Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 1.91% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Facility Management Market Analysis by Mordor Intelligence

The Greece facility management market size is projected to be USD 1.98 billion in 2025, USD 2.02 billion in 2026, and reach USD 2.22 billion by 2031, growing at a CAGR of 1.91% from 2026 to 2031. Demand is holding steady despite elongated public‐sector approval cycles, because European Union Recovery and Resilience Facility (RRF) disbursements continue to finance infrastructure upgrades and a robust tourism rebound is sustaining cash flows across hospitality assets. Corporate occupiers in Athens and Thessaloniki have moved from cost-cutting toward experience-led workplace strategies, placing hygiene, energy efficiency, and digital monitoring on equal footing with traditional maintenance. International hotel brands entering the country bring global procurement standards that elevate service specifications and drive adoption of integrated contracts. At the same time, wage inflation in technical trades is compressing hard-service margins and pushing smaller vendors to consolidate or partner with multinational platforms. Across every end-user group, ESG reporting requirements are changing the definition of service delivery, because owners must now document environmental performance in auditable formats that lenders and tenants scrutinize.

Key Report Takeaways

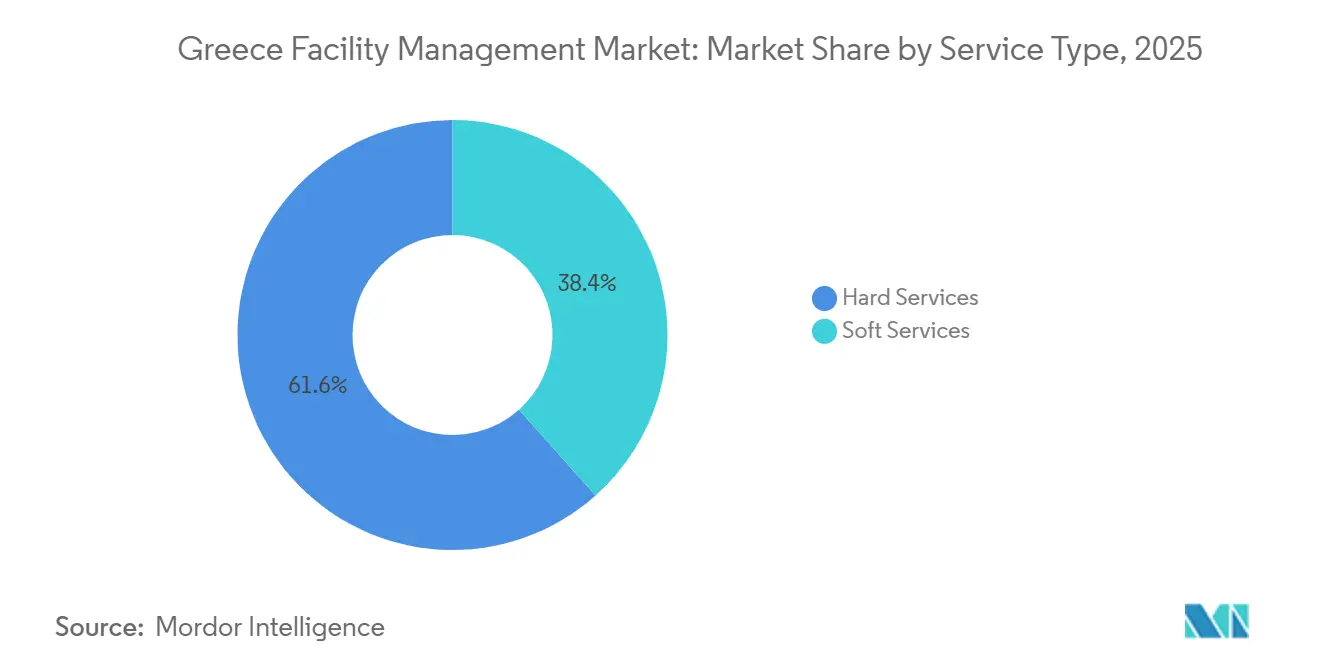

- By service type, hard services led with 61.58% of Greece facility management market share in 2025. By service type, soft services are advancing at a 2.47% CAGR through 2031.

- By offering type, outsourced arrangements accounted for 67.94% of Greece facility management market share in 2025, while integrated contracts are forecast to expand at a 2.03% CAGR to 2031.

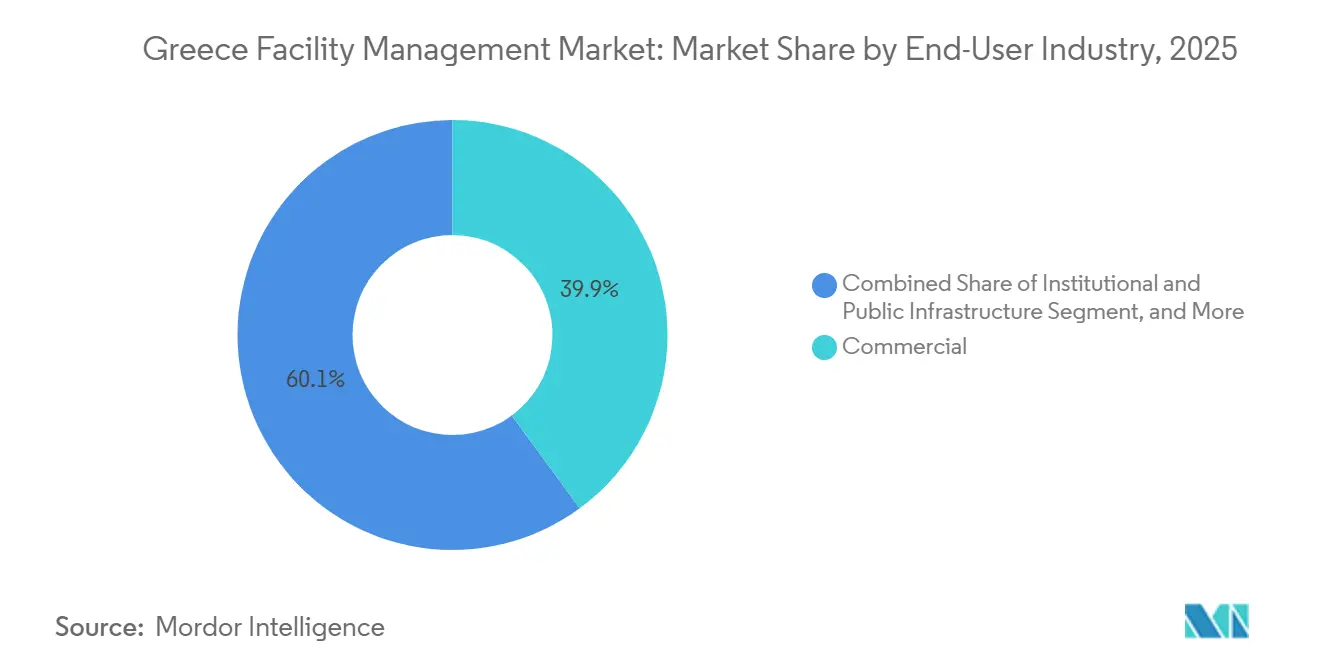

- By end-user, the commercial segment held 39.91% of Greece facility management market size in 2025 and is projected to post a 2.54% CAGR during 2026-2031. By end-user, hospitality is the fastest-growing segment, outpacing the overall Greece facility management market with double-digit revenue growth from RRF-backed hotel pipeline additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technology-Led Integrated FM Driving Operational Excellence | +0.6% | National, Early Adoption In Athens And Thessaloniki | Medium Term (2–4 Years) |

| ESG-Compliant FM Solutions Gaining Market Traction | +0.4% | National, Strongest In Hospitality And Institutional Sectors | Medium Term (2–4 Years) |

| Outsourcing Shift From In-House To Integrated FM Contracts | +0.5% | National, Led By Commercial And Hospitality Occupiers | Short Term (≤ 2 Years) |

| EU RRF Funding Catalyzing Smart Building Renovations | +0.7% | National, Priority In Public Infrastructure And Healthcare | Short Term (≤ 2 Years) |

| Tourism Supercycle Fueling Hospitality FM Demand | +0.5% | Coastal Regions And Major Islands | Short Term (≤ 2 Years) |

| Aging Commercial Real-Estate Retrofit Wave Unlocking Lifecycle Asset Management Deals | +0.4% | Athens And Thessaloniki CBDs | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Technology-Led Integrated FM Driving Operational Excellence

IoT sensors, cloud dashboards, and AI-based diagnostics are allowing managers to replace reactive work orders with data-driven, condition-based interventions that extend asset life and cut downtime. SingularLogic’s EnergySense deployment across nationwide fuel stations illustrates typical cost savings of 15-20 percent while giving clients an auditable pathway to ISO 50001 compliance.[1]Space Hellas, “The Space Hellas Group Maintains EBITDA,” SPACE.GR Yet fewer than 12 percent of commercial buildings possess open-protocol controllers, so integrators must retrofit gateways before unified analytics become possible, adding cost and elongating payback periods. Multinational vendors amortize these platform investments across pan-European contracts, giving them a price advantage that local providers struggle to match. Procurement teams have begun specifying BACnet or Modbus compatibility in recent tenders, a sign that standardization is emerging and will accelerate adoption over the next two years.

ESG-Compliant FM Solutions Gaining Market Traction

Greece transposed the EU Taxonomy into national law in 2024, compelling listed companies and financial institutions to disclose how much revenue, capex, and opex align with climate objectives. Facility managers now track energy, water, waste, and refrigerant leakage at building level and integrate those metrics into investor reports. LEED and BREEAM certifications, once niche, have become prerequisites for premium rents in Athens, commanding uplifts of 8-12 percent. Vendors showcase their own certified headquarters to win business; Manifest upgraded its offices to LEED Gold and earned ISO 50001 accreditation to underscore energy-management credibility.[2]Manifest, “CSR Report 2025,” MANIFEST.GR Because no centralized performance database exists, each provider designs bespoke measurement protocols, elevating compliance costs and making cross-portfolio benchmarking difficult. A pilot digital fire-safety registry launched in 2025 reduced certificate processing to one day, proving that government digitalization can remove similar ESG reporting frictions.[3]General Secretariat of Public Administration, “Certificate of Active Fire Protection,” MITOS.GOV.GR

Outsourcing Shift From In-House to Integrated FM Contracts

Budget-constrained occupiers are dissolving internal facilities teams and bundling cleaning, security, catering, and technical maintenance under single vendors, converting fixed payroll into variable service fees. International hotel chains entering on the back of a EUR 2.8 billion (USD 3.3 billion) investment pipeline tend to mandate integrated agreements from day one, accelerating the trend in resort destinations. Domestic corporates follow suit, attracted by lifecycle costing and risk transfer, but fragmented ownership, multiple landlords in a single tower, forces vendors to negotiate floor-by-floor, dampening economies of scale. Public tenders remain dominated by single-service awards because drafting integrated specifications requires expertise many agencies lack, perpetuating a two-speed market.

EU RRF Funding Catalyzing Smart Building Renovations

The country will receive RRF inflows equivalent to 3.6 percent of GDP by 2026, channeling capital into energy-efficiency retrofits, healthcare upgrades, and digital infrastructure. All projects carry mandatory green and digital components, so technical requirements often exceed local building codes and favor FM vendors certified to ISO 50001 or with LEED AP staff. Although award timelines can stretch beyond six months, once projects mobilize they create annuity-like maintenance contracts that bundle hard and soft services for tenors of three to five years. Administratively, the e-Authorities platform has proven that digitizing permit workflows can compress delays and, if extended to FM contracts, could lift market growth by a further 0.3-0.5 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Market Constraints Limiting Service Expansion | -0.5% | National, Acute In HVAC And Electrical Trades | Short Term (≤ 2 Years) |

| Economic Volatility Tempering Capital Allocation | -0.3% | National, Linked To Eurozone Monetary Policy | Medium Term (2–4 Years) |

| Fragmented Building Ownership Structure Hindering Integrated Contracts | -0.4% | Athens And Thessaloniki Urban Cores | Long Term (≥ 4 Years) |

| Public Procurement Red Tape Delaying FM Contract Award Cycles | -0.4% | National Public-Sector Buyers | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Labor Market Constraints Limiting Service Expansion

Unemployment fell below 9 percent in 2025, but shortages in HVAC, electrical, and fire-safety engineering remain acute as skilled technicians migrate to higher-wage Northern EU jobs.[4]Bank of Greece, “Economic Bulletin,” BANKOFGREECE.GR Wage inflation of 12-15 percent since 2023 erodes the cost advantage that once justified outsourcing, pressuring provider margins. The talent gap is most severe in digital competencies, sensor installation and BMS programming, because traditional vocational curricula do not cover data analytics. Apprenticeship programs are being co-developed with institutes, but new graduates will not appear for at least two years, leaving near-term capacity constrained.

Public Procurement Red Tape Delaying FM Contract Award Cycles

Single-bid submissions still dominate more than 70 percent of public tenders, suggesting limited competition and lengthy clarification rounds that postpone contract starts by up to a year. Even after an award, vendors face further delays due to site handovers and permit approvals. The administrative burden locks working capital and discourages smaller firms from bidding, lowering competitive intensity and keeping pricing opaque. While e-procurement portals are expanding, comprehensive reform is required to move from service-specific to integrated FM tenders that better match modern asset-management needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Diverging Growth Paths for Hard and Soft Services

Hard services commanded a 61.58 percent Greece facility management market share in 2025, reflecting the capital intensity of mechanical, electrical, and plumbing (MEP) upgrades in a building stock where 60 percent of commercial properties predate 2000. MEP and HVAC contracts dominate, because the Mediterranean climate drives heavy cooling loads and the EU F-gas phase-down compels refrigerant retrofits. Fire-safety compliance under Decree 13/2021 has also elevated demand for system inspections and certifications, adding steady recurring revenue. Soft services, although smaller in absolute value, are on a sharper trajectory, forecast to grow 2.47 percent annually through 2031. Permanent post-pandemic hygiene protocols in healthcare and hospitality require documented disinfection routines, while hybrid work models increase demand for variable cleaning rosters and flexible reception staffing.

Asset owners are layering predictive analytics onto hard-service scopes, embedding remote monitoring and automated fault detection into new contracts. That pivot supports outcome-based pricing, in which vendors guarantee uptime or energy savings, a model gaining traction among multinational tenants. On the soft side, bundling cleaning, landscaping, and catering into single invoices is simplifying vendor management for corporate occupiers. Successive tenders now stipulate ISO 45001 health and safety accreditation as a minimum threshold, nudging smaller janitorial operators either to invest in systems or partner with larger integrators. Collectively, these factors ensure that both service families remain indispensable pillars of the Greece facility management market across the forecast horizon.

By Offering Type: Outsourced Models Cement Dominance

Outsourced delivery captured 67.94 percent of spending in 2025, led by multinational corporations seeking centralized dashboards and standardized KPIs across regional portfolios. Integrated facility management contracts, where a single provider assumes responsibility for all hard and soft services under performance-linked payment terms, are expanding at a 2.03 percent CAGR. Early adopters include blue-chip office landlords and branded hotel chains importing global procurement policies. Single-service contracts remain common among smaller landlords, but administrative cost savings from consolidation are nudging them toward bundled or integrated solutions when existing agreements expire.

In-house teams still control 32.06 percent of expenditure, mainly inside large hospitals and industrial plants that value institutional memory and regulatory familiarity. Yet even these entities are moving to hybrid approaches: they retain mission-critical technicians yet outsource cleaning, catering, or grounds maintenance. Public institutions often default to single-service awards because integrated tenders require comprehensive scopes that many agencies lack capacity to write. The gap represents an education opportunity for vendors willing to host workshops on lifecycle costing, although the payback can exceed 18 months and deters firms with limited business-development budgets. Overall, outsourcing will keep increasing its Greece facility management market share as administrative reform and digital reporting needs make specialist providers more attractive.

By End-User Industry: Commercial Core, Hospitality Catalyst

Commercial real estate held 39.91 percent of Greece facility management market size in 2025, anchored in Athens and Thessaloniki central business districts where landlords upgrade aging towers to compete for multinational tenants. ESG certifications and tenant-experience apps are quickly transforming FM from a cost line into a revenue enabler, reinforcing demand for energy dashboards, indoor-air-quality monitoring, and concierge-style front-of-house services. Retrofit activity is set to accelerate further because many Class B assets need smart readiness scores to remain marketable.

Hospitality is the fastest-expanding vertical, powered by an 11 percent rise in tourism receipts during the first half of 2025. New openings in Mykonos, Santorini, and Crete now specify IoT-enabled preventive maintenance, guest-room energy management, and outsourced laundry and catering in their base-build budgets. International operators typically mandate three- to five-year integrated contracts covering HVAC, cleaning, landscaping, and security from day one, injecting a step-change in service specifications. Institutional and public infrastructure, spanning ministries, universities, and transport hubs, benefit from RRF-funded renovations but still wrestle with delayed tender cycles. Healthcare is moving rapidly because EU money earmarked for digital hospital upgrades requires long-term maintenance agreements featuring medical-grade cleaning and critical-system uptime guarantees. Industrial, retail, education, and residential collectively form the remaining demand pool, each with distinctive but lower-growth profiles.

Geography Analysis

Athens and its metropolitan fringe account for the largest slice of national spending, together with Thessaloniki they represent roughly 55-60 percent of the Greece facility management market. Athens concentrates headquarters offices, government ministries, and high-footfall cultural venues, all of which increasingly demand LEED or BREEAM compliance and therefore continuous performance monitoring. Thessaloniki’s blend of port logistics, manufacturing zones, and university campuses produces a different service mix, heavy on process-critical maintenance and laboratory cleaning. Vendor footprints mirror this distribution: multinational platforms maintain 24/7 control rooms in Athens, while regional branches in Thessaloniki handle industrial clients.

Coastal destinations such as Mykonos, Santorini, Crete, and Rhodes create pronounced seasonality. From April to October, outsourced providers ramp temporary staff for housekeeping, pool treatment, landscaping, and event catering. The same assets then downshift to skeleton crews during winter, challenging utilization planning and pressuring annual profitability. Vendors with mobile teams and strong labor agency partnerships outperform during these cycles. Fire-safety enforcement under Decree 13/2021 applies nationwide, but inspection intensity is noticeably higher in Athens and Thessaloniki, raising compliance workloads there.

Secondary cities, Patras, Heraklion, Larissa. and rural prefectures make up the remaining 40-45 percent of spending. Budgets are tighter, and public buyers often award to the lowest bidder, favoring local single-service firms over integrated contracts. The RRF is attempting to balance this disparity by allocating funds to regional road, rail, and broadband projects that will require ongoing FM. However, limited local administrative capacity slows mobilization, so national providers frequently partner with smaller firms to satisfy regional set-aside rules while maintaining quality oversight. This patchwork demands high operational flexibility and underscores why scale advantages alone do not guarantee success in the Greece facility management market.

Competitive Landscape

Innovation and Client Relations Drive Success

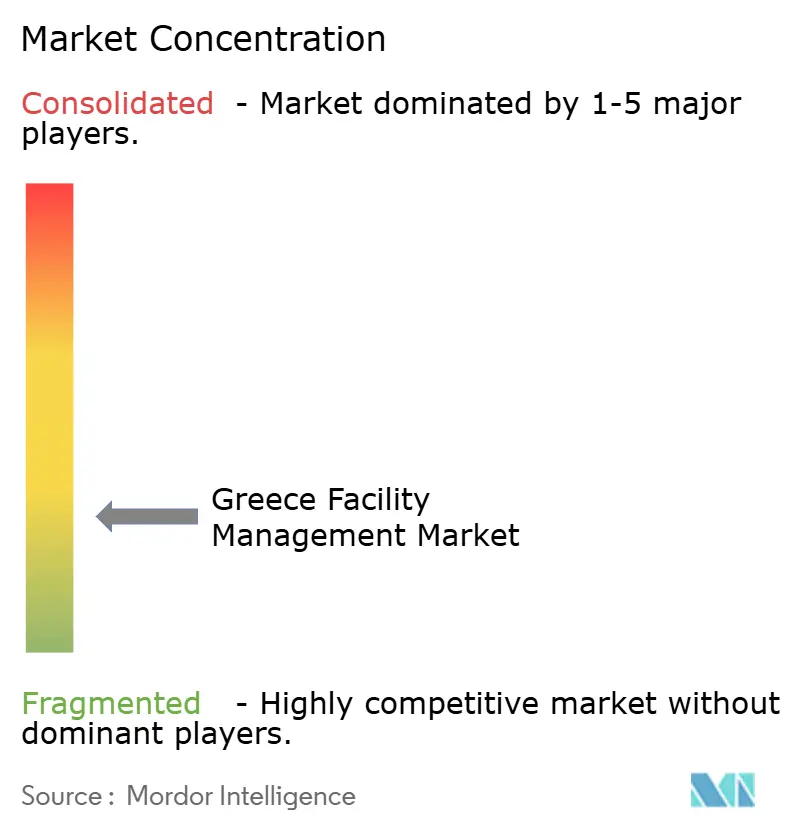

Competition is moderate, with the top five multinational operators, ISS, Sodexo, CBRE, JLL, and Cushman and Wakefield, collectively holding about 25-30 percent share. They leverage scale advantages and cloud platforms that deliver remote diagnostics, KPI benchmarking, and energy analytics. Multinationals secure pan-European master service agreements, such as ISS’s 2025 multi-country contract valued above USD 14.3 million, and then extend those scopes to Greek facilities. Local specialists like Manifest Services, Cowa Hellas, Globe Williams, Module FM, and IMAGIN control a combined 40-45 percent share by stressing client proximity and regulatory fluency.

Domestic firms differentiate through tailored pricing, granular knowledge of fragmented building ownership, and the ability to mobilize technicians quickly during tourist season peaks. Many have invested in ISO 50001 and ISO 45001 accreditations to remain competitive in public tenders. Technological gaps persist, though: fewer than 12 percent of Greek buildings possess the sensor networks required for full digital twins, so local providers often bundle retrofitting into their proposals, offsetting upfront hardware costs with multi-year service agreements. Consolidation is accelerating as wage inflation compresses margins and buyers favor integrated scopes. Several family-owned enterprises are now exploring minority stake sales to international strategic partners that can inject capital and digital toolkits.

White-space opportunities lie in outcome-based contracting, where payments hinge on energy savings or tenant satisfaction indices. Only a handful of vendors currently underwrite such commitments, but successful pilots within the commercial office segment could reshape pricing norms. Certifications have become a competitive filter; bids lacking LEED, BREEAM, or ISO credentials are increasingly shortlisted only for lower-spec contracts. Participation in industry groups such as the Hellenic Institute of Construction Fire Protection further enhances credibility.[5]KEMETA SA, “Building Security and Fire Safety Systems,” KEMETA.GR Collectively, these dynamics ensure rivalry will intensify, but capabilities rather than price alone will decide long-term winners in the Greece facility management market.

Greece Facility Management Industry Leaders

Cowa Hellas Facility Management AE

Manifest Services SA

MELKAT

IMAGIN Facility Management SA

IDMON Property Advisors & Technical Experts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Space Hellas reported H1 2025 consolidated turnover of EUR 72.0 million (USD 76.8 million) while preserving EBITDA margins and reducing total borrowing, underscoring sustained investment capacity for smart building projects relevant to FM.

- September 2025: Olympia Electronics disclosed an ESG Score A rating and announced participation in Light + Building 2026, reinforcing its position as a domestic supplier of emergency-lighting and fire-detection equipment critical to FM compliance.

- April 2025: The General Secretariat of Public Administration cut active fire-protection certificate processing to one day via the e-Authorities portal, lightening administrative load for facility managers.

- March 2025: The Ministry for Climate Crisis and Civil Protection introduced temporary six-month fire-safety certificates, enabling new hospitality and commercial properties to operate during peak season while final installations are completed.

Greece Facility Management Market Report Scope

The Facility Management Market encompasses various disciplines and services that maintain the operation, comfort, safety, and efficiency of the built environment, including buildings, infrastructure, and property. Facilities Management encompasses a number of parameters, including operations and maintenance. FM includes services such as building maintenance, maintenance operations, utilities, waste services, security, and others.

The Greece Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-House | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-House | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How big is the Greece facility management market in 2026?

It is expected to reach USD 2.02 billion in 2026, on its way to USD 2.22 billion by 2031.

What is driving demand for integrated facility management in Greece?

ESG reporting mandates, RRF-funded smart renovations, and multinational hotel chains that require single-vendor accountability are pushing occupiers toward integrated contracts.

Which service category is growing the fastest?

Soft services, especially hygiene-focused cleaning and catering, are projected to expand at a 2.47 percent CAGR through 2031.

Why are hard-service margins under pressure?

Skills shortages in HVAC and electrical trades are pushing wages higher, while older assets still need intensive technical upgrades, squeezing provider profitability.

Where is regional demand strongest?

Athens and Thessaloniki account for roughly 55-60 percent of national spending, but coastal tourism hubs generate rapid seasonal surges that specialized vendors exploit.

How will EU RRF funds affect the sector?

RRF inflows equivalent to 3.6 percent of GDP fund energy-efficient retrofits and digital infrastructure, creating multi-year maintenance opportunities once construction completes.

Page last updated on: