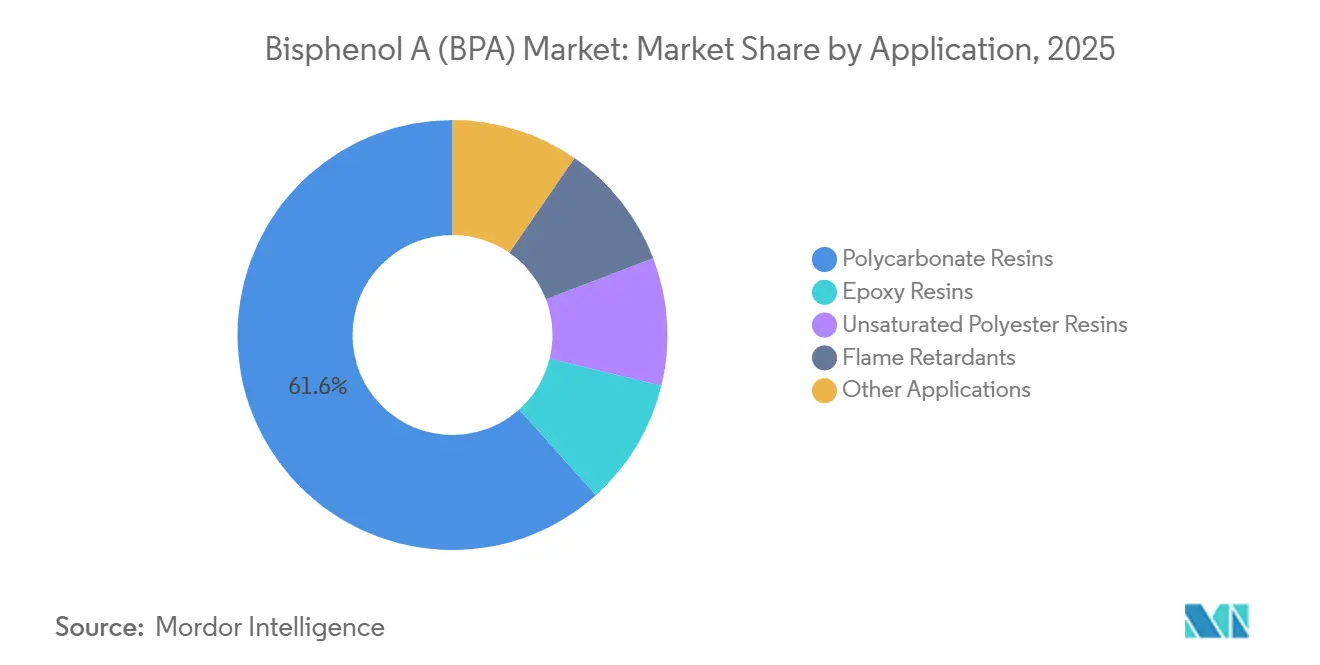

- By application, polycarbonate resins commanded 61.62% of the Bisphenol-A market share in 2025, whereas epoxy resins are forecast to expand at a 6.44% CAGR through 2031.

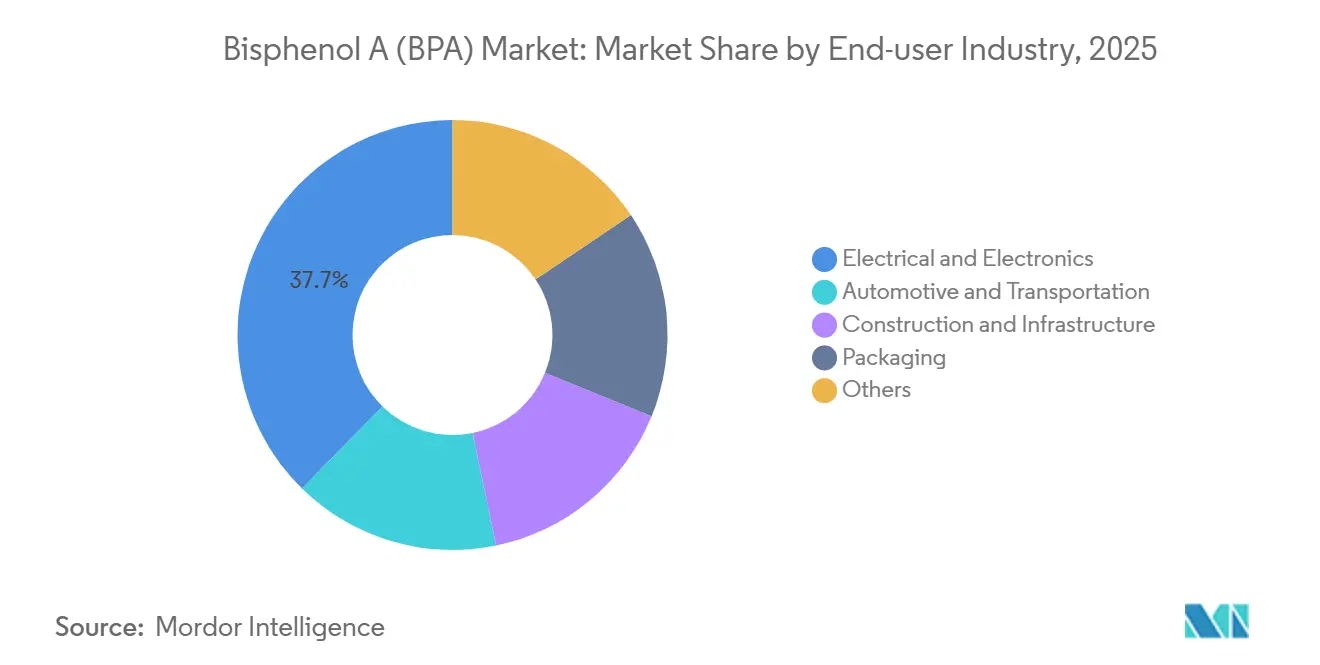

- By end-user industry, electrical and electronics captured 37.66% of the Bisphenol-A market size in 2025 and is advancing at a 6.55% CAGR between 2026 and 2031.

- By geography, Asia-Pacific captured 63.10% of the market and is advancing at a CAGR of 7.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bisphenol A (BPA) Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in epoxy-resin demand for wind-turbine blades | +1.2% | Europe, North America, APAC coastal regions | Medium term (2-4 years) |

| Asia-Pacific capacity additions lowering unit costs | +2.1% | APAC core, spill-over to Middle East & Africa | Short term (≤ 2 years) |

| Aerospace-grade BPA derivatives for advanced composites | +0.8% | North America, Europe | Long term (≥ 4 years) |

| Continuous-flow phenol–acetone integration boosting margins | +0.9% | Global, led by integrated producers in APAC | Medium term (2-4 years) |

| Closed-loop BPA depolymerization and upcycling technologies gain traction | +0.6% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Epoxy-Resin Demand for Wind-Turbine Blades

Wind-energy expansion is pulling high-performance epoxy resins into blades exceeding 100 m in length, and each blade contains several hundred kilograms of BPA-derived resin. Europe’s offshore installations consumed about 24,000 tons of such epoxy in 2025, and volumes rise as coastal permitting accelerates[1]European Composites Industry Association, “Offshore Wind Blade Growth,” european-composites.eu. The superior adhesion, chemical resistance, and fatigue life of BPA-based epoxy meet blade-longevity targets that determine the levelized cost of energy. Similar property sets are driving adoption within nacelle covers and spar caps. As the renewable-energy supply chain emphasizes durability over cost alone, integrated BPA suppliers gain stable offtake that is largely insulated from food-contact bans. In parallel, aerospace programs keep epoxy demand on a steady trajectory, though long certification cycles push the bulk of lift past 2028.

Asia-Pacific Capacity Additions Lowering Unit Costs

New plants in mainland China added 696,000 t/y of nameplate capacity during 1H-2024, putting downward pressure on global contract prices. These sites sit next to cumene and phenol-acetone hubs, cutting logistics outlays and working capital. Western producers with older, smaller reactors face higher fixed costs, so North American phenol assets ran at only 55-60% through 2025. The margin gap forces some to exit merchant BPA and pivot toward specialty derivatives. Additional captive units that support Chinese polycarbonate lines will shrink merchant trade further, crowding exporters from high-cost geographies and reshaping Bisphenol A market trade flows.

Aerospace-Grade BPA Derivatives for Advanced Composites

Ultra-pure BPA supports epoxy systems with glass-transition temperatures above 180°C, a threshold that bio-based candidates have yet to match. Hydrogenated BPA (HBPA) for electronics packaging stood at USD 23.5 million in 2024 and could reach USD 37.3 million by 2032 as higher thermal budgets enter semiconductor roadmaps. Aerospace qualification periods of three to five years lock suppliers into long revenue tails, encouraging R&D spend on next-generation grades. These high-margin niches shield a fragment of the Bisphenol A market from commodity cycles and make the segment attractive to companies seeking differentiation.

Continuous-Flow Phenol–Acetone Integration Boosting Margins

Continuous-flow technology optimizes residence time and heat removal better than batch reactors, lifting overall yield and cutting energy intensity by 5-8%. Plant operators who design flow reactors into new builds gain flexibility to pivot between BPA and other phenolic derivatives when spreads shift. Because Asia-Pacific greenfield sites start with a blank slate, they capture these benefits first. Western plants evaluating retrofits face downtime risk and higher capex, widening the structural cost gulf that defines competitiveness in the Bisphenol A market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phenol and acetone feedstock price volatility | -1.4% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Anti-dumping duties on Asian BPA exports | -0.7% | Europe, North America | Medium term (2-4 years) |

| Rapid adoption of BPA-free resins in critical electronics | -0.9% | Europe, North America, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Phenol and Acetone Feedstock Price Volatility

North American phenol averaged USD 902/t in Q4-2025 versus Asia-Pacific at USD 728/t, a gap that spurred arbitrage cargoes and drove spot volatility above 20%. Because BPA absorbs most phenol cost, polycarbonate sellers struggled to secure long-term contracts, and automotive OEMs moved toward fixed-price deals that shift risk back to resin suppliers. Non-integrated producers trimmed rates, leaving assets at 55-60% utilization. Upstream benzene remains tied to crude swings, so feedstock shocks can ripple through the Bisphenol A market within weeks.

Anti-Dumping Duties on Asian BPA Exports

The EU set definitive duties of 17.3–33% on Chinese BPA-based epoxy resin in July 2025, lifting landed cost by up to USD 300/t. While the move temporarily supports European margins, downstream compounders pay more for input, eroding export competitiveness. Registration rules added in October 2024 prolong customs clearance times and favor incumbents with compliance teams. Should the United States replicate EU protection by late 2026, global trade lanes for the Bisphenol A market will fragment further, increasing regional self-sufficiency and possible overbuild by 2029.

Segment Analysis

By Application: Polycarbonate Dominance Masks Epoxy’s Faster Path

Polycarbonate occupied 61.62% of the Bisphenol A market size in 2025, reflecting entrenched use in LED lenses, smartphone casings, and lightweight vehicle glazing[2]Mitsubishi Chemical Group, “Polycarbonate Market Applications,” mitsubishi-chem.co.jp. Price swings of 18-22% during 2025, however, encouraged automakers to test polycarbonate-ABS blends that lower BPA intensity without sacrificing impact performance. Even with these dilution tactics, global EV platforms rely on clear, tough glazing to cut mass, sustaining polycarbonate demand through 2031. Epoxy resin, by contrast, started from a smaller base but is forecast to outpace the overall Bisphenol A market at 6.44% CAGR, buoyed by wind-turbine blades and aerospace composites. Each offshore blade integrates hundreds of kilograms of resin, and blade lengths rising beyond 100 m lock in multi-decade service cycles that stabilize volume. Together, these two products will continue to represent more than four-fifths of the Bisphenol A market share during the outlook period.

Other applications, including flame-retardant tetrabromobisphenol A, unsaturated polyester resins, and specialty coatings, hold niche but profitable positions. Tetrabromobisphenol A dominates printed-circuit-board safety formulations where halogen-free substitutes weaken ignition resistance. Biomass-derived BPA under joint development by Mitsui Chemicals and Teijin could enter pilot scale by 2028, yet cost parity remains elusive. Collectively, these smaller outlets ensure demand diversity, but they lack the scale to counterbalance any future decline in commodity polycarbonate should substitution accelerate in consumer goods.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Electronics Lead While Automotive Quickens

Electrical and electronics absorbed 37.66% of global BPA volume in 2025 and are projected to expand at a 6.55% CAGR through 2031. Feature-rich devices and data-center hardware require tighter tolerances, pushing high-purity polycarbonate and epoxy laminates that command 20-30% premiums over commodity grades. Hydrogenated BPA meets moisture-resistance benchmarks in semiconductor encapsulation and represents about 40% of the HBPA sub-segment. Even as smartphone unit sales plateau, advanced form factors like foldables and augmented-reality headsets lift per-device resin loadings, extending growth for this slice of the Bisphenol A market.

Automotive and transportation consumed nearly one-quarter of polycarbonate in 2025 and gained momentum from EV adoption. Each battery pack uses 5-8 kg of epoxy-based adhesive for structural integrity, a figure that scales with pack capacity. Polycarbonate headlight lenses save 40-50% weight relative to glass, aiding range gains. Broader glazing remains constrained by scratch and UV performance, but incremental coating advances are narrowing the gap. Construction, packaging, and medical devices round out demand. Packaging faces direct regulatory headwinds, yet industrial coatings for large vessels retain limited derogations until 2028, cushioning decline. Altogether, the end-user mix underscores how electronics and mobility anchor forward demand, reinforcing the growth narrative for the Bisphenol A market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific held 63.10% of the Bisphenol A market share in 2025 and is projected to grow at a 7.32% CAGR to 2031. China alone operated 5.931 million t/y of capacity by 2024 and lifted January–August 2025 output 12% year-on-year to 3.15 million tons. Recent startups at Wanhua, Qingdao Haiwan, and Hengli added 696,000 t/y, underpinning regional cost leadership. India’s USD 37 billion petrochemical build-out through 2030 seeks to reduce heavy dependence on imports, 5.018 million-ton inflows of organic chemicals in FY 2023-24 signal latent demand the subcontinent will eventually meet locally.

North America and Europe together account for a declining slice of the Bisphenol A market as higher feedstock costs and anti-dumping duties distort trade. North American phenol hovered near USD 902/t in Q4-2025, squeezing integrated margins when Asian imports landed below domestic cash costs. EU duties of 17.3-33% shield local epoxy suppliers yet raise downstream compounder costs and encourage production shifts toward Asia. Western suppliers respond by doubling down on circular feedstocks and specialty grades, hoping to preserve value despite volume leakage.

South America and the Middle East & Africa remain small but strategic. SABIC’s diversification agenda, despite a 63.8% profit drop in Q3-2024, keeps polycarbonate on the investment map. Brazilian vehicle output ranks sixth worldwide, offering opportunities for lightweight glazing once currency stability returns. South African construction specifications now include flame-retardant polycarbonate panels, opening a modest but growing outlet. These emerging nodes will not rival Asia-Pacific in scale but add resilience to global Bisphenol A market demand.

Competitive Landscape

The Bisphenol A (BPA) market is moderately consolidated. Integrated Chinese firms capture commodity share by adding captive phenol-acetone and continuous-flow technology, which delivers a 5-8% margin lift over batch rivals. White-space innovation focuses on closed-loop recycling and aerospace-grade derivatives. Texas A&M’s 200 kt/y methanolysis pilot could supply 2% of 2031 needs if scale-up holds economics. Mitsui Chemicals and Teijin plan fermentation-derived BPA but still face cost-parity hurdles. Competitive strategy is thus polarizing: low-cost Asian producers chase scale, while Western incumbents pursue circular feedstocks, differentiated grades, and regulatory know-how.

Bisphenol A (BPA) Industry Leaders

Covestro AG

SABIC

LG Chem

Chang Chun Group

KUMHO P&B CHEMICALS.,INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mitsui Chemicals, Inc. and Mitsubishi Chemical Corporation initiated a collaborative study aimed at ensuring a stable supply of various phenol-related products. These products encompass phenol, acetone, α-methylstyrene, bisphenol A (BPA), and methyl isobutyl ketone.

- December 2024: The European Commission adopted a ban on the use of Bisphenol A (BPA) in food contact materials, due to its potentially harmful health impact. The ban means that BPA will not be allowed in products that come into contact with food or drink, such as the coating on metal cans, reusable plastic drink bottles, water distribution coolers, and other kitchenware.

Global Bisphenol A (BPA) Market Report Scope

Bisphenol-A (BPA) is a colorless crystalline solid belonging to the organic compound family. It is used primarily as a strengthener in polycarbonate plastics and epoxy resins. BPA is produced industrially by the condensation reaction of phenol and acetone, and it is known for its use in making various consumer goods such as water bottles, sports equipment, CDs, and DVDs.

The Bisphenol-A (BPA) market is segmented by application, end-user industry, and geography. By application, the market is segmented into polycarbonate resins, epoxy resins, unsaturated polyester resins, flame retardants, and other applications. By end-user industry, the market is segmented into electrical and electronics, automotive and transportation, construction and infrastructure, packaging, and others (medical, sports equipment, and more). The report also covers the market size and forecast for the bisphenol A market in 17 countries across major regions. For each segment, the market sizing and forecast were done based on volume (tons).

| Polycarbonate Resins |

| Epoxy Resins |

| Unsaturated Polyester Resins |

| Flame Retardants |

| Other Applications |

| Electrical and Electronics |

| Automotive and Transportation |

| Construction and Infrastructure |

| Packaging |

| Others (Medical, Sports Equipment, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Polycarbonate Resins | |

| Epoxy Resins | ||

| Unsaturated Polyester Resins | ||

| Flame Retardants | ||

| Other Applications | ||

| By End-user Industry | Electrical and Electronics | |

| Automotive and Transportation | ||

| Construction and Infrastructure | ||

| Packaging | ||

| Others (Medical, Sports Equipment, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global Bisphenol A market size?

It stands at 9.92 million tons in 2026 and is on track to reach 13.49 million tons by 2031.

Which application dominates BPA consumption?

Polycarbonate leads with 61.62% of the 2025 Bisphenol A market size.

Which region shows the fastest BPA demand growth?

Asia-Pacific is advancing at a 7.32% CAGR through 2031 and already holds 63.10% of global share.

How are regulations affecting BPA in food contact?

EU Regulation 2024/3190 bans BPA in food-contact items starting July 2026, shifting demand toward industrial uses.

What technological shifts could reshape future BPA supply?

Continuous-flow phenol-acetone integration and circular methanolysis recycling pilots promise lower costs and secondary feedstocks.

Page last updated on: