Leather Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

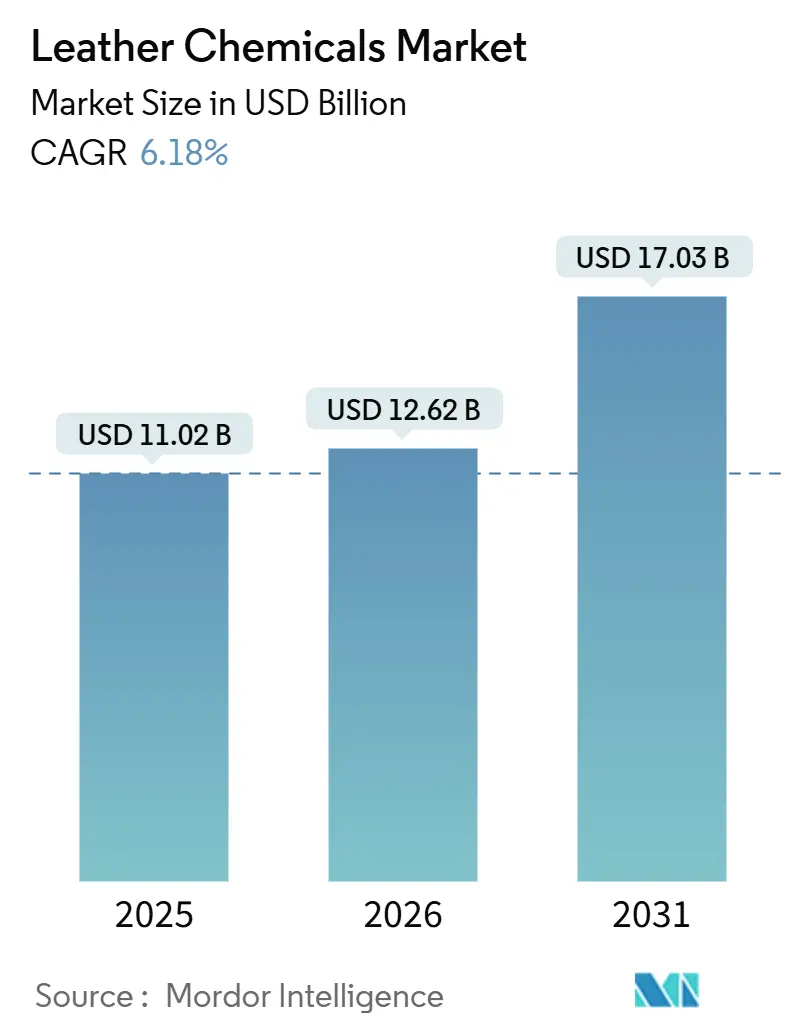

| Market Size (2026) | USD 12.62 Billion |

| Market Size (2031) | USD 17.03 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leather Chemicals Market Analysis by Mordor Intelligence

The Leather Chemicals Market size was valued at USD 11.02 billion in 2025 and is estimated to grow from USD 12.62 billion in 2026 to reach USD 17.03 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Driven by stricter Cr-VI thresholds, rising demand for chrome-free formulations, and brand mandates that favor low-VOC auxiliaries, the leather chemicals market is pivoting toward enzyme-assisted beam-house steps and bio-based finishing systems. Chrome-free chemistries already hold a majority position, while automotive and aviation upholstery stimulate the adoption of odor-neutral, aldehyde-tanned hides. Rapid expansion of Asia-Pacific tanneries underpins volume growth, yet compliance costs for wastewater treatment and energy remain key margin headwinds.

Key Report Takeaways

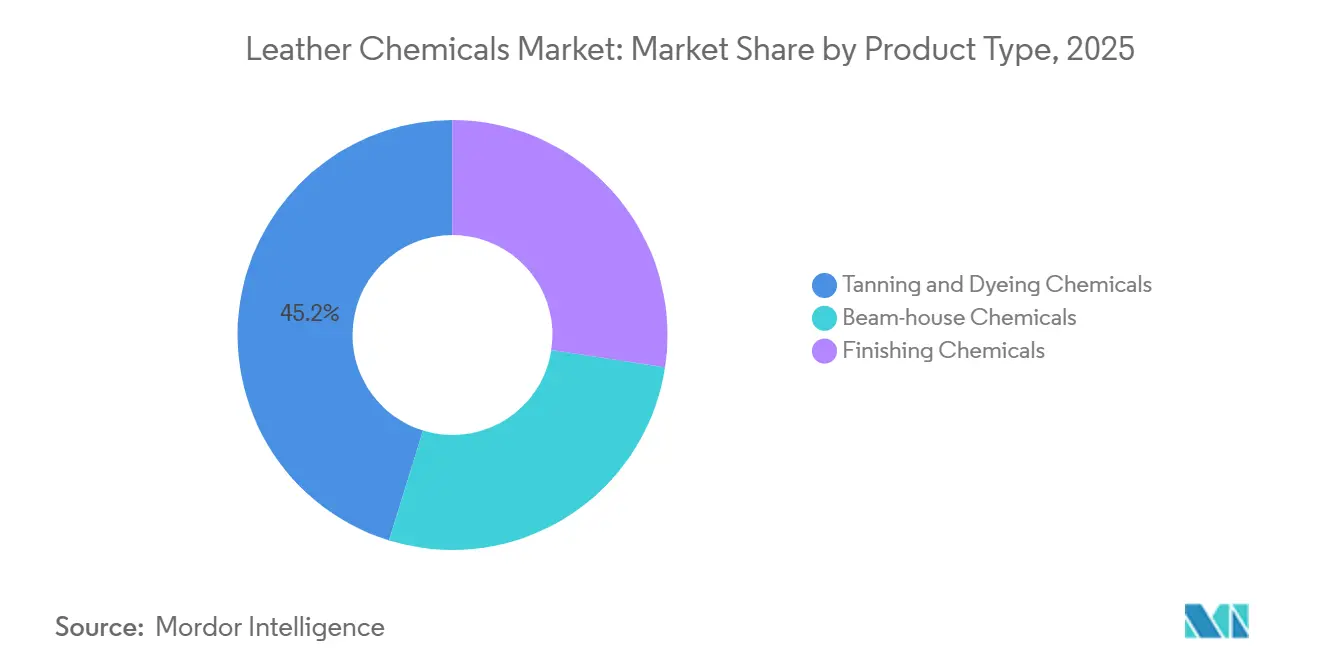

- By product type, Tanning and Dyeing held 45.22% share in 2025, while finishing chemicals accounted for a 6.98% CAGR between 2026 and 2031, the quickest pace across the processing chain.

- By chemical function, chrome-free technologies held 58.19% of the leather chemicals market share in 2025 and are projected to log the fastest 7.09% CAGR through 2031.

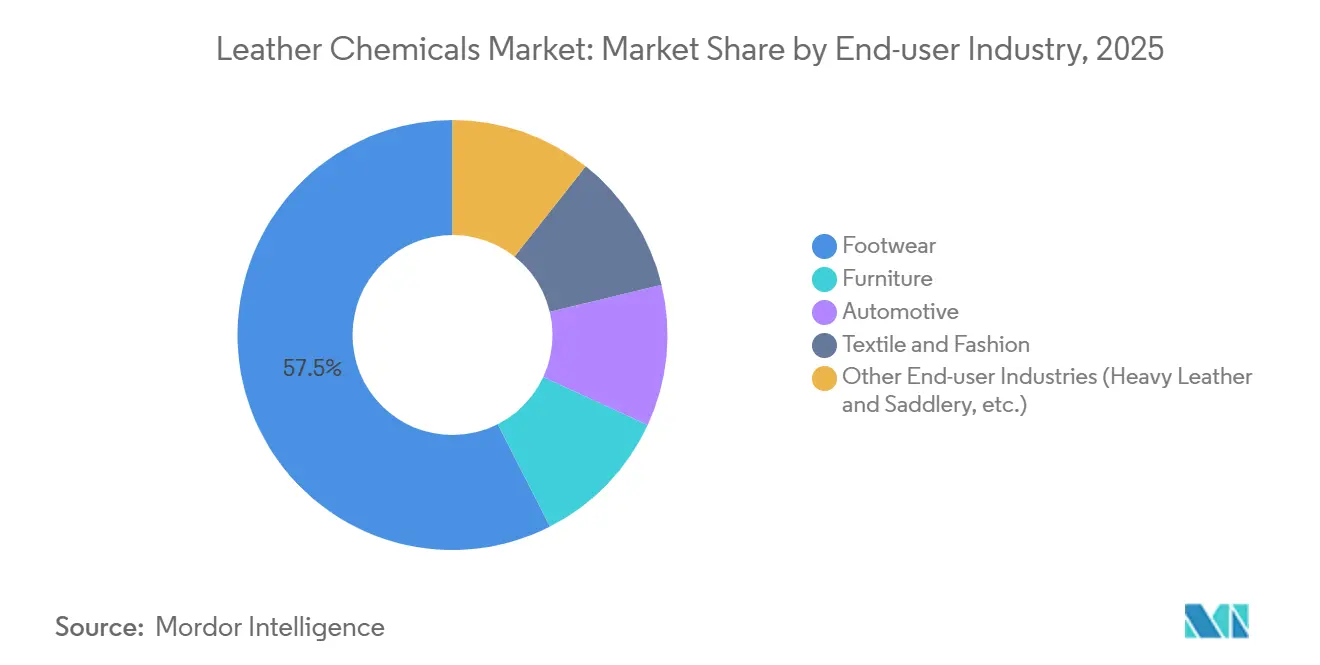

- By end-user industry, footwear captured 57.49% of the leather chemicals market size in 2025, while automotive chemicals are on course for a 7.14% CAGR to 2031.

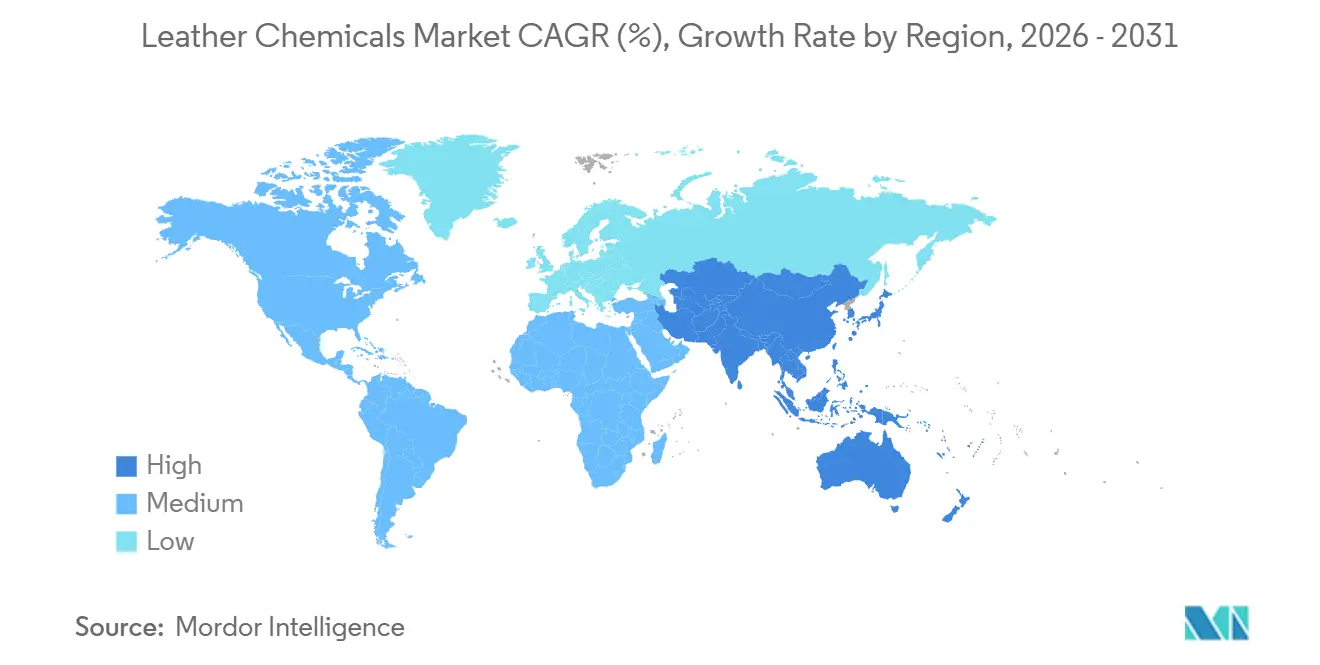

- By geography, Asia-Pacific contributed 48.79% of the global leather chemicals market demand in 2025 and is expected to expand at a 6.87% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Leather Chemicals Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in chrome-free & metal-free tanning technologies | +1.2% | Global, with early adoption in EU, North America, and China | Medium term (2-4 years) |

| Rapid growth of footwear & textile industries | +1.8% | APAC core (China, India, Vietnam), spill-over to South America | Short term (≤ 2 years) |

| Increasing demand for automotive & aviation upholstery | +0.9% | North America, Europe, China premium segments | Medium term (2-4 years) |

| Rising preference for bio-based fatliquors & syntans | +0.7% | EU, North America, Japan | Long term (≥ 4 years) |

| Enzyme-driven beam-house processes cut water 30% | +0.6% | Water-stressed regions: India, Middle East, North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Chrome-Free & Metal-Free Tanning Technologies

Luxury brands and OEMs require Cr-VI below 3 ppm to comply with EU REACH Annex XVII and state regulations, prompting rapid migration to wet-white systems that combine glutaraldehyde, titanium salts, and synthetic retanning polymers. Solutions such as CLARIANT Leva and Stahl EasyWhite Tan-E eliminate chromium sludge, cut hazardous disposal costs by 40%, and shorten processing cycles by 15%. In China, the GB 30585-2014 standard spurred upgrades across Zhejiang and Guangdong hubs, while Indian and Bangladeshi SMEs face higher raw-material costs and tighter pH controls that add 12-18% to inputs.

Rapid Growth of Footwear & Textile Industries

Asia produced 5.4 billion pairs of shoes in 2024, and India’s footwear output rose 9.2% in 2025, sustaining baseline demand for cost-efficient syntans and fatliquors[1]World Footwear Yearbook, “2024 Production Statistics,” worldfootwear.com. Vietnam and Indonesia expand capacity as China’s coastal wages climb, and their tanneries adopt chrome-free lines to meet multinational supplier codes. Fashion labels increasingly specify vegetable-tanned or recycled hides, reinforcing dual demand for economical metal-free agents and premium bio-syntans.

Increasing Demand for Automotive & Aviation Upholstery

Electric-vehicle interiors now stipulate total VOC below 50 µg/m³, achieved only with aldehyde-tanned leather and water-based polyurethane finishes. Aircraft seating remains a niche yet stable outlet; FAA and EASA flame-spread requirements lock in high-performance finishing packages that favor established vendors such as TFL and Buckman.

Rising Preference for Bio-Based Fatliquors & Syntans

European and North American luxury houses favor lignin-based syntans and plant-oil fatliquors that reduce Scope 3 emissions. Stahl EcoTan uses chestnut extracts that sequester 1.2 kg CO₂-eq per kilogram, while SCHILL+SEILACHER Levotan delivers similar softness to fish-oil systems but lowers aquatic toxicity by 60%. Price premiums of 25-35% confine adoption to high-value handbags, automotive seating, and branded footwear.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Cr-VI emission & wastewater norms | -0.8% | Global, with enforcement concentrated in EU, North America, China | Short term (≤ 2 years) |

| High energy & effluent-treatment costs | -0.5% | South Asia (India, Bangladesh, Pakistan), North Africa | Medium term (2-4 years) |

| Shift to mycelium/lab-grown leathers cuts chemical demand | -0.3% | North America, EU fashion and accessories segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Cr-VI Emission & Wastewater Norms

EU and Chinese standards cap Cr-VI at 3-10 mg/kg, forcing chrome-based tanneries to install expensive recycling loops or pivot toward trivalent salts. India’s revised effluent rules in 2025 cut TDS and BOD limits, requiring membrane bioreactors that can cost USD 1.5–3 million for mid-sized plants[2]Central Pollution Control Board, India, “Revised Effluent Standards for Tanneries,” cpcb.nic.in. Enforcement closures, such as 23 Dhaka tanneries in 2024, highlight compliance risk for fragmented clusters.

High Energy & Effluent-Treatment Costs

Electricity tariffs and zero-liquid-discharge mandates raise operating costs in South Asia and North Africa, where many facilities process under 1,000 hides per day. Capital intensity above USD 2 million for modern wastewater units remains a deterrent, slowing adoption of advanced chemicals and enzymes.

Segment Analysis

By Product Type: Finishing Chemicals Lead Growth Amid Customization Push

Finishing chemicals delivered the fastest growth at 6.98% CAGR, even as tanning and dyeing agents retained 45.22% of the leather chemicals market share in 2025. Water-based acrylic and polyurethane topcoats now hold 62% of sales in Europe, meeting VOC caps of 50 g/m². Digital inkjet compatibility drives incremental demand for silicone-modified top layers, enabling on-demand graphics without screen change downtime. Beam-house enzymes account for 18% of revenues, supported by protease blends that lower water use by 30% and lime 40%, vital for drought-prone clusters.

Chrome-based systems lose momentum as aldehyde-syntan packages now match shrinkage temperatures above 80°C at similar cost. Enzyme adoption accelerates in China’s Zhejiang province, where a 2025 tariff hike raised municipal water charges 18%, tipping the cost-benefit scale toward biochemical processes.

Note: Segment shares of all individual segments available upon report purchase

By Chemical Function: Chrome-Free Systems Capture Majority Share

Chrome-free agents held 58.19% of the leather chemicals market in 2025 and grew at a 7.09% CAGR through 2031. Synthetic organic tan packs blend acrylic polymers, melamine resins, and phenolic syntans, offering grain tightness and color yield on par with chrome yet eliminating Cr-VI concerns. Chromium-based agents still command a 28% share for heavy-duty gloves and industrial leather that require >85°C hydrothermal stability. Mineral alternatives based on zirconium or titanium account for 14% and serve white or pastel leathers where color purity is essential.

India’s Chrome-Free Leather Initiative subsidizes up to INR 5 million (USD 0.057 million) per tannery, accelerating aldehyde-based conversion in Tamil Nadu. Japan’s athletic footwear leaders mandate metal-free uppers, stimulating demand for vegetable extracts and syntan-retanned hides.

By End User: Automotive Upholstery Fastest Growing

Footwear contributed 57.49% revenue in 2025, but automotive upholstery is the quickest climber at 7.14% CAGR. EV makers such as BMW and Mercedes-Benz specify aldehyde-tanned, low-VOC hides, integrating water-based topcoats for cabin air-quality compliance. Furniture segments lean toward nubuck finishes that lower chemical intensity but fetch higher prices, while fashion divides between premium vegetable-tanned luxury goods and synthetic leather alternatives aimed at emission reduction.

Aviation remains niche yet sticky, with FAA and EASA mandates driving specialized phosphorus fire-retardant chemistries. Heavy leather for industrial PPE retains chrome dependence due to extreme durability needs.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated with 48.79% revenue in 2025 and will expand at 6.87% through 2031. China’s GB 30585-2014 enforcement and India’s subsidy scheme boost wet-white adoption, while Vietnam’s 1.55 billion-pair export base draws chrome-free investments. Indonesia leverages lower wages to attract mid-tier brands, and Japan’s chrome-free running-shoe policy deepens specialty demand.

In Europe and North America, Germany’s Bavarian automotive cluster sources chrome-free interiors, lifting water-based finishing penetration to 78%. Tuscany’s vegetable-tanning niche commands 40% price premiums, benefitting from established chestnut-extract supply chains. The United States imported 1.2 billion ft² of finished leather in 2024, reflecting near-shoring trends to Mexico and Latin America.

In South America and the Middle East, and Africa, Brazil’s 44 million hides per year feed Italian and US customers. Argentina capitalizes on low-cost bovine supply for automotive and furniture leather. Saudi Arabia invests USD 150 million to build a chrome-free cluster in Jeddah, targeting luxury autos and aviation. South Africa shifts toward enzyme-assisted processes to align with national water standards.

Competitive Landscape

The Leather Chemicals market is moderately fragmented. Mid-tier firms DyStar, Balmer Lawrie, and Zschimmer & Schwarz concentrate on regional niches, while specialists capture premium margins in digital printing and halal-certified additives. Patent activity jumped 22% year-on-year in 2025 as enzyme cocktails and hybrid zirconium-titanium tannages advanced. Opportunities exist in carbon-negative fatliquors, inkjet-ready topcoats, and species-specific enzyme kits. High capital needs for effluent control favor incumbents able to finance customer upgrades, potentially consolidating share among the top five.

Leather Chemicals Industry Leaders

Chemtan Company, Inc.

CLARIANT

Stahl Holdings B.V.

Şişecam

TFL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Stahl, a global player in specialty coatings for flexible materials, carved out its wet-end leather chemicals business. Now operating independently as Muno, the wet-end leather chemicals business is predominantly owned by Wendel.

- January 2024: Pidilite Industries Limited partnered with Italy-based Syn-Bios to widen access to advanced leather chemicals across South Asia.

Global Leather Chemicals Market Report Scope

Leather chemicals are chemical substances used during various steps of the leather-processing, such as beam house, tanning, dyeing, and finishing. These substances are necessary to give the leather the desired qualities, including durability, softness, and water resistance.

The Leather Chemicals market is segmented into product type, chemical function, end-user industry, and geography. By product type, the market is segmented into tanning and dyeing chemicals, beam house chemicals, and finishing chemicals. By chemical function, the market is segmented into chrome-based, chrome-free mineral, and synthetic organic. By end-user industry, the market is segmented into footwear, furniture, automotive, textile and fashion, and other end-user industries. The report also covers the market size and forecasts for the leather chemicals market in 17 countries across major regions. The market sizing and forecasts for each segment are based on value (USD).

| Tanning and Dyeing Chemicals |

| Beam-house Chemicals |

| Finishing Chemicals |

| Chrome-based |

| Chrome-free Mineral |

| Synthetic Organic |

| Footwear |

| Furniture |

| Automotive |

| Textile and Fashion |

| Other End-user Industries (Heavy Leather and Saddlery, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Tanning and Dyeing Chemicals | |

| Beam-house Chemicals | ||

| Finishing Chemicals | ||

| By Chemical Function | Chrome-based | |

| Chrome-free Mineral | ||

| Synthetic Organic | ||

| By End-user Industry | Footwear | |

| Furniture | ||

| Automotive | ||

| Textile and Fashion | ||

| Other End-user Industries (Heavy Leather and Saddlery, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate of the leather chemicals market toward 2031?

The market is forecast to expand at a 6.18% CAGR from 2026 to 2031 and reach USD 17.03 billion by 2031, as chrome-free systems and premium finishing technologies gain wider adoption.

Which segment is growing fastest within the leather chemicals industry?

Finishing chemicals top growth charts with a 6.98% CAGR thanks to demand for functional coatings that deliver abrasion resistance, anti-microbial traits, and digital-print compatibility.

Why is chrome-free tanning becoming standard practice?

Regulatory limits on hexavalent chromium and retailer sustainability audits are accelerating the shift to vegetable, mineral, and synthetic organic agents that eliminate Cr(VI) residues and reduce effluent toxicity.

How important is Asia-Pacific to the leather chemicals market?

Asia-Pacific commands nearly half of global demand and leads growth at a 6.87% CAGR due to large-scale operations in China and India and rising capacity in ASEAN manufacturing hubs.

What impact do vegan leather alternatives have on traditional chemical demand?

Synthetic and plant-based substrates require different processing chemistries, creating both competitive pressure and new opportunities for suppliers who develop primers, coatings, and dyes adapted to non-animal materials.