Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

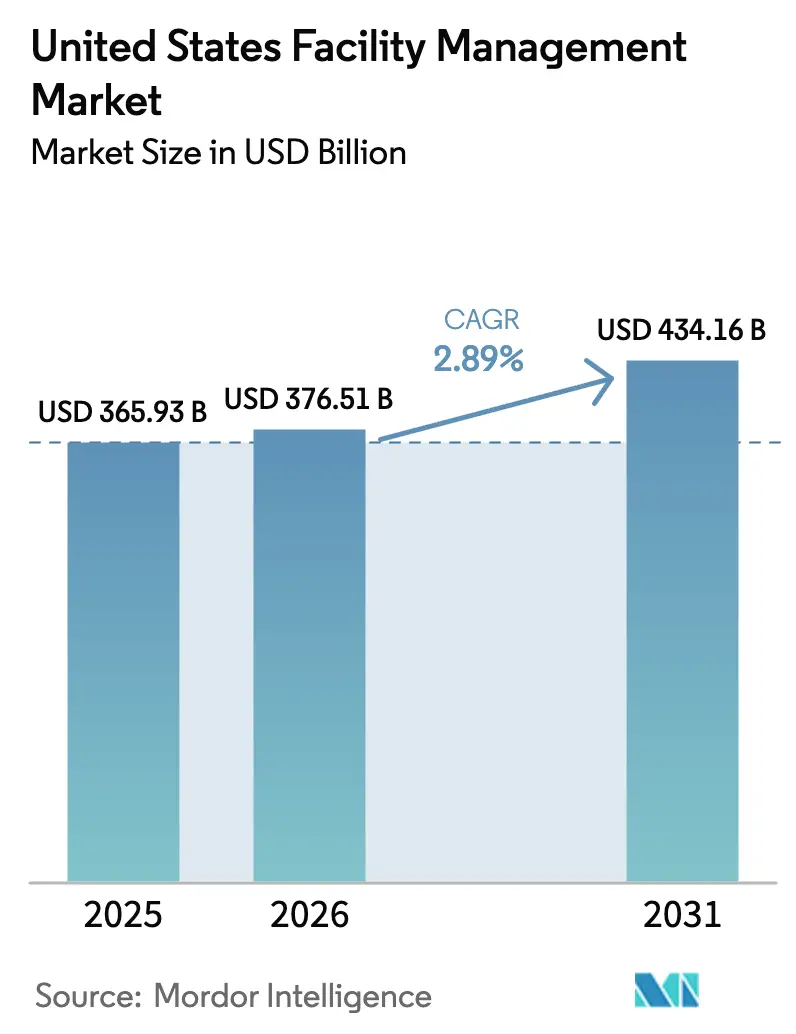

| Base Year Market Size (2025) | USD 365.93 Billion |

| Market Size (2026) | USD 376.51 Billion |

| Market Size (2031) | USD 434.16 Billion |

| Growth Rate (2026 - 2031) | 2.89% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Facility Management Market Analysis by Mordor Intelligence

The United States facility management market size was valued at USD 365.93 billion in 2025 and estimated to grow from USD 376.51 billion in 2026 to reach USD 434.16 billion by 2031, at a CAGR of 2.89% during the forecast period (2026-2031). Commercial real-estate vacancy at 14.1% in office assets contrasts with robust industrial absorption, shaping divergent demand for services. Hard services hold sway because organizations cannot postpone HVAC, fire-safety, or infrastructure upkeep, yet soft services gain ground as post-pandemic workplaces demand heightened security and wellness protocols. Regulation is equally decisive; the Inflation Reduction Act allocates USD 975 million to federal building upgrades, accelerating demand for energy-efficient retrofits. Technology integration from IoT sensors to AI-based predictive maintenance reshapes operating models by cutting downtime and optimizing utilities.

Key Report Takeaways

- By service type, hard services led with 58.45% of the United States facility management market share in 2025, while soft services are advancing at a 3.74% CAGR through 2031.

- By offering type, in-house operations held 59.05% share of the United States facility management market size in 2025, whereas outsourced services are projected to grow at a 3.70% CAGR to 2031.

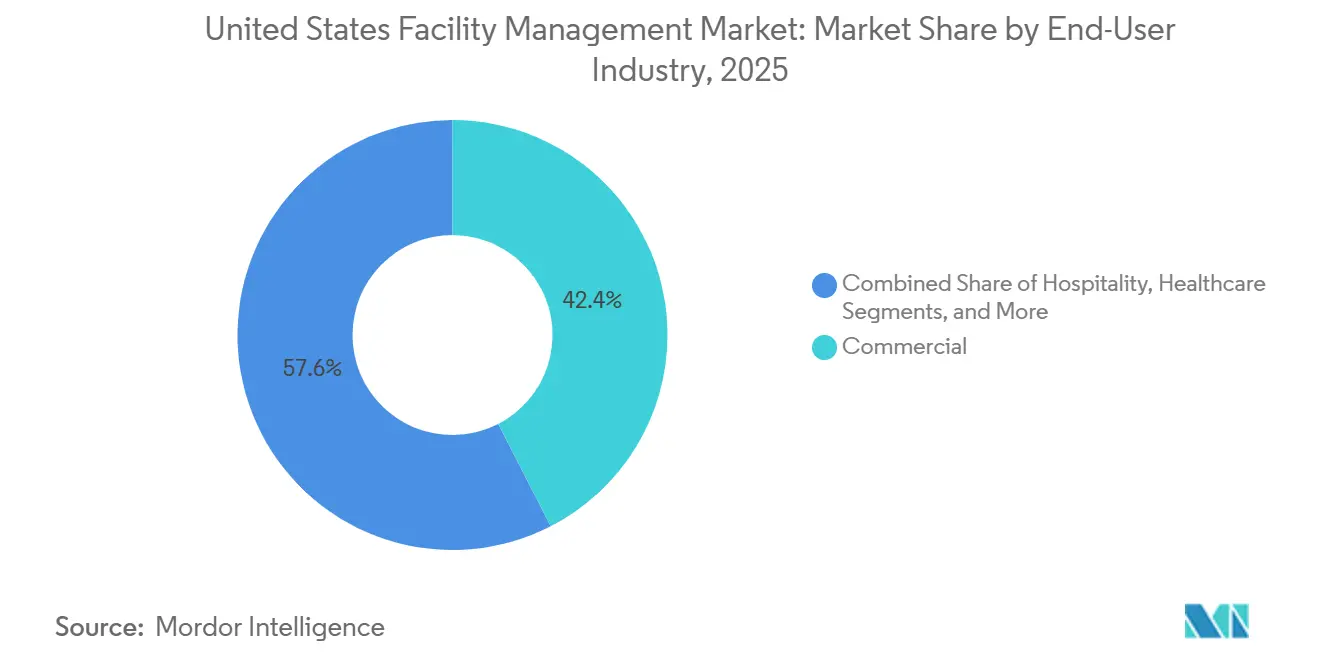

- By end-user industry, commercial facilities retained 42.44% of the United States facility management market share in 2025; institutional and public infrastructure is expanding at the fastest 5.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and population growth in metros | +0.8% | West and Southeast Sun Belt cities | Long term (≥ 4 years) |

| Sector investment priorities in infrastructure bills | +0.6% | National; Northeast and Midwest legacy infrastructure | Medium term (2-4 years) |

| Regulatory drivers on labour and safety | +0.4% | National; stricter in California and Northeast | Short term (≤ 2 years) |

| Technology-led integrated FM | +0.7% | National; early West Coast adoption | Medium term (2-4 years) |

| Building performance standards mandates | +0.5% | California, New York, Washington | Medium term (2-4 years) |

| Inflation Reduction Act tax incentives | +0.4% | States with complementary incentives | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Population Growth in Major Metros

Sun Belt hubs such as Austin and Phoenix continue to attract businesses and residents, increasing demand for both new facilities and retrofits that incorporate smart-building platforms.[1]Royal Institution of Chartered Surveyors, “The Planet of Cities: North American cities from 1980 to 2080,” rics.org Facility managers in these markets must juggle advanced automation with legacy infrastructure across mixed portfolios. Knowledge-economy tenants emphasize flexible spaces, pushing service providers to offer real-time occupancy analytics. Climate resilience has become integral after successive extreme-weather events, intensifying requirements for emergency maintenance planning. These combined pressures elevate service complexity and costs.

Sector Investment Priorities in United States Infrastructure Bills

Federal outlays direct USD 975 million to upgrade 40 million sq ft of public buildings, anchoring a spill-over of similar standards at state level.[2]U.S. General Services Administration, “Emerging and Sustainable Technology Program Details,” gsa.govBuy-American and prevailing-wage clauses inflate labor costs, compelling facility managers to refine procurement and workforce strategies. Grid-modernization spending adds responsibilities for EV-charger upkeep and energy-storage integration. Compliance tracking now factors prominently into FM contracts as owners seek assurance of bill eligibility. Thus, public spending shapes private service design.

Regulatory Drivers Specific to Labour and Safety Standards

OSHA’s updated Bloodborne Pathogens Standard now covers 793,728 facilities and magnifies documentation hours to 7.87 million, driving demand for compliance-centric FM offerings. Harmonized chemical-labeling rules effective July 2024 necessitate new signage, inventory control and staff training. Permit-Required Confined Spaces revisions enlarge the addressable market for specialty safety services. Providers with in-house regulatory expertise command premium fees yet absorb rising insurance expenses against non-compliance penalties.

Technology-Led Integrated FM (IoT, BMS, AI-Based Predictive Maintenance)

AI algorithms detect equipment failure weeks ahead, converting reactive repairs into scheduled micro-shutdowns that extend asset life. Healthcare operators deploy large-language models for policy documentation, reducing administrative load and enhancing audit readiness. IoT sensors feed cloud analytics that fine-tune HVAC performance hourly, trimming utilities and emissions. Yet connected endpoints expand cyber-attack surfaces, forcing FM vendors to add security operations to core scopes. Data-driven space-use insights also enable clients to resize footprints in hybrid work settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Profitability rates of major FM players | -0.4% | High-cost metros nationwide | Short term (≤ 2 years) |

| Workforce indicators – labor participation | -0.6% | Skilled-trade shortages across all regions | Long term (≥ 4 years) |

| Rising commercial real-estate vacancies | -0.5% | Northeast and Midwest cores | Medium term (2-4 years) |

| Cybersecurity liability exposure | -0.3% | Technology-intensive markets nationally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Profitability Rates of Major FM Players

Operating expenses exceeded revenue growth in 2024, shrinking margins and constraining tech investment. ABM Industries posted 3.3% revenue expansion but faced wage and utility inflation that eroded gains. Fragmented competition limits pricing power, especially for costly cyber-security and regulatory services. Elevated electricity now equals 58.9% of utility spend, forcing either pass-through pricing or service downgrades. The squeeze pushes small providers toward consolidation or niche specialization.

Workforce Indicators – Labor Participation

Labor force participation is forecast to fall to 61.2% by 2033, aggravating the scarcity of HVAC, electrical and plumbing technicians vital to facility operations.[3]U.S. Bureau of Labor Statistics, “Labor Force Projections 2023-33,” bls.gov Deferred maintenance on university campuses tops USD 2 trillion because staffing shortfalls block proactive programs. Wage escalation outpaces client budgets, jeopardizing contract renewals in retail and hospitality. Health systems illustrate workaround models, such as Guthrie Clinic’s virtual-care hub, mitigating a 43% nursing shortfall, yet such capital outlays remain out of reach for many FM vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Market Stability

Hard services controlled 58.45% of the United States facility management market in 2025 as clients prioritized non-discretionary asset upkeep. Predictive maintenance tools and IoT sensors are turning legacy MEP tasks into data-driven routines that curb unplanned downtime. Compliance with ever-tighter fire-safety and energy codes bolsters demand even amid cost pressures. The United States facility management market size for hard services will continue to edge upward given regulation-driven upgrades. Soft services, expanding at a 3.74% CAGR, now bundle AI-enabled surveillance, infection-control cleaning, and flexible catering models aligning with hybrid work.

Soft-service providers differentiate through ESG-aligned cleaning chemicals and real-time occupancy data that right-size staffing. Security contracts increasingly incorporate cyber-physical monitoring of access-control devices. As post-pandemic employee-experience initiatives endure, workplace support offerings gain relevance. However, labour shortages inflate wages, challenging profitability. The ecosystem thus evolves around integrated platforms that merge hard-asset health with occupant wellness metrics across the broader United States facility management market.

By Offering Type: In-House Operations Maintain Control

In-house teams retained 59.05% share as corporates guard mission-critical data and building systems. Cyber-threat anxiety and confidential R&D spaces favor direct supervision. In-house models integrate cultural alignment and immediate command-and-control during incidents. The United States facility management market share for in-house delivery is therefore likely to decline only gradually.

Outsourced solutions post a 3.70% CAGR, propelled by need for specialist energy, compliance and technology expertise. Single-service contracts give way to bundled packages and fully integrated FM, where performance-based terms shift risk toward providers. Vendors leverage scale to deploy AI dashboards across portfolios, proving cost avoidance and emissions savings to justify fees. For cost-sensitive owners, blended models combining core in-house staff with expert partners are gaining traction in the evolving United States facility management market.

By End-User Industry: Commercial Dominance Faces Institutional Challenge

Commercial users took 42.44% share in 2025, led by IT and retail facilities demanding redundancy-rich networks and temperature-controlled logistics. Yet hybrid work moderates space demand, stalling growth. Technology tenants still push for high-density power and advanced automation, sustaining premium FM scopes. The United States facility management market size in commercial assets, therefore, shows steady, not stellar, expansion.

Institutional and public infrastructure rises at 5.04% CAGR as federal funding modernizes courts, schools, and transit hubs. Compliance with zero-emission targets and accessibility codes foregrounds specialized FM skills. Hospitals invest in infection-control ventilation and backup power, while airports require baggage-handling expertise. These segments create longer contract tenures, cushioning revenue during private-sector swings in the United States facility management market.

Geography Analysis

The Northeast commands the largest regional slice, supported by dense urban stock and stringent carbon mandates that sustain retro-commissioning contracts. Legacy skyscrapers in New York and Boston require constant mechanical upgrades to meet Local Law 97 and similar rules. Financial-services headquarters also demand 24/7 uptime and cyber-secured building systems, underpinning premium service rates in the United States facility management market.

The Southeast records the quickest expansion as population influx and industrial relocations create fresh facility footprints. Metro areas such as Atlanta and Charlotte open greenfield warehouses and healthcare campuses needing full-suite FM. Hurricane exposure drives resilience investments in backup power and flood-mitigation, further broadening scopes. Cost-advantaged labor markets temper margin pressures compared with coastal peers.

Midwest demand is mixed; shrinking Rust-Belt cities scale back office portfolios while food-processing and renewable-energy facilities sustain specialized service needs. Harsh winters spike heating and building-envelope maintenance. Federal grants for grid upgrades around Great-Lakes manufacturing clusters provide a cushion.

The Southwest thrives on semiconductor fabs and data centers hungry for clean-room protocols and water-efficiency expertise. Extreme heat elevates cooling loads, pressuring FM to optimize chilled-water systems. Aerospace and defense installations add high-security requirements that command above-average pricing.

The West remains the innovation crucible. California’s aggressive building-performance codes force early adoption of AI-driven energy dashboards and seismic-resilient designs. High labor costs accelerate automation of routine inspections. Wildfire and drought risk incentivize smart-irrigation retrofits across corporate campuses, pushing integrated FM to the forefront of the United States facility management market.

Competitive Landscape

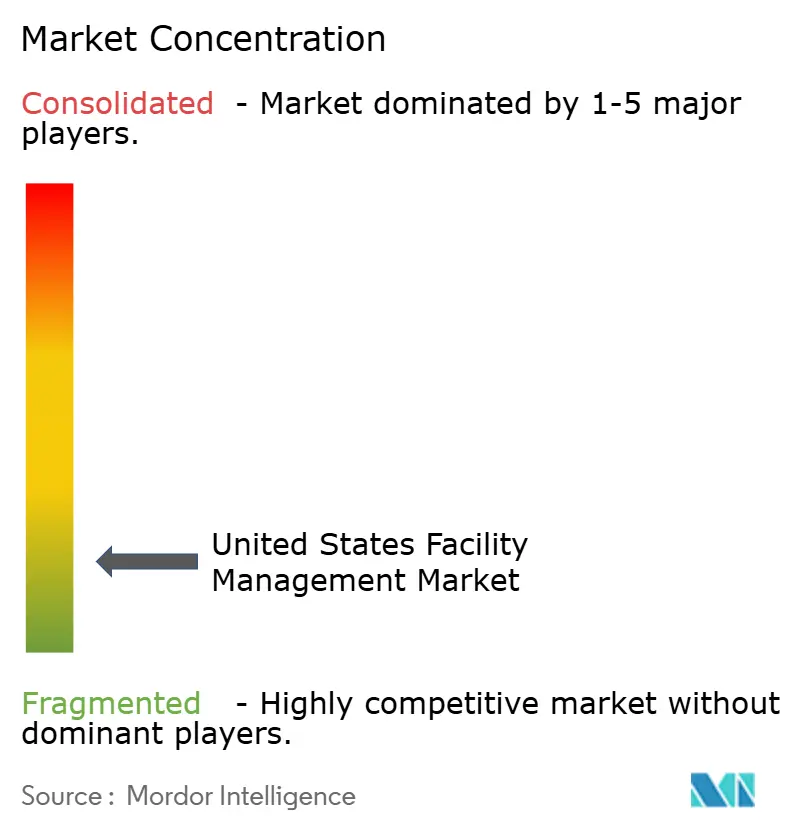

The United States facility management market shows moderate fragmentation but rising consolidation. CBRE’s USD 400 million Industrious and USD 800 million J&J Worldwide Services acquisitions extend its integrated public-sector reach. ABM invests in ERP and workforce-optimization software to keep pace. Technology is now a key battleground; providers deploy IoT sensor grids and machine-learning algorithms to deliver verifiable savings and justify outcome-based contracts.

Mid-tier firms carve niches in high-growth verticals such as data centers, life sciences, and cybersecurity. White-space opportunities include performance-risk contracting, where vendors guarantee energy or uptime metrics for premium fees. Intellectual-property filings for predictive-maintenance models reflect intensifying R&D. Workforce shortages, however, threaten scalability, making acquisition of specialized regional firms a faster route to talent.

Price competition persists for commoditized services, but specialized compliance and energy offerings command double-digit premiums. Clients increasingly solicit multi-service bundles to cut administrative overhead, pressuring small single-service outfits to partner or merge. Resulting market dynamics suggest continuing M&A momentum as providers seek scale advantages in the United States facility management market.

United States Facility Management Industry Leaders

Jones Lang LaSalle Incorporated

Cushman & Wakefield plc

Emeric Facility Services

SMI Facility Services

CBRE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CBRE reported 16% facilities-management net-revenue jump in Q1 2025 on strength in tech and life-sciences clients.

- March 2025: ABM Industries lifted FY 2025 EPS guidance to USD 3.65–3.80 after winning USD 1 billion in contracts.

- February 2025: CBRE closed its USD 800 million purchase of J&J Worldwide Services, adding 3,300 staff for Department of Defense sites.

- January 2025: CBRE Group completed full ownership acquisition of Industrious for USD 400 million, forming a Building Operations & Experience segment

United States Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates a broad range of disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, processes, places, and technology. FM contributes to the business's bottom line through its responsibility for maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation. Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services.

The United States facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current United States facility management market size?

The market is valued at USD 376.51 billion in 2026 and is projected to reach USD 434.16 billion by 2031.

Which service type leads the market?

Hard services dominate with 58.45% share because critical infrastructure upkeep cannot be deferred.

Why are outsourced facility services growing faster?

Organizations seek specialized expertise in energy management and compliance, pushing outsourced services toward a 3.70% CAGR through 2031.

Which region shows the fastest market growth?

The Southeast grows quickest due to population migration, manufacturing expansion, and healthcare construction.

How is technology changing facility management?

IoT sensors and AI-based predictive maintenance enable proactive interventions, reducing downtime and utility costs while adding cybersecurity requirements.

What drives institutional facility management demand?

Federal funding for building modernization and stringent performance mandates accelerate growth in government and educational facilities.

Page last updated on: