Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

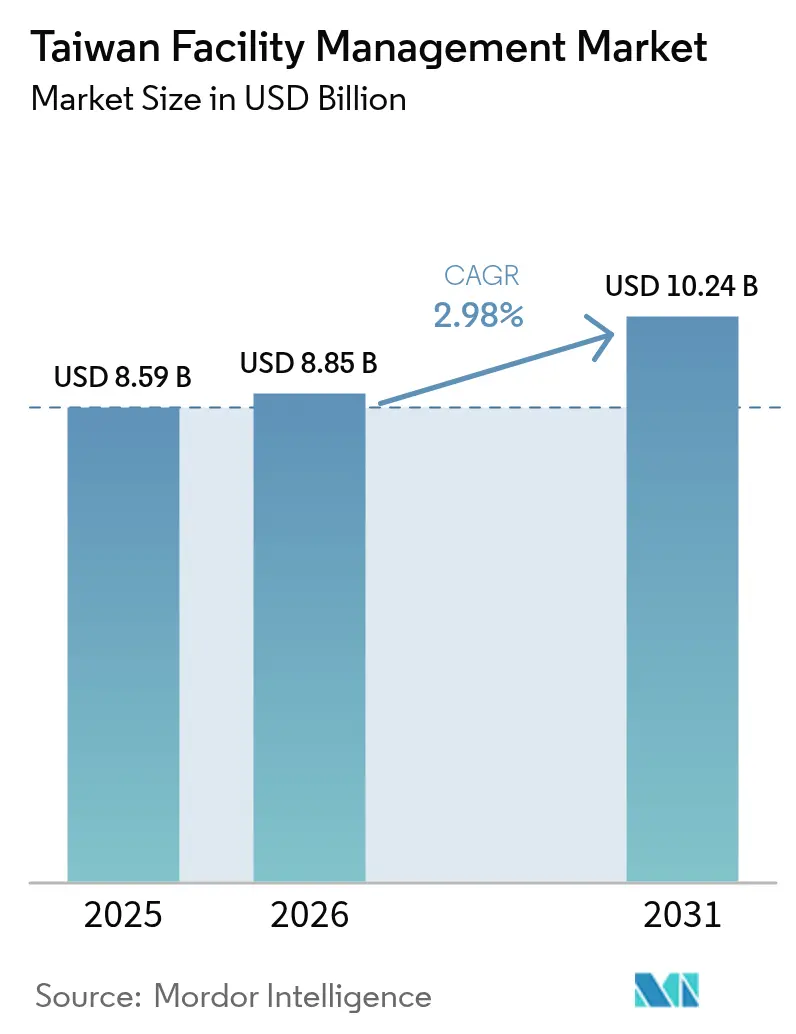

| Base Year Market Size (2025) | USD 8.59 Billion |

| Market Size (2026) | USD 8.85 Billion |

| Market Size (2031) | USD 10.24 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

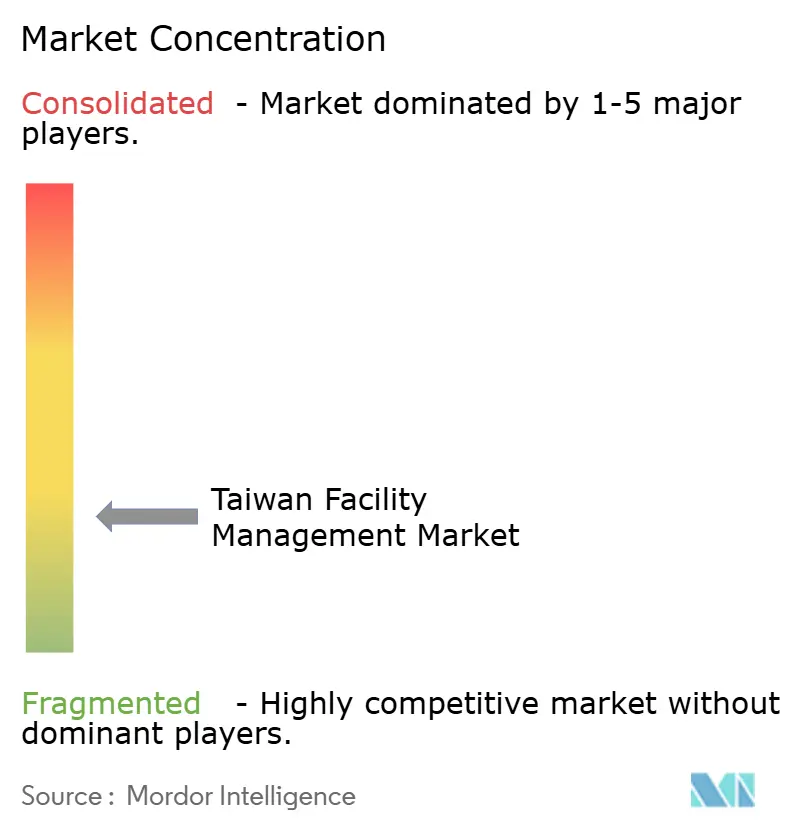

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Facility Management Market Analysis by Mordor Intelligence

Taiwan facility management market size in 2026 is estimated at USD 8.85 billion, growing from 2025 value of USD 8.59 billion with 2031 projections showing USD 10.24 billion, growing at 2.98% CAGR over 2026-2031. The expansion of the Taiwan facility management market reflects three structural forces: the demographic pivot to a super-aged society, the public sector’s USD 5.8 billion sovereign AI build-out, and tightening workplace-safety and green-building rules. Demand for hard services remains dominant because semiconductor fabs, data centers, and mixed-use transport hubs require meticulous mechanical, electrical, and plumbing (MEP) oversight. At the same time, chronic labour shortages and a sharp rise in outsourcing have moved soft-service contracts—security, cleaning, front-of-house, and workplace experience—up the corporate agenda. Vendors able to combine Internet-of-Things (IoT) monitoring, AI-enabled predictive maintenance, and certified green-building methodologies capture rising premiums in healthcare and secondary-city mega-projects. Fees, however, face pressure because more than 200 registered service providers bid on government projects, and many clients still award contracts solely on lowest price.

Key Report Takeaways

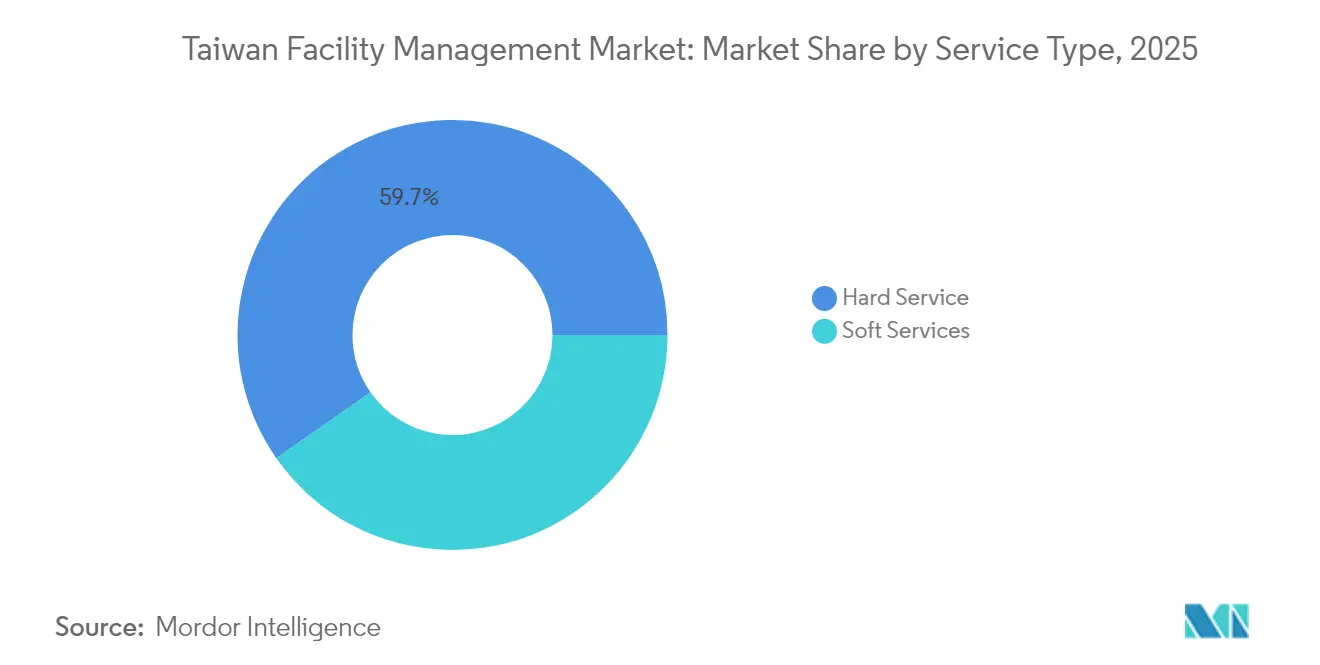

- By service type, hard services held 59.72% of Taiwan's facility management market share in 2025, while soft services are projected to grow at a 4.9% CAGR during 2026-2031.

- By offering type, outsourced models commanded 66.12% of the Taiwan facility management market size in 2025 and are forecast to advance at a 4.82% CAGR to 2031.

- By end-user industry, commercial facilities led with 39.88% revenue share in 2025; industrial and process facilities are expected to record the fastest 6.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and Population Growth in Major Metros | +1.1% | Taipei, New Taipei, Taoyuan, Taichung | Medium term (2-4 years) |

| Increasing Corporate Outsourcing of Non-Core Facility Operations | +0.8% | National, concentrated in tech corridors | Short term (≤ 2 years) |

| Mandatory Green Building Certifications and Retrofits | +0.6% | National, early adoption in major cities | Long term (≥ 4 years) |

| Infrastructure Pipeline Investment | +0.4% | National, priority in secondary cities | Medium term (2-4 years) |

| Proliferation of Mixed-Use Mega-Developments in Secondary Cities | +0.3% | Taichung, Kaohsiung, Tainan | Long term (≥ 4 years) |

| Advancement in Facility Management Technology | +0.2% | National, tech sector leadership | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanisation and population growth in major metros

Taiwan’s shifting population puts simultaneous pressure on legacy urban cores and newly urbanising rings. Taipei’s headcount fell below 2.5 million in 2024, while New Taipei and Taoyuan added residents each month, driving demand for new residential, retail, and science-park assets. The TWD 720 billion loan window within the Extended Invest Taiwan programme aims to mobilise TWD 1.2 trillion in private capital for such assets, locking in long-cycle facility management contracts. Nvidia’s 3.89-hectare Constellation campus underscores how tech giants act as anchor tenants that insist on predictive-maintenance regimes and energy-optimised HVAC. Peripheral universities that receive the Water Resources Agency’s TWD 13.2 billion research-park funds also require integrated facility management spanning classrooms, dormitories, and pilot lines.[1] 鉅亨網, “政院投132億建重點校際研教園區…,” cnyes.com The combined effect raises baseline demand for certified technicians capable of migrating between ageing stock and smart buildings.

Increasing corporate outsourcing of non-core facility operations

Hospitals, rail operators, and semiconductor fabs increasingly view non-core tasks as financial drag. Taipei MRT relied on an Analytic Hierarchy Process to rank electromechanical maintenance priorities, after which it outsourced air-conditioning and power-supply work to specialist firms. Hospitals adopt similar logic; 78% of nurses work overtime and 12% leave annually, so administrators externalise cleaning, catering, and building operations. The hospitality sector likewise outsources because it cannot hire enough on-premise technicians even after offering housing subsidies. Manufacturers echo the pattern; fixed-asset purchases jumped 69.1% year-on-year in Q4 2024 yet focused on production equipment, not facilities, so upkeep of clean rooms, power plants, and fire systems shifts to managed-service partners. Vendors that deliver verifiable uptime and carbon-reduction metrics differentiate amid tight service-level agreements.

Mandatory green-building certifications and retrofits

Taiwan’s Ecology, Energy Saving, Waste Reduction, Health (EEWH) scheme has evolved from a voluntary label to a compliance mandate. Since 2025, hospitals must implement programmes that cut 99,000 tonnes of carbon annually or lose budget incentives. Construction costs rise 10-15% when designers specify low-emission materials and smart-lighting controls. Flagship projects such as Tainan’s Forest NEX recorded 30% CO₂ cuts en route to blue-diamond status, signalling market willingness to absorb higher capex in exchange for lifetime operating savings. Real-estate players follow suit; Shin Kong Life’s Huashan Financial Center targets silver certification yet maintains 50% occupancy, showing lessees will pay a rent premium for better air quality and lower energy bills. Facility managers, therefore, integrate commissioning, energy analytics, and occupant-health metrics into service scopes.

Infrastructure pipeline investment

Public outlays of TWD 236.4 billion across 105 construction projects support a steady queue of airports, rail links, and desalination facilities. The Railway Bureau manages the Airport Terminal 3 link and the Chiayi elevated line, each requiring life-cycle asset-management plans that span traction, signalling, and passenger amenities. SUEZ’s EUR 508 million Hsinchu desalination plant will deliver 100,000 m³ per day after 2028 and includes a 20-year operations contract that bundles mechanical maintenance, membrane cleaning, and remote monitoring. Semiconductor projects deepen the trend: clean-room specialists UIS and L&K Engineering reported record TWD 179 billion in combined orders for fabs that will rely on continuous FM support. Consequently, service providers with rail, water, and high-tech credentials lock in long-term revenue visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Talent Shortage in Specialized FM Skills | -0.5% | National, acute in tech and healthcare sectors | Long term (≥ 4 years) |

| Price Wars Due to Highly Fragmented Vendor Landscape | -0.3% | National, intensified in commodity services | Medium term (2-4 years) |

| Regulatory and Legislative Framework for Market Entrants | -0.2% | National, complex compliance requirements | Short term (≤ 2 years) |

| Impact of Macroeconomic Indicators on FM Demand | -0.1% | National, sector-specific variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent talent shortage in specialised FM skills

Super-ageing demographics shrink Taiwan’s labour pool even as facility complexity rises. The economy lists 247,000 open positions, including 53,000 in construction, leaving many campuses without licensed electricians or HVAC fitters. [2]公視新聞網 PNN, “大缺工時代來臨…,” pts.org.tw Younger workers prefer predictable hours and digital workflows, yet legacy apprenticeship routes rarely provide them. Hospitals face parallel stress: nurse attrition forces rescheduling of preventive maintenance because wards cannot spare spare rooms for shutdowns. Hotels offer lodging and higher wages but still struggle to fill steward and technician posts. Vendors therefore blend AI sensors, centralised command centres, and remote-support tablets to reduce on-site headcount, as KONE’s elevator fleet shows with a 40% drop in entrapment risk.

Price wars due to highly fragmented vendor landscape

More than 200 local firms compete for municipal tenders, and procurement rules still emphasise lowest bid. Government requests even pushed building-material prices down 5-10% in mid-2025, squeezing subcontractor margins. [3]Blocktempo, “打房逼到建商!…,” blocktempo.com Smaller providers lack scale to finance IoT roll-outs or ISO certification, yet must match discount rates set by global players that cross-subsidise Taiwan with overseas profits. International firms such as ISS A/S and CBRE Group leverage integrated platforms to keep cost-to-serve low and still invest in analytics. The resulting spread widens every annual renewal cycle, prompting small operators either to exit or merge, which in turn fosters a gradual consolidation trend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard services remain dominant, soft services accelerate

Hard services accounted for 59.72% of Taiwan facility management market share in 2025 thanks to a manufacturing estate dotted with power-hungry semiconductor fabs and data centers. Clients demand uninterrupted MEP, clean-room filtration, and fire-suppression operations, supporting a resilient revenue base for specialised contractors. Soft services, however, show stronger momentum, expanding at a 4.9% CAGR through 2031 as employers bundle cleaning, concierge, and workspace well-being into staff-retention packages amid labour scarcity. Asset-management assignments rise because the super-aged building stock needs structured capital-planning, particularly across 15 public hospitals where EEWH retrofits proceed in phases. MEP and HVAC workloads also jump, fuelled by server-hall expansions under the sovereign-AI initiative. Fire-safety audits tighten post-February-2025 guideline updates that force employers to form in-house investigation teams after incidents.

Hard-service vendors now integrate IoT sensors that feed predictive-maintenance engines able to flag motor-bearing failures seven days before stoppage. The practice helps semiconductor clients avoid particulate spikes that can destroy wafers worth USD 100 million per batch. In soft services, workplace-experience apps schedule desk hoteling, food delivery, and micro-break cleaning, thereby lifting occupant satisfaction scores even with lean staff. The broader effect is a subtle shift from commodity cleaning to value-based employee-services contracts, which gradually narrows the price gap between hard and soft portfolios.

By Offering Type: Outsourcing extends its lead

Outsourced models contributed 66.12% of Taiwan facility management market size in 2025 and post the fastest 4.82% CAGR to 2031 as boards channel scarce staff toward revenue-generating roles. Integrated FM solutions gain traction because single-provider accountability simplifies risk management for multi-site giants such as TSMC, which operates 11 local production lines. Bundled FM suits mid-size firms that prefer cost savings without full integration, while single-service contracts persist where facilities require best-of-breed skills, for example biocontainment labs. In-house teams remain only where intellectual-property and security mandates override savings, notably within defence R&D units and certain central-bank vaults.

Within outsourcing, outcome-based agreements replace labour-hour billing. Clients specify uptime, energy-intensity benchmarks, and occupant health metrics, while vendors invest in dashboards that auto-pull sensor data to demonstrate compliance. The feedback loop enables shared savings models, rewarding providers with bonus pools once energy spends fall below baseline. Capability gaps widen in favour of firms that combine on-site technicians with off-site analytics centres, driving acquisitions such as Exyte’s January 2025 purchase of Kinetics Group, which brings semiconductor and biopharma credibility.

By End-User Industry: Commercial leads, industrial surges

Commercial buildings, especially tech campuses and retail-logistics nodes, captured 39.88% revenue in 2025, underpinned by Taiwan’s services pivot. Data centers integral to the AI-infrastructure roadmap accelerate requirements for redundant power and high-density cooling. Industrial and process facilities, however, chart a 6.71% CAGR through 2031 because semiconductor firms lifted fixed-asset purchases to TWD 695.2 billion in Q4 2024, outlaying for new fabs in Hsinchu and Kaohsiung. Healthcare facilities present complex compliance matrices; nurse shortages drive cleaning and porter outsourcing, while EEWH standards oblige chiller retrofits that lower hospital energy bills 12%. Hospitality lags in certification, with only 154 of 14,000 hotels holding green labels, so retrofit spending will rise through 2030 as international sports events demand eco-accredited accommodation.

Institutional projects benefit from the TWD 236.4 billion public-construction pipeline, adding rail stations, libraries, and social-housing complexes that bake in smart-building and community-care features. Mixed-use schemes in Taichung’s D-ONE and Kaohsiung’s Asia New Bay Area integrate shopping, coworking, and aged-care amenities, requiring cross-functional facility-management playbooks. Other segments—multi-housing, entertainment, and education—ride on population ageing and infrastructure grants, enlarging the addressable Taiwan facility management market.

Geography Analysis

Taipei remains the single largest client base even as net migration turns negative because its premium stock of grade-A offices, hospitals, and cultural venues demands continuous technical stewardship. Legacy towers undergo curtain-wall replacements and chiller upgrades that increase per-square-meter service billings. New Taipei and Taoyuan are the growth engines; the latter attracts mega-campuses under the Extended Invest Taiwan scheme, including Foxconn’s latest AI-server plant, and therefore locks in long-term mechanical, security, and logistics commitments. Taoyuan also hosts the Farglory Free-Trade Zone, a 32,917-square-meter lease that requires 24/7 access-control and thermal-plant oversight.

Secondary cities register strong pipeline momentum. Taichung enjoys 70% pre-sales at the 總太 V1 office tower and prepares to open the D-ONE shopping centre, Taiwan’s largest by retail area. Facilities adopt multi-tenant energy dashboards that allocate costs per store, elevating demand for certified energy managers. Kaohsiung leads smart social-housing pilots that embed AI medical suites and rooftop solar across TWD 11 billion worth of apartments slated for 2031 completion. Each building block specifies predictive-maintenance protocols from handover, guaranteeing vendors an annuity revenue stream.

Tainan blends heritage redevelopment with lagoon-front condominiums such as the 457-unit Mansion of Waterfront, where residents pay service fees pegged to EEWH performance. Hsinchu remains a specialised zone for fabs, where particle contamination targets dictate air-change rates at up to 300 per hour, creating niche premium for hyper-clean technicians. Across all regions, transport projects like the Airport Terminal 3 MRT line widen the catchment for commuters and thereby raise footfall in adjacent commercial districts, which then contract integrated FM teams to keep escalators, lifts, and surveillance systems fault-free.

Competitive Landscape

The Taiwan facility management market houses a blend of multinational conglomerates and over 150 domestic firms. Global outfits such as CBRE and ISS leverage regional command centres to bulk-buy sensors and deploy joint digital platforms, enabling them to deliver 22% year-on-year revenue gains in 2024 while holding margins despite wage inflation. Mid-tier specialists thrive in semiconductor niches; clean-room contractors supply ISO 14644-1 Class 1 environments and command premium call-out fees. Exyte’s 2025 acquisition of Kinetics Group shows consolidation around high-tech verticals, allowing end-to-end packages from design to ongoing asset care.

Local providers compete on responsiveness and home-market knowledge but struggle to fund R&D. Some join forces with OEMs: Siliconware’s partnership to launch a 1 MW on-site solar-plus-storage microgrid positions it as both facility operator and power-services intermediary. Technology integration is the main differentiator; KONE’s AI predictive maintenance cuts technician visits by 25%, freeing staff for more complex tasks and reducing service level agreement breaches. Regulatory literacy also matters; companies with documented safety systems gain fast-track approvals under February 2025 guideline changes, easing tender submission.

Although price competition persists, the market edges towards value-based contracts. Firms that document energy savings or uptime improvements win loyalty in healthcare and transport segments. Fragmentation gradually subsides as top-tier multinationals expand share and local champions merge to attain scale. The combined top five players now control about 55% of spending, suggesting a moderately concentrated structure that is moving toward oligopolistic equilibrium.

Taiwan Facility Management Industry Leaders

Diversey Holdings, Ltd

Rentokil Initial Plc

ABV Integrated Facility Services

AssetPlus Taiwan Limited

Evergreen International Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Foxconn subsidiary Ingrasys Technology leased 32,917 m² in Taoyuan’s Farglory Free-Trade Zone to expand AI-server production, anticipating 50% topline growth.

- July 2025: Taiwan Speciality Chemicals Corp bought 65% of Hung Jie Technology for TWD 3 billion, boosting semiconductor parts-cleaning capacity and associated FM services.

- June 2025: SUEZ, CTCI, and Hung Hua signed a EUR 508 million contract to build Hsinchu’s seawater desalination plant, securing a multi-year operations package

- January 2025: Exyte acquired Kinetics Group to reinforce high-tech facility-management offerings in biopharma and semiconductors

Taiwan Facility Management Market Report Scope

Facility management (FM) is the sector or industry that incorporates many disciplines to ensure the safety, functionality, comfort, and efficiency of the built environment by integrating people, processes, places, and technology.

The Taiwan facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Taiwan facility management market?

The Taiwan facility management market size is USD 8.85 billion in 2026.

Which segment is growing fastest?

Industrial and process facilities show the highest projected growth with a 6.71% CAGR through 2031.

Why are soft services gaining traction?

Labour shortages and the war for talent push employers to outsource cleaning, security, and workplace-experience functions that enhance staff retention.

How do green-building rules affect facility budgets?

EEWH compliance lifts construction costs 10-15% but reduces lifetime energy expenses and attracts premium rents.

Which cities present the most new business?

Taoyuan, Taichung, and Kaohsiung lead demand because of tech-park expansion, mixed-use retail projects, and smart social-housing pilots.

What role does AI play in the sector?

AI-enabled predictive maintenance lowers equipment downtime and offsets technician shortages by identifying faults before failure.

Page last updated on: