Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

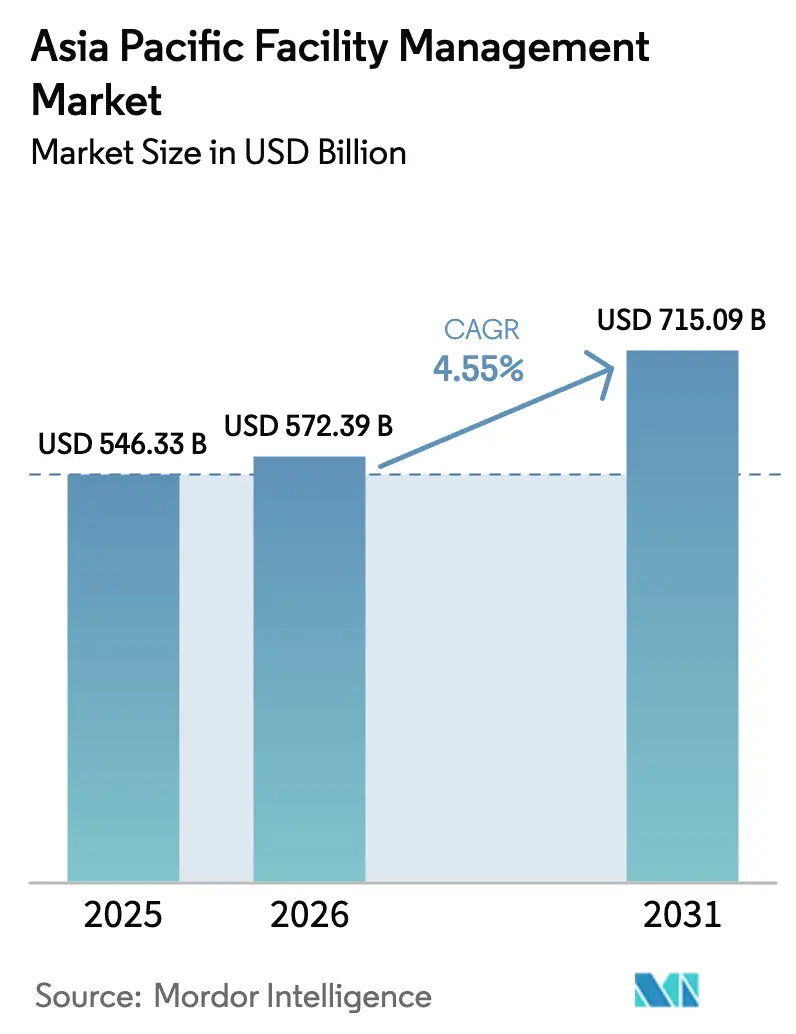

| Base Year Market Size (2025) | USD 546.33 Billion |

| Market Size (2026) | USD 572.39 Billion |

| Market Size (2031) | USD 715.09 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

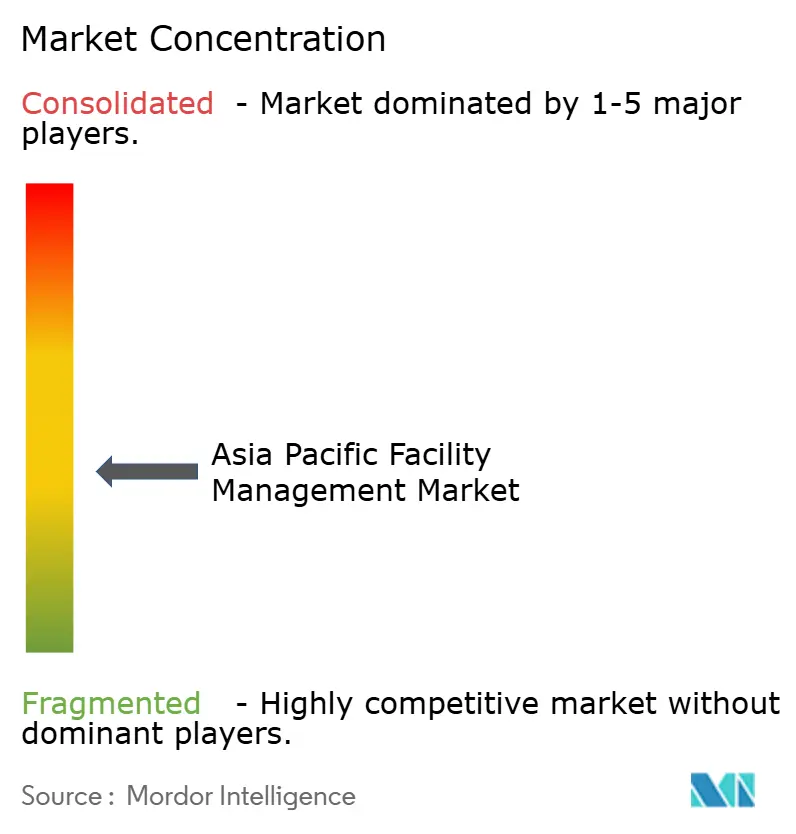

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Facility Management Market Analysis by Mordor Intelligence

The Asia Pacific facility management market size is expected to grow from USD 546.33 billion in 2025 to USD 572.39 billion in 2026 and is forecast to reach USD 715.09 billion by 2031 at 4.55% CAGR over 2026-2031. Rapid outsourcing of non-core building operations, expansion of data-intensive infrastructure, and stricter sustainability mandates are reshaping service demand across the region. Multinational occupiers in China, India, and Singapore continue to favour integrated contracts that shift compliance risk to specialized partners while unlocking capital efficiency. In parallel, tech-enabled asset monitoring has become a differentiator, with premium office towers in Tokyo and Hong Kong installing dense IoT sensor networks that feed predictive-maintenance engines. Labor shortages in Japan and Korea reinforce the pivot toward third-party providers, as aging demographics squeeze the supply of qualified technicians. Finally, the push for green-building certifications has amplified the need for real-time tracking of energy, waste, and indoor-air metrics, to the benefit of providers able to embed analytics into day-to-day operations.

Key Report Takeaways

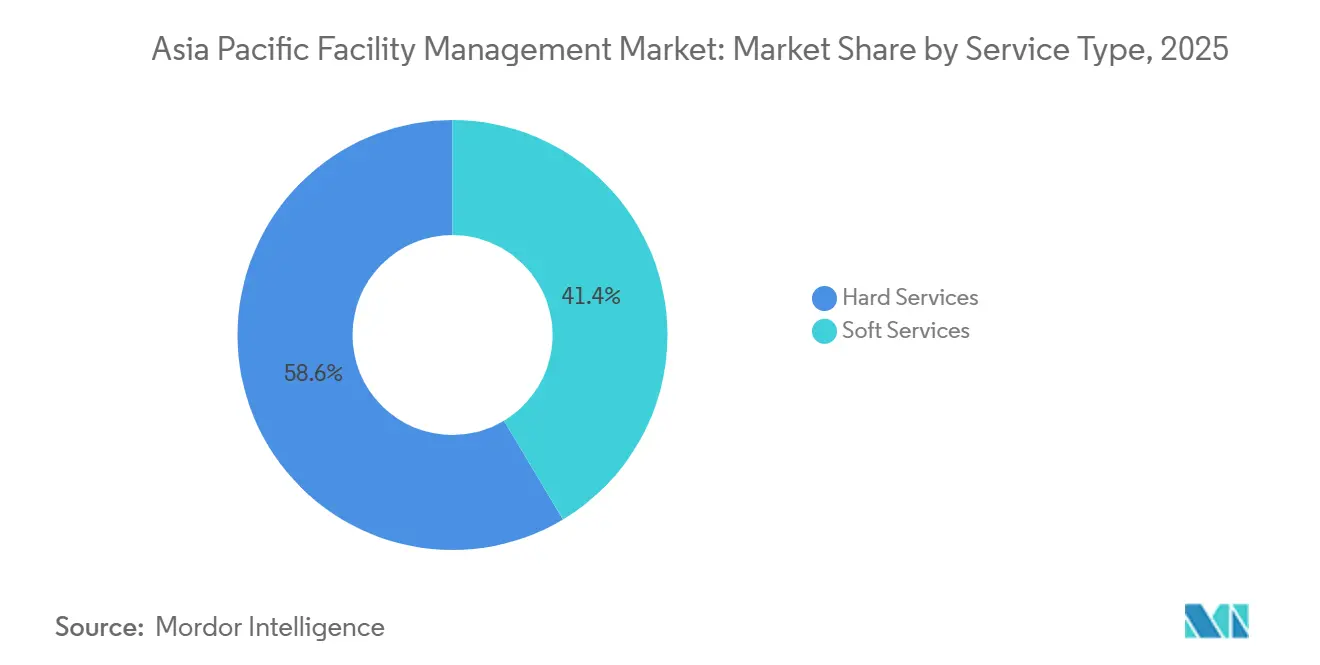

- By service type, hard services led with 58.59% of the Asia Pacific facility management market share in 2025, while soft services are projected to advance at 5.18% CAGR through 2031.

- By offering type, outsourced arrangements accounted for 72.49% of regional revenue in 2025, and integrated FM is forecast to expand at 4.89% CAGR between 2026-2031.

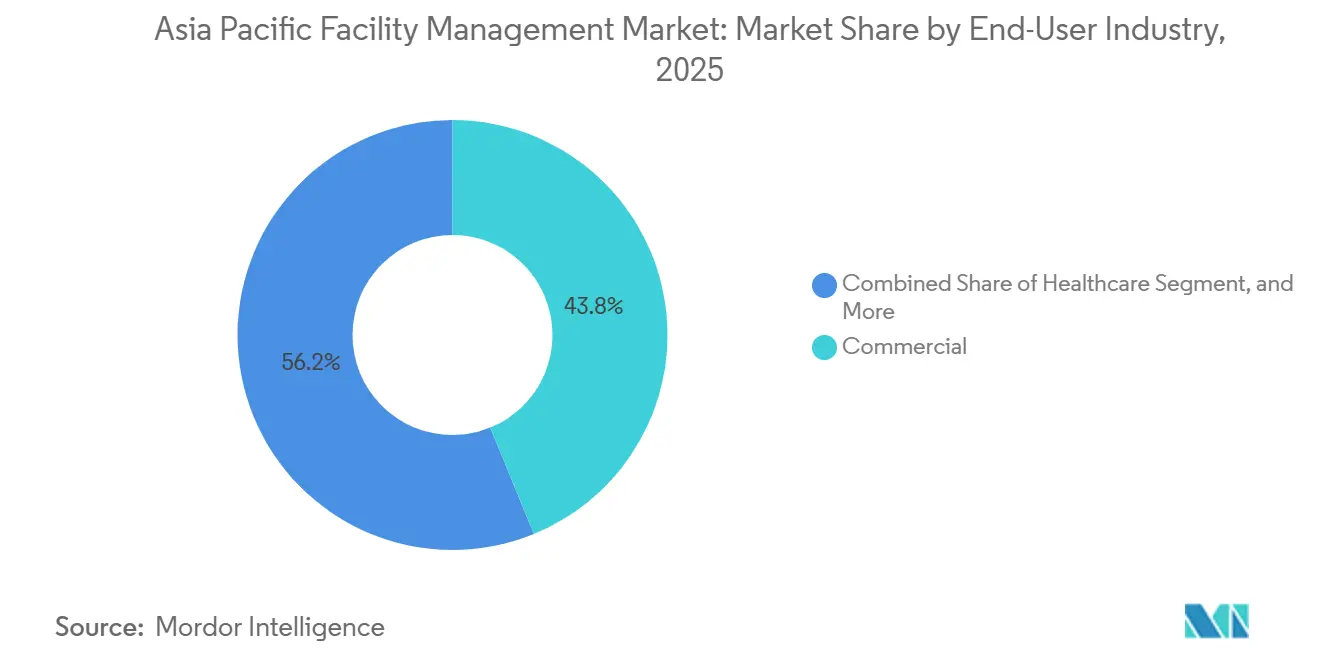

- By end-user industry, commercial facilities captured 43.82% of spending in 2025, whereas healthcare facilities are set to climb at 4.92% CAGR through 2031.

- By geography, China dominated with a 46.04% revenue share in 2025, but India is projected to log the fastest 5.23% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Outsourcing in Building Management | +1.20% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Heightened Safety and Security Needs | +0.80% | Urban centers across APAC, particularly Japan, Korea, Singapore | Short term (≤ 2 years) |

| Technological Advancements in Smart FM Solutions | +1.00% | Singapore, Hong Kong, Japan, Australia; spillover to Tier-1 Chinese cities | Long term (≥ 4 years) |

| ESG-Driven Green Building Certification Adoption | +0.70% | Australia, Singapore, Japan, Korea; emerging in India, Thailand | Medium term (2-4 years) |

| Expansion of Data Centre Construction Across Asia-Pacific | +0.60% | India, Indonesia, Malaysia, Japan; secondary growth in Thailand, Philippines | Medium term (2-4 years) |

| Growth of Life-Sciences and Healthcare Facilities Requiring Specialized FM Services | +0.50% | China, India, Singapore, Korea; public-health infrastructure in Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing in Building Management

Corporations across the region continue to offload non-core functions, seeking cost predictability and unified service-level agreements. Outsourced contracts made up 72.49% of regional value in 2025, and third-party teams now manage expansive industrial estates where in-house crews lack scale. A 2025 JLL poll found 68% of real-estate heads planning heavier outsourcing over the next three years.[1]Jones Lang LaSalle, “Asia Pacific Real Estate Investment Outlook 2025,” jll.com.sg Labor-market tightness in Japan and Korea, coupled with stronger risk-transfer requirements from multinationals, supports the continuous growth of the Asia Pacific facility management market.

Technological Advancements in Smart FM Solutions

Building owners in premium corridors are deploying IoT devices that stream equipment-health data into cloud-based CAFM platforms. Singapore’s mandate requiring smart FM in new government buildings above 5,000 m² by 2025 catalysed private uptake and demonstrated measurable energy savings.[2]Building and Construction Authority, “Smart FM Systems Mandate for Government Buildings,” bca.gov.sg Predictive analytics can cut downtime by up to 50% while extending asset life, reinforcing the move toward data-driven maintenance in the Asia Pacific facility management market. However, secondary cities lag, underscoring a digital divide that well-positioned mid-tier integrators aim to bridge.

Heightened Safety and Security Needs

Urban growth has intensified safety concerns, especially in densely populated hubs such as Tokyo and Seoul. Clients demand continuous CCTV analytics, biometric access, and cyber-physical convergence to protect both occupants and OT networks. Stricter fire-safety codes illustrated by Japan’s 2024 Building Standards Act revision require annual compliance audits and certified technicians.[3]Ministry of Land, Infrastructure, Transport and Tourism, “Building Standards Act Revision 2024,” mlit.go.jp These mandates elevate spending on monitoring, evacuation planning, and emergency-response readiness, expanding the Asia Pacific facility management market.

ESG-Driven Green Building Certification Adoption

With institutional investors tying capital to emissions metrics, landlords increasingly chase LEED, BREEAM, and regional schemes like Singapore Green Mark. Certified assets in Asia Pacific command 5-10% rental premiums and higher occupancy, pushing owners to integrate real-time metering of energy, water, and waste.[4]CBRE Group, “Green Building Adoption and Rental Premiums in Asia Pacific,” cbre.com FM providers offering verifiable ESG dashboards are winning multi-year contracts, cementing sustainability as a structural driver for the Asia Pacific facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs for Integrated FM Technologies | -0.90% | Emerging markets in Southeast Asia, Tier-2 and Tier-3 cities in China and India | Short term (≤ 2 years) |

| Fragmented Regulatory Standards Across Countries | -0.70% | ASEAN markets, India state-level variations, China provincial differences | Long term (≥ 4 years) |

| Low Digital Maturity Among Traditional FM Clients | -0.40% | Industrial and manufacturing sectors in Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Short Contract Tenures Limiting Long-Term Investment Payback | -0.50% | Retail, hospitality, and small-to-medium enterprise clients across APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs for Smart FM Technologies

Comprehensive sensor retrofits for a 100,000 m² office can run USD 1.5-2.5 million, a price tag that overshoots annual FM budgets in many Tier-2 markets. Return-on-investment horizons of four years exceed typical two-to-three-year contract cycles, deterring clients from committing capital. Consequently, adoption outside first-tier cities remains spotty, slowing the digital transformation of the Asia Pacific facility management market.

Fragmented Regulatory Standards Across Countries

Providers must juggle disparate fire codes, labour laws, and environmental rules. Thailand’s tighter overtime limits, for example, complicate workforce planning when compared with Vietnam’s more flexible framework. The absence of mutual-recognition agreements for trade certifications restricts technician mobility, inflating compliance costs and dampening cross-border scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Services Gain Momentum on Heightened Hygiene Priorities

Soft services generated accelerated demand once hygiene rose to the top of occupier agendas. In 2025, hard services delivered 58.59% of Asia Pacific facility management market share, reflecting the essential nature of MEP upkeep in aging stock. Yet soft-service contracts covering cleaning, security, and catering are projected to outstrip the overall market with a 5.18% CAGR. The Asia Pacific facility management market size, attributed to soft services, continues to climb as healthcare and hospitality clients embed rigorous disinfection regimes beyond pandemic peaks. Japan’s tight labour pool has pushed corporations to outsource janitorial and reception roles, while advanced video analytics convert traditional guard patrols into tech-assisted surveillance suites. In India and China, subsidized staff dining on corporate campuses fuels catering growth, positioning soft services as a volume and value driver.

The competitive dynamic involves mid-sized regional vendors scaling rapid-response cleaning teams, while global firms deploy robotics for repetitive floor care. Meanwhile, asset-centric hard-service players are layering condition-based maintenance to extend asset life, aligned with clients’ capex-deferral strategies. Fire-safety checks in Singapore and Tokyo, mandated annually, ensure baseline demand even as predictive diagnostics reduce unplanned callouts. Consequently, the Asia Pacific facility management market accommodates a widening service-type spread, with integrated providers bundling both streams to secure stickier contracts.

By Offering Type: Integrated FM Contracts Accelerate Despite Price Sensitivity

Integrated bundles continue to penetrate, growing at 4.89% CAGR through 2031 and commanding premium pricing for single-point accountability. Outsourced models collectively held 72.49% of spending in 2025. Enterprises consolidating regional footprints particularly manufacturing majors prefer one provider for multi-site portfolios, driving the Asia Pacific facility management market toward holistic delivery. However, cost-conscious small businesses in Indonesia and Vietnam still lean on single-service arrangements, preserving a fragmented tail.

Procurement teams increasingly evaluate technology stack, ESG reporting, and risk-transfer terms when selecting partners. Bundled hard-service packages remain a midpoint for clients unwilling to relinquish total control yet seeking administrative simplicity. Despite stubborn in-house proportions in government and defense assets, many captive teams now subcontract specialized elevator or fire-alarm testing, blurring traditional boundaries. Overall, integrated offerings illustrate the ongoing professionalization of the Asia Pacific facility management market.

By End-User Industry: Healthcare’s Specialized Demands Outpace Commercial Volume

Commercial real estate, from Grade-A offices to omnichannel warehouses, delivered 43.82% of 2025 revenue. Yet hospitals, clinics, and life-science labs should rise faster, at 4.92% CAGR to 2031, owing to infection-control mandates and expanding public-health budgets. The Asia Pacific facility management market size for healthcare assets is buoyed by requirements for continuous air-quality monitoring, medical-gas maintenance, and compliance with ISO 14644 clean-room standards.

In contrast, retail chains emphasize cost containment, often awarding separate cleaning and pest-control contracts to avoid vendor lock-in. Hospitality spending hinges on occupancy swings, but upscale resorts in Bali and Phuket have begun outsourcing linen management and kitchen sanitation to embed hygiene as a brand promise. Meanwhile, institutional campuses deliver predictable work scopes yet proceed through competitive tenders that compress margins, compelling suppliers to differentiate via workforce certification levels. This divergence underscores the varied opportunity contours inside the Asia Pacific facility management market.

Geography Analysis

China’s vast floor space guarantees volume, but energy-retrofit mandates under the Fourteenth Five-Year Plan are pivoting spend toward ESG-linked FM. Multinationals in Tier-1 cities impose global reporting templates, reinforcing demand for integrators fluent in both Mandarin and enterprise analytics. India’s federal incentives combined with accelerating logistics and e-commerce construction flank a dispersed regulatory matrix, challenging providers to craft state-specific compliance playbooks.

Japan remains technology-forward; Building Information Modelling and asset digital twins are mainstream in Tokyo skyscrapers. Labor scarcity prompts automation pilots such as autonomous cleaning fleets, sustaining higher-than-average margins in the Asia Pacific facility management market. Korea follows with similar digital penetration, albeit in a chaebol-centric ecosystem where long-standing partnerships dominate contract awards.

Indonesia and Thailand anchor emerging Southeast Asian expansion. Regulatory fluidity there opens doors for domestic specialists to co-deliver with global brands. Vietnam and the Philippines, though smaller, post double-digit FM spend increases buttressed by new semiconductor and hyperscale data-center builds funded by foreign direct investment. Australia rounds out the landscape with mature integrated contracts tightly aligned to green-lease requirements, reinforcing the region’s spectrum of maturity levels.

Competitive Landscape

The Asia Pacific facility management market remains moderately fragmented; the ten largest firms collectively capture roughly 35-40% of regional revenue. CBRE, JLL, ISS, Cushman and Wakefield, and Sodexo leverage cross-border delivery frameworks, proprietary CAFM platforms, and bundled hard-plus-soft services to secure multi-country portfolios. Domestic champions in China and India often undercut on labour cost and navigate local content rules, preserving market share in provincial municipalities.

Strategic playbooks cluster into three camps. Technology leaders deploy AI-based anomaly detection, mobile engineer dispatch, and energy-optimization algorithms to win clients that value uptime. Cost leaders focus on wage arbitrage, lean supervision, and bulk procurement of consumables to sustain thin-margin contracts across retail chains. Niche specialists concentrate on data-center maintenance, hospital sterility, or cleanroom operations, extracting premium rates in return for strict compliance protocols.

Private-equity interest continues to spur bolt-on acquisitions, evidenced by JLL’s 2025 buy-out of an Indonesian FM firm that added 1,200 staff. Meanwhile, prop-tech startups aggregate micro-vendors through digital marketplaces, threatening low-complexity scopes in the Asia Pacific facility management market. Intellectual-property races also emerge, highlighted by Mitie’s patent filing for AI-driven energy optimization, illustrating the sector’s shift from labour-heavy roots to knowledge capital.

Asia Pacific Facility Management Industry Leaders

Aden Group

Aeon Delight Co., Ltd. (Aeon Co Ltd)

Group Atalian

Broadspectrum (Ventia)

C&W Facility Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cushman and Wakefield secured final commissioning sign-off for its USD 80 million seven-year data-center FM contract in Mumbai, moving the campus into full service ahead of schedule.

- December 2025: ATALIAN Global Services unveiled a USD 50 million three-year digital-platform rollout across Singapore, Hong Kong, Japan, and Australia, aiming for real-time KPI dashboards for all major clients.

- October 2025: Sodexo launched a sustainability-focused FM suite in China, bundling energy audits, waste-diversion initiatives, and indoor-air monitoring to help landlords attain LEED and China Three Star labels.

- August 2025: Cushman and Wakefield won a 1.2 million ft² data-center mandate in Mumbai, incorporating precision cooling, UPS upkeep, and 24/7 security.

Asia Pacific Facility Management Market Report Scope

The Asia Pacific Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-house, Outsourced), End-user Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-user Industries), Facility Complexity Level (Single-site, Multi-site, Campus/Complex, Specialized), and Geography (China, India, Japan, Korea, Indonesia, Thailand, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries |

By Facility Complexity Level

| Single-site Facilities |

| Multi-site Facilities |

| Campus / Complex Facilities |

| Specialized Facilities (Data Centers, Hospitals, Laboratories) |

By Country

| China |

| India |

| Japan |

| Korea |

| Indonesia |

| Thailand |

| Rest of Asia-Pacific |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries | ||

| By Facility Complexity Level | Single-site Facilities | |

| Multi-site Facilities | ||

| Campus / Complex Facilities | ||

| Specialized Facilities (Data Centers, Hospitals, Laboratories) | ||

| By Country | China | |

| India | ||

| Japan | ||

| Korea | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia Pacific facility management market today?

It was valued at USD 572.39 billion in 2026 and is projected to reach USD 715.09 billion by 2031.

Which service type is expanding fastest in the region?

Soft services are expected to grow at 5.18% CAGR on the back of heightened hygiene and security requirements.

Why are integrated FM contracts gaining traction?

Multinational occupiers favor single-point accountability, consolidated reporting, and risk transfer, driving integrated contracts to a 4.89% CAGR.

Which country is forecast to grow the quickest?

India is set to register a 5.23% CAGR, supported by manufacturing incentives and rapid urbanization.

What is the main technology barrier facing emerging markets?

High upfront costs for IoT sensors and CAFM platforms, combined with short contract tenures, slow adoption outside Tier-1 cities.

How does ESG influence procurement?

Landlords chasing green-building certifications prioritize FM partners that can track energy, waste, and indoor-air metrics in real time, shaping bid criteria region-wide.

Page last updated on: