Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.05 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.71 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Facility Management Market Analysis by Mordor Intelligence

The Ireland facility management market size is expected to increase from USD 2.05 billion in 2025 to USD 2.16 billion in 2026 and reach USD 2.71 billion by 2031, growing at a CAGR of 4.64% over 2026-2031. Driven by the country’s role as a European data-center hub, the shift toward integrated contracts is displacing fragmented single-service arrangements as clients demand cost transparency and outcome-based metrics. Accelerating regulatory deadlines for near-zero-energy buildings are expanding recurring revenue streams tied to building management systems. Intensifying wage pressure, persistent labor shortages, and legacy building constraints tighten provider margins, while consolidation among mid-tier players is reshaping competitive dynamics. Clients are increasingly favoring risk-sharing partnerships that bundle hard and soft services under single vendors able to invest in IoT platforms and predictive maintenance capabilities.

Key Report Takeaways

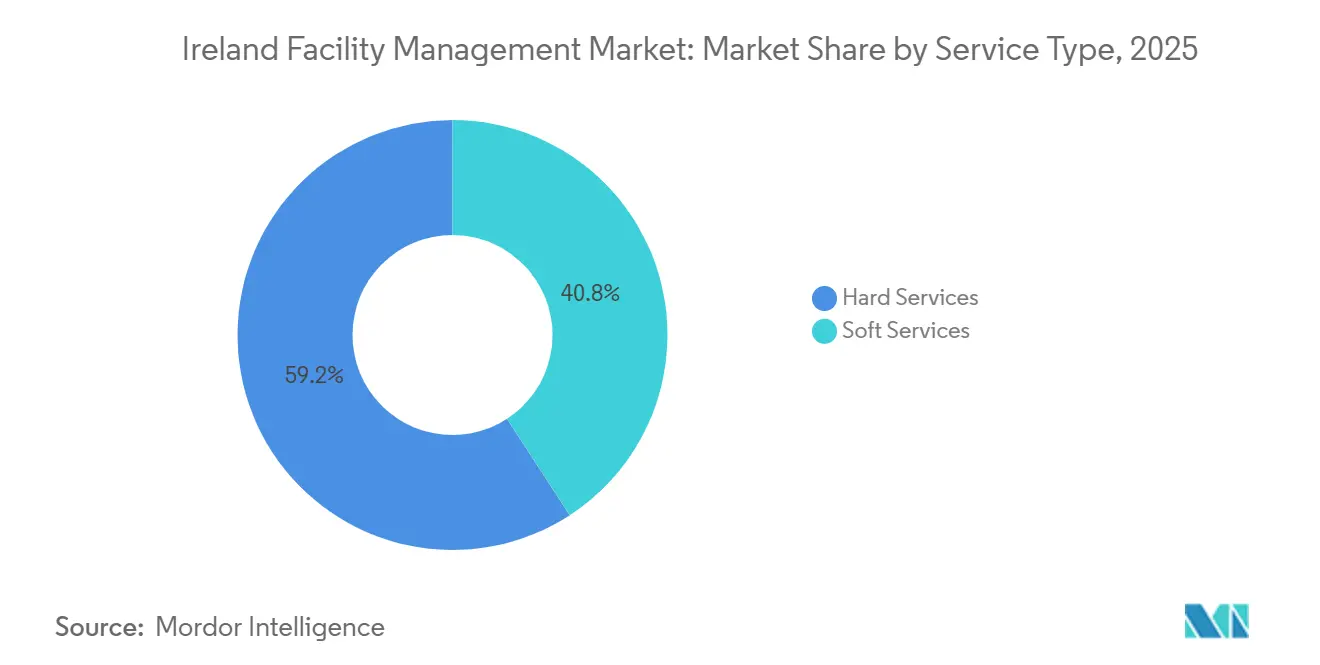

- By service type, hard services led with 59.19% of the Ireland facility management market share in 2025, while soft services are projected to expand at a 4.86% CAGR to 2031.

- By offering mode, outsourcing accounted for 67.68% share of the Ireland facility management market size in 2025, and the segment is forecast to grow at a 4.73% CAGR through 2031.

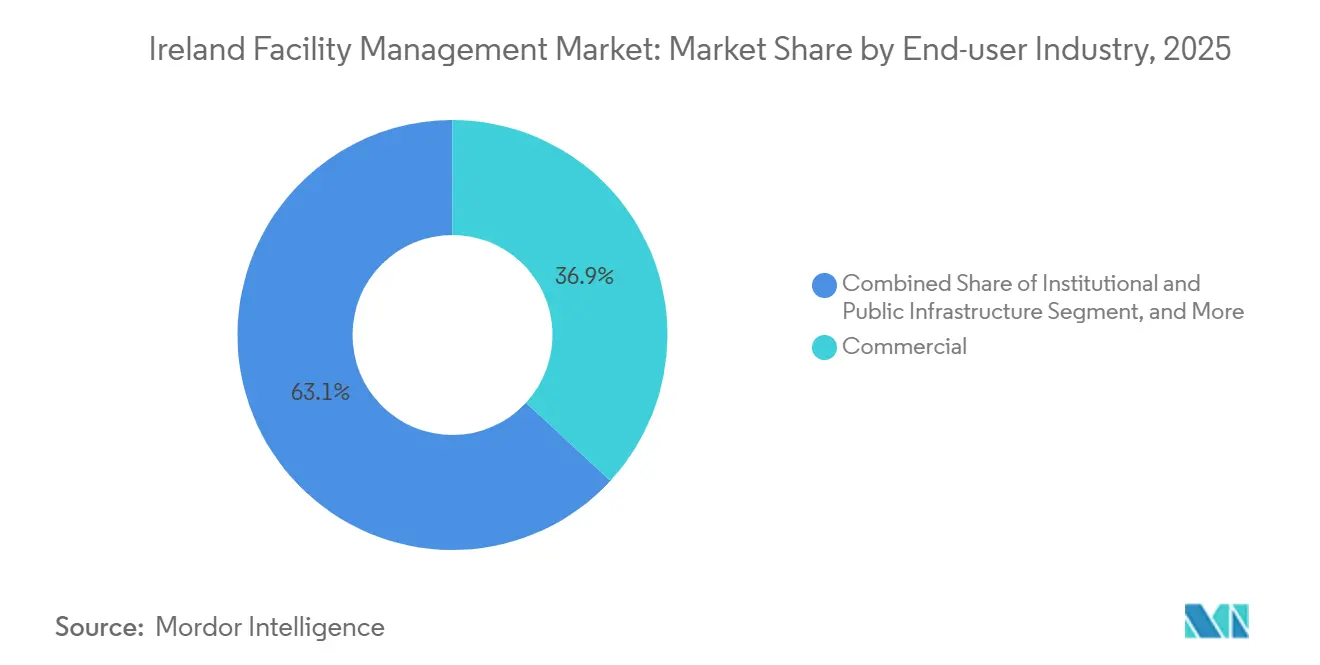

- By end-user industry, commercial real estate held 36.86% of the Ireland facility management market share in 2025, whereas institutional and public infrastructure is advancing at a 4.91% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization And Population Growth In Major Metros | +0.8% | National, Concentrated In Dublin, Cork, Galway, Limerick | Medium Term (2–4 Years) |

| Regulatory Drivers Specific To Labor And Safety Standards | +0.7% | National, Heightened Enforcement In Healthcare And Public Infrastructure | Long Term (≥ 4 Years) |

| Technology-Led Integrated FM (IoT, BMS, AI-Based Predictive Maintenance) | +1.1% | National, Early Adoption In Data-Center And Grade A Offices | Medium Term (2–4 Years) |

| ESG-Compliant FM Solutions Demand | +0.9% | National, Strongest In Commercial Real Estate And Institutional Sectors | Long Term (≥ 4 Years) |

| Edge Computing Adoption In Data-Center-Driven Asset Monitoring | +0.5% | Dublin, Kildare, Meath Corridors | Short Term (≤ 2 Years) |

| Public-Private Partnerships In Social Housing Facilities | +0.6% | National, Pilot Projects In Dublin, Cork, Galway | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Technology-Led Integrated FM (IoT, BMS, AI-Based Predictive Maintenance)

IoT sensors embedded in HVAC equipment, elevators, and lighting arrays stream operational data to cloud dashboards, allowing facility teams to replace reactive repairs with predictive maintenance that cuts downtime by up to 30%.[1]Siemens Ireland, “Building Automation Solutions,” siemens.com Data-center operators, consuming 21% of national electricity in 2023, have been first movers in deploying AI algorithms that optimize chiller loads and avert thermal hotspots. Grade A landlords in Dublin’s docklands now integrate occupancy and air-quality sensing to justify 15% rental premiums above non-certified stock. Retrofitting legacy Georgian or Victorian structures costs EUR 50-80 per m² (USD 55-88) because wiring has to be concealed without altering heritage fabric. Scaling remains constrained by the nation’s limited pool of roughly 1,200 BMS-literate technicians, intensifying competition for analytic talent.

Urbanization and Population Growth in Major Metros

Ireland’s population reached 5.28 million in April 2024 and is rising 2.2% annually, with net migration clustering in Dublin, Cork, and Galway. Office vacancy in Dublin fell to 11.8% in Q3 2024, prompting landlords to refurbish older buildings and secure WELL certifications that bundle HVAC, cleaning, and security into integrated contracts. The Housing for All program targets 33,000 social homes a year, creating a pipeline of long-term maintenance concessions. Skilled trades wages climbed 12% year on year by mid-2025, delaying project completions and deferring FM revenue recognition.[2]Construction Industry Federation, “Building Wage Index 2025,” cif.ie Concentrated urban growth also forces regional operators to raise pay offers, eroding their cost advantage.

Regulatory Drivers Specific to Labor and Safety Standards

The Energy Performance of Buildings Directive obliges all new Irish buildings to achieve near-zero energy performance by 2030, so owners are installing advanced BMS platforms that shift HVAC contracts from one-off servicing to multiyear managed agreements.[3]Sustainable Energy Authority of Ireland, “Building Energy Rating,” seai.ie Carbon-tax escalation from EUR 48.50 (USD 57.6) in 2024 to EUR 100 (USD 119) by 2030 underpins demand for energy-auditing FM specialists. Stricter liability under the Workplace Safety and Health Act, effective January 2025, is encouraging commercial landlords to consolidate vendors and centralize incident reporting . Quarterly fire-system inspections are now mandatory in buildings over 18 m, generating repeat revenue for certified hard-service providers. These layered mandates put smaller firms at a disadvantage because they lack compliance departments.

ESG-compliant FM solutions demand

Under the Corporate Sustainability Reporting Directive, 68% of multinational tenants require FM suppliers to disclose Scope 3 emissions, fueling demand for green cleaning chemicals and electric service fleets. The Climate Action Plan earmarks upgrades for 45,000 commercial buildings and 500,000 homes, creating a EUR 8 billion (USD 8.8 billion) retrofit opportunity.[4]Government of Ireland, “Housing for All Plan,” gov.ie Banks reinforce momentum; AIB offers 25-bp interest discounts to property owners that hire ISO 14001-certified FM providers. Price premiums of 8-12% are achievable on ESG-oriented contracts, yet verification gaps due to absent third-party registries risk client skepticism.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortage And Wage Inflation | -0.9% | National, Acute In Dublin, Cork, Galway | Short Term (≤ 2 Years) |

| Fragmented Legacy Building Stock Increasing Integration Complexity | -0.6% | Dublin, Cork, Limerick Historic Districts | Medium Term (2–4 Years) |

| Brexit-Induced Supply Chain Delays | -0.3% | National, Most Visible In MEP Component Imports | Short Term (≤ 2 Years) |

| Fixed-Price Contract Margin Compression | -0.2% | National, Concentrated In Soft Services | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage And Wage Inflation

National unemployment sat at 4.2% in December 2025, and net emigration of tradespeople is depleting the pool of HVAC technicians, electricians, and safety inspectors. Average facilities-sector wages leapt 5.8% year on year in Q3 2025, versus 3.2% economy-wide, squeezing providers locked into pre-2024 fixed-price contracts that assumed slower pay inflation. Some operators have absorbed margin declines of 200-300 bps and exited unprofitable accounts. Higher entry-level salary thresholds for non-EU work permits further hamper recruitment of cleaners and catering staff. Reduced inflows of UK-trained technicians post-Brexit lengthen mobilization lead times.

Fragmented Legacy Building Stock Increasing Integration Complexity

Dublin contains over 8,600 protected structures whose heritage status restricts invasive retrofits. Upgrading these properties to Building Energy Rating B2 costs EUR 200-350 per m² (USD 220-385), roughly double post-2000 buildings, because installers must preserve original fabric under conservation oversight. Narrow medieval street grids in Cork and Limerick curtail crane access, tripling labor costs when rooftop chillers need replacement. Absence of BIM data for pre-1990 assets forces manual asset mapping that can consume nine months before predictive maintenance platforms can even be deployed. Smaller FM firms, lacking working capital for elongated mobilizations, often avoid heritage portfolios, reinforcing consolidation momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard services commanded 59.19% of the Ireland facility management market share in 2025, reflecting sustained expenditure on MEP upkeep, HVAC optimization, and fire-safety compliance, particularly across an office stock where 60% predates 2005. As landlords install sensors on boilers, chillers, and electrical panels, contracts are shifting toward condition-based models that pay for avoided downtime rather than labor hours. Quarterly fire-system inspections required under revised Technical Guidance Document B cement predictable revenue for firms with certified technicians. Energy-efficiency retrofits tied to the near-zero mandate are bundled with multi-year maintenance guarantees, deepening wallet share for integrators capable of financing upgrades and operating IoT platforms.

Soft services deliver a smaller baseline yet are projected to outpace hard services at a 4.86% CAGR through 2031 as hospitals and landlords consolidate cleaning, catering, and security under single vendors. Dublin’s docklands recorded a 22% uptick in security contracts during 2025 as employers re-open offices and enforce access-control protocols. Outcome-based cleaning that ties payment to hygiene audit scores is now standard in healthcare, supported by real-time ATP testing and UV-C tracking. Catering operators offset 4.1% food-cost inflation by migrating to central production kitchens that trim per-meal labor up to 25%. Hybrid work patterns drive demand for on-site concierge and employee-experience services, positioning premium soft-service providers to cross-sell digital visitor-management tools.

By Offering Type: Outsourcing Dominates As Clients Seek Risk Transfer

Outsourced delivery claimed 67.68% of the Ireland facility management market size in 2025, expanding as organizations convert fixed internal labor into variable-fee contracts that migrate operational risk to specialists. The Ireland facility management market size for integrated facility management (IFM) is scaling fastest, as demonstrated by EirGrid’s EUR 27.1 million (USD 29.8 million) award that folds hard and soft services into a single life-cycle responsibility. Bundled FM appeals to mid-cap landlords that want purchasing leverage while retaining visibility over individual work streams.

Single-service outsourcing persists where highly specialized expertise is needed, such as data-center thermal management or GMP-compliant cleanrooms. In-house FM, at 32.32% in 2025, remains common among hospitals and universities that prize institutional knowledge, yet expenditure ceilings capping public-sector growth at 5% per year are nudging agencies toward hybrid sourcing models. The April 2024 merger of Neylons and Apleona, creating a 2,700-person national platform, illustrates how scale is becoming mandatory to compete for multi-site IFM concessions.

By End-User Industry: Institutional Segment Outpaces Commercial Growth

Commercial real estate retained 36.86% of the Ireland facility management market share in 2025 as technology and finance multinationals expanded footprints in Dublin, Cork, and Galway. Tenants insist on WELL certifications and carbon neutrality, pushing landlords to embed integrated FM scopes that marry HVAC, cleaning, and ESG reporting. Nonetheless, the institutional and public-infrastructure segment is forecast to climb at a 4.91% CAGR through 2031 on the back of the EUR 165 billion (USD 181.5 billion) National Development Plan that funds hospitals, schools, and transport hubs.

Healthcare clients prioritize infection-control cleaning, waste segregation, and air-quality audits; ABM’s EUR 10 million (USD 10.6 million) Galway hospital contract exemplifies willingness to pay premiums for certified providers. Public-private DBFM concessions lock in annuity-like revenue over 25 years, attractive to investors seeking stable cash flows. Hospitality demand is rebounding with Dublin hotel occupancy at 82% during 2025, yet seasonality and tourism volatility temper long-term contract appeal. Pharmaceutical clusters in Cork and Limerick require GMP-validated cleanroom and calibration services that can price 40-60% above standard FM but necessitate highly specialized teams.

Geography Analysis

The Ireland facility management market is centered in the Greater Dublin Area, which generated about 48% of national demand in 2025. With 3.2 million m² of Grade A and B offices, landlords sign multi-year IFM deals bundling HVAC, cleaning, security, and energy optimization, supported by vacancy falling to 11.8% during Q3 2024. Dublin’s data-center corridor hosts 82 active sites that draw premium FM spending on cooling, backup power, and 24-hour monitoring. Yet a 4.0% local unemployment rate forces providers to pay technicians 12-18% wage premiums over regional averages, squeezing older fixed-price agreements.

Cork is the second growth pole, thanks to pharmaceutical plants run by Pfizer, Johnson and Johnson, and Eli Lilly that demand GMP-grade HVAC validation, cleanroom upkeep, and calibration. Retrofits of its 650,000 m² commercial stock to EPC B2 ratings spur contracts for insulation, LED, and BMS upgrades. Galway and Limerick benefit from hospital and university expansions tied to the National Development Plan. The new National Paediatric Hospital in Dublin, due 2027, sets the template for 25-year FM concessions across regional health facilities.

Outside the main metros, dispersed property portfolios and limited pools of certified technicians hinder economies of scale. Heritage restrictions in rural towns often necessitate manual surveys and reversible installations that elongate mobilizations. Smaller local contractors retain share where relationships outweigh cost, complicating expansion plans for national integrators. The Ireland facility management industry thus exhibits a two-tier geography: scale-intensive urban hubs dominated by multinational providers and fragmented regional markets serviced by niche specialists.

Competitive Landscape

The top five providers, Noonan Services, Apleona Ireland, Mitie Group, OCS Group, and Sodexo, held roughly 42% of the Ireland facility management market in 2025, indicating moderate fragmentation. Noonan, with 15,000 staff and GBP 350 million (USD 395 million) turnover, remains the soft-service leader through longstanding public-sector ties. Apleona vaulted into first place after acquiring Neylons in April 2024, creating a 2,700-employee platform approaching EUR 180 million (USD 198 million) revenue that can underwrite data-analytics investments.

Multinationals such as Mitie and Sodexo leverage global purchasing to undercut pricing on commodity services, but they struggle in heritage building maintenance where local regulatory knowledge is prized. Outcome-based contracts, exemplified by EirGrid’s 98% asset-availability clause, favor operators with predictive maintenance capabilities and robust balance sheets. Early technology adopters deploy IoT sensors, AI fault detection, and mobile workforce apps to shrink response times, but the scarcity of analytics-savvy technicians forces many to partner with software firms or pursue targeted acquisitions.

Regional specialists carve niches in data-center cooling, pharmaceutical cleanrooms, and conservation-grade refurbishments, segments protected by certification hurdles that insulate margins from commoditization. Consolidation is likely to accelerate as scale becomes prerequisite for national tenders bundling multi-site hard and soft scopes. Wage inflation and compliance complexity continue to pressure smaller operators, sharpening the divide between full-service integrators and local specialists.

Ireland Facility Management Industry Leaders

CBRE Group Inc

Sodexo Group

Kier Group PLC

Sensori Facilities Management

Cushman & Wakefield PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ABM Industries secured a EUR 10 million (USD 10.6 million) cleaning contract with the Health Service Executive covering Galway hospitals, emphasizing infection-control protocols and real-time hygiene monitoring.

- April 2025: Gas Networks Ireland issued a EUR 15 million (USD 16.5 million) tender for integrated facility management across its national gas infrastructure for five years.

- February 2025: Mitie Group opened a regional hard-services hub in Cork, creating 120 jobs focused on MEP, fire safety, and energy management.

- January 2025: OCS Group launched a carbon-neutral initiative pledging fleet electrification and green cleaning chemicals by 2030.

Ireland Facility Management Market Report Scope

By integrating people, place, process, and technology, facility management confines multiple disciplines to ensure any building's functionality, comfort, safety, and efficiency. At the same time, complex services include physical and structural services like fire alarm systems, lifts, etc. Soft services include cleaning, landscaping, security, and similar human-sourced services, providing solutions to end-user industries. The Ireland facility management market is defined based on the revenues generated from the services used in various end-user applications nationwide. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from the various types used in various end-user industries across Ireland. In addition, the study provides the Ireland facility management market trends, along with key vendor profiles.

The Ireland Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-House | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-House | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large will facilities outsourcing become in Ireland by 2031?

Outsourced contracts are projected to reach USD 2.71 billion by 2031, expanding at a 4.64% CAGR as organizations shift fixed internal costs to variable fee arrangements.

Which service category is expanding most quickly?

Soft services such as cleaning, catering, and security are forecast to grow at a 4.86% CAGR through 2031 on rising demand for bundled, outcome-based contracts.

Why are institutional buildings driving future growth?

Public investment under the EUR 165 billion National Development Plan funds hospitals, schools, and transport hubs that embed long-duration FM concessions, pushing institutional demand at a 4.91% CAGR.

What role does technology play in competitive differentiation?

Providers deploying IoT sensors and AI-based predictive maintenance cut equipment downtime up to 30%, satisfy outcome-based clauses, and win premium contracts.

How are labor shortages affecting providers?

Wage inflation of 5.8% and reduced technician availability compress margins on fixed-price deals, forcing smaller firms to exit unprofitable accounts or seek acquisition partners.

Which regions outside Dublin hold growth potential?

Cork's pharmaceutical corridor and planned hospital expansions in Galway and Limerick are generating demand for GMP-grade and clinical facilities services despite a smaller overall base.

Page last updated on: