Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.21 Billion |

| Market Size (2026) | USD 11.40 Billion |

| Market Size (2031) | USD 12.95 Billion |

| Growth Rate (2026 - 2031) | 2.57% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia packaging market size is projected to be USD 11.21 billion in 2025, USD 11.40 billion in 2026, and reach USD 12.95 billion by 2031, growing at a CAGR of 2.57% from 2026 to 2031. Corrugated and flexible formats are expanding quickly because e-commerce logistics handled 101 million delivery orders in Q2 2025, while traditional retail packaging demand is flat. Shelf-life labeling reforms that require Arabic-language disclosure are accelerating adoption of high-barrier multilayer films. Localization incentives embedded in Vision 2030 are drawing multinational fast-moving consumer goods (FMCG) producers to build Saudi plants, which tightens local supply and stimulates backward integration among converters. Rising resin input costs and paper-based substitution trends are reshaping material preferences, resulting in a measured but structurally significant pivot toward fiber-based and recyclable solutions.

Key Report Takeaways

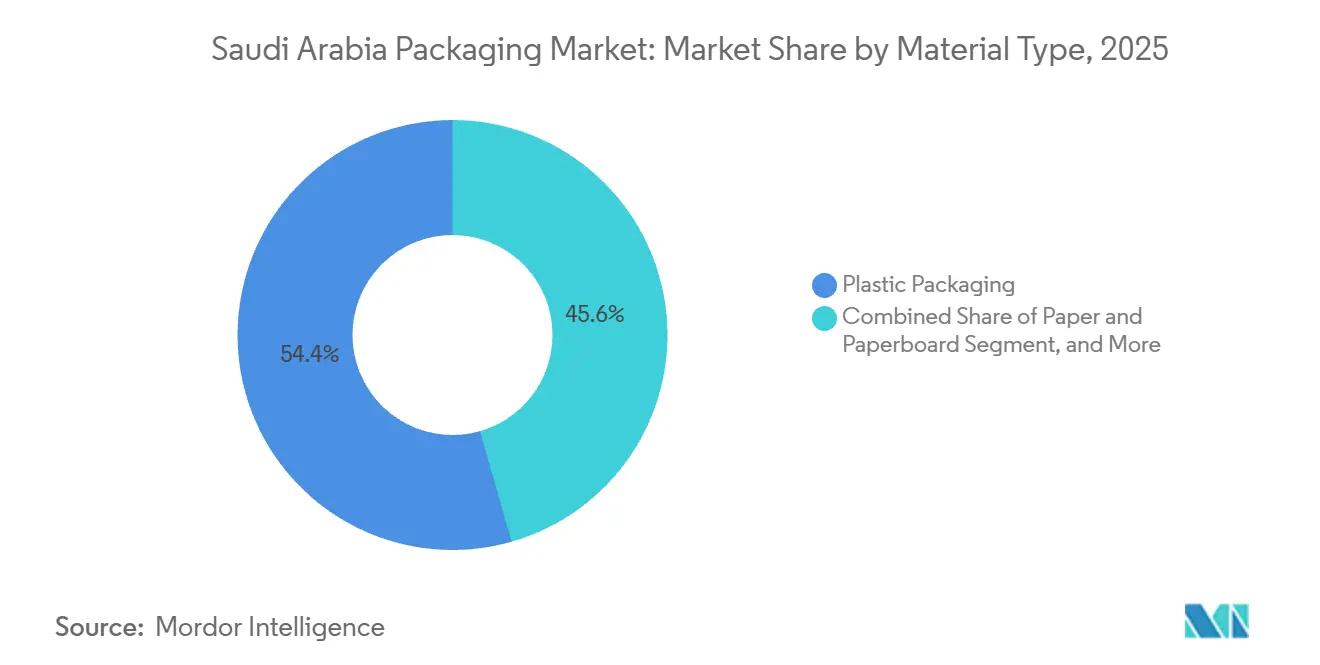

- By material type, plastic packaging held 54.44% of market share in 2025, but paper and paperboard is projected to expand at a 3.43% CAGR through 2031.

- By product type, flexible packaging formats captured 35.66% of the market share in 2025, whereas single-use paper products are forecast to grow at a 3.83% CAGR to 2031.

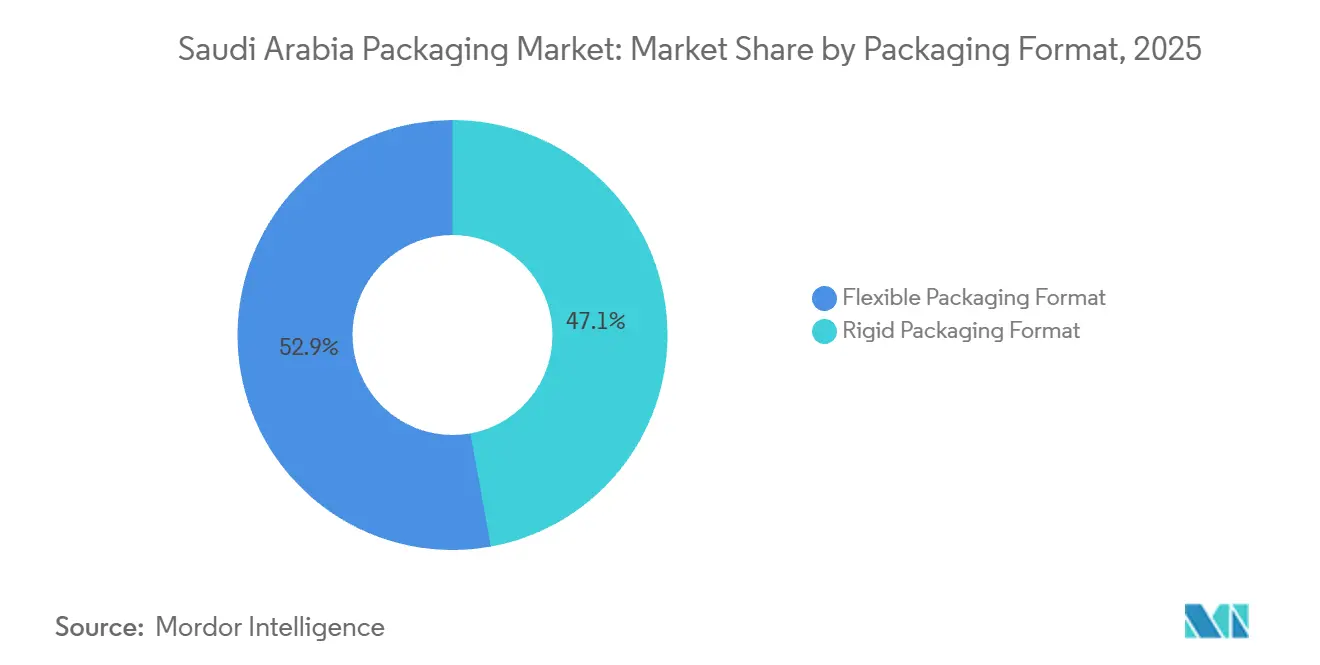

- By packaging format, flexible format accounted for 52.86% of the Saudi Arabia packaging market share in 2025 and will rise at a 3.52% CAGR through 2031.

- By end user, food commanded 27.48% share of the Saudi Arabia packaging market size in 2025, while personal care and cosmetics are advancing at a 3.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom Driving Corrugated and Last-Mile Formats | +0.8% | Riyadh, Jeddah, Dammam metro areas | Short term (≤ 2 years) |

| Mandatory Shelf-Life Labeling Reforms (SFDA) | +0.5% | National food and beverage sector | Medium term (2-4 years) |

| Vision 2030 Localization Incentives | +0.6% | Jubail, Yanbu, Ras Al Khair clusters | Medium term (2-4 years) |

| Rapid Growth of Ready-To-Eat Meal Services | +0.3% | Major urban centers | Short term (≤ 2 years) |

| GCC-Wide Deposit-Return Initiatives | +0.2% | Saudi Arabia through SIRC projects | Long term (≥ 4 years) |

| Smart, Track-and-Trace Pharma Pilots | +0.2% | Riyadh and Jeddah distribution hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Corrugated and Last-Mile Formats

Saudi Arabia’s e-commerce revenue is projected to reach USD 30 billion in 2026, expanding at 13.5% CAGR through 2027, and the logistics network processed 101 million delivery orders during Q2 2025.[1]Saudi eCommerce, “Saudi E-commerce Market to Reach USD 30 Billion by 2026,” saudiecommerce.com The surge obliges box makers to invest in high-speed flexo-folder-gluers that marry output with next-day delivery targets. Last-mile parcels now specify lighter B- and E-flute grades for freight efficiency while still meeting compression standards for automated fulfillment. Middle East Paper Company (MEPCO) is installing a 450,000-ton-per-annum containerboard line scheduled for Q4 2027 that will reduce imported linerboard dependency and stabilize liner pricing.[2]Middle East Paper Company, “Investment in PM5 Line,” mepco.com.sa Flexible mailers are also scaling; polyethylene co-extrusions with tamper-evident strips now substitute rigid corrugated for low-fragility apparel and electronics shipments. As parcel volume climbs, converters with automated case-erectors gain service advantage and lock in longer contracts with major e-commerce platforms.

Mandatory Shelf-Life Labeling Reforms Accelerating High-Barrier Films

The Saudi Food and Drug Authority (SFDA) requires expiry, production, and storage information in Arabic under SFDA.FD 150-1 and SFDA.FD/GSO 150-2, compelling food brands to pivot from single-layer polyethylene to multilayer structures with oxygen transmission rates below 1 cc/m²/day. Metallized polypropylene and aluminum-oxide-coated PET are gaining share because they safeguard freshness across longer supply chains, crucial for remote retail in the Empty Quarter. SABIC has commercialized heat-resistant mono-polyethylene films that retain barrier performance yet remain recyclable, satisfying both compliance and circular-economy targets. Converters possessing seven-layer co-extruders now command premium pricing, while those lacking lamination lines face shortfalls and outsource barrier coating, elongating lead times.

Vision 2030 Localization Incentives for FMCG Manufacturing

Vision-aligned incentives worth USD 2.66 billion award a 10% price premium on qualified domestic content, prompting multinationals to localize production. FMCG clusters in Jubail and Yanbu benefit from concessional Saudi Industrial Development Fund loans, lowering capital hurdles for packaging plants co-located with beverage and dairy fillers. Tetra Pak’s Jeddah facility exports 40% of aseptic cartons to eleven Middle Eastern markets, leveraging Saudi Arabia’s trade corridors while satisfying local-content rules that inflate margins domestically. However, the incentive rubric counts mold tooling toward content thresholds, advantaging capital-intensive rigid packaging at the expense of flexible producers that import key machinery from Europe.

Rapid Growth of Ready-To-Eat Meal Services

Female labor-force participation and urban migration have raised per-capita snack spend from USD 40 in 2023 toward an expected USD 50 by 2030. Microwave-ready trays and retort pouches therefore outpace canned alternatives. Municipal diversion targets 90% landfill-avoidance by 2040 tilt QSR chains toward fiber-based clamshells and molded-pulp bowls. Hotpack Global is investing SAR 1 billion (USD 267 million) in a facility that will supply paper and biomass formats, adding 1,200 jobs over seven years. Active packaging innovations, including oxygen scavenger sachets, now prolong chilled shelf life without preservatives, widening distribution radii for cloud kitchens serving western Riyadh.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 30% Excise Tax on Single-Use Plastics | -0.4% | National, timing unresolved | Medium term (2-4 years) |

| Delayed Food-Grade rPET Standards | -0.3% | Beverage and food sectors | Long term (≥ 4 years) |

| Sub-Scale Domestic Paper Recycling | -0.2% | Nationwide collection gaps | Long term (≥ 4 years) |

| Rising Resin Input Costs | -0.3% | Linked to SABIC feedstock | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

30% Excise Tax on Single-Use Plastics

Saudi Arabia restructured its sweetened-beverage excise into a volumetric levy in January 2026, signaling that single-use plastics may soon face a similar tax.[3]Saudi Tax Authority, “Excise Tax on Sweetened Beverages,” zatca.gov.sa If set at SAR 1.13/kg (USD 0.30/kg), polyethylene shopping bags and polypropylene takeaway containers would see 8-12% unit-cost inflation, accelerating substitution to paper. Quick-service restaurants have begun piloting molded-pulp and kraft wraps to lock in post-tax compliance. Yet vague implementation schedules stall capital outlays for mechanical recycling because converters cannot model payback horizons. Conflicting oxo-biodegradable standards adopted by SASO risk fragmenting investment by incentivizing additives that impair recyclability.

Delayed Implementation of Food-Grade rPET Standards

Saudi Investment Recycling Company exports 1,650 tonnes of PET flakes to Europe, but beverage producers must still import certified food-grade recycled resin because SFDA has not issued contaminant limits or decontamination protocols. The gap pushes virgin-resin dependence higher and erodes the economics of local closed-loop schemes. Without super-clean wash lines aligned to European Food Safety Authority thresholds, converters cannot obtain letters of no-objection. Consequently, circularity claims remain aspirational and the Saudi Arabia packaging market loses a margin-accretive feedstock opportunity to overseas processors.

Segment Analysis

By Material Type: Paper Accelerates As Plastics Dominate

Plastic packaging contributed 54.44% of Saudi Arabia packaging market share in 2025, powered by high-density polyethylene bottles, polypropylene closures, and PET bottles. Paper and paperboard, however, are forecast to log a 3.43% CAGR, the highest among materials, as municipal waste mandates pressure food-service players to ditch polystyrene for fiber trays. Middle East Paper Company is installing a 450,000-tonne containerboard machine that will inject significant domestic linerboard capacity, easing supply constraints for corrugated converters. In parallel, SABIC’s renewable polypropylene initiatives advance bio-based thin-wall food tubs that comply with European Union tethered-cap rules, illustrating that plastic innovation continues even amid sustainability headwinds.

Converters view recycled-content paper as a hedge against resin volatility because WASCO now collects half of nationwide recovered fiber. Nevertheless, the Saudi Arabia packaging market size advantages plastics in moisture-rich food and beverage channels where barrier efficacy outweighs recyclability concerns. Metal segments, largely aluminum cans, face squeeze from pouch replacements, while container glass remains niche in premium spirits and pharma. Polyvinyl chloride and expanded polystyrene lose relevance as toxicity and landfill directives gain momentum, steering investment toward polyhydroxyalkanoate trials despite today’s 40% price premium.Paper’s price competitiveness rises further when Vision 2030 procurement premiums grant domestic fiber-based formats a baked-in 10% advantage. Corrugated’s embrace of light-weight fluting lowers freight emissions, closing parity gaps with flexible mailers. Plastics still anchor tamper-evident pharmaceutical and household chemical packs, yet material diversification is unmistakable as brand owners publish recycled-content roadmaps.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type : Single-Use Paper Outpaces Rigid Plastics

Flexible plastics commanded 35.66% of market share in 2025, driven by stand-up pouches and stretch film. The single-use paper category, encompassing clamshells, kraft bags, and molded-pulp trays, is projected to grow at a 3.83% CAGR, the fastest trajectory, as Riyadh and Jeddah target 90% landfill diversion. Hotpack Global’s planned facility will supercharge domestic capacity for compostable bowls and lids, supplying cloud kitchens that favor fiber for brand-storytelling around sustainability. Corrugated boxes remain indispensable to e-commerce fulfillment, and folding cartons protect high-value pharmaceuticals and cosmetics.

Rigid plastics, including blow-molded detergent bottles and injection-molded caps, benefit from SABIC’s down-gauged HDPE grades that achieve 15% weight savings without compromising stress-crack resistance. Metal cans continue long-term volume attrition as beverage fillers test PET bottles for carbonated soft drinks to cut freight cost. Container glass holds ground in olive oil and syrups where brand equity and inertness are vital. Consequently, the Saudi Arabia packaging market share for flexible plastics will remain strong, yet incremental growth is tilting toward paper as regulation and consumer sentiment converge.

By Packaging Format: Flexibles Extend Leadership

Flexible formats generated 52.86% of Saudi Arabia packaging market value in 2025 and will grow at 3.52% CAGR through 2031. Stand-up pouches, retort sachets, and e-commerce mailers exploit superior cube efficiency and lower logistics costs relative to rigid alternatives. Napco National’s 2025 acquisition of Arabian Flexible Packaging consolidates extrusion and printing assets, enabling portfolio breadth that pairs polyethylene wicket bags with metallized snack films. SABIC’s circular polypropylene containing 50% ocean-bound plastic signals material-side commitment to recycled content, helping brand owners future-proof against fee-based extended producer responsibility schemes.

Rigid formats such as blow-molded bottles protect carbonation and deliver tamper evidence in beverages and pharmaceuticals, aided by Vision 2030 content calculations that factor mold tooling into domestic value. Yet flexibles advance with laser micro-perforation for breathable produce pouches and hybrid barrier coatings that render mono-material laminates recyclable. The Saudi Arabia packaging market size devoted to flexible formats thus rises as food-service sachets and ready-meal pouches displace cans and jars, while rigid players respond by adding tethered caps and lightweight neck finishes to defend core segments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Personal Care And Cosmetics Take The Lead

Food applications accounted for 27.48% of market share in 2025, reflecting entrenched consumption of ambient staples, but personal care and cosmetics are primed for 3.67% CAGR through 2031, the quickest among sectors. GSO 1943:2022 mandates Arabic labeling and tamper-evident seals, boosting demand for airless pumps, sachets, and refill pouches. Beverage packaging stays large via PET bottles and Tetra Pak cartons, the latter exporting 40% of Jeddah output to regional neighbors. Pharmaceuticals rely on serialization-ready blister packs and shipper cartons embedding GS1 DataMatrix codes that enable unit-level traceability.

Industrial and chemical segments specify high-density polyethylene drums and intermediate bulk containers that leverage SABIC’s stress-crack-resistant resins for down-gauged walls. Agriculture remains a niche but steady sector, with greenhouse films and fertilizer bags riding on government food-security projects. As Saudi youth drive beauty e-commerce, converters court cosmetics brands through short-run digital printing and premium metallic effects, thereby elevating the Saudi Arabia packaging market share held by personal care formats against maturing food demand.

Geography Analysis

Saudi Arabia houses 206 paper and cardboard factories representing 44.9% of Gulf Cooperation Council capacity and captures 77.5% of regional capital commitments, underscoring its dominance in the region. Vision 2030’s incentives funnel investment into Jubail, Yanbu, and Ras Al Khair, where converters co-locate with FMCG plants to shave lead times and collect domestic-content premiums. Tetra Pak’s Jeddah plant ships aseptic cartons to eleven Middle Eastern markets, proving Saudi Arabia’s strategic proximity to high-growth export destinations.

Recycling infrastructure is still forming; plastics recovery across the Gulf hovers near 10%, but Saudi Investment Recycling Company’s PET flake exports to the United Kingdom and Spain reveal emerging collection economics. Roland Berger projects that raising GCC plastics recycling to 40% could unlock USD 6 billion annually and 50,000 jobs, adding macroeconomic incentive for deposit-return legislation. MEPCO’s forthcoming linerboard machine will reduce inbound liner imports, reallocating corrugated supply toward Riyadh fulfillment hubs and potentially squeezing UAE sheet-plants.

Employment mirrors capacity concentration: 32,500 Saudi workers comprise 71.5% of GCC paper labor, and Hotpack’s new site will add 1,200 positions, lifting sector livelihood and domestic content simultaneously. Shelf-life labeling reforms also erect a regulatory moat, because Arabic printing and food-grade certification raise entry costs for smaller converters in adjacent Gulf states. Consequently, the Saudi Arabia packaging market continues to solidify as the regional hub, exporting fiber and polymer formats while importing only specialty closures and graphics-intensive labels.

Competitive Landscape

The market is fragmented. Domestic players Napco National, Obeikan Investment Group, and Saudi Arabian Packaging Industry anchor regional scale, whereas Amcor, Tetra Pak, and Huhtamaki deploy global know-how to meet multinational brand standards. Napco’s 2025 move for Arabian Flexible Packaging expands extrusion and rotogravure capacity, helping it bundle polyethylene bags with high-barrier snack films across the GCC. MEPCO’s linerboard investment tightens corrugated supply and disadvantages UAE sheet-plants that lack paper mills, hinting at potential cross-border consolidation pressures.

Technology adoption splits the field: multinational pharma suppliers already leverage enterprise track-and-trace suites to satisfy SFDA serialization, while smaller generic manufacturers prefer contract packagers offering aggregation as a service. SABIC’s ocean-bound polypropylene and ISCC-PLUS-certified feedstocks allow converters to differentiate via sustainability without incurring resin qualification delays. Tetra Pak’s USD 3 million carton-recycling joint venture with Obeikan Paper Industries secures post-consumer fiber and poly-aluminum feedstock, intertwining supply-chain resilience with environmental positioning.

Flexible film remains the fiercest battleground; lead time, print customization, and sustainability credentials dictate share shifts. Rigid packaging stays capital intensive, and mold-tool amortization slows new-entrant encroachment. Overall, the combined share of the top five players hovers near 55%, leaving sufficient headroom for mid-size innovators to scale in niches such as bag-on-valve aerosols and compostable trays.

Saudi Arabia Packaging Industry Leaders

ASPCO

Napco National Company

Saudi Arabian Packaging Industry W.L.L

Al-Shams Printing, Packaging and Trading Company

Printopack Abee

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Tetra Pak started building a EUR 60 million (USD 68 million) pilot plant in Lund to scale paper-based barrier technology for aluminum-free cartons, with subsequent deployment slated for Jeddah high-speed lines.

- January 2025: Saudi Arabia switched the sweetened-beverage excise from 50% ad valorem to a tiered volumetric levy, setting precedent for prospective plastic taxes.

- August 2025: Napco National completed the acquisition of Arabian Flexible Packaging, consolidating regional flexible-film capacity.

- May 2025: TraceLink and Saudi Azm rolled out aggregation software linking serialized cartons to pallet identifiers for SFDA compliance.

Saudi Arabia Packaging Market Report Scope

The Saudi Arabia packaging industry encompasses the development, production, and distribution of various packaging materials and products used across multiple sectors, including food, beverage, pharmaceuticals, personal care, and industrial applications. This industry plays a critical role in preserving product quality, ensuring safety, and enhancing consumer convenience.

The Saudi Arabia Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Product Type (Paper and Paperboard Products, Plastic Products, Metal Products, and Container Glass Products), Packaging Format (Rigid, and Flexible), and End-User (Food, Beverage, Pharmaceuticals and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, Automotive, and Other End-Users). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polyethylene Polypropylene (PP) |

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Product Types | ||

| Plastic Product Type | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-Grade Products | ||

| Other Rigid Plastics Product Types | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics Product Types | ||

| Metal Product Type | Cans | |

| Aerosol Containers | ||

| Caps and Closures | ||

| Other Metal Product Types | ||

| Container Glass Product Type | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user

| Food |

| Beverage |

| Pharmaceuticals and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-users |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polyethylene Polypropylene (PP) | ||

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Polystyrene (PS) | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Product Types | |||

| Plastic Product Type | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-Grade Products | |||

| Other Rigid Plastics Product Types | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics Product Types | |||

| Metal Product Type | Cans | ||

| Aerosol Containers | |||

| Caps and Closures | |||

| Other Metal Product Types | |||

| Container Glass Product Type | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user | Food | ||

| Beverage | |||

| Pharmaceuticals and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-users | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Saudi Arabia packaging market?

The market stood at USD 11.40 billion in 2026 and is on course to reach USD 12.95 billion by 2031.

Which material type is growing fastest?

Paper and paperboard are forecast to grow at a 3.43% CAGR through 2031 as waste-diversion rules spur fiber adoption.

How is e-commerce influencing packaging demand?

E-commerce handled 101 million parcels in Q2 2025, driving strong demand for corrugated boxes and polyethylene mailers.

What sectors will drive future volume growth?

Personal care and cosmetics packaging is projected to grow at 3.67% CAGR through 2031 due to expanding beauty consumption.

How will potential plastic taxes affect converters?

A 30% excise on single-use plastics could raise polyethylene pack costs by up to 12%, accelerating shifts to paper-based alternatives.

Which companies are investing in Saudi fiber capacity?

Middle East Paper Company is adding a 450,000-tonne containerboard machine scheduled for Q4 2027 commissioning.