Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

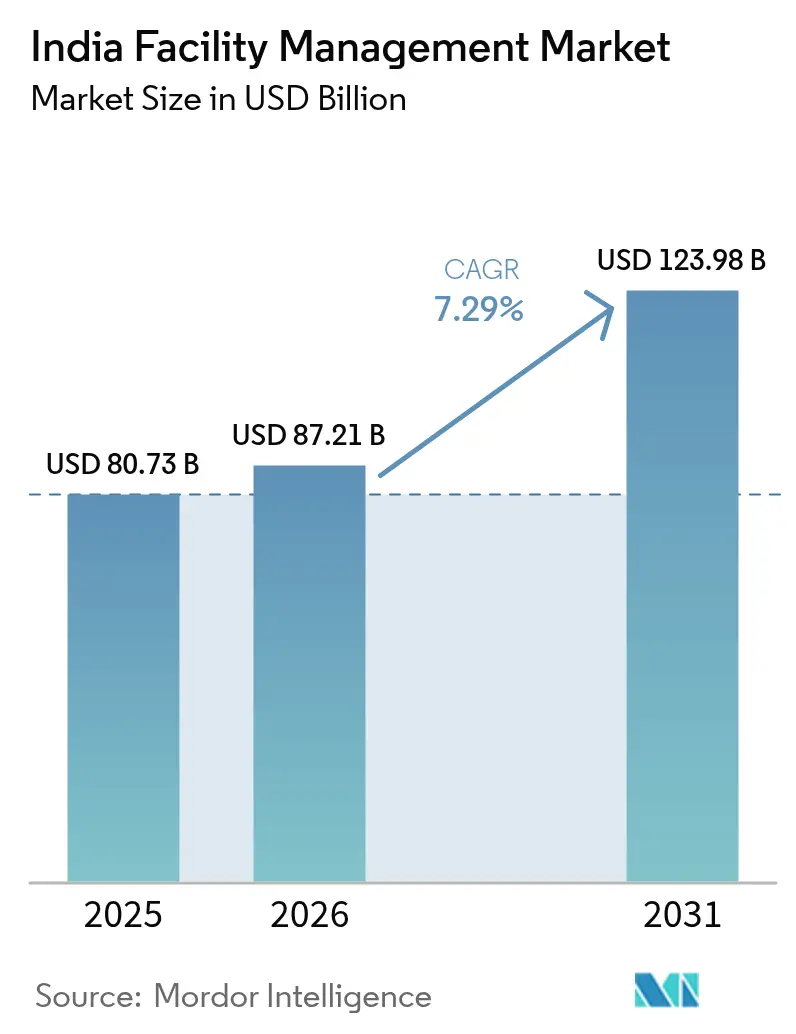

| Base Year Market Size (2025) | USD 80.73 Billion |

| Market Size (2026) | USD 87.21 Billion |

| Market Size (2031) | USD 123.98 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Facility Management Market Analysis by Mordor Intelligence

The India facility management market size is expected to increase from USD 87.21 billion in 2026 to reach USD 123.98 billion by 2031, growing at a CAGR of 7.29% over 2026-2031. Early adoption of predictive-maintenance platforms, sustainability-linked retrofits and integrated contracts is translating into larger average deal values. Grade A offices in technology corridors are running near capacity, which elevates demand for 24-hour mechanical, electrical and plumbing support, while semiconductor and electronics plants require cleanroom certification and uninterrupted power. Corporate landlords now embed energy-performance guarantees in service-level agreements, rewarding providers that invest in Internet of Things (IoT) sensors and analytics. At the same time, the Production Linked Incentive (PLI) scheme keeps industrial project pipelines full and expands the addressable pool for hard-services specialists.

Key Report Takeaways

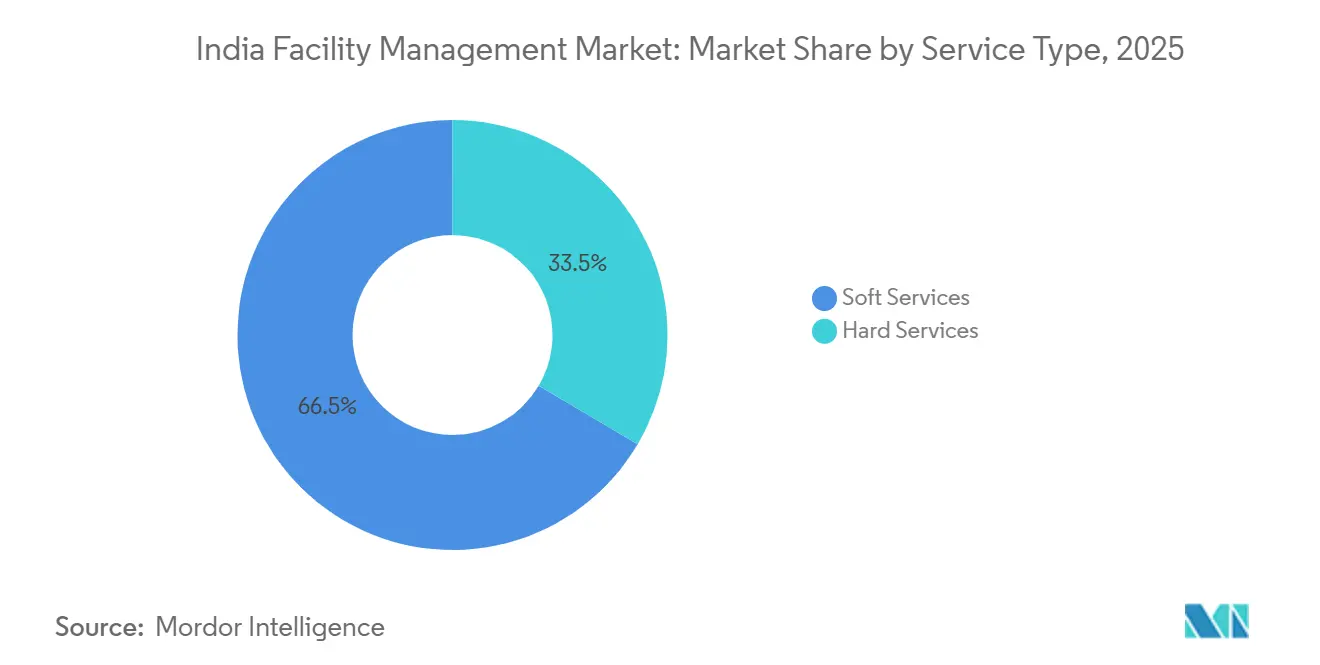

- By service type, soft services led with 66.52% of the India facility management market share in 2025. Hard services are projected to expand at an 8.37% CAGR through 2031, outpacing the India facility management market.

- By offering type, in-house models retained 67.56% share of the India facility management market size in 2025, but outsourced integrated contracts are growing at 9.03% annually.

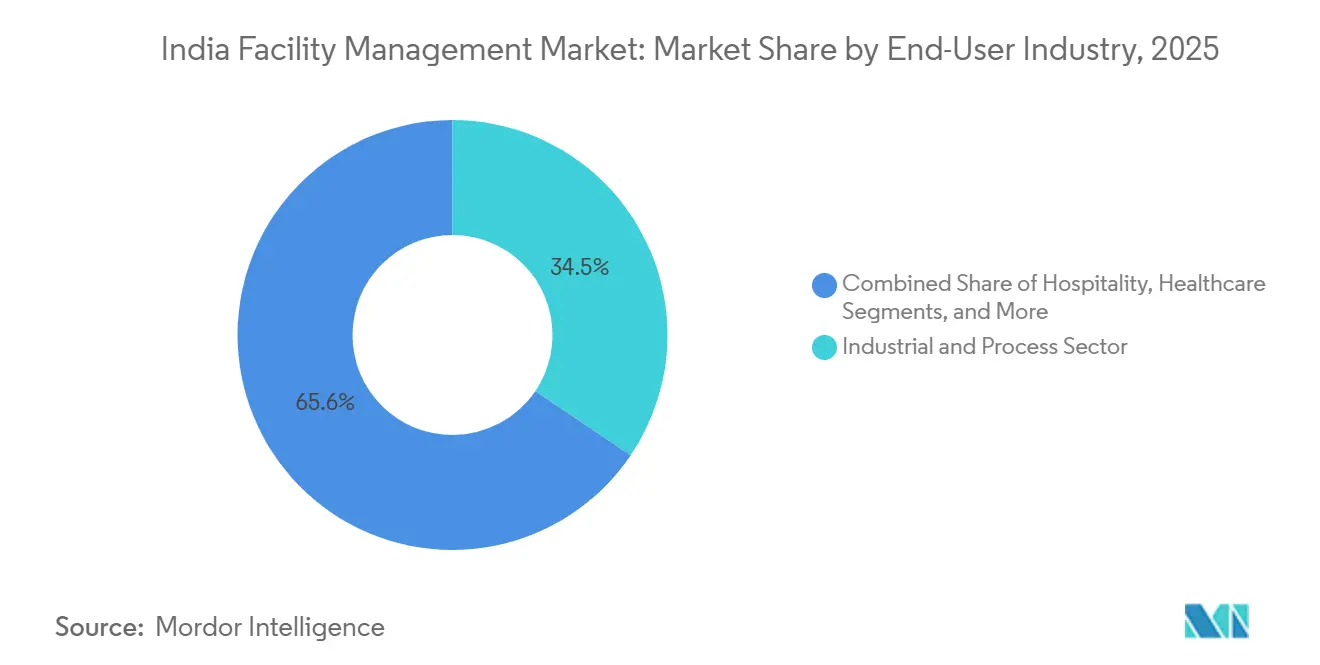

- By end-user, industrial facilities commanded 34.42% of 2025 revenue, while healthcare is advancing at a 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Commercial Real Estate Expansion | +1.8% | National, Concentrated In Bengaluru, Mumbai, Delhi NCR, Hyderabad, Pune, Chennai | Medium Term (2–4 Years) |

| Technology Integration, IoT, AI And Automation | +1.5% | National, Early Adoption In Metro And GCC Hubs | Long Term (≥ 4 Years) |

| Increasing Outsourcing Trend | +1.3% | National, Accelerating In Tier-2 Cities Such As Ahmedabad, Jaipur, Kochi, Chandigarh | Medium Term (2–4 Years) |

| Hygiene And Health Compliance Mandates | +1.0% | National, Heightened In Healthcare And Hospitality | Short Term (≤ 2 Years) |

| Uptake Of Outcome-Based FM Contracts In Tier-2 Cities | +0.8% | Tier-2 And Tier-3 Urban Centers | Medium Term (2–4 Years) |

| ESG-Linked Lending Driving Green Facility Upgrades | +0.7% | National, Led By BRSR-Compliant Corporates And IGBC-Certified Projects | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Rapid Commercial Real Estate Expansion

Developers completed more than 79 million sq ft of Grade A offices during 2025, keeping Bengaluru, Hyderabad and Pune below 13% vacancy. New-build specifications call for smart meters, LEED or IGBC certification and fire-safety systems aligned with the National Building Code 2016.[1]“India Office Market Overview,” CBRE, cbre.co.in Facility managers therefore handle round-the-clock HVAC optimization, periodic fire-audits and predictive analytics that minimize downtime. Flexible workspace operators added capacity in core micro-markets, creating variable daily occupancy that drives use of occupancy sensors and space-utilization dashboards.[2]“Office Leasing and Real Estate Trends,” JLL India, jll.co.in Collectively, these trends push bundled hard-and-soft contracts to the forefront of landlord strategy. Providers that can integrate mechanical, cleaning, security and energy services under performance-linked fees win longer tenures and higher margins.

Technology Integration, IoT, AI and Automation

IoT sensors now track temperature, vibration and power in more than 500 million sq ft of commercial and industrial space, feeding cloud platforms that flag anomalies well before failure.[3]“Building Automation and Smart Building Solutions,” Johnson Controls, johnsoncontrols.com Artificial intelligence tools evaluate historical work orders and asset telemetry, enabling maintenance interventions that cut unplanned downtime by up to 30%. Digital twins simulate refurbishments and renewable-energy additions to guide capex decisions. The Securities and Exchange Board of India (SEBI) asked the top 1,000 listed firms to disclose energy-use data, so clients can increasingly demand real-time dashboards. Service providers able to connect building-management software with enterprise resource planning platforms gain competitive insulation.

Increasing Outsourcing Trend

Integrated facility management (IFM) contracts expanded 9.03% in 2025 as chief financial officers sought variable-cost structures and single-vendor accountability. Outcome-based terms now appear in roughly one-quarter of new awards, tying payments to uptime and energy savings. Secondary cities such as Kochi, Ahmedabad and Jaipur, which host new GCC sites, often have no legacy facility teams, so they outsource from day one. Tier-2 penetration of IFM is therefore running ahead of metro levels. Higher contractual risk pushes incumbents to invest in staff training, technology platforms and command centers, raising the capital bar for newcomers.

Hygiene and Health Compliance Mandates

Post-pandemic rules require daily sanitization of high-touch surfaces and continuous indoor-air monitoring in healthcare and hospitality. Hospitals under the Ayushman Bharat Health Infrastructure Mission must demonstrate such compliance to secure federal funding, fuelling demand for certified cleaning, biomedical-waste handling and 24-hour HVAC oversight. Commercial landlords in Mumbai, Bengaluru and Delhi NCR adopt similar hygiene scores to reassure multinational tenants. Hotels deploy touchless check-in and antimicrobial coatings, lifting technical complexity. Vendors that certify staff under ISO 9001 and ISO 45001 gain pricing power while low-skill outfits face erosion.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages And Skill Gaps | -1.2% | National, Acute In Metros With High Attrition | Short Term (≤ 2 Years) |

| Margin Pressure From Rising Operational Costs | -1.0% | National, Pronounced In Labor-Intensive Soft Services | Short Term (≤ 2 Years) |

| High Client Price Sensitivity And Fragmented Procurement Practices | -0.6% | National, Severe In Public Sector And SME Segments | Medium Term (2–4 Years) |

| Smart-Building Automation Reducing Manned-Guarding Demand | -0.4% | National, Early Impact In New Grade A Offices | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Labour Shortages and Skill Gaps

Metro attrition in housekeeping and guarding exceeded 40% in 2025 as workers jumped to e-commerce and gig platforms. Technical trades show deeper deficits: vocational institutes graduate fewer than 50,000 HVAC and BMS technicians against 150,000 annual demand. Providers therefore run academies and apprenticeship programs, lifting recruitment costs and elongating ramp-up times. Wage inflation of 10%-12% compresses margins when contracts lack automatic escalation clauses. Some firms pilot remote monitoring to cut site headcount, but regulations and client preferences for physical presence still limit scale.

Margin Pressure from Rising Operational Costs

Diesel for backup generators rose 8% year-over-year in 2025, cleaning chemicals by 6%-10% and insurance premiums by up to 15%.[4]“Input Cost Inflation Squeezes FM Margins,” Business Standard, business-standard.com Yet public-sector undertakings and small businesses hold rates flat, forcing vendors to absorb the increases. Fragmented tendering, each building issues separate bids, prevents scale benefits in consumables and staffing. Lowest-price procurement clauses further erode profitability. Larger groups cross-subsidize thin-margin contracts with advisory services, whereas mid-tier specialists lack diversification and struggle to invest in technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Outpace Soft on Technology Tailwinds

Hard services generated faster growth than the overall India facility management market, expanding at an 8.37% CAGR thanks to mandatory compliance and energy-saving retrofits. The National Building Code 2016 obliges fire-detection and suppression in high-rise assets, spurring retrofit programs across older stock. Bureau of Energy Efficiency (BEE) codes encourage chiller replacement and variable-frequency drives that trim consumption by up to 35%. Consequently, institutional landlords deploy condition-based monitoring suites, creating sticky recurring revenue anchored to the India facility management market size.

Soft services still delivered 66.52% of 2025 revenue by virtue of daily cleaning, office support and guarding. However, manned-security posts are falling as access control and video analytics spread, particularly in new Grade A offices, reducing guard density by almost one-third. Cleaning moves toward rope-access facade works and post-construction deep cleans that command premiums. Catering digitizes menus and tracks waste to satisfy wellness targets. Fragmentation persists, constraining economies of scale, but niche operators carve profit in specialized disinfection or linen sterilization.

By Offering Type: Outsourcing Gains as Outcome Models Mature

Integrated facility management, which bundles multiple service lines, is the fastest rising slice of the India facility management market size, growing 9.03% annually. Multinationals favor IFM for single invoicing and data transparency; payments hinge on uptime or energy-saving metrics, deepening engagement length. Vendors must therefore deploy IoT gateways, mobility apps and centralized command centers. Bundled deals combining two or three services remain popular in Tier-2 cities, bridging clients from single-line outsourcing toward full integration.

Despite the shift, in-house models still represented 67.56% of 2025 revenue because many public agencies and conglomerates view facilities as strategic. Security-sensitive functions or GMP-driven assembly lines keep staffing internal to safeguard compliance. Yet talent scarcity and the opportunity cost of capex stored in non-core assets push several conglomerates to externalize gradually, often beginning with single-service pilots such as housekeeping before graduating to bundled portfolios

By End-User Industry: Healthcare Surges on Infrastructure Push

Healthcare is the fastest advancing vertical at a 9.42% CAGR, underpinned by the rollout of 1.5 lakh Health and Wellness Centres and critical-care blocks that need infection control, biomedical-waste segregation and ISO-certified HVAC routines. Private chains added up to 18,000 beds in 2025 and outsource non-clinical operations for cost efficiency and audit traceability. Pharmaceutical plants built under the PLI scheme adopt ISO Class 5-8 cleanrooms and continuous particulate monitoring, anchoring high-value long-term contracts.

Industrial and process facilities contributed 34.42% of 2025 revenue, the largest slice of the India facility management market share. Semiconductor fabs, electronics lines and automotive clusters demand uninterrupted power and ISO 14001 and ISO 45001 compliance. Commercial real estate, especially GCC-dominated offices, retains a robust pipeline, while hospitality saw occupancy rebound to 68%-70% in 2025, boosting need for guest-experience housekeeping. Institutional campuses and transport hubs offer volume but low margins due to price-sensitive tendering.

Geography Analysis

Metros, Bengaluru, Mumbai, Delhi NCR, Hyderabad, Pune and Chennai, accounted for roughly two-thirds of 2025 facility-management revenue. Bengaluru alone leased close to 20 million sq ft of offices, driving requirement for constant HVAC runtime and BMS analytics. Mumbai’s premium districts recorded 8%-10% rent growth, prompting landlords to adopt IFM to safeguard asset value. Delhi NCR added between 12 million and 14 million sq ft, with professional-services occupiers insisting on bundled contracts.

Tier-2 cities such as Ahmedabad, Jaipur, Kochi and Chandigarh are rising fast, posting 15%-18% leasing growth in 2025 and offering greenfield opportunities for the India facility management market. Outcome-based contracts already make up one-third of awards here, higher than the national average, because occupants lack legacy staff and demand turnkey engagement. However, procurement remains price driven and margins thinner.

Central and state Smart Cities Mission budgets inject funds for command-and-control centers, energy-efficient public buildings and integrated transport nodes. These projects demand BMS integration and preventive-maintenance regimes aligned to ISO 50001, distributing India facility management market revenues beyond the six metros.

Competitive Landscape

Top 10 players captured about 35%-40% of 2025 revenue, indicating moderate concentration. Multinationals ISS and Sodexo compete with domestic groups Quess, BVG India and Dusters Total, while real-estate advisers CBRE, JLL and Knight Frank cross-sell IFM alongside brokerage. Technology stands out as a differentiator: ISS opened a USD 15 million command center in Mumbai for remote asset monitoring. CBRE launched a healthcare vertical with Apollo Hospitals, installing IoT BMS across 2.5 million sq ft.

Quess, the largest domestic employer, reported INR 5,451 crore (USD 654 million) revenue in Q2 FY25, with double-digit growth in IFM. BVG India won state hospital contracts for HVAC monitoring and biomedical waste. Knight Frank bought a Pune-based industrial FM firm, adding 10 million sq ft of managed space.

Emerging disruptors deploy proprietary IoT devices, AI analytics and tenant apps. Yet capital demands and data-integration concerns limit scale for pure-tech entrants, favoring hybrids that blend digital platforms with on-ground execution. Vendors race to embed ESG measurement dashboards to align with SEBI’s Business Responsibility and Sustainability Reporting, a capability now central in RFP scoring.

India Facility Management Industry Leaders

ISS Facility Management

Sodexo Facilities Management Services India Pvt. Ltd.

Quess Corporation

Updater Services Pvt. Ltd.

BVG India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Quess Corporation secured INR 250 crore (USD 30 million) in multi-year Tier-2 IFM contracts covering Ahmedabad, Jaipur and Kochi.

- December 2025: CBRE South Asia set up a dedicated healthcare vertical with Apollo Hospitals across 15 facilities.

- November 2025: JLL India landed a 5-year, INR 180 crore (USD 21.6 million) IFM deal for 3 million sq ft in Bengaluru, Hyderabad and Pune.

- October 2025: ISS Facility Services invested USD 15 million in a Mumbai command center enabling 24-hour remote oversight.

India Facility Management Market Report Scope

Facility Management encompasses various disciplines ranging from complex services such as physical structure services, lifts, etc., to soft benefits such as human interaction, cleaning, etc. FMs contribute to the business's bottom line through their responsibility for often maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation. The objective of professional FM as an interdisciplinary business function is to coordinate the demand and supply of facilities and services in public and private organizations. The Indian market for outsourcing such facilities is expected to grow over the coming years, owing to the organization's efforts to concentrate on the core process growth.

The India Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare (Public Facilities, Private Facilities) |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare (Public Facilities, Private Facilities) | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large will facilities outsourcing become in India by 2031?

Outsourced integrated contracts are forecast to reach nearly one-third of the India facility management market by 2031, expanding at 9.03% annually as corporations shift from in-house delivery.

Which end-user vertical is set to grow the fastest?

Healthcare facilities, boosted by the Ayushman Bharat Health Infrastructure Mission, are advancing at a 9.42% CAGR through 2031, outpacing all other segments.

What role does technology play in Indian FM contracts?

IoT sensors, AI analytics and digital twins now underpin outcome-based agreements, helping providers commit to 99.5% uptime and double-digit energy savings.

Why are hard services growing quicker than soft services?

Regulatory fire-safety retrofits, energy-efficiency mandates and predictive-maintenance adoption drive an 8.37% CAGR for hard services, above the market average.

Which cities outside the six metros offer expansion potential?

Tier-2 hubs such as Ahmedabad, Jaipur, Kochi and Chandigarh show 15%-18% office-leasing growth, making them prime targets for new integrated FM contracts.

How is ESG influencing vendor selection?

Corporates subject to SEBI sustainability reporting favor providers that supply real-time carbon dashboards and ISO 50001 advisory, boosting demand for green FM capabilities.

Page last updated on: