Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 47.62 Billion |

| Market Size (2031) | USD 62.32 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerosol Market Analysis by Mordor Intelligence

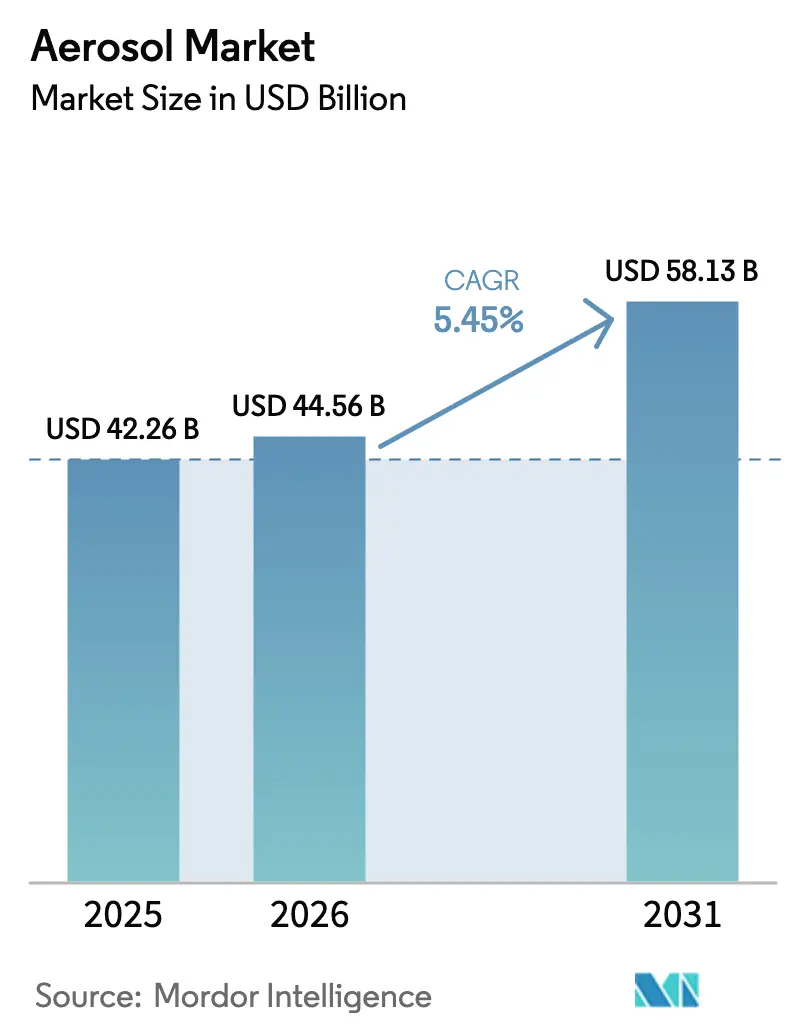

The Aerosol Market size is expected to grow from USD 45.12 billion in 2025 to USD 47.62 billion in 2026 and is forecast to reach USD 62.32 billion by 2031 at 5.53% CAGR over 2026-2031. The continued phase-down of high-GWP hydrofluorocarbons, growing consumer demand for portable packaging, and investments in low-carbon propellant systems are key factors driving this trend. On the supply side, aluminum can manufacturers are moving upstream to establish recycling loops that comply with extended producer responsibility requirements. Innovations in bag-on-valve technology are expanding the potential patient base for respiratory and topical drug applications. However, insurers, regulators, and municipal waste authorities are imposing stricter regulations on flammability, end-of-life collection, and volatile organic compound limits, increasing cost pressures across all segments of the aerosol market.

Key Report Takeaways

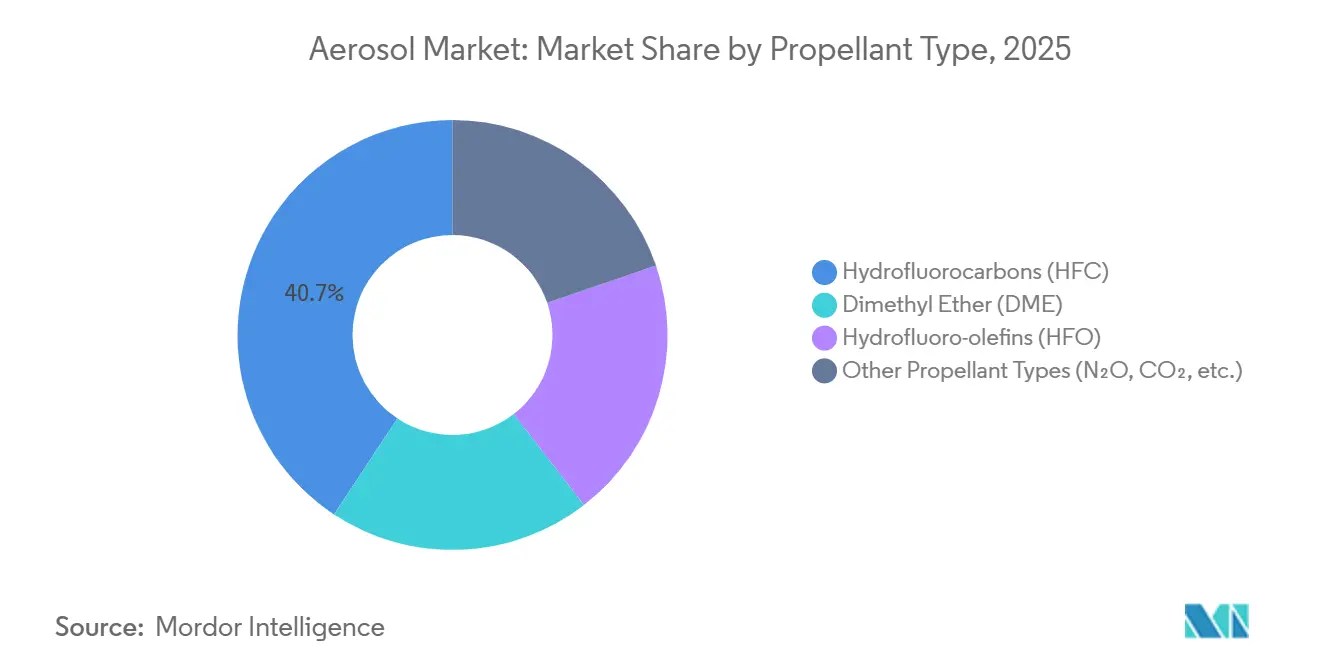

- By propellant type, hydrofluorocarbons held 40.71% of the aerosol market share in 2025, while hydrofluoro-olefins are expanding at a 6.61% CAGR through 2031.

- By can type, aluminum commanded 45.83% of the aerosol market share in 2025, while plastic is projected to grow at a 6.01% CAGR through 2031.

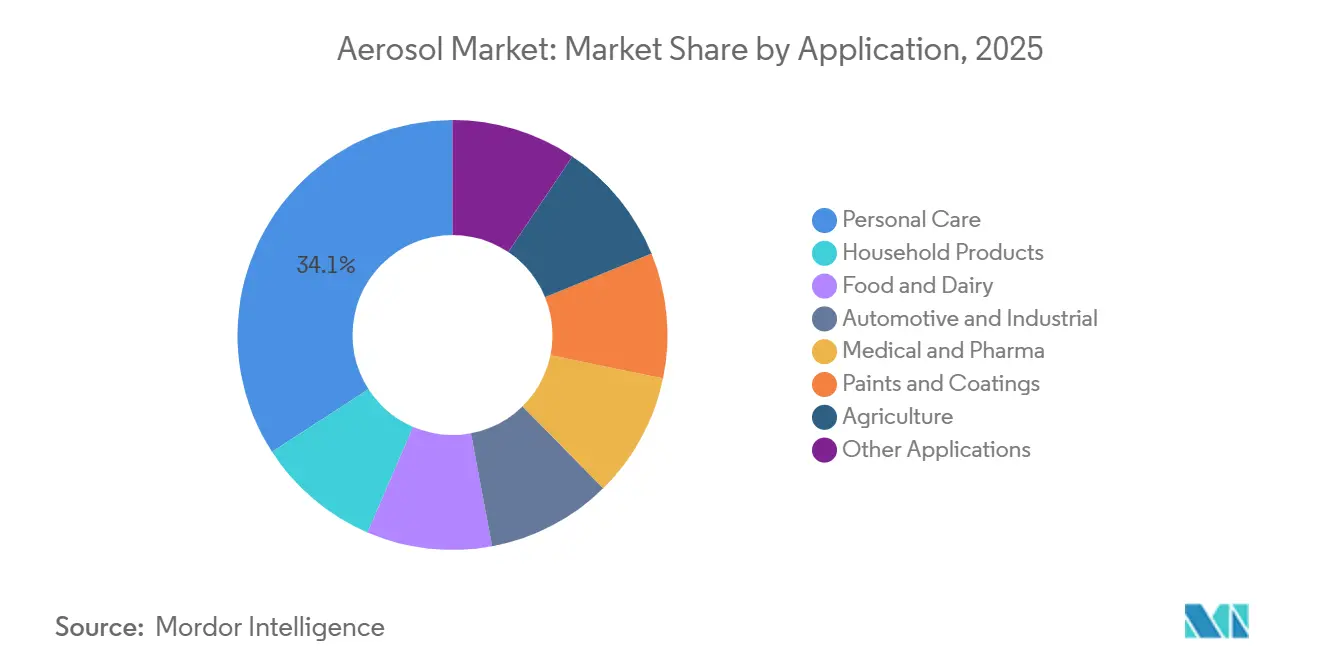

- By application, personal care commanded 34.13% of the aerosol market share in 2025, while medical and pharma is projected to grow at a 6.33% CAGR through 2031.

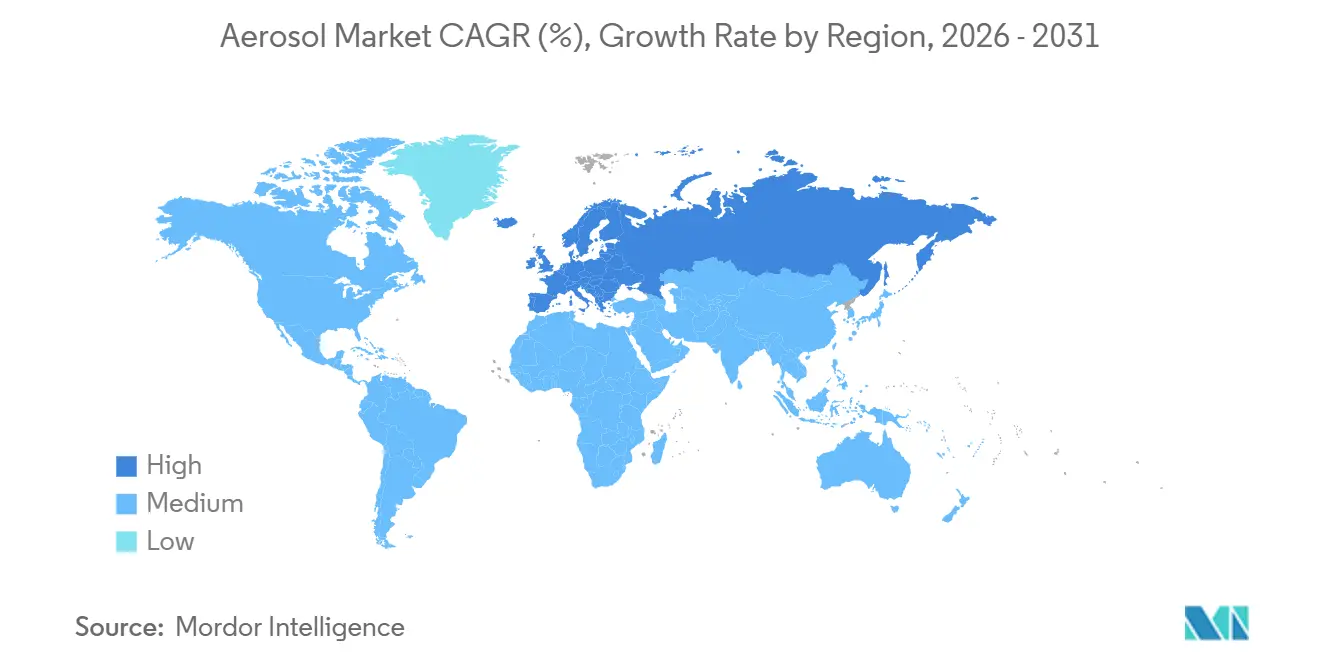

- By geography, Europe led with 32.19% of the aerosol market share in 2025 and is expected to record the fastest 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerosol Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of paints-and-coatings spray applications | +0.8% | Global, with concentration in North America aerospace hubs and European automotive refinish markets | Medium term (2-4 years) |

| Convenience-driven portable packaging across sectors | +1.2% | Global, led by Asia-Pacific urban centers and North American on-the-go consumption | Short term (≤ 2 years) |

| Regulatory shift to low-GWP propellants spurring re-tooling | +1.5% | North America and Europe (EPA AIM Act, EU F-Gas Regulation); spillover to APAC export-oriented manufacturers | Long term (≥ 4 years) |

| Adoption of bag-on-valve tech for pharmaceutical-grade dosing | +0.6% | North America and Europe (FDA, EMA regulatory approvals); emerging in Japan and South Korea | Medium term (2-4 years) |

| Growth of on-the-go sanitizing aerosols in shared micro-mobility fleets | +0.5% | North America and Europe urban centers; pilot deployments in APAC (Singapore, Seoul, Tokyo) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Paints-and-Coatings Spray Applications

Aerospace original equipment manufacturers are adopting aerosolized coatings that cure more quickly and minimize overspray. As a result, AkzoNobel has allocated EUR 50 million in 2024 to expand its aerospace facility in the Netherlands. Axalta and Dürr have launched digital paint-mixing kiosks that dispense custom colors into on-demand aerosol cans, reducing the inventory space required in body shops. BASF’s overspray-free aerosol chemistry is becoming popular in confined industrial environments where traditional HVLP guns face challenges with hazardous air pollutants. Narrow-body aircraft assembly lines prefer these sprays due to limited rework opportunities, while rheology modifiers ensure consistent spray patterns despite temperature fluctuations. These trends highlight a premium niche within the aerosol market, benefiting suppliers capable of certifying coatings for aviation applications.

Convenience-Driven Portable Packaging Across Sectors

Single-use aerosols are increasingly replacing bulk bottles in personal care, household cleaning, and food service industries. Unilever’s Cif Infinite Clean probiotic spray, introduced in April 2025, offers multi-day surface protection at a GBP 4 price point. Similarly, Lion Corporation’s silver-ion toilet fogger, launched in Japan the same month, addresses the demand for deep-cleaning solutions. Fonterra’s Anchor whipped cream extends shelf life to 12 months, providing labor savings for cafés. Airlines and hotels prefer TSA-compliant 100 mL cans, while e-commerce warehouses benefit from shatter-resistant plastic aerosols that reduce product returns. These factors emphasize the role of portable formats in driving aerosol market growth.

Regulatory Shift to Low-GWP Propellants Spurring Re-Tooling

The U.S. AIM Act will limit consumer aerosol global warming potential (GWP) to 150 starting January 2025, prompting a shift from HFC-134a to alternatives such as HFO-1234ze and dimethyl ether[1]U.S. Environmental Protection Agency, “Phasedown of Hydrofluorocarbons,” epa.gov. AstraZeneca has filed to transition Breztri Aerosphere inhalers to HFO-1234ze across multiple jurisdictions, achieving a 99.9% reduction in life-cycle emissions without affecting dosage. In the EU, quotas on virgin HFCs have driven spot prices above USD 20 per kg in 2025. ISO 14001 certification has become a standard requirement for aerosol contract fillers targeting multinational clients. However, smaller fillers face financial constraints in upgrading gas-handling systems, leading to market consolidation among larger, well-capitalized players.

Adoption of Bag-on-Valve Tech for Pharmaceutical-Grade Dosing

Bag-on-valve systems separate drug formulations from propellants, eliminating the need for preservatives and reducing oxidation risks. Between 2024 and 2025, the FDA approved generic beclomethasone, albuterol, and fluticasone metered-dose inhalers using this technology. Aptar’s APF Futurity metal-free pump, launched in 2024, offers full recyclability. Additionally, RFID-enabled actuators monitor patient adherence and facilitate pharmacy refills, enabling value-based reimbursement models. Adoption is increasing in Japan and South Korea, where aging populations are driving demand for chronic respiratory medications. This technology provides a competitive edge for qualified suppliers, enhancing margins within the aerosol market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flammability and safety liabilities | -0.5% | Global, with heightened enforcement in North America and Europe under DOT and UN transport codes | Short term (≤ 2 years) |

| Consumer pushback in zero-waste retail outlets | -0.4% | Europe and North America urban centers; emerging in Australia and New Zealand | Medium term (2-4 years) |

| Scarcity of pharma-grade CO₂ propellant amid CCUS demand | -0.3% | North America (U.S. merchant CO₂ supply chain); secondary impact in Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flammability and Safety Liabilities

Dimethyl ether, propane, and butane remain classified as Division 2.1 flammable gases under UN transport codes, necessitating explosion-proof warehousing and higher insurance premiums. U.S. DOT regulations limit pallet loads for online retail distribution, increasing fulfillment costs[2]U.S. Department of Transportation, “Hazardous Materials Regulations,” transportation.gov . OSHA ventilation requirements may require mid-sized fillers to invest up to USD 500,000 in HVAC upgrades. Recalls, such as the 2024 brake-cleaner incident, can harm brand reputation and result in significant liability costs. These factors pose challenges to margin expansion in the aerosol market.

Consumer Pushback in Zero-Waste Retail Outlets

Refillable systems, such as Zep’s Flairosol degreasers launched in September 2024, eliminate the need for propellants and volatile organic compounds (VOCs), appealing to environmentally conscious consumers at retailers like Lowe’s and eco-stores. AeroFlexx pouches, adopted by Aveda, reduce plastic usage by 70% and offer concentrate refills. Germany’s VerpackG regulations and EU packaging proposals impose increasing fees on non-recyclable cans. Brands reliant on convenience must address these challenges by quantifying carbon footprints and ensuring recyclability to maintain consumer trust.

Segment Analysis

By Propellant Type: HFO Adoption Accelerates While HFCs Remain Predominant

Hydrofluorocarbons (HFCs) represented 40.71% of 2025 revenue, while hydrofluoro-olefins (HFOs) are projected to grow at a 6.61% CAGR through 2031. The Environmental Protection Agency (EPA) has reduced 2026 HFC allowances by 15% compared to the 2024 baseline, establishing HFO-1234ze as the primary alternative. AstraZeneca’s planned shift to HFO-1234ze ensures dose stability while achieving a 99.9% reduction in global warming potential (GWP). Dimethyl ether is capturing market share from liquefied petroleum gas (LPG) in Asia-Pacific personal care applications, as it requires minimal adjustments to production lines. Nitrous oxide remains the leading choice for whipped dairy applications, while carbon dioxide (CO₂) is essential for food safety. Small-scale fillers risk losing contracts unless they obtain ISO 14001 certification and demonstrate the use of sub-150 GWP blends. These trends are driving a two-tier aerosol market, where access to capital influences the pace of compliance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Can Type: Aluminum Dominance Meets Plastic’s Lightweight Challenge

Aluminum accounted for 45.83% of the aerosol market share in 2025, benefiting from its infinite recyclability. Ball Corporation invested USD 290 million in Colorado in 2024 to produce cans with 90% recycled content, returning them to shelves within 60 days. Steel continues to serve industrial applications requiring 180 psi pressure ratings, despite 20% higher coating costs. Glass and tin cans remain popular in prestige fragrances but face a 5% return rate in e-commerce. Plastic cans are expected to grow at a CAGR of 6.01% through 2031, as their lightweight properties reduce freight emissions by 0.15 kg CO₂ per 100 units shipped. However, European Union regulations mandating recyclable packaging by 2030 are accelerating research into mono-material PET solutions. These developments are expected to shape procurement strategies across the aerosol market over the next decade.

By Application: Medical Aerosols Outpace Personal Care Growth

Personal care applications led the market in revenue, contributing 34.13% in 2025, supported by Beiersdorf’s EUR 350 million deodorant production expansion in Leipzig. However, the medical and pharma segment is anticipated to grow faster, with a CAGR of 6.33% through 2031, driven by FDA-approved generics that reduce patient costs. Household products are benefiting from innovations such as probiotics and silver-ion technologies, while automotive sprays are transitioning to PFAS-free lubricants that extend service intervals threefold. Paint aerosols are experiencing renewed demand in the aerospace sector, as evidenced by AkzoNobel’s EUR 50 million facility upgrade. Food aerosols rely on nitrous oxide’s fourfold expansion, while agricultural sprays remain niche due to concerns about drift. These varied growth rates highlight the importance of portfolio diversification within the aerosol market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Europe accounted for 32.19% of the market revenue in 2025 and is projected to grow at a CAGR of 6.56% through 2031. F-Gas quotas and VerpackG fees favor aluminum cans, which integrate seamlessly into deposit systems. Ball Corporation’s acquisition of Alucan in October 2024 secured additional capacity in Spain and Belgium for HFO-compliant production lines.

Asia-Pacific is accelerating, driven by urban demand for cosmetics in China and e-commerce packaging needs in India. Lion Corporation’s antibacterial fogger highlights Japan’s preference for high-function household aerosols. Thailand’s tourism sector boosts travel-size aerosol sales, while South Korea benefits from K-beauty exports.

North America faces AIM Act deadlines, pushing fillers toward HFO-based blends. Ball Corporation’s USD 160 million acquisition of Florida Can Manufacturing in February 2025 ensures supply for household goods customers. Zep’s Flairosol line demonstrates the growing market for propellant-free sprays in DIY retail. Health Canada’s June 2025 advisory on nitrous oxide suggests stricter regulations for whipped-cream chargers.

South America, and Middle-East and Africa remain emerging markets, where urbanization drives demand for deodorants and disinfectants. However, infrastructure gaps in recycling and propellant logistics limit growth compared to Europe and the Asia-Pacific. Nearshoring to Mexico is shortening lead times for U.S. customers and modestly diversifying global aerosol supply chains.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The aerosol market exhibits moderate concentration, with the top five suppliers controlling approximately 53% of combined capacity. Valve manufacturing remains fragmented, with key players including Lindal, Aptar, and Coster. Ball Corporation pursued three acquisitions between October 2024 and January 2026, including Alucan, Florida Can Manufacturing, and an 80% stake in Benepack valued at USD 195 million, to enhance vertical integration. Aptar’s APF Futurity pump incorporates dose tracking, creating regulatory re-validation barriers that strengthen customer retention. Opportunities remain in micro-mobility sanitizers and electrostatic farm sprays. AeroFlexx’s refillable pouches, set to launch under Aveda in 2027, challenge single-use cans by reducing plastic content by 70%. Barriers to entry now center on HFO handling, ISO 14001 compliance, and the high costs of multi-million-dollar filling lines. These factors enforce a disciplined capital cycle within the aerosol industry while encouraging acquisitions when niche innovators achieve scale.

Aerosol Industry Leaders

Ball Corporation

Crown

Beiersdorf

Aptar

Ardagh Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2026: Beiersdorf and Ball Corporation achieved a key milestone in their strategic partnership by transitioning all of Beiersdorf's European aerosol cans to 100% post-consumer recycled (PCR) aluminium. This initiative began with a pilot project in 2024 and culminated in the complete adoption of 100% PCR aluminium packaging across the region.

- March 2026: Glenmark Pharmaceuticals announced that its subsidiary, Glenmark Specialty SA, had received final approval from the U.S. Food and Drug Administration (USFDA) for Fluticasone Propionate Inhalation Aerosol USP, 44 mcg per actuation. The USFDA had determined the product to be bioequivalent and therapeutically equivalent to the reference listed drug (RLD), Flovent HFA Inhalation Aerosol, 44 mcg, manufactured by GlaxoSmithKline (NDA 021433).

Global Aerosol Market Report Scope

Aerosols are extremely tiny solid particles or liquid droplets suspended in the air or other gases. They consist of solid particles that can be placed in the atmosphere by large dust storms, volcanic eruptions, or soot particles from large fires.

The aerosol market is segmented by propellant type, can type, application, and geography. By propellant type, the market is segmented into hydrofluorocarbons (HFC), dimethyl ether (DME), hydrofluoro-olefins (HFO), and other propellant types (N₂O, CO₂, etc.). By can type, the market is segmented into aluminum, steel, plastic, and glass and tin. By application, the market is segmented into personal care, household products, food and dairy, automotive and industrial, medical and pharma, paints and coatings, agriculture, and other applications. The report also covers the market size and forecasts for the aerosol in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Propellant Type

| Hydrofluorocarbons (HFC) |

| Dimethyl Ether (DME) |

| Hydrofluoro-olefins (HFO) |

| Other Propellant Types (N₂O, CO₂, etc.) |

By Can Type

| Aluminum |

| Steel |

| Plastic |

| Glass and Tin |

By Application

| Personal Care |

| Household Products |

| Food and Dairy |

| Automotive and Industrial |

| Medical and Pharma |

| Paints and Coatings |

| Agriculture |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Propellant Type | Hydrofluorocarbons (HFC) | |

| Dimethyl Ether (DME) | ||

| Hydrofluoro-olefins (HFO) | ||

| Other Propellant Types (N₂O, CO₂, etc.) | ||

| By Can Type | Aluminum | |

| Steel | ||

| Plastic | ||

| Glass and Tin | ||

| By Application | Personal Care | |

| Household Products | ||

| Food and Dairy | ||

| Automotive and Industrial | ||

| Medical and Pharma | ||

| Paints and Coatings | ||

| Agriculture | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size of the aerosol market?

The aerosol market stands at USD 47.62 in 2026 and is forecast to reach USD 62.32 billion by 2031, advancing at 5.53% CAGR over 2026-2031.

Which propellant class is growing fastest through 2031?

Hydrofluoro-olefins are expanding at a 6.61% CAGR through 2031as low-GWP regulations tighten across major economies.

Why did aluminum dominate in can type in 2025?

Infinite recyclability, deposit-return schemes, and brand commitments to circular packaging keep aluminum at a 45.83% share in 2025.

Which application is set to outpace personal care through 2031?

Medical and pharma are projected to grow at a 6.33% CAGR through 2031, driven by generic inhalers and bag-on-valve adoption.