Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

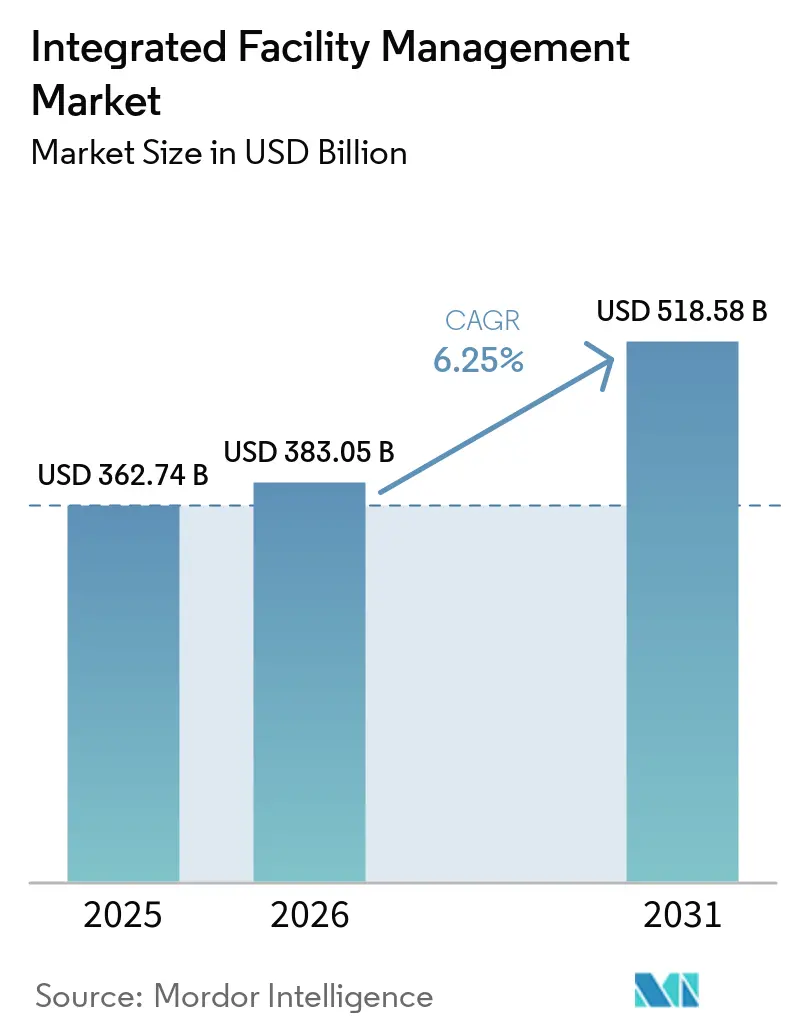

| Market Size (2026) | USD 383.05 Billion |

| Market Size (2031) | USD 518.58 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integrated Facility Management Market Analysis by Mordor Intelligence

The Integrated Facility Management Market size was valued at USD 362.74 billion in 2025 and is estimated to grow from USD 383.05 billion in 2026 to reach USD 518.58 billion by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

The market is shifting away from fragmented vendor structures toward single-accountability models that combine hard and soft services on technology-enabled operating platforms. Demand in the integrated facility management market is supported by deeper outsourcing cycles in North America and Europe, rapid real estate and infrastructure expansion in Asia-Pacific, and building-performance rules that place direct financial pressure on disconnected operations. Long-tenure contracts continue to support the integrated facility management (IFM) market because they create recurring revenue and more stable cash flows than one-time advisory work. Competition in the integrated facility management market is rising as large operators invest in predictive maintenance tools, performance-linked delivery models, and technical capabilities for data centers and life sciences sites. Near-term expansion in the IFM market still faces pressure from skilled labour shortages, cyber liability around connected buildings, and equipment cost volatility that can delay mobilization and weaken margins.

Key Report Takeaways

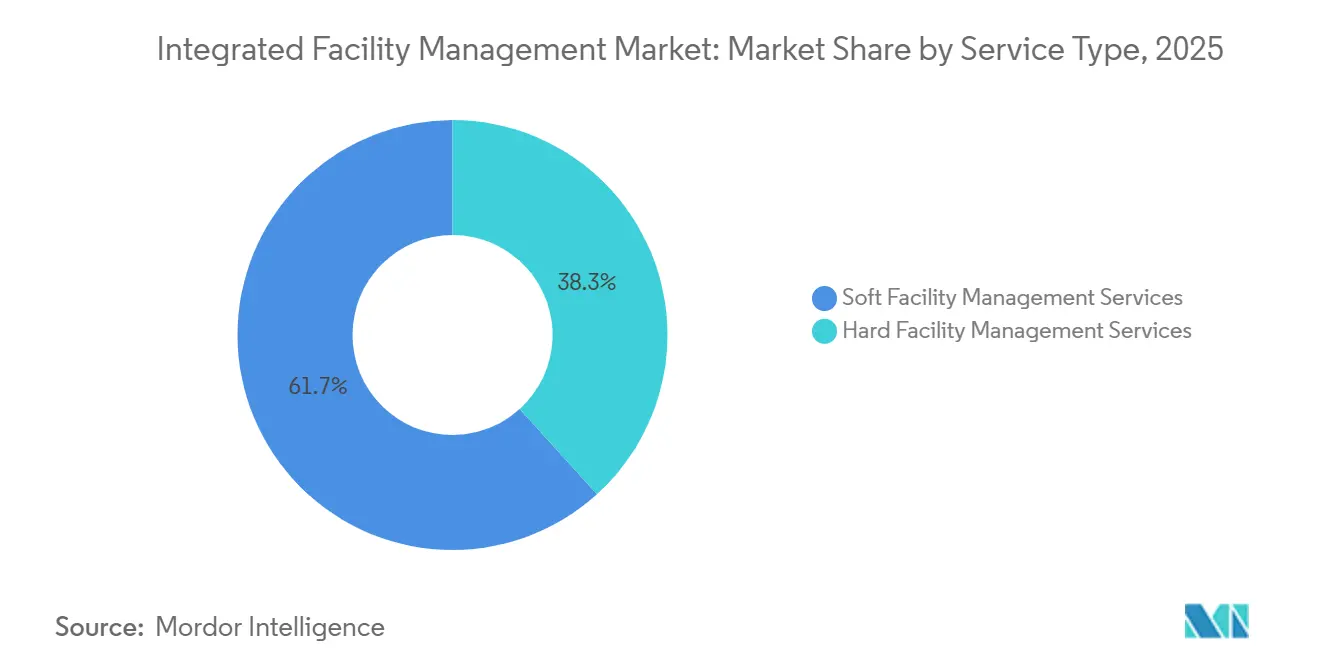

- By service type, soft facility management accounted for 61.73% of revenue share in the integrated facility management market in 2025, while the hard facility management market is projected to expand at a 6.83% CAGR through 2031.

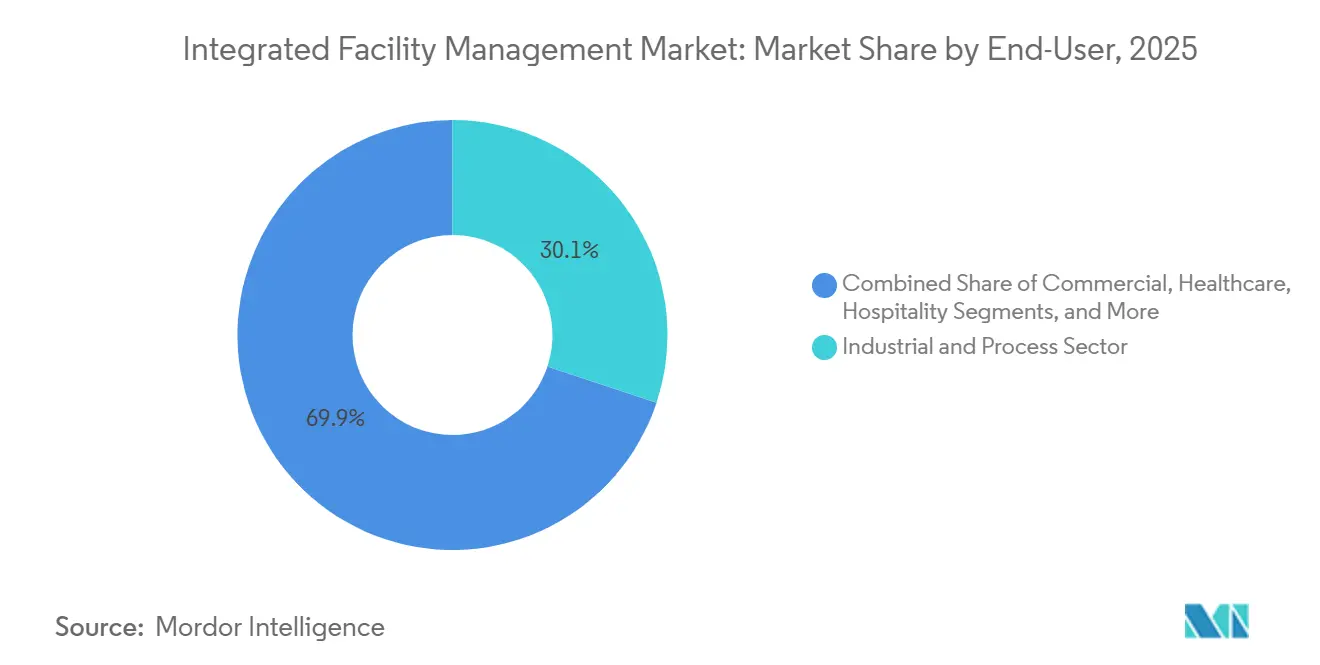

- By end user, the industrial and process sector segment accounted for 30.11% of revenue in the integrated facility management (IFM) market in 2025, while the commercial segment is projected to grow at 7.59% CAGR through 2031.

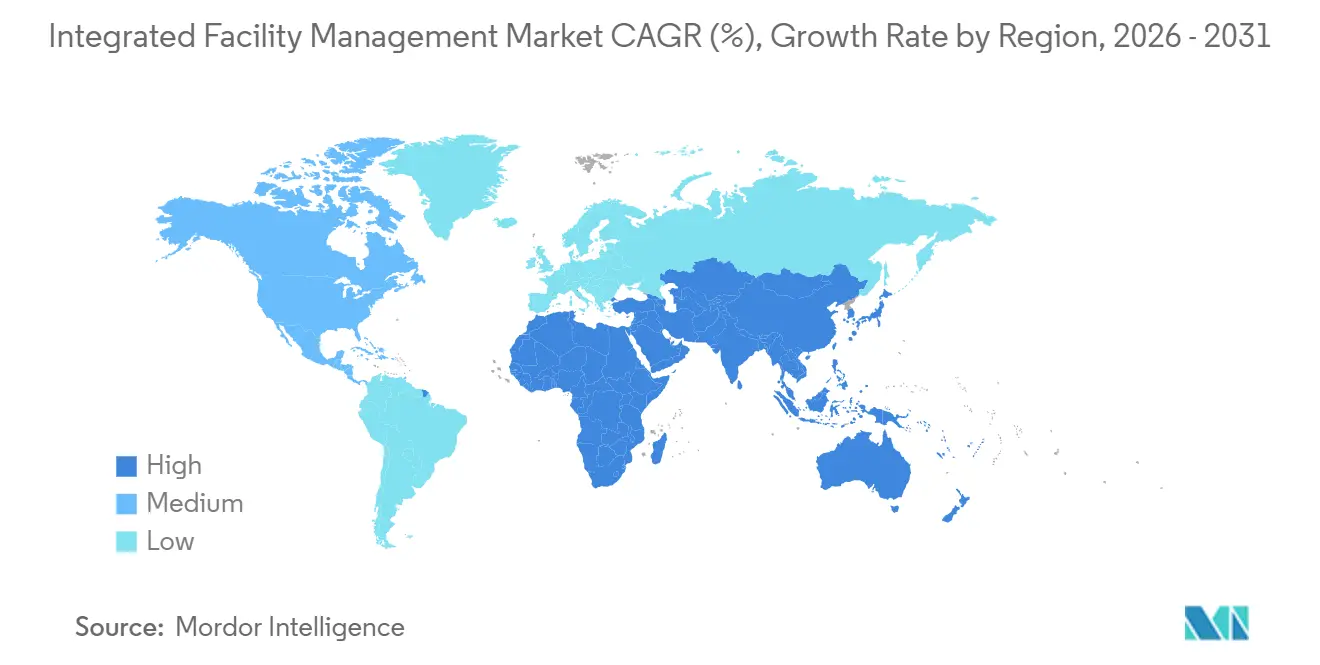

- By geography, Asia-Pacific accounted for 40.76% of the total IFM market revenue in 2025 and is projected to expand at 7.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Building and Predictive Maintenance Adoption | +1.5% | Global, strongest concentration in North America, APAC, and Germany | Short term (≤ 2 years) |

| Outsourcing Of Non-Core Workplace and Estate Operations | +1.3% | Global, most pronounced in North America and Western Europe | Medium term (2-4 years) |

| ESG And Building-Performance Compliance Mandates | +1.0% | North America and EU core, spill-over to APAC and MEA | Medium term (2-4 years) |

| Data Center and Life Sciences Capacity Expansion | +0.7% | North America, Western Europe, APAC, Singapore, India | Short term (≤ 2 years) |

| Demand For Single Accountability Across Multi-site Portfolios | +0.5% | Global, strongest in APAC and Europe | Long term (≥ 4 years) |

| Outcome-based FM Contracts Linked to Carbon and Uptime KPIs | +0.3% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart Building and Predictive Maintenance Adoption: AI Now Sets the Procurement Floor

AI-enabled monitoring and IoT building systems are changing how integrated facility management is procured and delivered. Uptime and energy performance are now moving from service aspirations into contract obligations in large enterprise accounts. Honeywell reported in April 2025 that 60% of organizations had integrated AI-driven maintenance systems, while 84% of commercial building decision-makers planned to expand AI further.[1]Honeywell, “AI In Building Maintenance Study,” Honeywell, honeywell.com CBRE reported 13% growth in its facility management segment in 2025, supported by data center technical services and local FM deployments linked to smart infrastructure programs.[2]CBRE Group, “Annual Results 2025,” CBRE, cbre.com Providers with long-tenure contracts are building asset-level performance baselines that new entrants cannot easily match, which raises switching costs for clients. Siemens expanded this shift in May 2026, launching Asset Performance Advanced, a managed building service that combines predictive failure classification with automated workflow execution for HVAC and building automation systems.[3]Siemens, “Siemens Global,” Siemens, siemens.com

Outsourcing Of Non-Core Workplace and Estate Operations: First-Time Outsourcers Expand the Addressable Market

The integrated facility management (IFM) market is gaining from a broader outsourcing cycle as building systems become harder for occupiers to manage in-house. Mechanical, electrical, air-quality, security, and control systems now require a level of coordination that many occupiers do not maintain internally. JLL reported 9% revenue growth in its Real Estate Management Services segment in the fourth quarter of 2025, supported by workplace management expansion and new client wins in sectors that had relied on self-operated FM models.[4]CBRE Group, “Annual Results 2025,” CBRE, cbre.com CBRE also extended its outsourcing platform through the USD 800 million acquisition of J&J Worldwide Services in February 2024, adding federal facilities with long-term fixed-price contracts and institutional-grade service requirements. Mid-market occupiers are adding fresh demand to the integrated facility management market as office footprints are redesigned around hybrid attendance patterns and service flexibility. IFMA reported in 2025 that leading organizations increasingly treat FM as a direct lever for financial, environmental, and workforce outcomes, which is moving procurement attention from operations teams to executive leadership.

ESG And Building-Performance Compliance Mandates: Penalties Are Driving Procurement Decisions

Compliance rules are strengthening demand in the integrated facility management market because they now attach direct financial consequences to building underperformance. New York City Local Law 97 imposes fines of USD 268 per metric ton of CO₂-equivalent emissions above building-specific caps, which pushes owners toward providers that can manage verified carbon performance at the portfolio level. California's Title 24 Building Energy Efficiency Standards, effective January 1, 2026, target USD 4.8 billion in cumulative energy cost savings and a 4 million metric ton reduction in greenhouse gas emissions. These rules make integrated contracts more attractive because unified delivery produces cleaner operating data than disconnected single-service arrangements. Buyers are also placing greater weight on verified energy-management capability when they screen vendors for large enterprise tenders. This is lifting the value of providers that can connect maintenance, energy reporting, and operational accountability in one service model.

Data Center and Life Sciences Capacity Expansion: Specialized FM Becomes a Barrier to Entry

The IFM market is also expanding through a technical niche tied to hyperscale data centers and life sciences facilities. These environments need continuous power redundancy, precise environmental control, and strict maintenance protocols that standard commercial contracts do not cover. CBRE said its data center solutions revenue approached USD 700 million in the third quarter of 2025 and projected the segment to reach USD 2 billion in 2026, with a 20% annual growth rate. ISS won a full integrated facilities services contract in January 2026 for a major life sciences and pharmaceutical customer in Switzerland, valued at nearly DKK 300 million (USD 43 million) annually across four locations. Farnek also reported AED 58 million (USD 15.8 million) in first-quarter 2026 contract wins, including total FM services for Equinix data centers in Dubai and Abu Dhabi. Tender barriers are rising in these verticals because providers without critical-systems engineers, cleanroom experience, and energy-management credentials are being screened out early.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Multi-Trade Technical Labor | -1.2% | Global, most acute in North America, United Kingdom, and Japan | Medium term (2-4 years) |

| Cybersecurity Liability from Connected Building Stacks | -0.7% | Global, highest exposure in North America, EU, and Middle East | Short term (≤ 2 years) |

| Margin Compression from Inflation Reset Lag in FM Contracts | -0.5% | North America and EU | Short term (≤ 2 years) |

| Tariff And Lead-time Volatility in HVAC And Controls Supply | -0.4% | North America, spill-over to APAC and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage Of Multi-Trade Technical Labor: Supply Gaps Are Becoming Strategic Risks

The integrated facility management (IFM) market is facing a structural labour problem rather than a short hiring cycle. Providers need more electricians, HVAC technicians, control specialists, and compliance staff than current training pipelines can supply. The SFG20 State of Facilities Management 2026 report found that 51% of FM organizations reported staff shortages and 42% reported a significant skills gap, especially in compliance, digital capability, and energy management. JLL projected 2.1 million unfilled skilled trades positions by 2030, with potential economic losses of USD 1 trillion per year if the gap persists. The U.S. Bureau of Labor Statistics projected HVAC technician employment to grow 8.1% and electrician roles to grow 9.5% through 2034, both above the 3.1% average for all occupations. This slows hard FM mobilization in the integrated facility management market while also pushing providers to invest more aggressively in remote diagnostics and predictive maintenance to reduce site-level labour dependence.

Cybersecurity Liability from Connected Building Stacks: OT-IT Convergence Introduces Systemic Risk

Cyber exposure is becoming a more visible restraint on the integrated facility management market as connected building systems expand across portfolios. Building management systems, HVAC controls, lighting networks, and access platforms are now tied more closely to enterprise IT environments than in earlier outsourcing models. Claroty reported in September 2025 that 45% of cybersecurity professionals ranked cyber-physical system risk as a primary concern, 73% of organizations were re-evaluating third-party remote access, and 46% had experienced breaches linked to third-party access during the prior 12 months. This risk is changing contract design because IT security teams are now directly involved in FM vendor approval and controls review. Compliance requirements tied to IEC 62443 and ISO 27001 are extending qualification timelines and raising delivery costs for smaller operators that do not maintain dedicated cyber teams. The result is a slower and more selective buying process in the IFM market, especially for large occupiers with complex building stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Growth Signals a Technical Service Premium

Soft facility management (FM) held 61.73% of the integrated facility management (IFM) market share in 2025. Its lead reflects the long-standing outsourcing of cleaning, security, catering, reception, and office support across commercial, institutional, and hospitality portfolios. These services are usually the first to move outside the client organization because they are easier to standardize across multiple sites. Office support and security continue to carry the largest weight within soft FM, while cleaning is moving through a technology upgrade cycle with greater use of robotic tools and occupancy-based scheduling. Compass Group reported FY2025 revenue of USD 46.1 billion and net new business growth of 4-5% for the fourth straight year, which supports the durability of institutional catering within the IFM market.

Hard FM is projected to expand at a 6.83% CAGR through 2031, making it the fastest-growing service category in the IFM market. Growth is being driven by data center critical-systems management, energy-system retrofits, and mechanical, electrical, and plumbing servicing in technically demanding environments. Asset management, MEP services, and HVAC maintenance remain the largest hard FM activities because aging infrastructure and compliance cycles leave limited room for deferred work. This shift shows where pricing power is building in the integrated facility management industry, since performance-linked hard FM contracts tied to uptime, energy use, and carbon outcomes carry more value than task-based service schedules. Mitie strengthened that position in May 2026 through a GBP 26 million (USD 33 million) M&E maintenance and energy management contract with AstraZeneca at its Macclesfield pharmaceutical campus.

By End User: Industrial Dominance Meets Commercial Momentum

The industrial and process segment accounted for 30.11% of the integrated facility management market size in 2025. This lead came from cleanrooms, semiconductor plants, pharmaceutical environments, oil and gas sites, and heavy manufacturing assets where downtime directly affects output and revenue. These facilities need a deeper mix of technical maintenance, contamination control, engineering support, and compliance management than standard office portfolios. Healthcare facilities, institutional, and public infrastructure also create significant demand because they require hard services delivered alongside strict hygiene and safety standards. ABM Industries moved further into this part of the integrated facility management industry in December 2025 when it agreed to acquire WGNSTAR for USD 275 million, with the combined semiconductor solutions portfolio expected to reach USD 325 million in annualized revenue.

The commercial segment is set to grow at 7.59% CAGR through 2031, making it the fastest-expanding end-user group in the IFM market. Return-to-office programs are increasing service frequency needs, while technology and business services occupiers are making first-time outsourcing decisions to support workplace experience goals. CBRE reported double-digit facility management revenue growth in 2025 across life sciences, healthcare, and financial services enterprise accounts, which shows how commercial demand is broadening into more specialized environments. JLL also said its Workplace Management data center segment doubled year over year in 2025, confirming that the line between commercial real estate FM and technical digital infrastructure support is narrowing.

Geography Analysis

Asia-Pacific held 40.76% of the integrated facility management market share in 2025 and is projected to grow at a 7.24% CAGR through 2031. The region combines mature outsourcing markets such as Japan, Australia, and Singapore with high-growth corridors in China, India, and Southeast Asia. Japan is showing especially strong momentum because integrated FM contracts are helping occupiers handle labour pressure, tighter governance needs, and growing ESG reporting expectations. Azbil expanded the use of AI-enabled FM platforms across Japanese facilities in 2024, while NTT Facilities also advanced IoT-based monitoring deployments in the same year. The integrated facility management market in Asia-Pacific is also benefiting from new-build demand tied to commercial real estate growth, smart-city programs, and data center pipelines in Singapore and India.

North America and Europe remain the highest-margin regional blocks in the integrated facility management (IFM) market. European demand is being supported by the need for verified facilities data, stronger carbon accountability, and a clear preference for fewer suppliers across large portfolios. In the United Kingdom, ISS secured an annual IFM contract with a major government department that starts in the second quarter of 2026, reinforcing the role of public-sector outsourcing in regional demand. Germany remains the region's highest-value single-country market, and Apleona extended its Deutsche Bank IFM agreement through December 2029 across 825 properties and 1.9 million sqm in Germany and Luxembourg. In North America, procurement is being reshaped by building-performance rules such as Local Law 97 in New York City and Title 24 in California, which favour providers that can deliver portfolio-level emissions accountability.

The Middle East is one of the fastest-moving sub-regions in the IFM market because of Saudi Arabia's project pipeline, UAE smart-city investment, and tourism-led hospitality demand. Farnek reported AED 58 million (USD 15.8 million) in first-quarter 2026 FM contract wins covering Equinix data centers and UAE education institutions, which shows the breadth of current demand in the Gulf Cooperation Council. Africa remains at an earlier stage, with South Africa, Nigeria, and Egypt leading activity as commercial property growth increases institutional outsourcing demand despite technical labour constraints. South America is centered on Brazil and Argentina, where multinational occupiers are looking for more consistent service standards across expanding commercial real estate portfolios.

Mordor Intelligence provides coverage of the integrated facility management market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

Top Companies in Integrated Facility Management Market

The integrated facility management market remains moderately fragmented, but consolidation at the upper end is becoming more visible. Large providers such as CBRE, ISS, JLL, Sodexo, and Compass Group hold strong positions through broad geographic reach, technical depth, and digital operating platforms. Even so, no operator controls a dominant portion of the integrated facility management market, which leaves significant room for outsourcing expansion and specialist entry. Compass Group said in its 2025 annual report that its share of the global food and support services market remained under 15%, which supports the view that large providers still cover only part of total addressable demand. Scale is therefore important in the integrated facility management (IFM) market, but it is not yet enough to create winner-take-most conditions.

Acquisition activity is the main route to capability expansion in the integrated facility management market. CBRE completed the USD 1.2 billion acquisition of Pearce Services in November 2025 to deepen its position in digital and power infrastructure services. OCS Group completed the acquisition of EMCOR UK in December 2025 for GBP 190 million (USD 241 million), creating a platform with more than 7,000 engineers and stronger exposure to defense, data centers, healthcare, and life sciences. ABM Industries also moved into semiconductor support through the WGNSTAR acquisition, showing that buyers are paying a premium for technical labour pools and high-compliance delivery models.

White-space demand is concentrated in semiconductor fabrication FM, APAC mid-market outsourcing, and lifecycle services for public-private infrastructure assets in the Gulf and Southeast Asia. Technology vendors are also becoming more active as competitors because firms such as Siemens and Honeywell are moving from building automation into managed building services with stronger access to equipment-level data. Regional operators with strong compliance credentials and digitally traceable delivery are gaining ground where enterprise buyers want local responsiveness without losing reporting quality, as current contract wins in the UAE show. The IFM market is therefore separating more clearly between providers that can carry performance risk at scale and providers that remain limited to lower-value subcontracting roles.

Integrated Facility Management Industry Leaders

ISS Facility Service

Compass Group PLC

Sodexo Inc.

Jones Lang LaSalle IP Inc.

CBRE Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mitie secured a £26 million (USD 33 million) M&E maintenance and energy management contract with AstraZeneca at its Macclesfield pharmaceutical campus, deploying its Orbit platform for continuous energy monitoring. The win extends Mitie's footprint in life sciences FM, a segment with structurally higher technical requirements and margins than standard commercial contracts.

- May 2026: Farnek secured AED 58 million (USD 15.8 million) in new FM contracts in Q1 2026, including total FM services for Equinix's data centers across Dubai and Abu Dhabi. This ranks among the largest data center FM awards in the GCC and signals the region's emergence as a meaningful data center IFM market.

- March 2026: ISS extended its integrated facilities services contract with a major global customer for over DKK 700 million (USD 100 million) annually for an additional two years, effective Q3 2027, covering cleaning, catering, technical maintenance, engineering, and workplace experience services globally.

- March 2026: Sodexo completed the acquisition of Grupo Mediterránea in Spain following regulatory approval, creating a combined entity with over 21,000 employees, 1,700 sites, and service to over 500,000 consumers daily. The deal cements Sodexo's position as a leading FM and food services operator across Spain and Portugal.

Global Integrated Facility Management Market Report Scope

The Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)) and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End-user Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the integrated facility management market?

The integrated facility management market was valued at USD 362.74 billion in 2025 and is projected to reach USD 518.58 billion by 2031 at a 6.25% CAGR during 2026-2031.

Which region leads integrated facility management (IFM) demand?

Asia-Pacific led with 40.76% of revenue in 2025 and is also the fastest-growing regional block in the current outlook, with a 7.24% CAGR through 2031.

Which service category is growing the fastest in facility management?

Hard FM is the fastest-growing service type, with a 6.83% CAGR through 2031, supported by data centers, energy retrofits, and complex MEP requirements.

Which end-user group contributes the most revenue?

Industrial and process facilities led with 30.11% of revenue in 2025 because cleanrooms, semiconductor sites, and pharmaceutical assets need specialized technical coverage.

What factors are driving outsourcing in IFM market?

Demand is being supported by first-time outsourcing, smart building adoption, and stronger carbon compliance rules that favor unified service delivery and verified operating data.

What are the main risks affecting providers in 2026?

The main pressure points are shortages of multi-trade labor, cybersecurity liability from connected buildings, and cost pressure from delayed contract repricing and equipment volatility.

Page last updated on: