Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

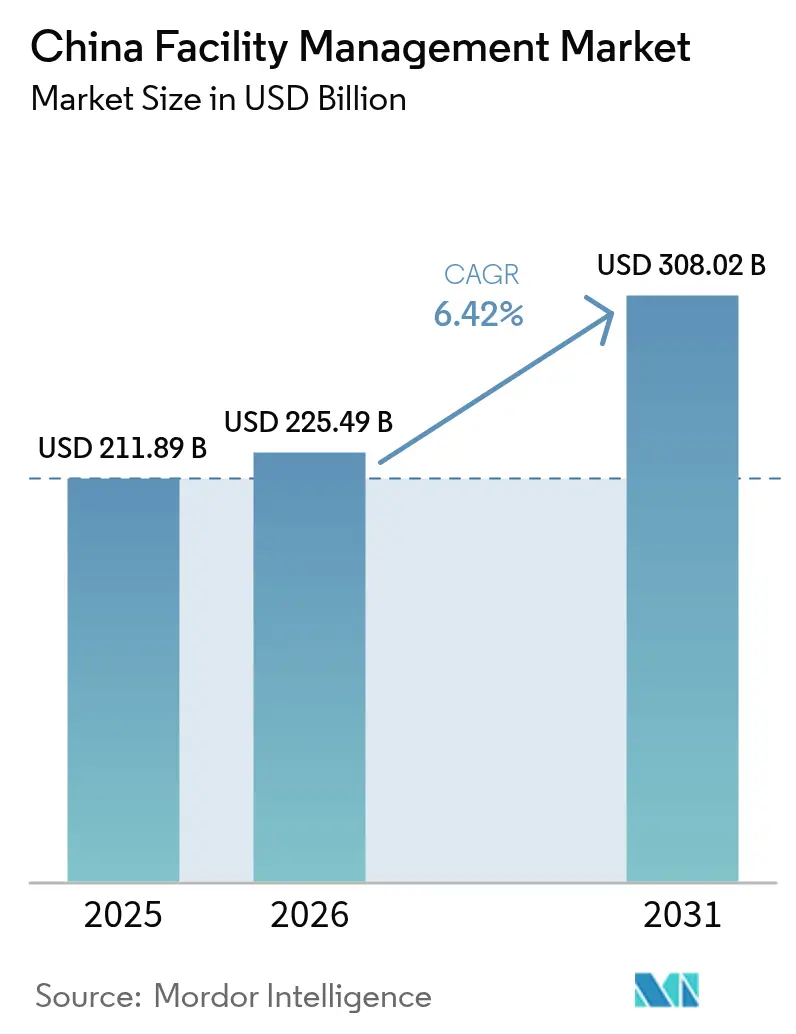

| Base Year Market Size (2025) | USD 211.89 Billion |

| Market Size (2026) | USD 225.49 Billion |

| Market Size (2031) | USD 308.02 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

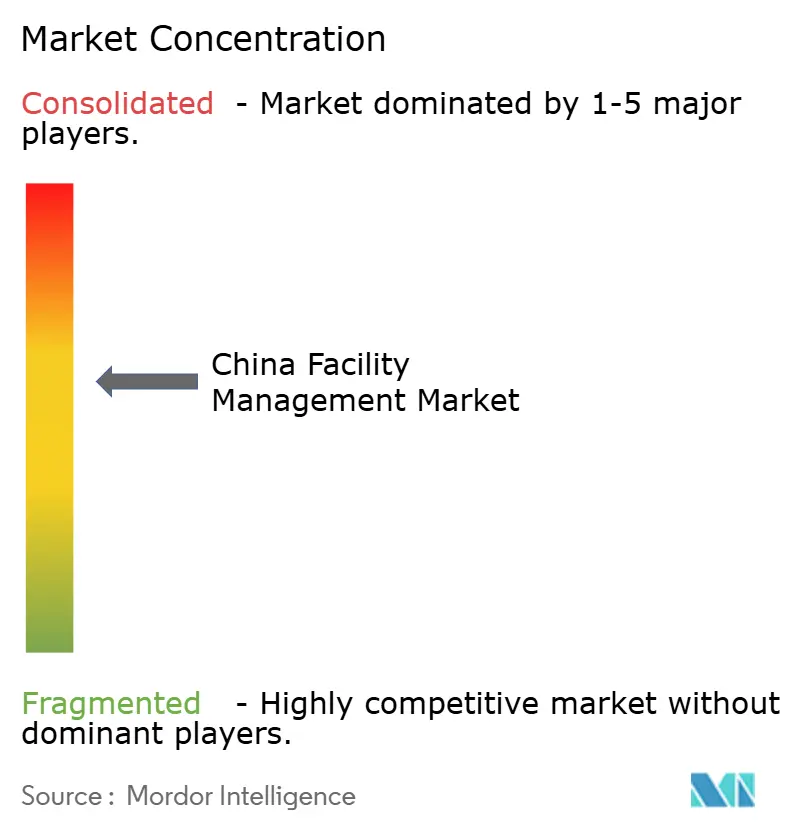

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Facility Management Market Analysis by Mordor Intelligence

The China facility management market size is expected to grow from USD 211.89 billion in 2025 to USD 225.49 billion in 2026 and is forecast to reach USD 308.02 billion by 2031 at 6.42% CAGR over 2026-2031. Growth is underpinned by state-owned enterprises (SOEs) accelerating outsourcing, commercial landlords embracing smart-building technologies, and expanding demand for ESG-compliant services. Tier-2 and tier-3 cities are becoming powerful growth nodes, even as the real-estate debt crisis limits new supply in the short term. Bundled and integrated contracts now outpace single-service agreements as clients pursue outcome-based procurement. Technology-enabled, energy-efficient solutions are reshaping competitive positioning, while in-house teams at large tech firms create selective substitution risk. Fragmentation persists, yet the quest for scale and digital capability is nudging the China facility management market toward gradual consolidation.

Key Report Takeaways

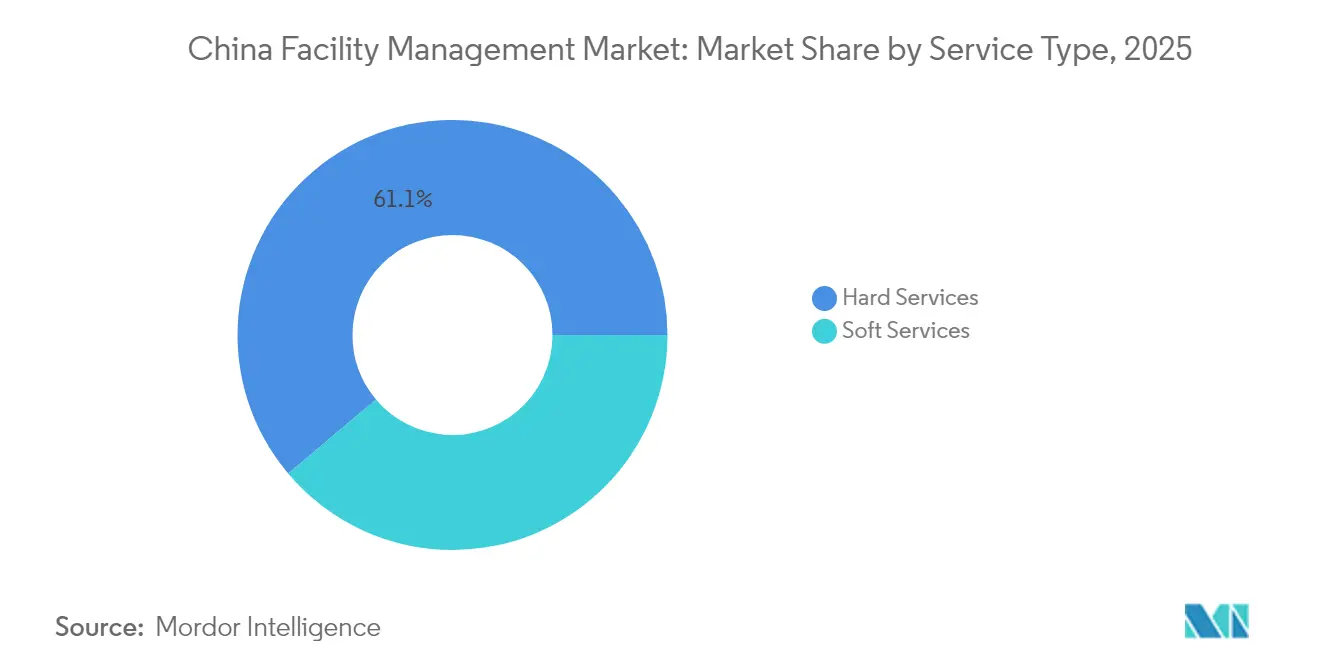

- By service type, hard services led with 61.15% revenue share in 2025; soft services are on track to post a 7.18% CAGR through 2031.

- By offering type, the outsourced segment accounted for 68.25% of the China facility management market share in 2025, while its blended growth is projected at a 6.63% CAGR to 2031.

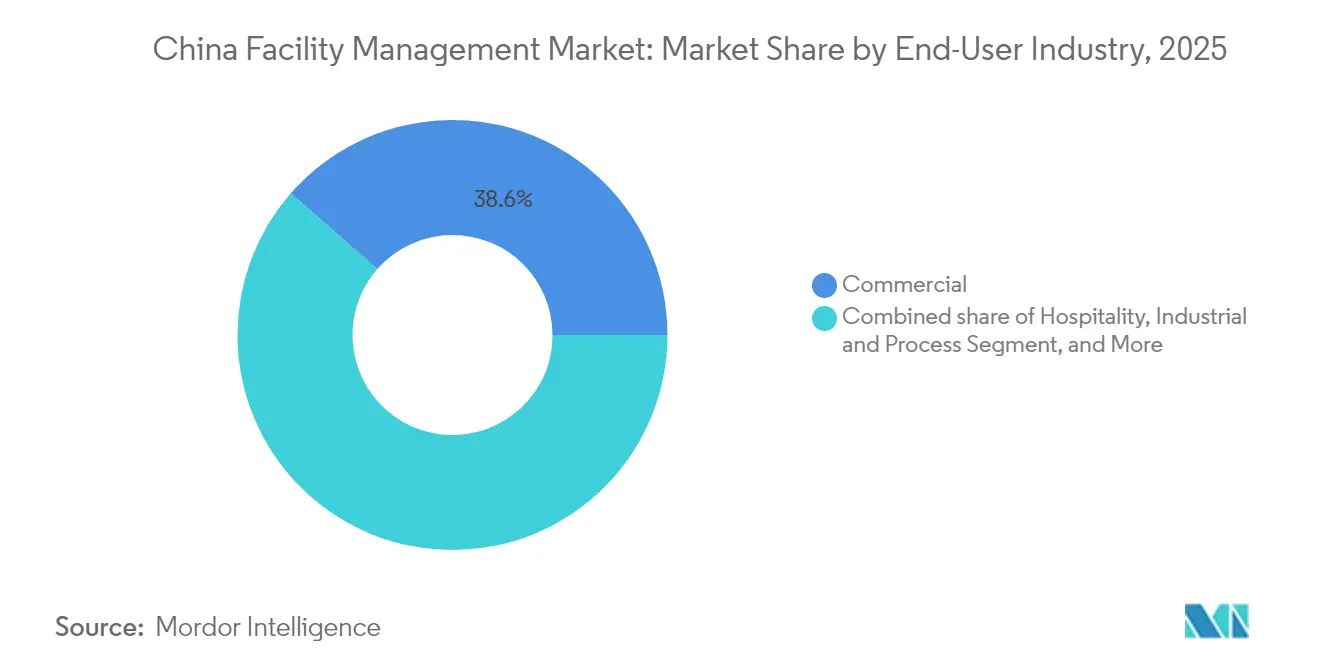

- By end-user industry, commercial facilities captured 38.55% of the China facility management market size in 2025; industrial and process sites are expected to expand at a 7.46% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing momentum among SOEs | +1.2% | Beijing, Shanghai, Guangzhou | Medium term (2-4 years) |

| Smart-building and IoT adoption | +1.8% | Tier-1 expanding to tier-2 | Long term (≥ 4 years) |

| Growth in green-certified stock | +1.1% | Nationwide metros | Long term (≥ 4 years) |

| Tier-2 and tier-3 CRE expansion | +0.9% | Central and Western hubs | Medium term (2-4 years) |

| Mixed-ownership reform of public assets | +0.7% | National | Medium term (2-4 years) |

| E-commerce cold-chain logistics | +0.8% | Coastal corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing Adoption Among State-Owned Enterprises

Central SOEs booked profits of CNY 2.6 (USD 0.36) trillion and revenue of CNY 39.8 (USD 5.51) trillion in 2024, freeing capital to concentrate on strategic priorities while outsourcing non-core operations. Stock-performance-linked oversight heightened pressure on operational efficiency, prompting a steady flow of bundled contracts to professional providers. The State-owned Assets Supervision and Administration Commission (SASAC) aligns outsourcing policy with national goals, giving the China facility management market a predictable pipeline from SOE portfolios. [1]State-owned Assets Supervision and Administration Commission of the State Council (SASAC), http://en.sasac.gov.cn/ Medium-term growth is reinforced as more provincial SOEs replicate the central blueprint in transport, energy, and telecom estates.

Integration of Smart Building Technologies and IoT-Driven Predictive FM

AI-enabled building-management systems cut energy use and carbon emissions by up to 30% in large office towers, while IoT diagnostics achieve 97% fault-identification accuracy. Property technology firms deploy more than 10,000 sensors in flagship complexes, slashing labor cost by 62%. Generative AI tools even redesign plant layouts to meet Industry 4.0 workflows, shrinking installation lead-time and downtime. As tenants equate indoor-environment quality with talent retention, the China facility management market sees premium pricing for providers offering end-to-end digital twins, cloud dashboards, and data-driven energy retrofits.

Growth of Green Building Stock Driving Demand for Energy-Efficient FM

China hosts 3,620 LEED-certified projects and over 25,000 domestic Three-Star green buildings, many mandated to meet Basic Grade codes by 2025. [2]GBCI, "1,563 LEED green building projects, representing more than 24 million gross square meters (GSM) of space, were LEED-certified in Mainland China" https://www.gbci.org/, Facility operators must deliver measurable resource savings across energy, water, and waste, driving adoption of advanced metering, recommissioning, and renewable micro-grids. ESG-linked financing further rewards landlords that partner with sustainability-focused vendors. The China facility management market therefore prizes certifications such as WELL, RESET, and ISO 14001 as differentiators during tendering.

Expansion of Commercial Real Estate in Tier-2 and Tier-3 Chinese Cities

Urbanization reforms elevate cities like Chengdu (population 20.93 million in 2023) and Chongqing as alternative corporate hubs where grade-A stock is still affordable. [3]https://www.britchamswchina.org/chengdu/ Municipal transport upgrades and newly liberalized land-use rules propel office, logistics, and retail construction pipelines. Early movers among facility firms lock in multi-year integrated contracts, positioning cross-selling as occupiers scale. The shift diversifies revenue away from saturated tier-1 markets, mitigating vacancy-rate pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-estate debt overhang | -0.9% | Nationwide metros | Short term (≤ 2 years) |

| In-house FM at tech majors | -0.6% | Tier-1 tech clusters | Medium term (2-4 years) |

| Fragmented fire-safety codes | -0.4% | Cross-province sites | Long term (≥ 4 years) |

| Carbon-audit cost under ETS | -0.3% | Heavy-industry belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Real-Estate Debt Crisis Limiting New Facility Supply and Renovation Budgets

Major developers such as China Vanke reported USD 6.2 billion losses, and commercial deals slid to USD 38.6 billion in 2024 from USD 60.3 billion in 2021. Distressed-asset sales at steep discounts divert capital from refurbishment, compressing FM budgets. Providers face intensified price negotiations, especially in offices where vacancies exceed 21% in Beijing. Short-term headwinds will be eased only after balance-sheet repair unlocked construction starts

Rising Competition from In-House FM Teams of Large Technology Conglomerates

Tencent bought 70,601 m² in Beijing for CNY 6.42 (USD 0.86) billion and Alibaba opened a 470,000 m² campus, both staffed by proprietary FM divisions. Tech giants integrate AI building analytics with corporate IT stacks, creating high entry barriers for external vendors. Outsourced specialists respond by focusing on multi-tenant assets and industries where neutrality and compliance outweigh data-sovereignty concerns

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Retain Scale, Soft Services Outpace

Hard services contributed 61.15% of the China facility management market in 2025 due to mandatory life-safety and MEP upkeep under GB 55037-2022 fire code. Demand clusters around HVAC retrofits, asset reliability, and statutory inspections. Soft services, projected at a 7.18% CAGR to 2031, gain from heightened post-pandemic hygiene standards, agile workplace support, and AI-enabled energy stewardship that delivered annual savings of CNY 1.25 million in pilot malls. With ESG disclosures expanding, soft-service vendors now bundle waste diversion and catering carbon-tracking as premium add-ons. As a result, the China facility management market size for soft services is on a steeper trajectory than its hard-services counterpart

By Offering Type: Outsourced Dominance with Integrated Models Ascending

Outsourced contracts captured 68.25% of the China facility management market share in 2025 and are on course for a 6.63% CAGR through 2031, reflecting client focus on core-business differentiation. Single-service agreements still prevail in smaller assets, but bundled and fully integrated FM increasingly win corporate and public-sector tenders where total lifecycle cost of ownership guides procurement. Integrated FM solutions improve governance by consolidating KPIs across safety, sustainability, and occupant experience. Conversely, the in-house share remains 31.75%, held mainly by tech and heavy-industry owners prioritizing data control. The cost-to-serve for advanced analytics favors scale operators, reinforcing future outsourcing momentum in the China facility management market.

By End-User Industry: Commercial Sector Leads, Industrial Segment Accelerates

Commercial facilities including offices, data centers, and omnichannel retail, accounted for 38.55% of 2025 revenue. Corporate occupiers chase differentiated tenant experience as a lever to reduce high vacancy, especially in Shanghai where speculative grade-A supply keeps rents negotiable. The industrial and process segment is forecast to grow at 7.46% CAGR, propelled by cross-border e-commerce and a cold-chain logistics market already valued at CNY 339.1 billion. Temperature-controlled warehouses, semiconductor fabs, and battery plants rely on stringent GMP-style protocols, offering rich wallet-share for FM specialists versed in ISO 50001 energy management.

Geography Analysis

Eastern provinces remain the revenue anchor, buoyed by Shanghai’s 152,460 m² of net office absorption and 343,500 m² in retail take-up during Q3 2024. Mature infrastructure and multinational tenancy support sophisticated scopes—energy dashboards, WELL-certified fit-outs, and 24/7 command centers—allowing premium fees. South-Central locales led by Chengdu post the highest forward CAGR as population inflow, low real-estate cost, and policy incentives attract head-office relocations. New supply triggers early outsourcing of cleaning, security, and MEP under multi-year contracts, boosting the China facility management market size in interior basins.

The Northwest and Southwest corridors register rapid growth under the Western Development Strategy that funnels public-works capex into photovoltaics, high-speed rail, and logistics hubs. Local authorities embed green-building benchmarks in tenders, benefitting firms armed with ISO 45001 safety credentials and carbon-footprint calculators. North and Northeast markets, although mature, still offer stable demand as political and financial institutions in Beijing uphold quality benchmarks that ripple through vendor selection.

Competitive Landscape

The landscape stays moderately fragmented: the top five players represent under 40% of total revenue, yet concentration is inching upward as clients consolidate supplier panels. Global majors such as CBRE logged 16% year-over-year FM revenue growth in Q1 2025 and deepened their domestic footprint by merging a USD 3 billion project-management arm with Turner & Townsend. [4]CBRE Group, Inc. "Reports Financial Results for First-Quarter 2025" https://ir.cbre.com/press-releases/detail/250/cbre-group-inc-reports-financial-results-forCushman & Wakefield likewise surpassed earnings targets by sharpening sector specialization in data centers and life sciences. Domestic giants Onewo Space-Tech and China Shine leverage cost agility and local-government networks, while ISS and Sodexo pursue tuck-in acquisitions—Sodexo’s 2025 purchase of Compass China businesses expands its food-service-linked integrated FM reach. Success increasingly hinges on IoT platforms, energy-optimization algorithms, and ESG reporting dashboards, differentiating leaders in the China facility management market.

China Facility Management Industry Leaders

-

Leadec Industrial Services (Shanghai) Co., Ltd.

-

Sodexo China

-

ESG Holdings Limited

-

Aeon Delight Co., Ltd.

-

CBRE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aden Services has formed a strategic IFM partnership with TotalEnergies to manage its 35,000 sqm China headquarters. Services include cleaning, maintenance, landscaping, and hygiene, all powered by Aden’s digital twin platform for smart oversight and performance tracking. This collaboration highlights a shared commitment to sustainability and innovation in workplace management, setting a new benchmark for IFM in China.

- May 2025: JLL has launched JLL Property Assistant, an AI-driven solution built on the JLL Falcon platform to boost performance across retail, industrial, and office properties. Seamlessly integrating with platforms like Yardi, MRI, and Prism, it delivers real-time insights through a natural language interface. Designed to streamline operations and improve decision-making, the assistant is poised to redefine standards in facility and asset management.

- January 2025: Sodexo agreed to acquire Compass subsidiaries in mainland China, consolidating its catering-driven FM portfolio.

- January 2024: CBRE confirmed plans to combine its project-management unit with Turner & Townsend, building a USD 3 billion revenue platform for infrastructure and green-energy projects.

China Facility Management Market Report Scope

The China facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the forecast size of the China facility management market by 2031?

The China facility management market size is projected to reach USD 308.02 billion by 2031, reflecting a 6.42% CAGR from 2026.

Which service category is growing fastest?

Soft services—covering cleaning, security, catering, and office support—are forecast to grow at 7.18% CAGR through 2031, outpacing hard-service categories.

Why are tier-2 and tier-3 cities important for facility management providers?

These cities exhibit rapid commercial-real-estate expansion and favorable cost structures, offering early-mover advantages to providers that build local operations.

Who leads the competitive landscape?

Global players including CBRE, Cushman & Wakefield, ISS, and Sodexo hold sizeable shares, while domestic leaders like Onewo Space-Tech and China Shine compete on local networks and cost.

Page last updated on: