Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

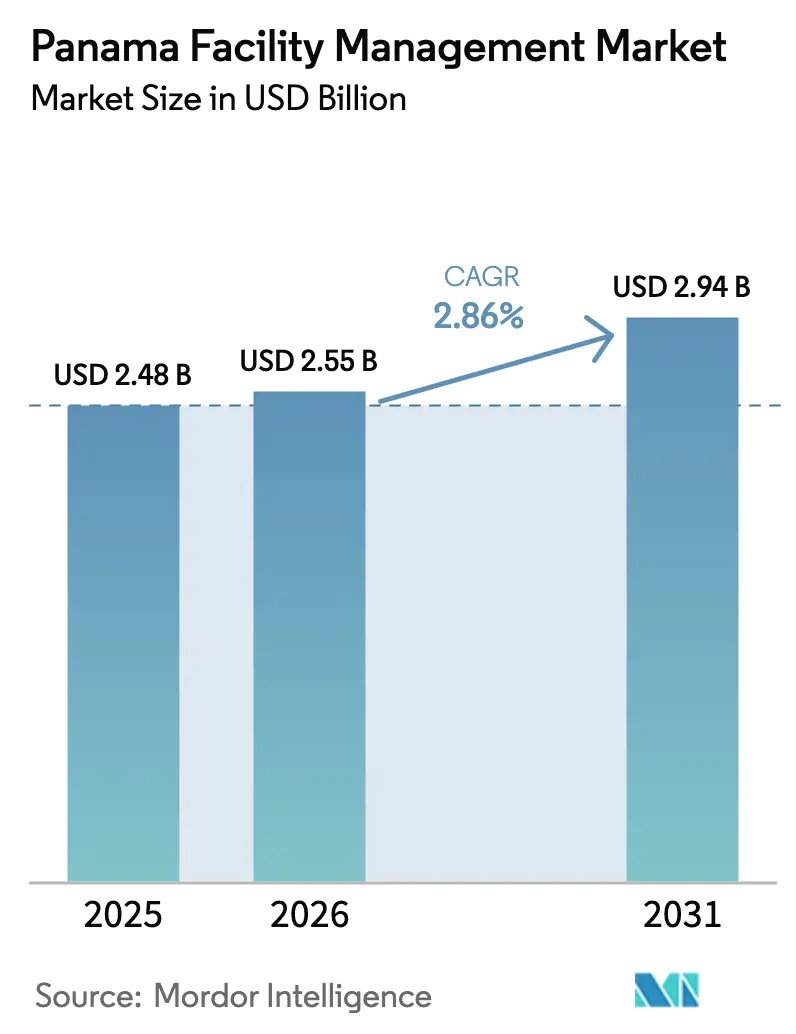

| Base Year Market Size (2025) | USD 2.48 Billion |

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 2.86% CAGR |

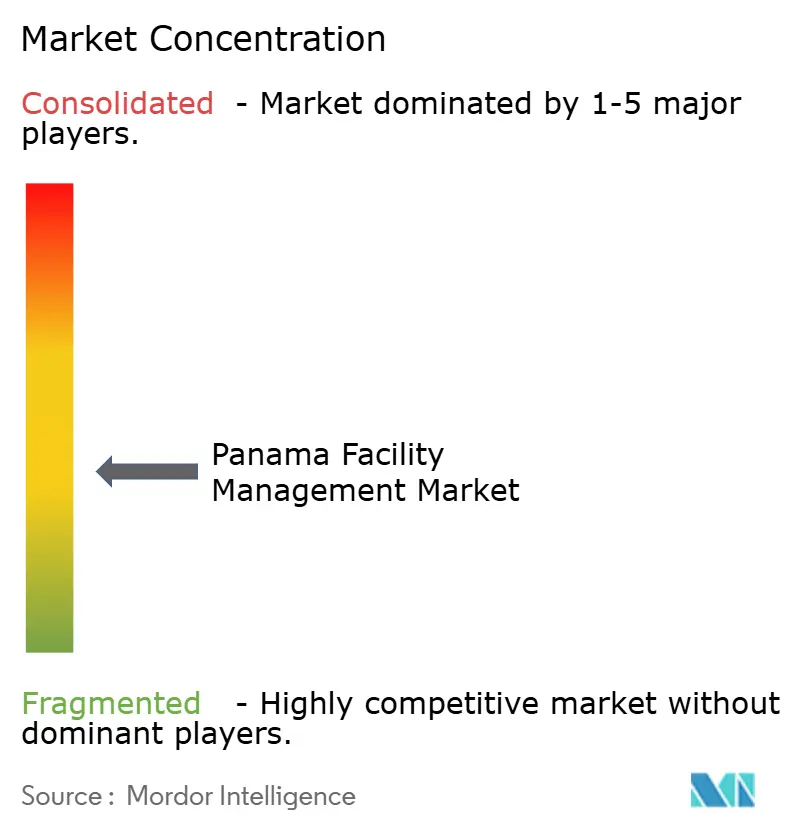

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Panama Facility Management Market Analysis by Mordor Intelligence

The Panama facility management market size is expected to grow from USD 2.48 billion in 2025 to USD 2.55 billion in 2026 and is forecast to reach USD 2.94 billion by 2031 at 2.86% CAGR over 2026-2031. Expansion is linked to the country’s role as a logistics and financial hub, the Panama Canal’s water-security investments, and steady demand for integrated services across commercial, institutional, and infrastructure portfolios. Hard services continue to dominate value creation, yet technology-enabled soft services are winning greater budget share as occupiers emphasize employee experience. Outsourcing momentum is accelerating because organizations want predictable costs, guaranteed outcomes, and access to advanced building-management technology. Competitive intensity is rising as global players deploy IoT and AI tools that deliver measurable performance gains, while mid-sized local providers leverage on-the-ground relationships to protect key accounts. Near-term growth depends on skilled-labor availability, regulatory clarity for foreign providers, and resilience measures that mitigate climate-related disruptions across Canal Zone assets.

Key Report Takeaways

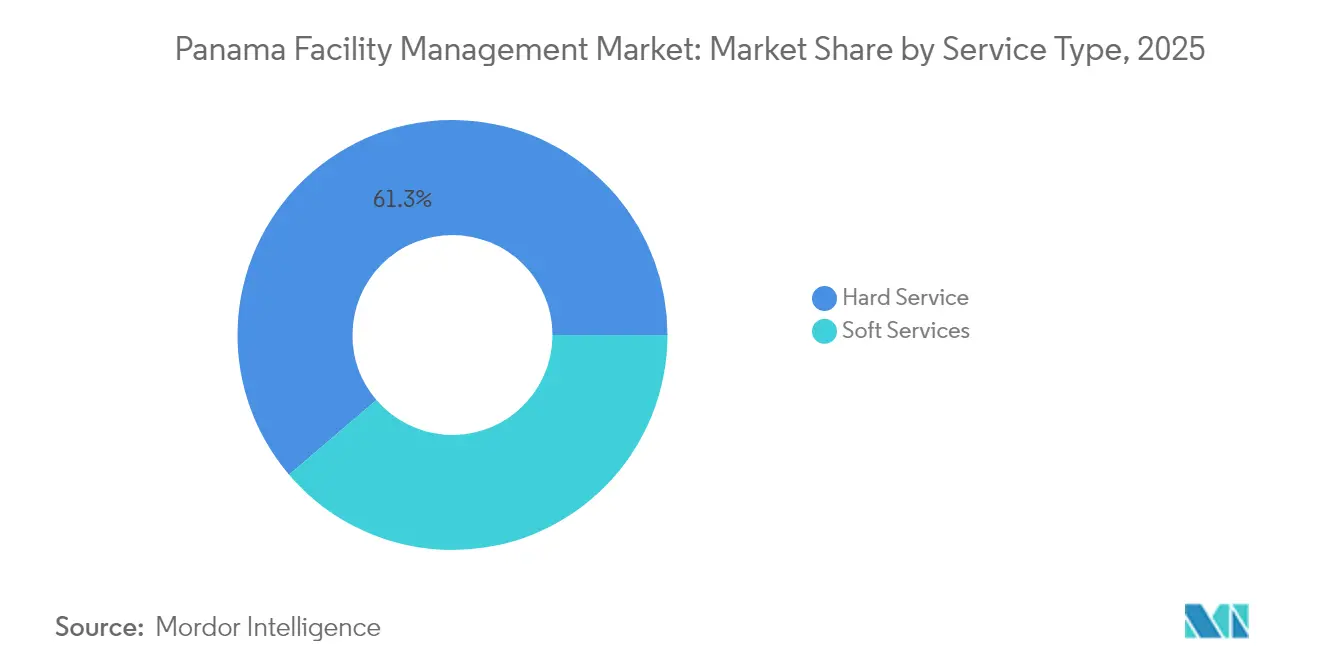

- By service type, hard services led with 61.25% of the Panama facility management market share in 2025, while soft services are advancing at a 3.7% CAGR through 2031.

- By offering type, in-house solutions commanded 58.05% of the Panama facility management market size in 2025, whereas outsourced services are increasing at a 3.92% CAGR through 2031.

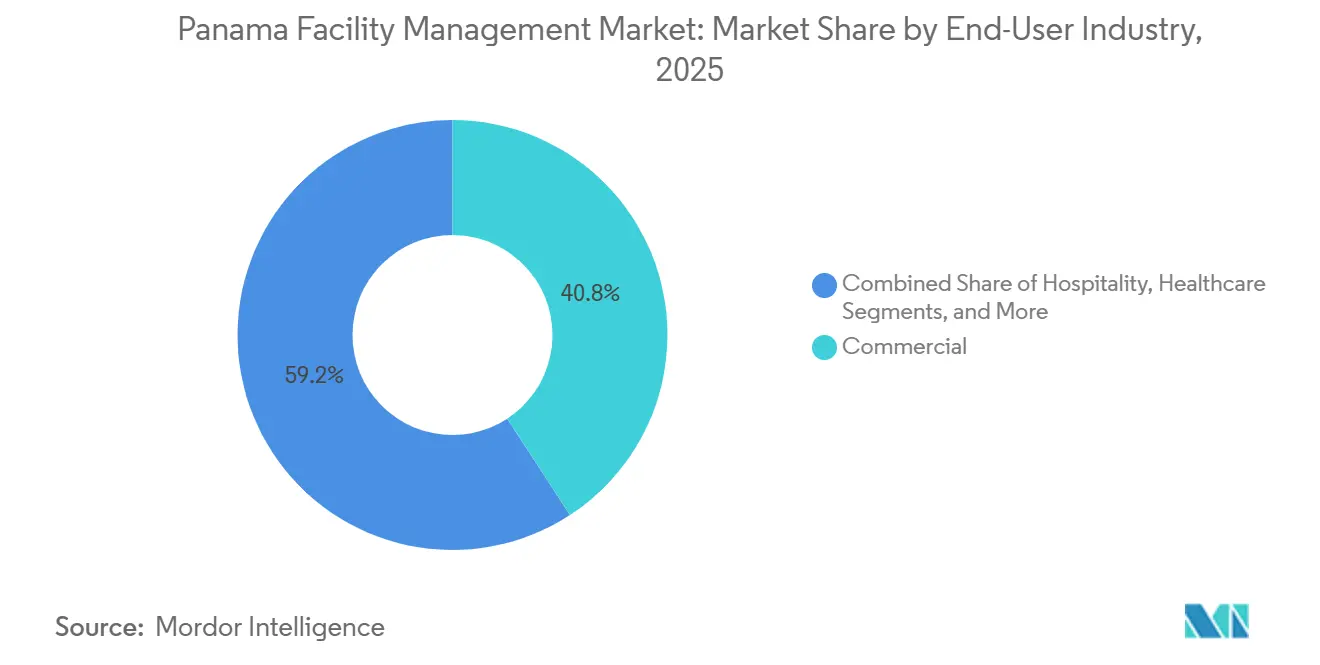

- By end-user industry, commercial facilities accounted for 40.80% share of the Panama facility management market size in 2025, while institutional and public-infrastructure facilities are growing at a 5.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Panama Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid commercial real estate expansion | +0.8% | Panama City, Colon Free Zone | Medium term (2-4 years) |

| Technology integration (IoT, AI, automation) | +0.6% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Increasing outsourcing trend | +0.5% | National, early gains in Panama City | Short term (≤ 2 years) |

| Rising focus on workplace experience | +0.4% | Commercial districts, multinational offices | Medium term (2-4 years) |

| Government infrastructure stimulus | +0.7% | Canal Zone, Colon, David corridor | Long term (≥ 4 years) |

| Surging demand for ESG-compliant FM | +0.3% | Panama City, international business zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Commercial Real Estate Expansion

More than 400,104 m² of prime office space is under construction and USD 160 million of shopping-mall projects are progressing, extending beyond traditional business districts into mixed-use zones. Developers now embed facility-management specifications early in design to maximize operating efficiency and tenant comfort, a shift that favors providers offering integrated hard-and-soft service bundles. The USD 345 million Panama Pacífico program demonstrates geographic diversification that requires multi-site management capability. Class A rent compression from USD 24.41 to USD 23.29 per m² underscores the new performance-over-location mindset, driving adoption of data-driven FM contracts that guarantee cost and energy outcomes.

Technology Integration (IoT, AI, Automation)

IoT sensors, AI analytics, and automated controls are moving operations from reactive to predictive. Johnson Controls reports up to 30% energy savings and 20% maintenance-cost reduction after deploying its OpenBlue platform across commercial portfolios. [1]Johnson Controls, “OpenBlue Expands Use of AI and Autonomous Building Controls,” johnsoncontrols.comLEED-driven demand for smart building systems is growing as firms pursue sustainability metrics endorsed by the Panama Green Building Council. Humid tropical conditions amplify HVAC efficiency benefits, and real-time monitoring lets managers pre-empt failures, protect indoor air quality, and extend asset life. Providers that package analytics dashboards, automated work-order flows, and outcome-based SLAs are outpacing labor-intensive rivals.

Increasing Outsourcing Trend

Multinationals in finance, logistics, and technology sectors are transitioning from self-delivery to vendor-managed models. CBRE posted 16% facilities-management revenue growth in Q1 2025, attributing bookings to clients seeking end-to-end solutions. Sodexo’s acquisition pipeline and CRH Catering deal highlight appetite for bundled services that cut management complexity. Outsourcing converts fixed overhead into variable spend while giving occupiers access to scarce technical skills. Early adopters favor single-service contracts for cleaning or HVAC, but demand is rapidly shifting toward integrated FM agreements with performance guarantees.

Rising Focus on Workplace Experience and Employee Well-Being

Hybrid work patterns give occupiers leverage to differentiate through healthy, flexible environments. Advanced air-quality sensors, biophilic design elements, and circadian lighting are becoming standard expectations, particularly among multinational tenants competing for qualified talent. Johnson Controls’ personalized climate systems illustrate the pivot toward occupant-centric services. Providers that quantify wellness metrics such as reduced absenteeism and higher space utilization—command premium fees and long-term renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and skill gaps | -0.7% | National, acute in technical roles | Short term (≤ 2 years) |

| Margin pressure from rising operational costs | -0.5% | National, concentrated in cities | Medium term (2-4 years) |

| Regulatory complexity for foreign FM providers | -0.3% | National, affects international ops | Long term (≥ 4 years) |

| Climate-driven disruptions increasing liability | -0.4% | Canal Zone, coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Skill Gaps

World Bank data show only 20% of low-income youth reach tertiary education, leaving a limited pool of trained technicians. [2]World Bank Group, “Panama Must Improve the Quality of Jobs and Strengthen Human Capital,” worldbank.orgEmployers struggle to hire HVAC programmers, BAS integrators, and compliance specialists; many switch to higher-paying construction roles or emigrate. Providers raise wages and invest in up-skilling, which erodes margins and slows geographic rollout of advanced services.

Margin Pressure from Rising Operational Costs

Import tariffs and global material shortages escalate prices for replacement parts and consumables. [3]Habitaro, “Aranceles y Materiales de Construcción: Cómo Afecta su Precio en 2025,” habitaro.comEnergy tariffs rise alongside economic growth, challenging providers that guarantee utility savings. Canal-zone labor disputes illustrate how wage negotiations can escalate quickly. Higher insurance premiums tied to extreme-weather risk add further cost layers, pushing smaller vendors out of large-scale bids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Value Creation While Soft Services Accelerate

Hard services generated 61.25% of the Panama facility management market size in 2025, led by MEP and HVAC regimes essential for port, rail, and commercial facilities. Specialized engineering support for the USD 1.6 billion reservoir project and Canal hydraulics keeps demand high. Asset-intensive environments prioritize preventive and predictive approaches to extend equipment life, and clients often lock providers into multi-year agreements to safeguard uptime.

Soft services are growing at a 3.7% CAGR as occupiers seek enhanced employee experience, security, and hygiene. Multinationals adopt smart-cleaning schedules based on occupancy sensors, while security contracts include analytics-enabled surveillance. Healthcare operators embrace UV-robot disinfection partnerships to meet stringent protocols. The trend suggests that the Panama facility management market will transition toward balanced hard-and-soft portfolios that blend technical resilience with occupant well-being.

By Offering Type: Outsourcing Gains Ground Amid In-House Control

In-house teams retained 58.05% of Panama facility management market share in 2025, a reflection of the public sector’s preference for direct oversight of sensitive infrastructure. Ministries and Canal authorities keep strategic decision-making internal while contracting niche tasks to specialists. Cost-containment limits large-scale headcount increases, opening the door for hybrid models.

Outsourced solutions are forecast to grow 3.92% annually as corporates convert fixed costs to flexible service lines. Single-service packages for janitorial, HVAC, or landscaping act as stepping-stones toward bundled and integrated offerings. The Panama facility management market size tied to integrated outsourcing is expanding fastest, aided by CBRE’s and Sodexo’s outcome-based contracts that guarantee energy and maintenance KPIs. Providers that present transparent dashboards and continuous-improvement roadmaps win competitive tenders.

By End-User Industry: Institutional Momentum Surpasses Commercial Stability

Commercial occupiers maintained 40.80% of the Panama facility management market size in 2025. Finance, IT, and telecom segments require high-availability environments and tight regulatory compliance, supporting sustained contract renewals. Retail and warehouse premises benefit from the 15.1% jump in container throughput, but office downsizing from hybrid work moderates overall growth.

Institutional and public-infrastructure facilities are pacing at a 5.75% CAGR through 2031. Government modernization, transport connectivity, and education-campus expansion at Ciudad del Saber underpin robust pipeline opportunities. Rail, port, and reservoir works spawn long-horizon FM contracts that reward specialized certifications in water, environmental, and safety management. As these assets move from construction to operations, demand shifts toward lifecycle services that merge engineering with ESG stewardship.

Geography Analysis

Facility-management demand is densest in the Canal Zone and Panama City, where critical logistics assets and 400,104 m² of new offices converge. Continuous Canal expansion and the Rio Indio water-security initiative require specialized hard services, environmental monitoring, and resilience planning. Multinational headquarters and government agencies cluster in the capital, driving integrated contracts that combine technology, security, and wellness programs.

Colon Free Zone and Pacific-coast corridors are emerging growth poles. Port volumes reached 9.57 million TEU in 2024, spurring demand for logistics-oriented facility solutions, from yard-equipment maintenance to temperature-controlled storage. The USD 23 billion port-portfolio acquisition by a BlackRock-led consortium unlocks opportunities for providers capable of standardizing FM practices across multiple terminals. Mixed-use projects at Panama Pacífico extend demand into residential and light-industrial segments.

Interior regions such as David and Chiriquí province are poised to gain from the David–Panama railway and agricultural-modernization programs. Though the local workforce is smaller, government incentives and decentralization objectives attract service providers willing to train local technicians. Early contracts focus on station facilities, track maintenance depots, and supporting commercial developments, setting the stage for gradual sophistication of regional FM requirements.

Competitive Landscape

The Panama facility management market hosts a mix of global integrators and home-grown specialists competing across service tiers and sectors. CBRE, Sodexo, and Johnson Controls expand through acquisitions and digital platforms, delivering bundled hard-and-soft services with performance guarantees. CBRE’s combination with Turner and Townsend added project-management and green-energy depth, further differentiating its value proposition. Johnson Controls’ OpenBlue ecosystem offers AI-driven insights that cut chiller costs by 67% and boost ROI to 155% within three years.

Local players such as Grupo Melo Servicios Generales and Mantenimiento y Aseo S.A. leverage regulatory know-how, cultural affinity, and established municipal relationships to anchor public-sector and retail accounts. Their agile structures support quick deployment in secondary cities, yet limited capital constrains large-scale technology upgrades. Partnerships with equipment vendors or niche software startups provide pathways to remain competitive.

Emerging disruptors focus on narrow domains such as energy management dashboards, drone-based façade inspections, or remote-monitoring centers. They collaborate with incumbents to fill capability gaps rather than pursue full-service models. Overall, bargaining power is shifting toward clients who demand transparent data and outcome-based fees, prompting providers to invest in IoT infrastructure, workforce up-skilling, and integrated command centers.

Panama Facility Management Industry Leaders

Ecolab Inc.

Grupo EULEN

Sodexo Inc.

Hines Group

CBRE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Panama starts construction of the 475 km Panama City–Paso Canoas railway, opening 14 stations and substantial FM opportunities across depots and passenger hubs.

- May 2025: Completion of the Panama–David route design advances the USD 8 million high-speed project, expanding facility-service prospects in western provinces.

- April 2025: Johnson Controls publishes study showing 155% ROI from OpenBlue deployments, citing 10% energy cuts and 67% chiller-maintenance savings over 50 million ft².

- April 2025: APM Terminals acquires Panama Canal Railway Company, integrating rail and port operations for smoother cargo flow.

Panama Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through its responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The market for integrated facility management service (IFM), along with single and bundled services, is included in the outsourced FM services segment.

The Panama facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size and forecast growth of the Panama facility management market?

The market is valued at USD 2.55 billion in 2026 and is projected to reach USD 2.94 billion by 2031, reflecting a 2.86% CAGR.

Which service type dominates the industry today?

Hard services dominate with 61.25% market share, driven by the country’s infrastructure-heavy logistics and Canal operations.

Why are outsourced facility management services gaining traction in Panama?

Organizations want to refocus on core activities, access specialized skills, and secure outcome-based contracts, prompting outsourced services to expand at a 3.92% CAGR.

Which end-user segment is expected to grow fastest through 2031?

Institutional and public-infrastructure facilities lead with a 5.75% CAGR, fueled by government modernization, railway construction, and water-security projects.

How is technology reshaping facility management practices?

IoT sensors, AI analytics, and smart-building platforms such as Johnson Controls’ OpenBlue deliver up to 30% energy savings and 20% lower maintenance costs, making data-driven services a competitive necessity.

What key challenges could restrain market growth?

Acute skilled-labor shortages, rising operational costs, complex regulations for foreign providers, and climate-driven disruptions across Canal Zone assets all exert downward pressure on margins and service continuity.

Page last updated on: