Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The South Africa Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value.

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

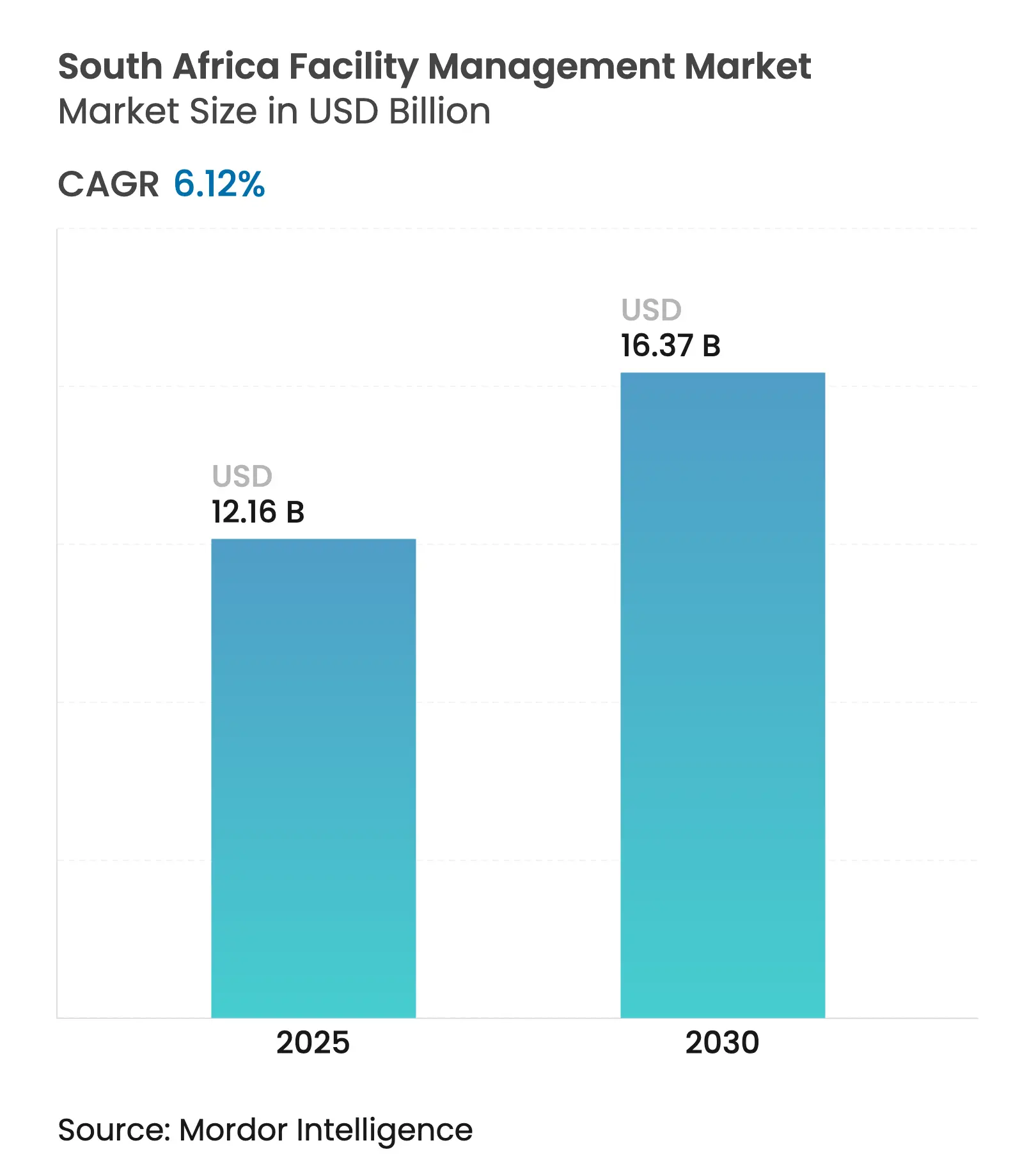

| Market Size (2025) | USD 12.16 Billion |

| Market Size (2030) | USD 16.37 Billion |

| Growth Rate (2025 - 2030) | 6.12 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The South Africa facility management market size stands at USD 12.16 billion in 2025 and is forecast to reach USD 16.37 billion by 2030, translating into a 6.12% CAGR over 2025-2030. A mix of public-sector infrastructure spending, mounting energy costs, and accelerating digital adoption underpins this growth trajectory, positioning facility management as a critical support industry for economic recovery. Government commitments to inject more than USD 54 billion into transport, energy, and water projects are expanding the opportunity pool for service providers [1]Xinhua, “South Africa to Spend over 54 bln USD on Infrastructure in Next 3 Years,” ENGLISH.NEWS.CN. Load-shedding pressures are simultaneously driving demand for integrated energy management solutions, while green-building regulations spur investment in high-efficiency MEP and HVAC services. In parallel, hyperscale data-center projects led by Teraco and Equinix are broadening the addressable market and prompting specialization in mission-critical FM competencies. Fragmented competition, skills shortages, and tightening labour regulations temper growth, yet they also incentivize technology deployment, workforce upskilling, and performance-based contracting to protect margins.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Urbanization and Population Growth in Major Metros Urbanization and Population Growth in Major Metros | 1.20% | Johannesburg, Cape Town, Durban metropolitan areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:1.20% | Geographic Relevance:Johannesburg, Cape Town, Durban metropolitan areas | Impact Timeline:Medium term (2-4 years) |

Sector Investment Priorities in South Africa's Infrastructure Pipeline Sector Investment Priorities in South Africa's Infrastructure Pipeline | 1.80% | National, with concentration in transport and energy corridors | Long term (≥ 4 years) | |||

Current Occupancy Rates Current Occupancy Rates | 0.80% | Commercial districts in major cities | Short term (≤ 2 years) | |||

Regulatory Drivers Specific to Labour and Safety Standards Regulatory Drivers Specific to Labour and Safety Standards | 0.90% | National, with emphasis on public sector facilities | Medium term (2-4 years) | |||

Growth in Green Building Certifications Growth in Green Building Certifications | 0.70% | Urban centers with corporate headquarters | Medium term (2-4 years) | |||

Digitalization and Smart FM Solutions Adoption Digitalization and Smart FM Solutions Adoption | 1.10% | Technology hubs in Johannesburg, Cape Town, Durban | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Urbanization and population growth in major metros

Rapid metropolitan expansion is amplifying demand for South Africa facility management market services across newly built office towers, retail precincts, and mixed-use developments. Johannesburg property values rose 6% in 2024 with rental yields of 7-10%, while Cape Town delivered 4-5% annual growth, underscoring the depth of FM opportunities[2]The African Investor, “12 Stats for the Johannesburg Real Estate Market in 2025,” THEAFRICANVESTOR.COM. Emerging migration patterns are shifting professional populations toward secondary towns, prompting modern FM requirements in previously under-served areas. Mixed-use precincts such as Sandton and Woodstock commonly adopt integrated FM contracts to manage multi-tenant sites and shared utilities. Combined with a USD 54 billion infrastructure pipeline, these urban dynamics sustain a robust project queue for contractors.

Sector investment priorities in South Africa’s infrastructure pipeline

Allocated spending of ZAR 402 billion for transport, ZAR 219.2 billion for energy, and ZAR 156.3 billion for water creates a multi-sector runway for South Africa facility management market providers. More than 150 projects catalogued in the Construction Book 24/25 are now open for private participation, encompassing roads, ports, and power assets that each require construction-phase site services and long-term O&M agreements. Specialized FM capabilities-ranging from high-voltage maintenance to water-treatment oversight-are increasingly embedded in concession contracts, elevating revenue visibility. Local-content rules and skills-development clauses further advantage domestically anchored FM firms that can demonstrate training and supplier-development track records.

Growth in green-building certifications

Certified buildings yield energy savings of 20-30% and water savings of 30-40% relative to conventional assets, catalysing demand for energy-efficiency services and performance-guaranteed FM contracts[3]Council for Scientific and Industrial Research, “CSIR Releases Statistics on Power Generation in South Africa for 2024,” CSIR.CO.ZA. Escalating electricity tariffs-up 10% annually over the past decade-motivate owners to retrofit HVAC, lighting, and water-recycling systems, reinforcing uptake of the South Africa facility management market’s energy-efficient MEP segment. Tax incentives equal to 125% of renewable-energy project costs and a maturing carbon-credit marketplace enhance ROI for FM-led solar and storage installations, particularly in healthcare campuses and large office parks.

Digitalization and smart FM solutions adoption

South Africa’s smart-building segment is projected to grow 32% annually and could generate USD 2 billion in revenue by 2026, signalling sharp acceleration in IoT-enabled FM demand. Predictive maintenance, occupancy analytics, and remote-monitoring platforms are moving FM from a cost center to a performance partner. Eighty-six percent of traditional property outfits now engage prop tech firms, integrating AI and data analytics to raise tenant satisfaction and asset uptime. Municipal modernization programs further amplify adoption as local governments pilot IoT sensors to enhance public-facility service delivery, adding digital competencies to essential bid requirements.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Profitability Rates of Major FM Players Profitability Rates of Major FM Players | -0.90% | National, with concentration in competitive urban markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.90% | Geographic Relevance:National, with concentration in competitive urban markets | Impact Timeline:Short term (≤ 2 years) |

Workforce Indicators – Labour Participation Workforce Indicators – Labour Participation | -1.10% | National, with acute impact in skilled trades | Medium term (2-4 years) | |||

Intermittent Power Supply and Load Shedding Costs Intermittent Power Supply and Load Shedding Costs | -1.30% | National, with severe impact in industrial areas | Short term (≤ 2 years) | |||

Skills Shortage in Advanced FM Technologies Skills Shortage in Advanced FM Technologies | -0.80% | Urban centers requiring specialized technical capabilities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Profitability rates of major FM players

Recurring diesel outlays to counter load shedding have trimmed operating margins for retailers and their FM contractors; Shoprite alone flagged a potential 10% profit erosion tied to backup-power expenses. Commoditized cleaning and guarding contracts endure fierce price competition, while currency volatility raises wage bills pegged to the national minimum of ZAR 28.79 per hour. The squeeze limits reinvestment in technology and training, slowing overall market modernization despite growing client expectations.

Workforce indicators – labour participation

National unemployment of 32% conceals acute trade-skill scarcities in electrical, plumbing, and HVAC fields. Construction and FM industry groups warn that insufficient apprenticeships and costly training pathways are shrinking the talent pipeline. Skills gaps impede South Africa facility management market providers from scaling integrated and smart-building services, obliging firms to implement aggressive retention tactics and bolster in-house academies. Brain-drain migration to overseas markets compounds the shortage, stretching project delivery timelines.

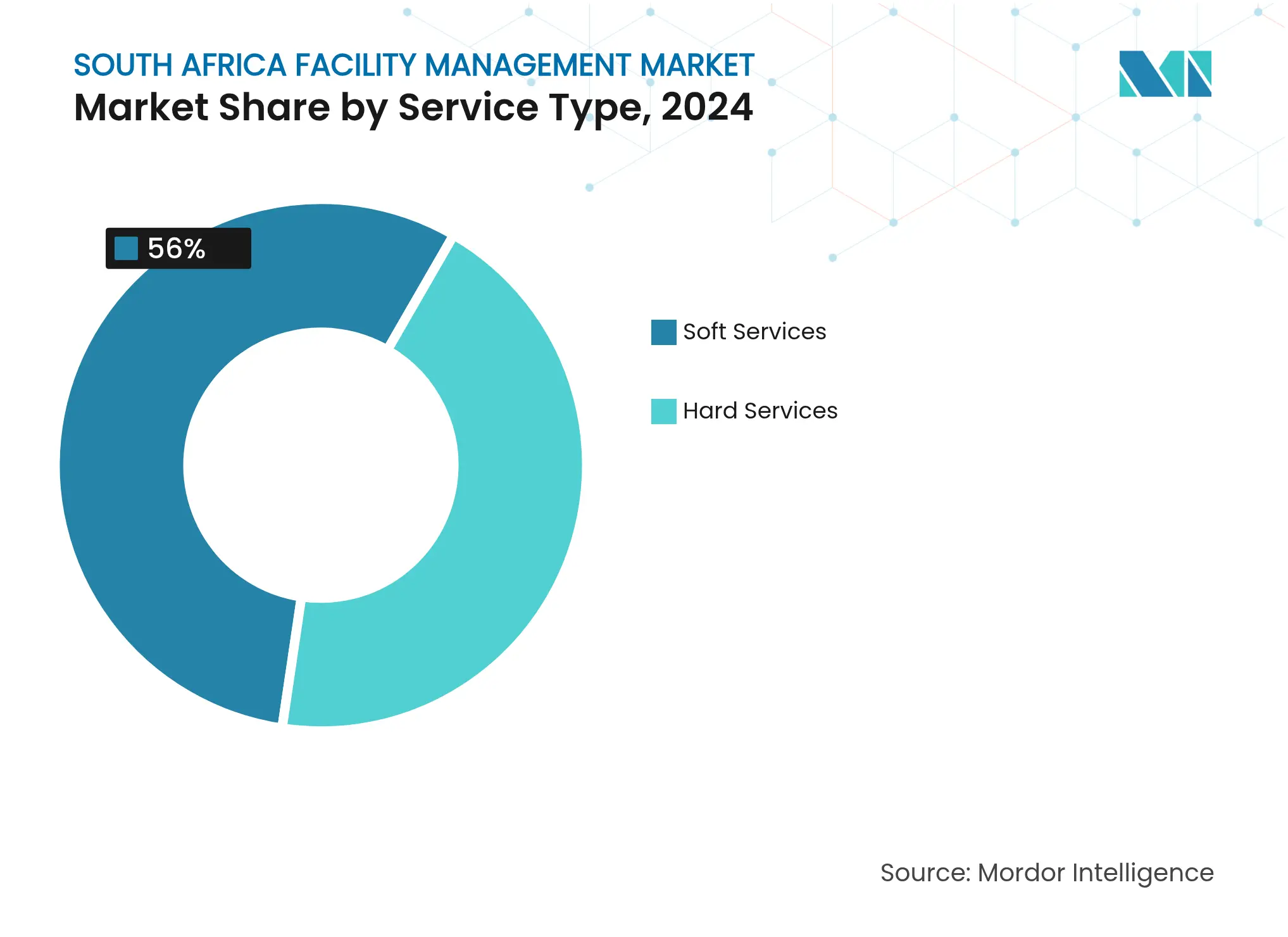

By Service Type: Soft services lead despite hard-service innovation

Soft services commanded a 56% slice of the South Africa facility management market in 2024 thanks to non-discretionary cleaning and security needs across offices, malls, and public infrastructure. Energy-efficient MEP and HVAC sub-segments within hard services represent the fastest-growing pocket, expanding at a 10.8% CAGR as utility tariffs rise and green certifications multiply. The South Africa facility management market size attributed to soft-service contracts is projected to widen steadily, though its market share may erode marginally as data-rich hard services gain traction. Demand for predictive asset-management solutions is simultaneously steering clients toward blended contracts that fuse cleaning with sensor-enabled maintenance dashboards.

Hard-service uptake is reinforced by building-code updates that emphasize fire safety, indoor-air quality, and lift compliance, pushing owners to rely on technically certified FM partners. Digital security, robotics-assisted cleaning, and waste-recycling programs are upgrading soft service value propositions. Hybrid work has moderated in-office catering demand, yet FM providers are pivoting to flexible meal-prep models and subscription-based offerings to sustain volumes.

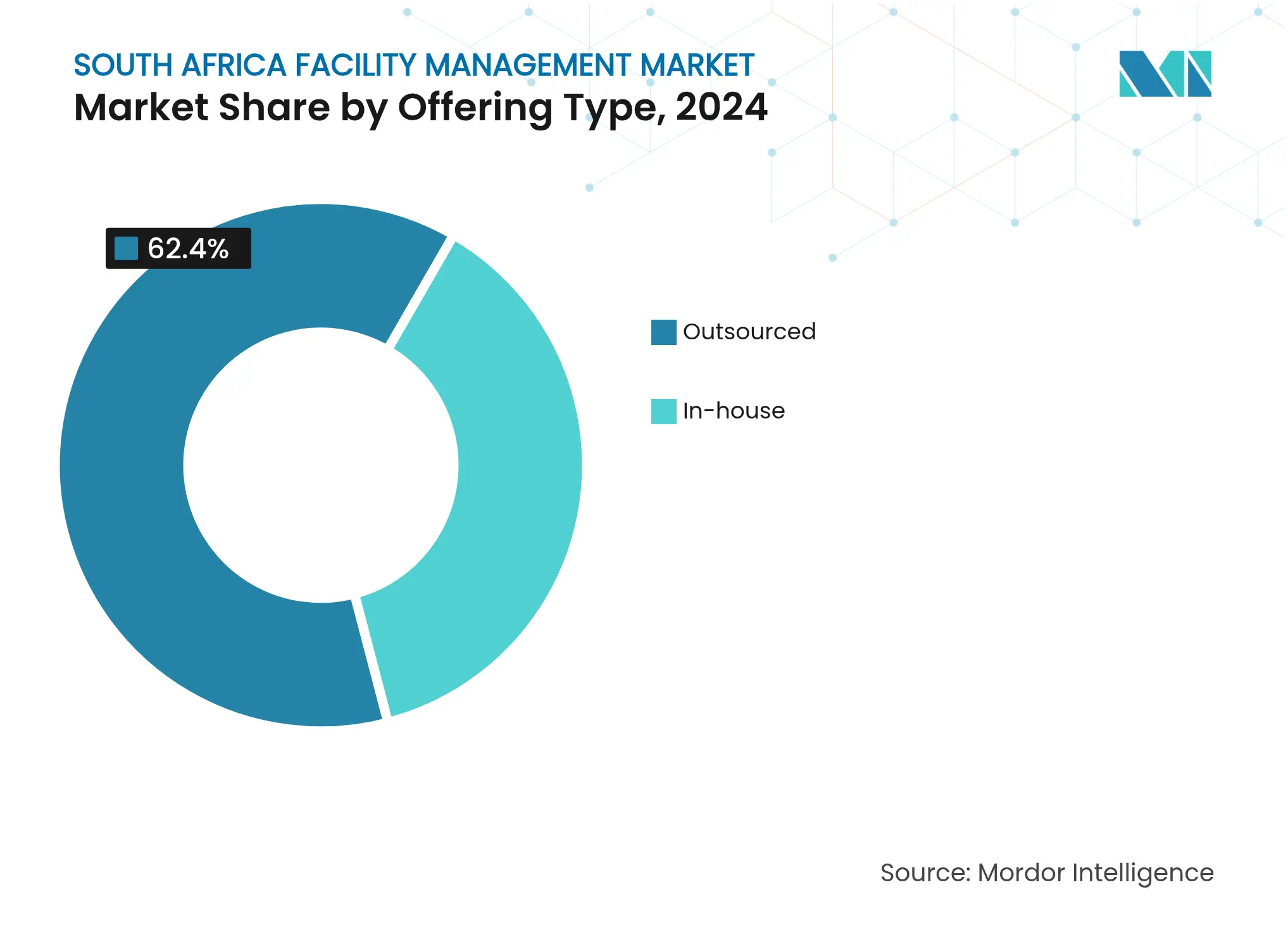

By Offering Type: Outsourced models dominate market evolution

Outsourced contracts held 62.4% of South Africa facility management market share in 2024 as organizations concentrated on core operations and cost certainty. The South Africa facility management market size attached to integrated FM is expected to overtake bundled models in the forecast window, buoyed by PFI concessions and campus-style developments that prefer long-tenor, full-scope agreements.

In-house teams retain 37.6% share, primarily among banks, parastatals, and defense-sensitive complexes valuing direct control. Yet labour-availability risks and rapid tech refresh cycles are prompting a gradual pivot toward hybrid structures in which strategic oversight remains internal while operational tasks migrate to specialist outsourcers. Performance-based contracting is deepening, tying fee escalation to energy-saving or uptime targets that reward innovation while capping client risk.

By End-user Industry: Commercial dominance faces data-center disruption

Commercial and corporate real estate accounted for 31% of 2024 demand, anchored by Johannesburg’s status as the continent’s financial capital. However, hyperscale data centers and ICT facilities are set to become the fastest-growing niche at 9.6% CAGR after Teraco and Equinix announced USD 840 million in aggregate South African CAPEX. The South Africa facility management market size for mission-critical sites will therefore outpace conventional office growth, supported by stringent uptime SLAs and 24/7 engineering requirements.

Institutional and public-infrastructure assets contribute a defensive revenue stream, reinforced by multi-year government FM tenders for airports and hospitals. Healthcare demand is expanding further as new private hospitals, such as the 222-bed Mediclinic George, standardize infection-control and biomedical-engineering maintenance regimes. Industrial, hospitality, and mixed-residential segments each offer specialized sub-opportunities-ranging from food-safety compliance to sports-arena crowd-flow analytics-that favour providers with sector-specific playbooks.

Johannesburg, Cape Town, and Durban collectively generated close to 70% of 2024 demand, mirroring their concentration of head offices, financial services, and logistics nodes. Johannesburg leads South Africa facility management market activity on the back of sustained office-tower development in Sandton and a cluster of ICT campuses in Midrand. Commercial property values climbed 6% in 2024 with vacancy rates tightening, fuelling service outsourcing and integrated energy-retrofit contracts.

Cape Town blends technology, tourism, and manufacturing drivers, widening the scope of service bundles requested. Strong municipal emphasis on green-building bylaws makes the city an epicentre for sustainability-focused FM pilots. Rental yields above 8% and ongoing migration from inland provinces are attracting new investors that frequently commission turnkey FM packages from project inception.

Durban and secondary metros such as Pretoria and Gqeberha are ascending as infrastructure funds decentralize spend beyond Gauteng and the Western Cape. Government road and port projects executed by SANRAL and Transnet are spurring demand for site-camp services and post-handover O&M frameworks [4]South African National Roads Agency, “Building South Africa through Better Roads: SANRAL Tenders,” SANRAL.CO.ZA. Mining belts in Mpumalanga and Limpopo add to regional diversification, requiring safety-critical, high-skill FM support for smelters and accommodation villages.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

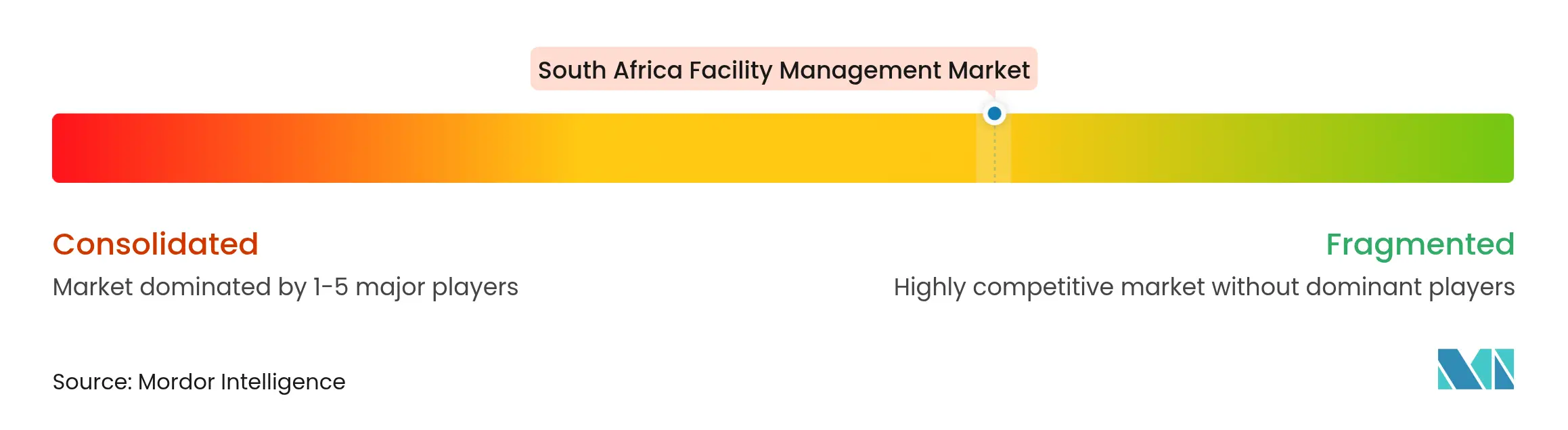

Market Concentration

The competitive fabric is moderately fragmented: the top five firms hold an estimated one-third of revenue, leaving room for regional specialists and tech-centric disruptors. Global heavyweights ISS, CBRE, and JLL leverage proprietary platforms and multinational client rosters to capture integrated FM mandates in banking and telecoms. Domestic champions Servest, Bidvest Facilities Management, and Tsebo Solutions differentiate through nationwide footprints, transformation credentials, and labour-relations acumen.

Technology has become the primary battlefront. CBRE’s creation of its Building Operations & Experience division after acquiring Industrious in 2025 underlines a push toward data-led workplace solutions that blend FM with flexible space. Local entrants partner with prop tech startups to embed IoT sensors, mobile work-order apps, and AI-driven predictive analytics, offsetting wage inflation and skills shortages. Sustainability branding is another contest arena: firms able to document verifiable energy savings and waste-diversion metrics secure premium pricing and long-tenor contracts with ESG-driven landlords.

Looking ahead, consolidation is likely among mid-tier cleaning and security vendors as margin compression intensifies. Conversely, niche scaling opportunities persist for firms focused on healthcare FM, data-centre specialist engineering, and renewable-asset maintenance, where certification barriers protect margins.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, processes, places, and technology. FMs contribute to the business's bottom line through their responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

The South Africa facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.