Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

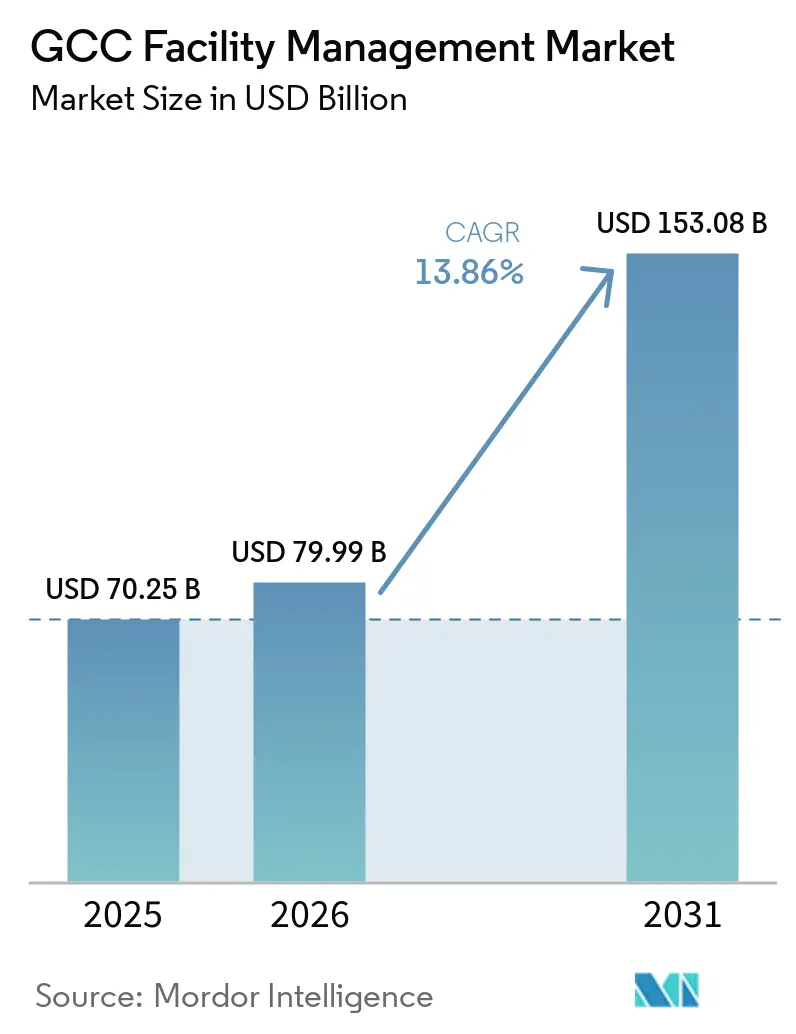

| Base Year Market Size (2025) | USD 70.25 Billion |

| Market Size (2026) | USD 79.99 Billion |

| Market Size (2031) | USD 153.08 Billion |

| Growth Rate (2026 - 2031) | 13.86% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Facility Management Market Analysis by Mordor Intelligence

The GCC Facility Management Market size is expected to increase from USD 70.25 billion in 2025 to USD 79.99 billion in 2026 and reach USD 153.08 billion by 2031, growing at a CAGR of 13.86% over 2026-2031. Accelerated diversification initiatives led by Saudi Arabia’s Vision 2030 and the UAE’s Smart City agenda continued to reshape corporate approaches to facilities, prompting rapid adoption of artificial-intelligence and Internet-of-Things platforms for building management. Megaproject pipelines such as NEOM, the King Salman International Airport expansion, and Dubai’s ongoing mixed-use developments underpinned robust demand for outsourced services, while data-center construction and mandatory green-building schemes reinforced specialized hard-service requirements. Competitive intensity remained moderate, yet technology investment and rising labor localization thresholds triggered consolidation pressure as smaller suppliers struggled to fund digital upgrades and training programs.

Key Report Takeaways

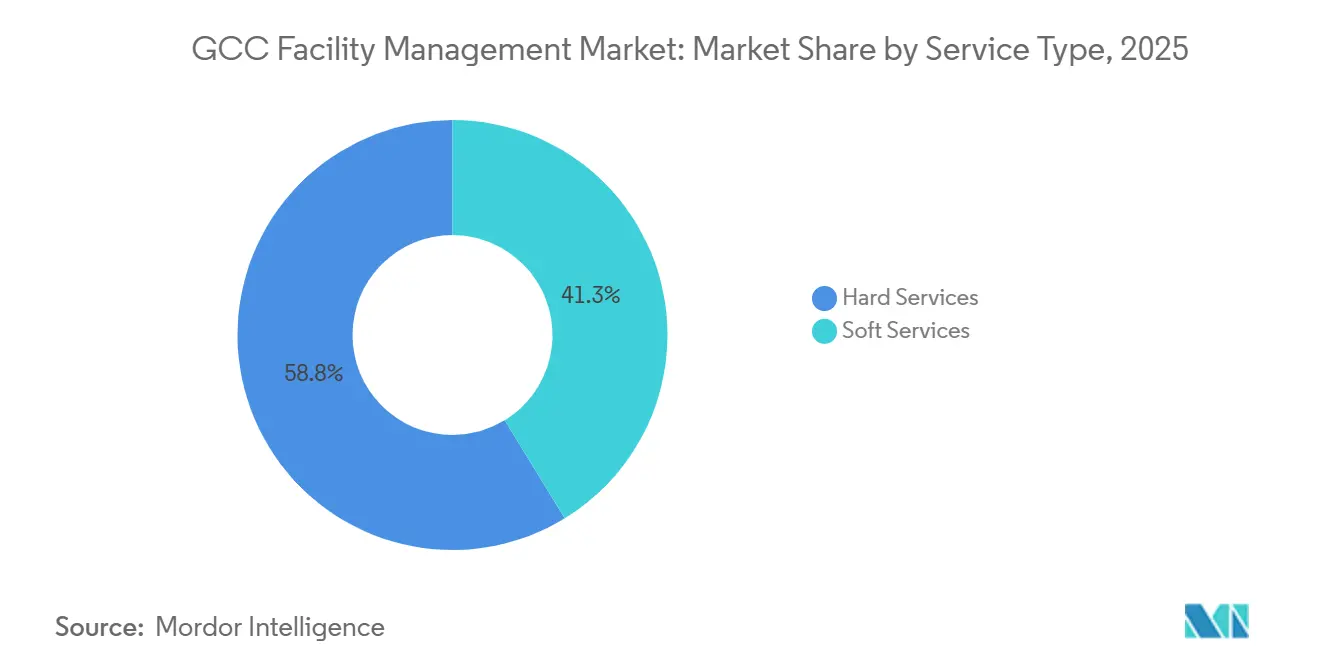

- By service type, hard services led with 58.75% revenue share in 2025; soft services are advancing at a 14.12% CAGR through 2031.

- By offering type, the outsourced model accounted for 61.15% of the GCC facility management market share in 2025, while integrated packages are projected to grow at 14.28% CAGR to 2031.

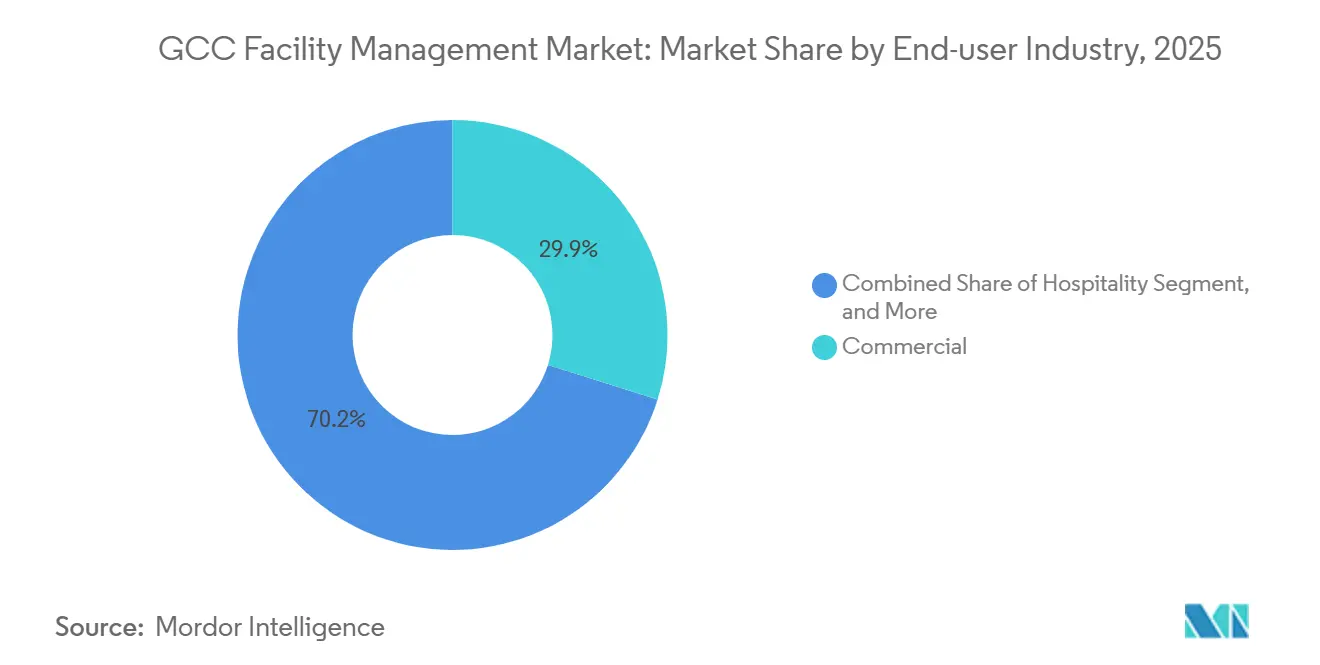

- By end-user industry, commercial facilities held 29.85% share of the GCC facility management market size in 2025 and industrial & process sites are expanding at a 16.42% CAGR through 2031.

- By country, Saudi Arabia commanded 43.75% revenue share in 2025; it is forecast to post a 12.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure development | +3.2% | Saudi Arabia core, spillover to UAE and Qatar | Long term (≥ 4 years) |

| AI and IoT integration in building management | +2.8% | UAE and Saudi Arabia leading, expanding to Kuwait and Qatar | Medium term (2-4 years) |

| Data-center expansion | +2.1% | UAE and Saudi Arabia primary, Qatar emerging | Medium term (2-4 years) |

| HVAC innovation and energy-efficiency needs | +1.9% | Global across all GCC states | Short term (≤ 2 years) |

| Green building certification mandates | +1.7% | UAE and Saudi Arabia leading, Bahrain and Qatar following | Medium term (2-4 years) |

| Privatization of municipal services | +1.5% | Saudi Arabia and Kuwait primary, UAE selective | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Development

Saudi Arabia’s Vision 2030 funneled USD 66.67 billion into healthcare alone by 2025, alongside airports, rail and smart-city districts, catalyzing unprecedented demand for integrated facility services.[1]Vision 2030 Secretariat, “Annual Report 2023,” SAUDI ARABIA VISION 2030, vision2030.gov.sa The 2023 launch of state-owned FMTECH signaled commitment to professionalize operations, compelling global contractors to form local joint ventures. Spill-over effect surfaced in the UAE and Qatar as authorities accelerated comparable diversification projects. Providers offering predictive maintenance, LEED expertise and workforce-localization strategies captured early contracts, reallocating resources toward giga-projects such as NEOM and the Red Sea resorts where multiyear FM budgets are embedded from the design phase.

AI and IoT Integration in Building Management

The UAE piloted AI-enabled digital twins at DEWA’s Al Shera’a headquarters, setting a regional benchmark for 30% energy savings and real-time asset analytics. This benchmark is reshaping procurement expectations across the UAE facility management. Enova’s Gemini-powered virtual assistant illustrated how cloud AI streamlined work-order resolution across mixed portfolios.[2]Enova by Veolia "Enova Launches Advanced AI-Powered Virtual Assistant in Collaboration with Google Cloud," enova-me.comSaudi developers followed suit, embedding IoT sensors in commercial towers within Riyadh’s King Abdullah Financial District to monitor more than 100,000 assets. Adoption widened the performance gap between tech-forward and traditional vendors, accelerating M&A activity as incumbents sought digital capabilities to maintain service-level compliance.

Data-Center Expansion

Regional colocation capacity has been growing significantly, driving the demand for specialized facilities management services focused on precision cooling and continuous uptime management. After partnering with Silver Lake, Khazna aimed to secure a significant share of Saudi Arabia's emerging data-center market. Operators mandated ISO 27001 security, concurrently integrating renewable micro-grids. Facility managers versed in digital-twin commissioning and lithium-ion UPS maintenance secured multi-year, performance-linked contracts across hyperscale campuses in Jeddah, Dubai South and Doha.

HVAC Innovation and Energy-Efficiency Needs

Cooling systems, which dominate peak electricity loads, have prompted clients to explore solar-assisted chillers and retrofits with R-32 refrigerants. At Saudi Aramco's headquarters, high-vacuum flat panels enabled significant energy substitution for chillers. Meanwhile, Aeroseal made strides in duct-sealing efficiencies for high-rise office towers with its recent debut in the Middle East. In a landscape where utility-tariff reforms penalize inefficient consumption, AI-driven predictive maintenance has emerged as a game-changer, significantly curbing unplanned outages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages | -2.3% | Global across all GCC states, acute in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Nationalization-policy challenges | -1.8% | Saudi Arabia and UAE primary, Kuwait and Bahrain moderate | Medium term (2-4 years) |

| Inflation-linked service contract cost pressures | -1.5% | Global across all GCC states | Short term (≤ 2 years) |

| Regulatory heterogeneity across GCC states | -1.2% | Cross-border operations primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages

Expatriates comprised significant portion of Bahrain’s FM workforce, yet new localization quotas tightened visas across Saudi and UAE sites, straining availability of certified HVAC and fire-safety technicians. Contractors missing Nitaqat thresholds faced sanctions, compelling aggressive scholarship programs and technical-college alliances. The resulting wage inflation pressured margins even as clients demanded cost reductions.

Nationalization-Policy Challenges

Saudiization, Emiratization and analogous rules forced multi-country operators to juggle divergent ratio targets, inducing compliance overhead and productivity dips during onboarding.[3]Khalid Al-Qabas, “Saudi Arabia’s Plan for Changing Its Workforce,” MIGRATION POLICY INSTITUTE, migrationpolicy.org Studies showed formal mentoring and job-redesign improved retention and eased cultural adjustment, yet interim contract delivery risks remained high. Long-term, firms achieving localization excelled in winning government concessions, offsetting early-stage cost drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Retained Primacy While Soft Services Accelerated

Hard services captured 58.75% of 2025 revenue, underpinning mission-critical mechanical, electrical and plumbing systems across harsh climates. Within this cohort, MEP and HVAC activities represented the largest slice as predictive-maintenance suites such as IBM Maximo trimmed procurement steps from 46 to 14 at Petroleum Development Oman, saving 2,300 hours annually. Asset owners locked multiyear contracts to safeguard LEED certifications and align with insurance stipulations.

Soft services, though smaller, posted the fastest expansion trajectory at 14.12% CAGR, buoyed by heightened hygiene, security and employee-experience standards in post-pandemic workplaces. Musanadah’s ISSA affiliation illustrated adoption of international cleaning protocols in Saudi hospitals. As flexible workspaces spread, demand for smart reception, barrier-less parking and app-based concierge surged. Catering subcontracts also shifted toward tech-enabled traceability, evidenced by Novotel’s seafood audit partnership across 19 hotels. Providers blending both service clusters under single SLAs achieved higher retention, driving integrated-model premiums.

By Offering Type: Outsourcing Strengthened Economies of Scale

Outsourced arrangements accounted for 61.15% of market revenue in 2025 and are forecast to advance 14.28% CAGR, validated by the King Abdullah Financial District’s decision to deploy IBM Maximo to supervise 100,000 assets across 94 structures and boost satisfaction to 95%. Clients cited cap-ex avoidance, technology access and regulatory compliance as prime motivations.

In-house teams persisted mainly within sovereign entities seeking direct control; however, even these adopted hybrid models for specialized data-center or energy-retrofit tasks. GCC facility management market share gains will likely compound in the outsourced cohort as municipal-service privatizations progress in Saudi Arabia and Kuwait.

By End-User Industry: Commercial Dominance Meets Industrial Momentum

Commercial real estate retained 29.85% of 2025 spending, propelled by Dubai retail hubs and new Riyadh CBD towers incorporating smart-parking rollouts via Parkin and Majid Al Futtaim. Tenant experience platforms linked HVAC, lighting and access control into occupant apps, elevating service-level baselines. .

Industrial and process facilities delivered the highest growth trajectory at 16.42% CAGR as governments accelerated manufacturing diversification. Emirates Global Aluminium’s Industry 4.0 lighthouse status highlighted digital-fleet maintenance delivering significant impact since its implementation. Demand for ISO 45001 safety compliance and predictive analytics fostered bundled FM packages integrating hard and soft scopes.

Geography Analysis

Saudi Arabia maintained 43.75% share in 2025, anchored by nearly USD 1 trillion city-building commitments under Vision 2030 that mandated full-life-cycle FM from design through operations. FMTECH’s establishment and the USD 7.2 billion King Salman Airport expansion amplified local capacity requirements. Providers aligning with localization and LEED Platinum standards secured early-stage master agreements. The GCC facility management market size attributable to Saudi Arabia is expected to double by 2030 as NEOM’s community zones enter operations.

The UAE held second rank through Dubai’s global-hub status and Abu Dhabi’s Estidama-driven sustainability codes. Smart-city pilots such as AI-enabled Al Shera’a HQ and barrier-less retail parking elevated service expectations. Government safety frameworks like OSHAD demanded certified providers, concentrating market power among high-capability firms. Large event venues and tourism complexes added seasonal load requiring flexible staffing models.

Qatar, Kuwait, Oman and Bahrain accounted for the balance, each exhibiting niche dynamics. Qatar’s World-Cup venues necessitated legacy-maintenance contracts, while Kuwait’s Vision 2035 pipeline spurred hospital and transport hubs. Oman’s oil-and-gas clusters leveraged cloud asset systems to standardize procurement. Bahrain’s financial district prioritized security-cleared soft-service personnel. Grid interconnection progress hinted at eventual harmonized FM standards, yet disparate labor and fire-safety rules still imposed compliance toggling for cross-border operators.

Competitive Landscape

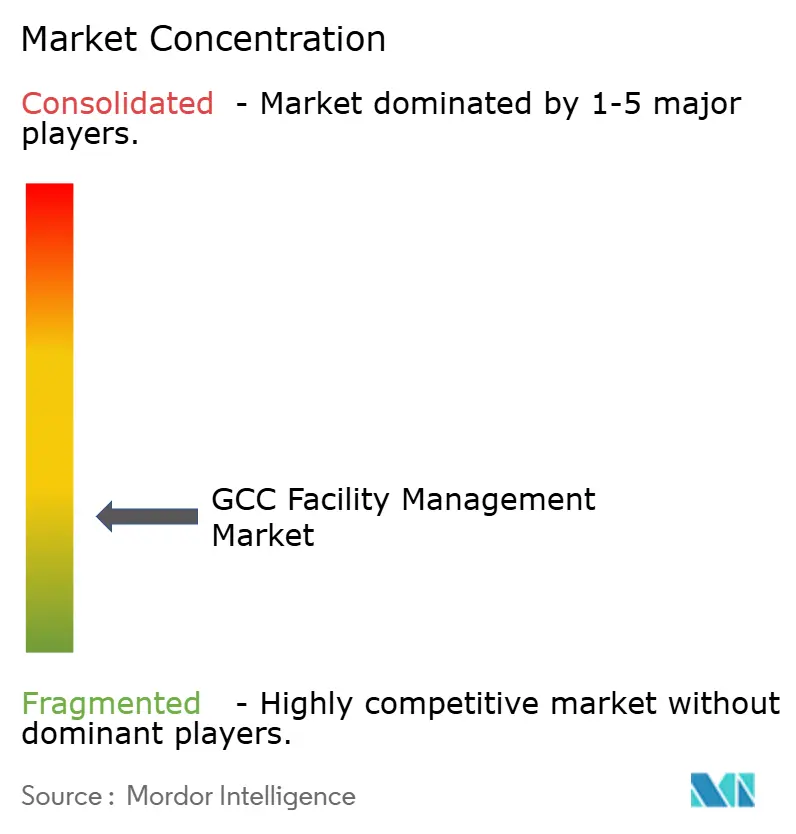

Market concentration remained moderate, shaped by international conglomerates and agile regional specialists. EMCOR Group, with USD 12.6 billion 2023 revenue, deepened Middle-East data-center capabilities via its USD 865 million Miller Electric acquisition announced January 2025. Sodexo and ISS leveraged global procurement and integrated-care models; the latter reported significant growth in Q2 2024, aided by contract wins that underscored margin resilience.

Regional champions such as Transguard, Farnek and Enova combined cultural fluency with tech investments. Farnek’s 2025 launch of an events-sector specialist highlighted vertical-market tailoring. Enova’s Google Cloud partnership showcased AI as a differentiator in service-ticket triage.

Strategic alliances, PPP frameworks, and capability-led M&A remained core growth levers. ADNH Catering increased its stake in Compass Arabia, pursuing scale in Saudi concessions. Landmark Group’s retail-expansion plan signaled downstream FM opportunities. As technology thresholds rose, niche HVAC, energy, and data-center specialists attracted acquisition interest from integrators aiming for end-to-end portfolios.

GCC Facility Management Industry Leaders

-

Emcor Facilities Services WLL

-

Sodexo Qatar Services

-

Al-Asmakh Facilities Management

-

G4S Qatar SPC

-

Cofely Besix Facility Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Disrupt-X and Tecpro Solutions partnered to expand the reach of ALEF 360°, an advanced real estate management platform, across the UAE and the broader Middle East, aligning with the growing demand in the GCC facility management market. Rebranded as Senzfy, the platform IoT integrated building management systems, facility and asset management, and energy monitoring into a unified solution.

- April 2025: Sulzer announced a strategic 10-year strategic partnership with Manweir WLL to deliver advanced repair and maintenance services for rotating equipment in Qatar. This collaboration, operating from Manweir’s state-of-the-art Ras Laffan facility, is designed to enhance service efficiency and reliability across the oil and gas, power, desalination, and industrial sectors.

- February 2025: iHorizons, headquartered in Doha, has entered into a strategic partnership with Service Works Global (SWG) Middle East to introduce advanced computer-aided facility management (CAFM) solutions across the GCC facility management market. This collaboration integrates iHorizons' expertise in digital innovation with SWG's specialization in CAFM technology to drive operational efficiency, optimize costs, and align with sustainability objectives.

- January 2025: ENGIE Solutions secured a three-year facilities management contract with DMCC for Uptown Tower in Dubai, a prominent development within the GCC facility management market. The agreement includes the provision of MEP, HVAC, and technical services for the LEED Gold-certified mixed-use tower. As part of the contract, ENGIE will implement its advanced Smart O&M platform, conduct comprehensive energy audits, and deliver specialized energy consultancy services to achieve a targeted 10% reduction in energy consumption.

GCC Facility Management Market Report Scope

Facility management services involve building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management and soft facility management spheres. Hard services comprise mechanical and electrical maintenance, fire safety and emergency services, building management systems controls, elevator/lifts, and conveyor maintenance, etc. Soft services include cleaning, recycling, security, pest control, handyman services, ground maintenance, waste disposal, etc.

The GCC facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others), and by country (Qatar, United Arab Emirates, Kuwait, Saudi Arabia, Oman, and Bahrain). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Country

| Qatar |

| United Arab Emirates |

| Kuwait |

| Saudi Arabia |

| Oman |

| Bahrain |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | Qatar | |

| United Arab Emirates | ||

| Kuwait | ||

| Saudi Arabia | ||

| Oman | ||

| Bahrain | ||

Key Questions Answered in the Report

What is the current value of the GCC facility management market?

The GCC facility management market size reached USD 79.99 billion in 2026.

How fast is the market expected to grow?

The market is forecast to register a 13.86% CAGR, pushing value to USD 153.08 billion by 2031.

Which service type generates the most revenue?

Hard services led with 58.75% revenue share in 2025, dominated by MEP and HVAC maintenance.

Why is outsourcing preferred in the region?

Outsourcing captured 61.15% share in 2025 because clients seek technology expertise, cost efficiency and compliance management offered by specialized providers.

Which end-user segment is growing the fastest?

Industrial and process facilities are projected to expand at a 16.42% CAGR as Saudi and UAE governments accelerate manufacturing diversification.

What is the biggest restraint facing facility managers?

Persistent skilled-labor shortages, intensified by nationalization quotas, are the most significant operational challenge across GCC states.

Page last updated on: