India Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

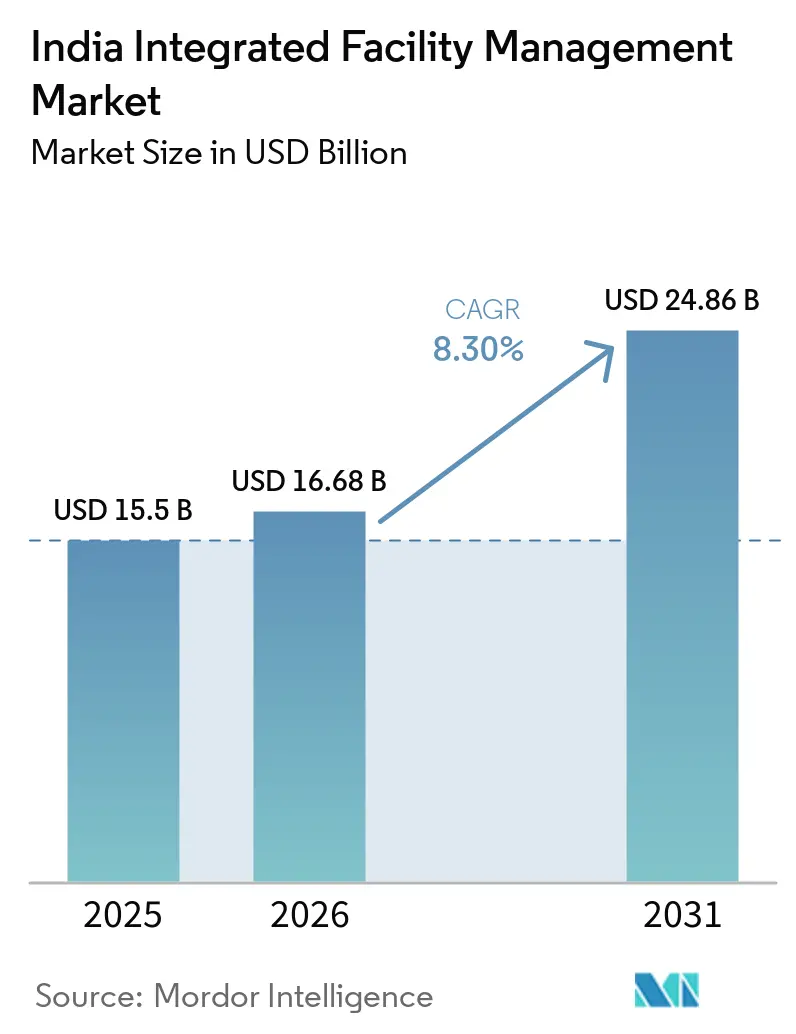

| Base Year Market Size (2025) | USD 15.5 Billion |

| Market Size (2026) | USD 16.68 Billion |

| Market Size (2031) | USD 24.86 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

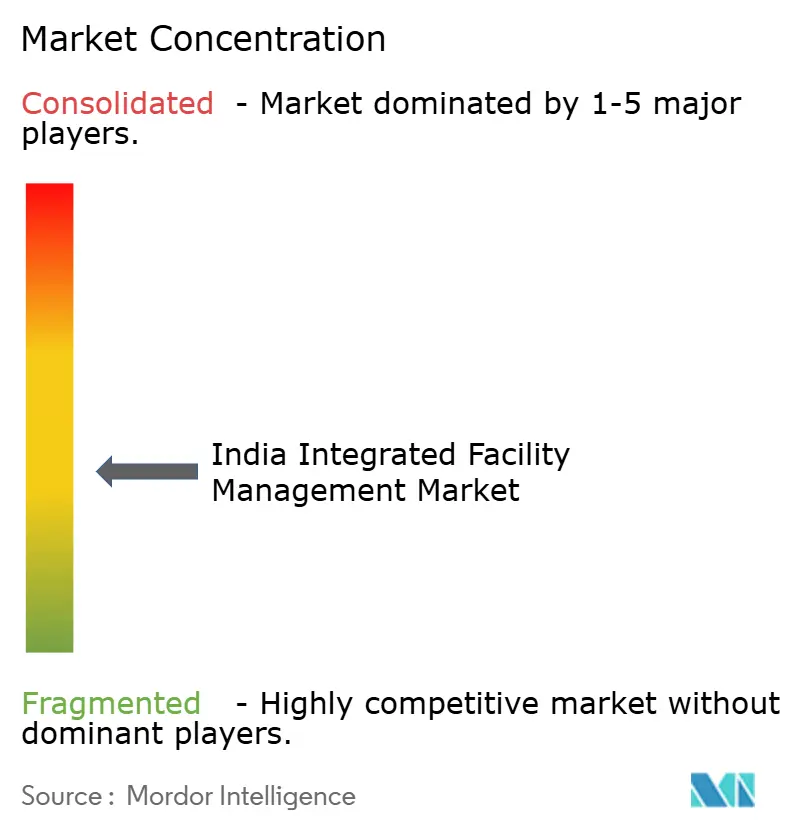

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Integrated Facility Management Market Analysis by Mordor Intelligence

The India Integrated Facility Management Market size is projected to be USD 15.5 billion in 2025, USD 16.68 billion in 2026, and reach USD 24.86 billion by 2031, growing at a CAGR of 8.30% from 2026 to 2031.

The growth path remains supported by formalization in the organized service base, even as the pace now reflects a larger revenue base and tighter margin conditions rather than weak demand, with CRISIL-assessed growth in the organized security and facility management space reaching 13% over the four years preceding FY26. Demand visibility is also tied to the commercial real estate cycle, where net office absorption across the top 8 cities reached a record 61.4 million sq ft in 2025, up 25% year over year, and Grade A demand is expected to stay elevated in 2026 at 70 to 75 million sq ft. Each new office lease creates a multi-year operating requirement, giving the India integrated facility management market a recurring revenue base broader than one-time project cycles and more resilient than discretionary service spending. Contracting is also moving from labour deployment models toward SLA-based delivery, which lifts average contract values as buyers seek measurable uptime, energy performance, hygiene standards, and workplace outcomes across larger portfolios. The India integrated facility management market is still fragmented, yet the distance between national leaders and mid-tier firms is widening as acquisitions, public capital raising, compliance infrastructure, and digital operating tools increasingly shape who can win and retain large integrated mandates.

Key Report Takeaways

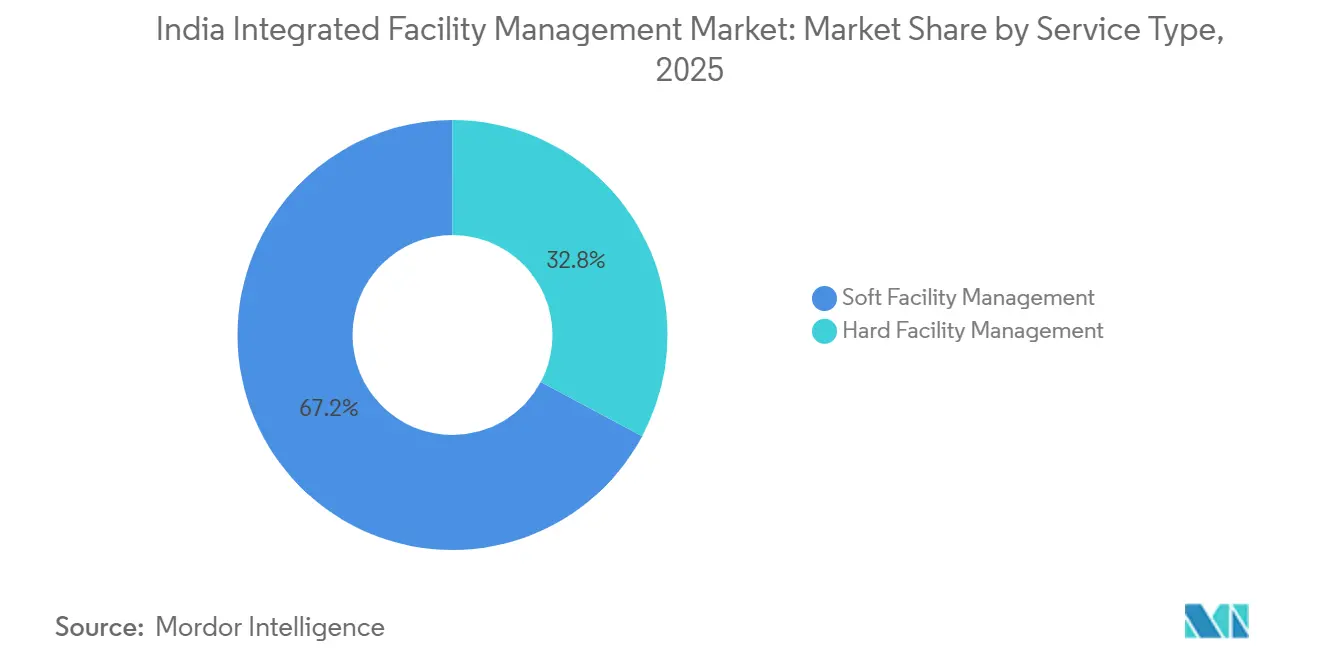

- By service type, soft facility management held 67.19% share of the India integrated facility management market size in 2025, while Hard FM is forecast to expand at a 9.47% CAGR through 2031.

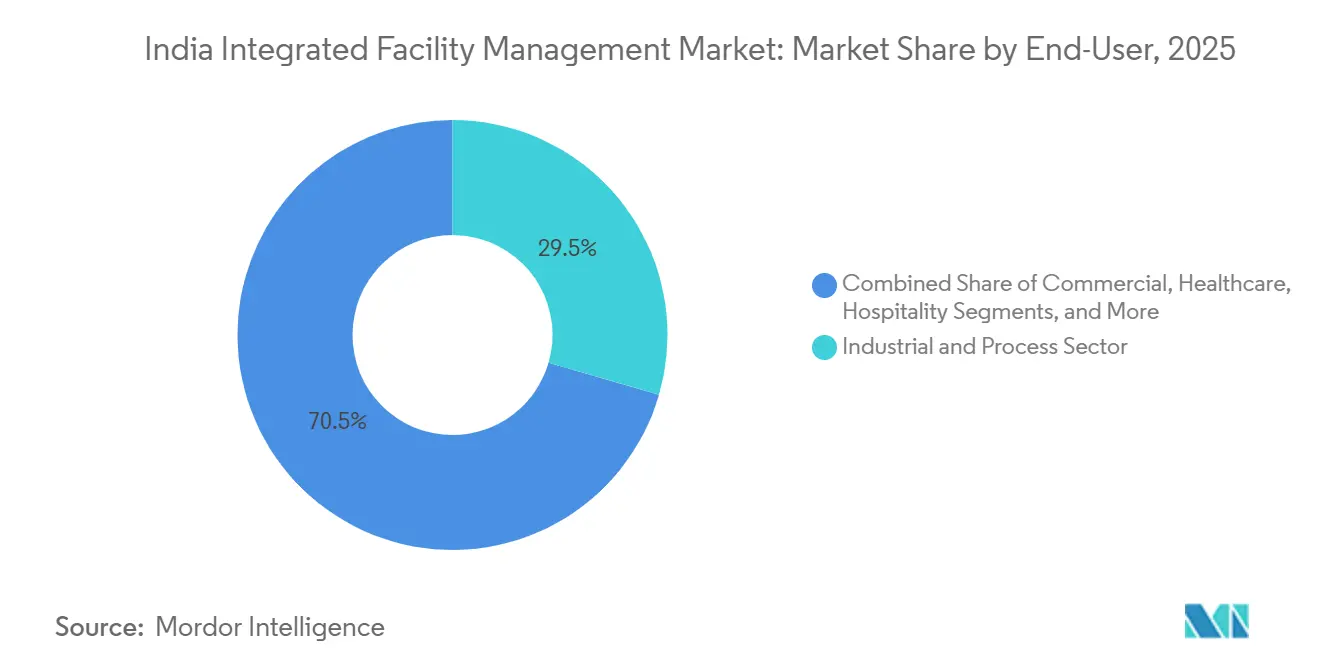

- By end user, the industrial and process sector held 29.48% of the India integrated facility management market share in 2025, while the commercial segment is projected to record the highest CAGR at 9.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on integrated facility management market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Grade A Offices and Mixed-use Campuses | +2.8% | National, with early gains in Bengaluru, Delhi-NCR, Hyderabad, Chennai, Mumbai | Short term (≤ 2 years) |

| Vendor Consolidation into Integrated and Outcome-based Contracts | +1.9% | National, concentrated in Tier-1 and Tier-2 commercial hubs | Medium term (2-4 years) |

| Wider Adoption of Smart Buildings and Predictive Maintenance | +1.6% | National, primarily Grade A office and data center stock | Medium term (2-4 years) |

| Sustainability-led Demand for Energy, Water and Waste Optimization | +1.2% | National, with regulatory influence led by Maharashtra and Telangana | Medium term (2-4 years) |

| Global Capability Centre Expansion Beyond Tier-1 Hubs | +0.8% | National, with early gains in Ahmedabad, Jaipur, Kochi, Coimbatore, Indore | Long term (≥ 4 years) |

| Data Centre and Mission-critical Infrastructure Buildout | +0.7% | National, concentrated in Mumbai, Chennai, Delhi-NCR, Bengaluru, with Tier-2 expansion | Short term (≤ 2 years) and Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion Of Grade A Offices and Mixed-use Campuses

India’s Grade A office market delivered its strongest year on record in 2025, with net absorption of 61.4 million sq ft across the top 8 cities, up 25% year over year, thereby directly expanding the professionally managed estate that requires continuous operating support.[1]Cushman & Wakefield, “India Office Market Performance in 2025,” Cushman & Wakefield. India is also expected to account for 40% of Asia-Pacific’s 61.3 million sq ft of new Grade A office supply in 2026, which keeps the onboarding pipeline active for the India integrated facility management market.[2]Economic Times, “Grade A Demand Outlook for 2026 in India Offices,” The Economic Times. The quality mix matters as much as the quantity mix, because 80% of the new 2026 supply is expected to be green-certified, and that raises the service threshold for energy management, water monitoring, indoor air quality control, and audit-ready reporting.[3]Colliers, “Green-certified Office Supply Outlook in India for 2026,” Colliers Mixed-use campuses are also bringing office, retail, hospitality, and food service functions into a single managed environment, which makes owners more likely to appoint one accountable operator across multiple service lines. This combination of scale, technical requirements, and ownership preference continues to favour integrated providers with balanced Hard FM and Soft FM depth, which supports the move toward fuller IFM contracts within the India integrated facility management market.

Vendor Consolidation into Integrated and Outcome-based Contracts

The India integrated facility management market is moving away from headcount-driven contracts and toward SLA-linked commercial models that measure uptime, energy efficiency, hygiene quality, and user experience rather than just labour deployment. Enterprises that use a single IFM partner across 5 or more service categories have reported an average 18% reduction in vendor management overhead, which gives procurement teams a direct cost and control argument for consolidation.[4]Stalwart Group, “Vendor Management Overhead Reduction Under Integrated Contracts,” Stalwart Group. This shift also lifts the strategic value of Hard FM, because technical metrics such as HVAC uptime, electrical reliability, and power usage performance are easier to verify and govern than many soft-service outputs at the bid stage. Institutional ownership is expanding across India’s office stock, with more than 380 million sq ft of Grade A space carrying REIT potential, and these owners prefer consistent standards across distributed portfolios rather than separate local operating arrangements. As this model becomes standard, smaller firms without national reach, data systems, and compliance depth are likely to lose share in the India integrated facility management market even when they remain locally competitive on price.

Wider Adoption of Smart Buildings and Predictive Maintenance

IoT sensors, AI-led analytics, and integrated Building Management Systems are shifting the India integrated facility management market from reactive maintenance toward predictive and more structured operating models. JLL has noted that AI tools can reduce equipment downtime by up to 50% and extend asset life by 20% to 40%, while some Bengaluru office complexes have reported energy savings of up to 35% after adopting AI-driven energy management systems. The benefits are clustering in higher-quality assets, and that matters because 79% of GCC office leasing in Q1 2026 was in green-certified buildings, which reinforces the link between premium real estate and deeper FM service intensity. Predictive maintenance platforms connected with computerized maintenance systems can reduce maintenance costs by 25% versus reactive models and can reach payback within 12 to 18 months, which helps providers defend higher base fees on integrated contracts. The result is a wider performance gap between organized providers that can operate data-rich environments and manual operators that still compete mainly on labour deployment, which is steadily reshaping the India integrated facility management market.

Sustainability-led Demand for Energy, Water and Waste Optimization

Sustainability-linked service demand is becoming an operating requirement rather than a branding option across large offices, campuses, and industrial sites within the India integrated facility management market. The immediate push comes from the growing share of green-certified stock, because 80% of new 2026 office supply is expected to carry green credentials and therefore needs closer tracking of energy, water, waste, and indoor environment conditions. Buildings consume nearly one-third of India’s total energy use, so clients are now treating energy management as a direct cost-control lever as well as a reporting requirement. ECBC-compliant buildings have demonstrated energy consumption reductions of 30% to 50% compared with conventional buildings, which strengthens the commercial case for specialist monitoring, audits, and optimization inside FM contracts. Providers that can combine BMS analytics, engineering support, and documented sustainability practices are therefore better placed to win higher-quality work as the India integrated facility management market shifts toward more accountable service scopes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-led Competition from Unorganized Vendors | -1.5% | National, more acute in Tier-2 and Tier-3 cities and soft FM segments | Short term (≤ 2 years) and Medium term (2-4 years) |

| Skilled Workforce Attrition and Wage Inflation | -0.8% | National, with higher wage premiums in metro areas | Short term (≤ 2 years) and Medium term (2-4 years) |

| Working-capital Stress from Delayed Receivables | -0.5% | National, particularly in government and public-sector contracts | Medium term (2-4 years) |

| Utility Reliability and Water-stress Exposure in Critical Assets | -0.3% | National, most acute in data center and healthcare facility corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-led Competition from Unorganized Vendors

Price-led competition from unorganized vendors remains the clearest structural brake on the India integrated facility management market, with smaller operators undercutting organized firms by 15% to 20% by bypassing Provident Fund, Employees’ State Insurance, and minimum wage obligations. The pressure is strongest in cleaning, housekeeping, and security, where labour is the main cost input and output quality is often harder for buyers to benchmark objectively during procurement. The problem does not end at contract award, because the visible price gap then shapes renewal discussions and creates fresh pressure on organized firms to accept lower rates on compliant delivery models. India’s labour code consolidation could improve the competitive balance over time, but state-level implementation remains uneven, and that keeps enforcement outcomes inconsistent across locations. Even so, large enterprise buyers are slowly shifting from lowest-bid decisions toward total-cost-of-ownership reviews, which should gradually improve the quality mix in the India integrated facility management market.

Skilled Workforce Attrition and Wage Inflation

Labor availability is tightening across the India integrated facility management market, with blue-collar attrition in labour-intensive sectors running at 5% to 7% and frontline FM churn reaching 10% to 20% a month at some providers. Gig platforms have added another layer of pressure by offering daily payouts of INR 800 to 1,200 (USD 9.5 to 14.3), and that flexibility competes directly with fixed monthly frontline roles. Wages in labour-intensive categories are rising 5% to 6% a year, while organized provider operating margins were estimated near 5% in FY26, which leaves limited room to absorb turnover and retraining costs. The shortage is more serious in technical roles such as HVAC, MEP, and BMS support because service-level failures in these functions are more visible to clients and have a direct effect on renewal decisions. Firms that build in-house academies, apprenticeships, and stronger retention systems are therefore gaining a more durable operating advantage as the India integrated facility management market becomes more technical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Growth Outpacing Broad Market

Hard facility management (FM) is forecast to expand at a 9.47% CAGR through 2031, which places it ahead of the overall growth rate and makes it the strongest service-side growth engine in the India integrated facility management (IFM) market. This acceleration is closely tied to higher technical density in Grade A assets and to data center expansion, with national capacity projected to rise from nearly 1.7 GW at the end of 2025 to more than 4 GW by FY30. That buildout increases demand for MEP services, HVAC management, electrical reliability, power backup support, and 24/7 technical staffing that general service operators cannot easily scale. Asset management services are also gaining a larger role as REIT-led portfolios and GCC campuses shift from periodic maintenance cycles toward lifecycle planning, replacement tracking, and capex-linked stewardship.

Soft FM held 67.19% share of the India IFM market size in 2025, which reflects the large labour base needed for cleaning, catering, office support, and security across India’s commercial, hospitality, healthcare, and institutional estate. The segment remains the revenue anchor for many providers because it touches daily occupancy experience and is difficult for large occupiers to internalize across multi-site portfolios. Even so, the service mix inside integrated contracts is gradually shifting, because hard services carry higher value per square foot and support more measurable SLA outcomes than many labour-heavy soft lines. Cleaning is benefiting from mechanization and robotic floor care, while office support and security functions are being upgraded through AI-assisted surveillance and intelligent visitor management, which helps the India IFM industry defend service quality in a price-sensitive environment.

By End User: Industrial Dominance Challenged by Commercial Momentum

The Industrial and Process Sector held 29.48% of the India integrated facility management market share in 2025, making it the largest end-user block by revenue. This position reflects the size, uptime needs, safety demands, and technical maintenance intensity of manufacturing plants, warehouses, logistics parks, mining assets, and energy facilities that continue to expand under domestic production programs. Demand in this segment is also becoming more compliance-linked, because multinational operators increasingly require service documentation, maintenance logs, and safety performance that align with audit-heavy operating systems. Logistics and warehousing are widening the addressable base further, since modern Grade A facilities now need integrated MEP, pest control, hygiene, and monitoring support rather than basic caretaking alone.

Commercial end users are projected to grow at a 9.11% CAGR through 2031, which makes them the fastest-expanding demand center in the India IFM market. GCC occupiers are central to this momentum, accounting for more than 44% of India’s office gross absorption in Q1 2026, and their campuses typically require workplace experience, sustainability support, catering, and technical FM in one coordinated scope. Healthcare is also becoming more relevant as hospitals and large care networks place greater emphasis on uptime, hygiene, biomedical support, and audit readiness within outsourced delivery structures. Hospitality, education, and government institutions add stability to the mix, and their increasingly standardized service expectations are lifting the baseline operating requirements across the India IFM industry.

Geography Analysis

The India integrated facility management market is concentrated in the major office and infrastructure corridors, with Bengaluru, Delhi-NCR, Hyderabad, Chennai, and Mumbai forming the core demand base for integrated contracts. This concentration reflects the location of India’s deepest Grade A office inventory, its highest-value mixed-use campuses, and the largest clusters of multinational occupiers and GCC operators. Record net absorption of 61.4 million sq ft across the top 8 cities in 2025 reinforced this metro-led pattern, because every newly occupied building expands the pipeline for multi-year operations, maintenance, cleaning, security, and workplace support services. The India integrated facility management market also benefits from the fact that new premium stock is increasingly green-certified and institutionally owned, which raises the need for standardized delivery and portfolio-level reporting across city networks. Large occupiers are therefore more willing to appoint providers with broad city coverage rather than separate local vendors, especially when contracts include technical services, sustainability tasks, and workplace management.

Bengaluru and Hyderabad remain especially important because GCC demand is deep, office quality is high, and occupiers are more likely to seek integrated, technology-enabled service models. Mumbai and Chennai carry added importance for the India integrated facility management market because they are also central to data center expansion, which increases the share of technically demanding Hard FM work and raises the value of engineering capabilities. Delhi-NCR combines large office campuses with mixed-use developments and a strong public and corporate client base, making it a key geography for scale-driven providers that want broad contract portfolios. These metro corridors are where organized firms can best convert national client relationships into multi-city mandates, because procurement teams prefer uniform service standards across their largest occupied locations.

The next layer of opportunity is moving into Ahmedabad, Jaipur, Kochi, Coimbatore, and Indore, where GCC expansion and managed campus development are starting to create a longer-term demand base for the India integrated facility management market. These cities do not yet offer the same contract density as Tier-1 hubs, but they matter because they let national providers extend networks before local competition formalizes at scale. The delivery model in these markets is likely to favour hub-and-spoke operations, where regional management and digital supervision are combined with local execution teams to manage cost and service consistency. Price sensitivity remains higher outside Tier-1 clusters, so the pace of organized penetration will depend on how quickly occupiers shift from lowest-cost procurement toward compliance, accountability, and measurable outcomes.

Competitive Landscape

The India integrated facility management market remains fragmented, with more than 1,200 registered service providers, but consolidation is becoming clearer at the top as organized leaders widen their advantage through scale, compliance systems, technology spending, and sector specialization. Winning large mandates now depends less on simple workforce capacity and more on the ability to manage SLA reporting, statutory compliance, audit readiness, and multi-city execution without service breaks. That is why the strongest firms are building operating moats around pan-India coverage, digital workflows, engineering depth, and the ability to support both Hard FM and Soft FM within one commercial framework. The India integrated facility management market is also separating along capital access lines, because firms with stronger balance sheets can invest in acquisitions, automation, and working capital while smaller peers remain tied to manual delivery and shorter planning cycles. Global players are benefiting as well, since India’s growing role as a GCC hub lets them extend existing international client relationships into local FM mandates with lower account acquisition friction.

SIS Limited’s majority acquisition of AP Securitas for INR 600 crore (USD 71.4 million), added nearly INR 1,200 crore (USD 142.9 million), in annualized revenue and marked the company’s largest purchase in FY26, showing how organized leaders are using M&A to strengthen regional density and revenue scale. SIS also invested more in AI-led automation, robotics, and technology partnerships under its Vision 2030 roadmap, which shows that the competitive race is moving beyond labour scale alone. BVG India’s October 2025 IPO refiling pointed in the same direction, with a proposed INR 300 crore fresh issue and FY25 consolidated revenue of INR 3,301.8 crore (USD 393 million), up 16.3% year over year. ISS demonstrated the multinational route into the India integrated facility management market through a 5-year India contract valued at DKK 100 million (USD 14.5 million), annually at the 2025 IRS, built on an existing European client relationship.

White space in the India integrated facility management market is strongest in healthcare FM, data center FM, and sustainability-linked services, where technical depth and delivery scale still do not often sit within the same provider. This creates room for capable challengers, but margin risk remains real because working capital can tighten quickly when public-sector receivables are delayed or when large contracts are won at aggressive rates. The next stage of consolidation is therefore likely to reward companies that can embed IoT monitoring, predictive maintenance, and auditable energy reporting into base contracts rather than sell them as optional add-ons. In practical terms, the India integrated facility management market is moving toward a structure where data quality, engineering reliability, and capital discipline matter at least as much as headcount.

India Integrated Facility Management Industry Leaders

BVG India Limited

Compass Group India (Compass Group PLC)

ISS Facility Services India Pvt. Ltd. (ISS A/S)

Impressions Services Private Ltd.

Krystal Integrated Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SIS Limited reported consolidated FY26 revenue of INR 16,030 crore (USD 1.91 billion), a 21% year-on-year increase; the Facility Management Solutions segment achieved its highest-ever quarterly EBITDA at INR 35 crore and 26.5% year-over-year growth in Q4 FY26; the company targets INR 20,000 crore (USD 2.38 billion) by FY27. Business Standard, May 2026.

- March 2026: CBRE South Asia Private Limited secured an end-to-end facility management mandate for CRC The Flagship, a 2.4 million sq ft Grade A+ IT and ITES commercial development on the Noida Expressway, covering operations and maintenance, predictive maintenance, sustainability management, and smart building systems, including BMS. Constro Facilitator, March 2026.

- October 2025: SIS Limited acquired a majority stake in Delhi-based AP Securitas for approximately INR 600 crore (USD 71.4 million), its largest acquisition, adding approximately INR 1,200 crore (USD 142.9 million) in annualized revenue and significantly expanding coverage in the National Capital Region market. Fortune India, March 2026.

- October 2025: BVG India Limited refiled its Draft Red Herring Prospectus with SEBI for an IPO comprising a INR 300 crore (USD 35.7 million) fresh issue plus an offer for sale, with proceeds primarily earmarked for debt repayment; the company reported INR 3,301.8 crore (USD 393 million) in consolidated revenue in FY25, up 16.3% year over year. Moneycontrol, October 2025.

India Integrated Facility Management Market Report Scope

India Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the India integrated facility management market by 2031?

The India integrated facility management market is projected to reach USD 20.34 billion by 2031 from USD 13.50 billion in 2026, at a CAGR of 8.5% over 2026-2031.

Which service category is growing the fastest in India?

Hard FM is the fastest-growing service type, with a forecast CAGR of 9.47% through 2031, supported by data centers, technical buildings, and more complex engineering requirements.

Which end-user group contributes the most revenue today?

The Industrial and Process Sector was the largest end-user segment in 2025, holding 29.48% of total revenue, driven by manufacturing, logistics, energy, and process-intensive operations.

Why are commercial occupiers becoming more important for service providers?

Commercial demand is forecast to grow at 9.11% through 2031, helped by strong GCC leasing, large Grade A campuses, and higher demand for workplace, sustainability, and technical support in one contract.

What is pushing contract values higher across large sites?

Buyers are shifting from labor-based contracts toward SLA-led models that measure uptime, energy use, hygiene, and user outcomes, which increases the value of integrated and technically capable service providers.

What is the biggest challenge for organized operators in India?

The biggest challenge remains price competition from unorganized vendors, especially in soft services, along with labor attrition and wage inflation that keep pressure on margins and service continuity.

Page last updated on: