Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

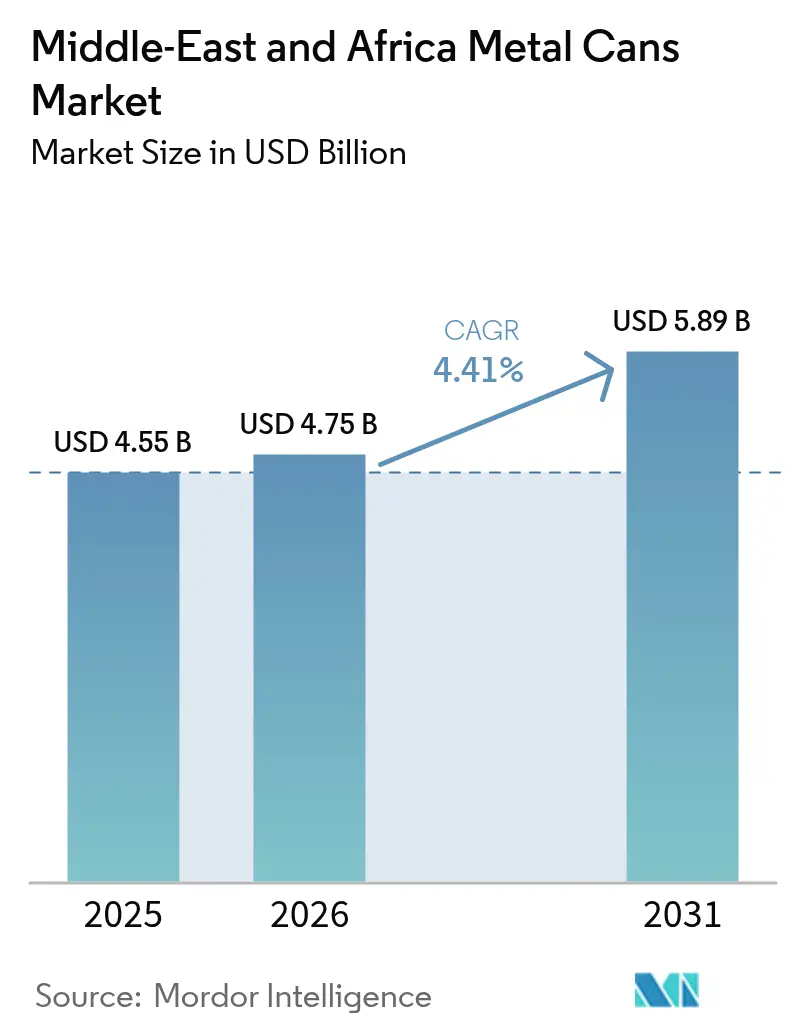

| Base Year Market Size (2025) | USD 4.55 Billion |

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 5.89 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

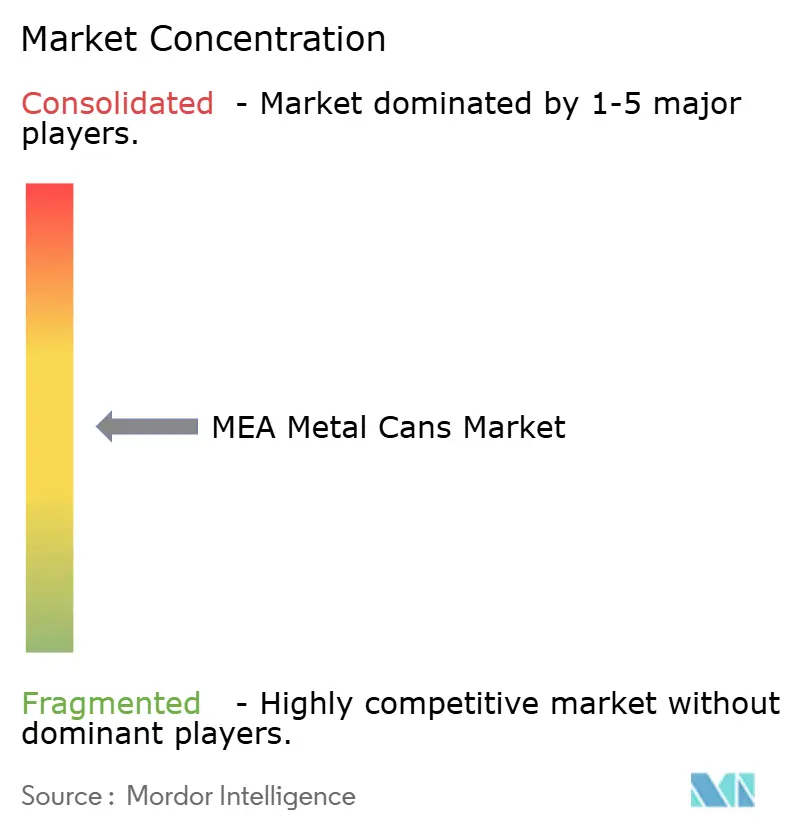

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Metal Cans Market Analysis by Mordor Intelligence

The Middle-East and Africa metal cans market size is expected to grow from USD 4.55 billion in 2025 to USD 4.75 billion in 2026 and is forecast to reach USD 5.89 billion by 2031 at 4.41% CAGR over 2026-2031. Demand climbs on the back of steadily rising disposable incomes, expanding modern retail formats, and government-led sustainability mandates that elevate aluminum recycling across the Gulf. Saudi Arabia’s Vision 2030 localization agenda, Emirates Global Aluminium’s recycling investment and capacity expansions by multiple beverage-can converters create a resilient regional supply even as aluminum price swings persist. Competitive pressure intensifies as new entrants erode historical oligopolies in South Africa, encouraging operational efficiency and lightweighting innovation. Strategic M&A, such as Sonoco’s acquisition of Eviosys, and vertical integration moves by GCC miners into downstream metals further redefine supply chains and customer relationships across the region.

Key Report Takeaways

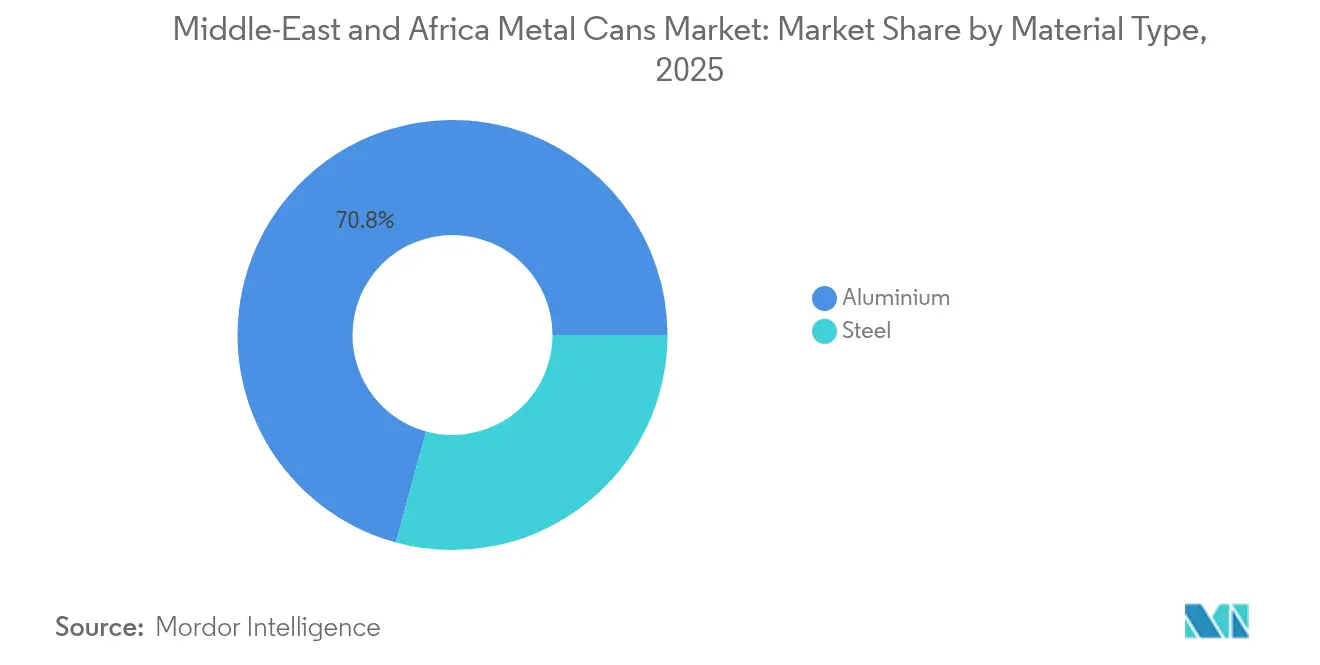

- By material type, aluminum captured 70.76% of the Middle East and Africa metal cans market share in 2025. Aluminum is projected to expand alongside a robust 5.27% CAGR to 2031.

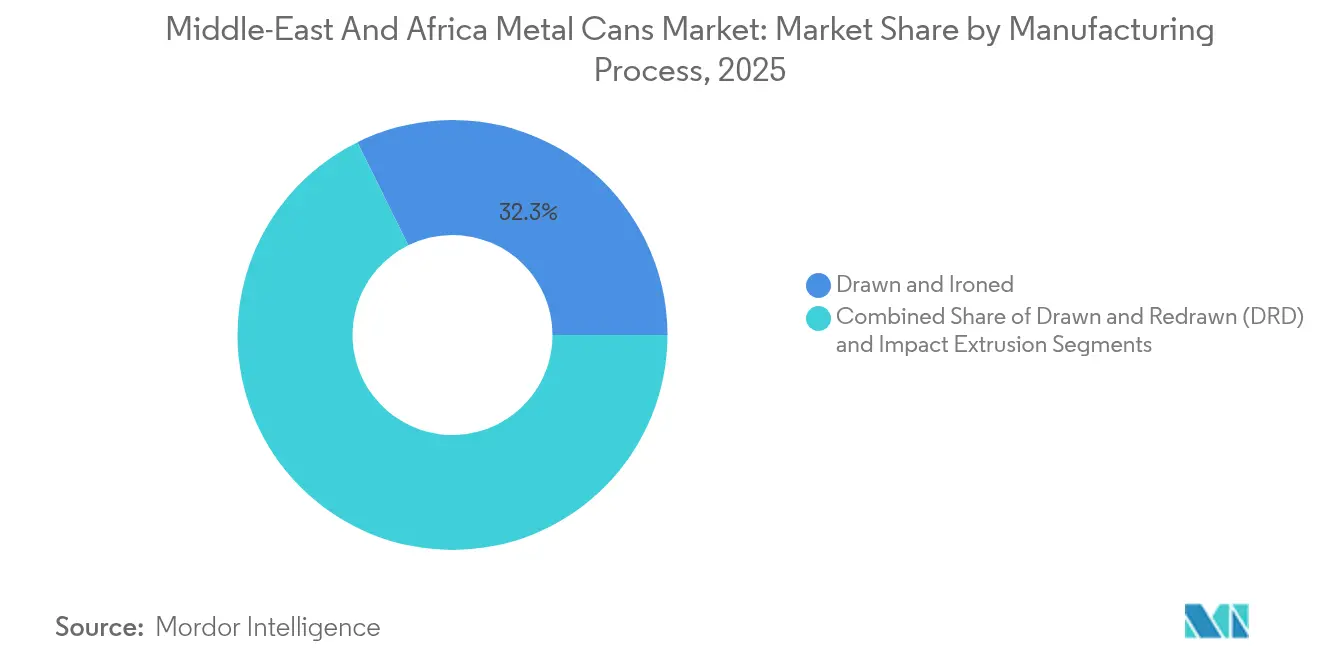

- By manufacturing process, drawn and ironed lines control 32.29% of 2025, volumesimpact extrusion is projected to expand at a 5.63% CAGR through 2031.

- By can structure, two-piece designs delivered 54.12% share in 2025, monobloc aerosol cans, however, posted the fastest 6.18% CAGR to 2031.

- By capacity/size, the 250-500 ml band held a 30.15% share in 2025, and sub-250 ml packs notch a 4.86% CAGR to 2031.

- By end-user, beverages held 38.05% revenue share in 2025; pharmaceuticals recorded the highest projected CAGR at 5.92% to 2031.

- By geography, Saudi Arabia led with a 37.74% share in 2025, while South Africa advances at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Metal Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and modern retail boost packaged F&B demand | +1.2% | GCC and South Africa | Medium term (2-4 years) |

| Government sustainability mandates spur aluminium-can recycling | +0.8% | Kenya, South Africa, UAE | Long term (≥ 4 years) |

| Expansion of GCC beverage-can capacity lowers import reliance | +0.7% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| RTD energy drinks and canned coffee adoption by Gen-Z consumers | +0.9% | Urban MEA | Medium term (2-4 years) |

| Halal-certified canned-food export surge within intra-MEA trade | +0.5% | Egypt-Saudi corridors | Medium term (2-4 years) |

| E-commerce growth drives demand for dent-resistant lightweight packs | +0.6% | UAE and South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Modern Retail Boost Packaged FandB Demand

Middle-class expansion across Egypt, Saudi Arabia, and South Africa funnels higher spending into packaged staples and indulgent ready-to-drink beverages. Egypt’s processed-food exports climbed to USD 6.1 billion in 2024, up 21%, underscoring escalating production volumes that favor robust metal protection for shipping-intensive routes.[1]Egypt Today, “Processed food exports hit record-breaking numbers in 2024,” egypttoday.com Hypermarket chains proliferate, stocking premium canned products that promise tamper evidence and long shelf life. Vision 2030 aims for 70% industrial localization, channeling fresh demand to domestic can makers. New offerings like a Saudi date-sweetened cola illustrate brand use of lithographed aluminum to differentiate on crowded shelves. Rising oil income cushions further translate into greater acceptance of slightly dearer yet longer-lasting metal packaging.

Government Sustainability Mandates Spur Aluminium-Can Recycling

Kenya’s Extended Producer Responsibility (EPR) law, effective May 2025, obliges can producers to register and finance post-use collection programs. South Africa has enforced similar rules since 2021, pushing Producer Responsibility Organizations to fund national recycling networks. The UAE supports this policy wave through Emirates Global Aluminium’s USD 90 million recycling complex, already 50% complete by May 2025.[2]EGA, “50% construction milestone on UAE recycling plant,” ega.ae These statutes lift recovered-metal feedstock availability, granting aluminum a circularity edge over multilayer plastics while supplying converters with lower-carbon billet that meets brand ESG goals.

Expansion of GCC Beverage-Can Capacity Lowers Import Reliance

Localizing manufacture trims logistics costs and currency risk. Gorilla Energy’s planned Jebel Ali plant and Sidel’s packaging MoU with Saudi authorities exemplify fresh investment that narrows the historic gap between fast-growing drink demand and can-making footprint. Abundant low-cost energy and access to bauxite act as structural incentives. Coupled with Egypt’s USD 3.276 billion processed-food exports to Arab neighbors, the GCC can reroute supply across the wider Middle-East and Africa metal cans market faster and at lower landed cost.

RTD Energy Drinks and Canned Coffee Adoption by Gen-Z Consumers

African energy-drink value is set to hit USD 5.93 billion by 2030 with Nigeria racing ahead at 14.14%. Younger buyers demand natural sweeteners, functional additives and Instagram-ready graphics, a checklist best met by high-definition printed aluminum. South Africa already captures roughly 40.13% of regional volumes, yet continual product refreshes spur run lengths that squeeze legacy steel lines. Ready-to-drink coffee gains similar traction in urban centers, pushing converters to adopt slimmer, tactile finishes that fit café-style aesthetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible plastics substitution in price-sensitive food segments | -0.9% | Sub-Saharan Africa, price-sensitive consumer segments | Medium term (2-4 years) |

| Volatile primary-aluminium premiums amid geopolitical supply risk | -1.1% | Global, with acute impact on import-dependent markets | Short term (≤ 2 years) |

| Weak post-consumer metal-collection systems in Sub-Saharan Africa | -0.7% | Sub-Saharan Africa, rural and peri-urban areas | Long term (≥ 4 years) |

| Regulatory uncertainty over BPA/PFAS can-linings | -0.6% | EU regulations affecting MEA exports, regulatory-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flexible Plastics Substitution in Price-Sensitive Food Segments

Large rural populations still base purchase decisions on unit cost, giving lightweight pouches an edge for staples like tomato paste or rice. Suppliers such as UFlex run 40,000 TPA film in the UAE and 114,000 TPA in Egypt, marketing metallized BOPET that mimics the barrier levels of cans at lower material weight. Senegal’s 35% import tariffs on processed foods accentuate cost pressures, steering fillers to cheaper substrates. To stem share loss, can makers emphasize 100% recyclability, flavor neutrality and resistance to pilferage in remote logistics chains.

Volatile Primary-Aluminium Premiums Amid Geopolitical Supply Risk

Exchange inventories dipped 10% on the LME and 30% on the SHFE by May 2025, lifting premiums for physical delivery. Trade actions from U.S. tariffs on Canadian billet to sanctions on Russian output cascade into higher inbound costs for Middle-East and Africa converters. Lacking hedging sophistication, mid-tier players face margin erosion whenever they cannot swiftly adjust contract pricing. While scrap-based billet offers partial relief, investments in recycling still lag near-term demand surges, magnifying the impact on the Middle-East and Africa metal cans market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Drives Sustainability Transition

Aluminum retained 70.76% of the Middle-East and Africa metal cans market share in 2025, vastly outstripping steel thanks to its 100% recyclability and favorable weight-to-strength ratio. Aluminum’s superior circularity aligns with new EPR schemes and brand decarbonization targets, prompting producers to channel capex into billet casting and in-house scrap recovery. Emirates Global Aluminium’s half-built recycling hub highlights this pivot, promising regional access to low-carbon feed that could unlock further lightweighting. Steel continues serving large-format food and industrial cans where impact resistance outweighs weight penalties; yet BPA substitute rules and higher freight costs curb its longer-term appeal. Novelis projects 4% annual demand growth for aluminum beverage sheet through 2031, underscoring confidence in the alloy’s trajectory.

The Middle-East and Africa metal cans market size for aluminum is projected to expand alongside a robust 5.27% CAGR to 2031, supported by GCC mining deals totaling USD 9.32 billion that assure upstream supply. Regulatory carrots such as reduced EPR fees for high-recycled-content packs reinforce alloy uptake in beverage, pharmaceutical, and cosmetic lines. Steel’s future hinges on cost leadership and niche applications like retortable 3-piece cans for industrial sauces, where thickness and dent resistance remain critical.

By Can Structure: Two-Piece Leadership Meets Aerosol Innovation

Two-piece designs delivered 54.12% share in 2025 due to their material-efficient draw and iron process that suits high-volume colas and energy drinks. Their thinner walls lower shipping mass, a boon for e-commerce distributors now handling rising beverage traffic. Monobloc aerosol cans, however, post the fastest 6.18% CAGR as personal care, household, and pharmaceutical sprays proliferate across emerging urban centers. Ball Corporation produces 1.2 billion aluminum aerosols annually, most carrying the Aluminum Stewardship Initiative certification that resonates with eco-minded shoppers. Three-piece formats survive where can height exceeds D&I limits, notably in powdered milk tins and bulk edible-oil packs.

Aerosol innovation centers on ultra-smooth internal coatings and dimensional accuracy for medical inhalers. Specialist firms apply plasma fluorocarbon layers to ensure zero drug interaction and accurate dosage control as Middle-East and Africa pharmacies broaden OTC shelves, demand for GMP-compliant aluminum canisters accelerates, widening the opportunity pool for highly automated extrusion lines. Converters simultaneously refine two-piece lines with taller draw ratios, enabling slim 250 ml cans popular among Gen-Z coffee drinkers.

By Capacity/Size: Mid-Range Dominance Shifts to Small-Format Growth

The 250-500 ml band held 30.15% share in 2025, favored by mainstream carbonated drinks and cost-per-milliliter efficiency. Yet sub-250 ml packs notch a 4.86% CAGR, propelled by premium energy shots, functional beverages, and portion-controlled cocktails. Gorilla Energy’s planned Halal-certified range employs sleek 250 ml cans to deliver portability and pricing tiers acceptable to a broad demographic. Digital grocery shoppers also prefer smaller volumes that fit congested last-mile boxes, cutting dent risk and return rates.

At the opposite end, 500-1,000 ml formats anchor family-size ready meals and canned fruit, especially within Egypt’s export-oriented processors. Above-1-liter containers serve industrial ingredients, paint, and lubricants; however, their slower category growth motivates can makers to redirect line upgrades toward faster-moving small formats. Fee structures under South Africa’s EPR make per-unit costs for oversized packs steeper, incentivizing fillers to downsize where possible without hurting value perception.

By Manufacturing Process: D&I Leadership Faces Impact-Extrusion Innovation

Drawn and ironed lines control 32.29% of 2025 volumes, underpinning beverage giants’ need for 2,000-cpm speeds and thin-wall accuracy. Ongoing R&D reduces wall thickness by another 3-5%, lowering alloy consumption without sacrificing stack strength. Impact extrusion logs a 5.63% CAGR, oriented toward aerosol, pharma, and luxury personal-care niches where tighter dimensional tolerances and chamfer-free shoulders are mandatory. Anomatic’s cGMP facility, able to anodize 2.5 billion units yearly, displays how surface-treatment depth and color consistency attract health-and-beauty brands.

The Middle-East and Africa metal cans market size generated by D&I technology benefits from integrated coil-coating and water-treatment systems that shrink carbon footprints. Meanwhile, impact extruders experiment with uni-alloy formats that simplify recycling streams, a goal advanced by Novelis and DRT’s 99% recycled-content can-end program. Process choice thus becomes a strategic lever balancing capex, sustainability metrics, and application specificity.

By End-User Industry: Beverage Dominance Meets Pharmaceutical Acceleration

Beverages retained 38.05% segment share in 2025, buoyed by carbonated soft drinks, craft malts, and an expanding repertoire of functional tonics. Energy-drink marketers rotate flavors quarterly, necessitating flexible tooling and vibrant graphics that aluminum readily provides. The pharmaceutical channel, though smaller, is set to post a 5.92% CAGR as inhalers, topical sprays, and sterile saline aerosols gain market depth amid rising chronic respiratory cases. Tri-Pac’s 10 million-unit aerosol line addition exemplifies supplier readiness to meet GMP and ISO 13485 needs.

Food canning remains vital, powered by Egypt’s USD 6.1 billion processed-food exports and halal protein shipments to Gulf buyers. Personal-care and cosmetics capitalize on monobloc cans’ replicable mirror finishes, reinforcing brand premium cues. Lubricants and industrial fluids require resistant internal lacquers, but volumes grow more modestly alongside regional automotive-fleet expansion.

Geography Analysis

Saudi Arabia anchors 37.74% of the Middle-East and Africa metal cans market share, leveraging Vision 2030’s industrial roadmap that targets USD 241.7 billion in industrial GDP by 2030, following conversion from 895 billion SAR at 2025 exchange rates. Localization pledges draw global can-line vendors to Riyadh as authorities dangle loan guarantees and tariff privileges. Aluminum smelters integrated with cheap natural gas deliver cost advantages few rivals can match.

South Africa, advancing at a 6.82% CAGR, rides beverage-can investment by four competing converters plus established scrap-collection networks nurtured under its EPR law. Rising e-commerce penetration and improving consumer confidence spur premium RTD launches that demand photorealistic can art and matte varnishes. The country’s port links enable onward shipment to fast-growing hinterland states.

Egypt blends low labor cost with Suez Canal proximity, feeding canned legumes and fish to Arab partners that absorbed USD 3.276 billion of its processed-food output in 2024. Nigeria’s surge in used-can exports underlines West Africa’s ambition to join the circular-metal economy, while Kenya’s 2025 EPR statute signals East Africa’s pivot toward formal recycling systems. Together, these diverse markets create a patchwork of regulatory, cost, and consumer variables that global brand owners address via multi-plant strategies and agile sourcing across the wider Middle-East and Africa metal cans market.

Competitive Landscape

Rivalry has intensified from South Africa to the Gulf as new entrants fracture once-concentrated supply. Nampak’s share in South African beverage cans has thinned since 2018, with three additional producers now active, compressing margins but spurring cost savings programs, IOL.. Globally, Sonoco’s USD 3.9 billion takeover of Eviosys stitched 44 plants across 17 nations into a formidable food and aerosol platform that can leverage procurement scale to underprice smaller African players.[3]Sonoco Products Company, “Sonoco Completes Acquisition of Eviosys,” sonoco.comCANPACK’s pending merger with Giorgi indicates further consolidation momentum.

Technology partnerships define the next frontier. Novelis teams with DRT to commercialize can ends made from 99% recycled alloy, lowering Scope 3 emissions for beverage majors. Ball patents holographic over-varnish systems that lift shelf standout, and Constellium pushes Aeral D&I barrels that shave 30% weight. Local champions respond by installing quality-vision systems and switching to water-based inks to satisfy multinational audit criteria.

Sustainability credentials now tip many purchase decisions. Aluminium Stewardship Initiative or ISO 14001 certifications increasingly sit alongside ISO 13485 and cGMP on tender scorecards, closing doors to converters lacking documented traceability. Capital is therefore channelled into closed-loop scrap capture, renewables-powered smelters, and lightweighting R&D as firms jockey for long-term supply contracts in the expanding Middle-East and Africa metal cans industry.

Middle-East And Africa Metal Cans Industry Leaders

ARYUM Metal Alüminyum Tüp Sanayi ve Ticaret A.Ş.

Ball Corporation

Crown Holdings, Inc.

SAPIN Saudi Arabian Packaging Industry Co. Ltd.

Avon Crowncaps and Containers Nigeria Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Emirates Global Aluminium reached the 50% construction milestone on the UAE’s aluminum recycling plant, boosting regional billet supply.

- May 2025: Saudi Arabia’s Ministry of Industry confirmed Vision 2030 progress toward USD 241.7 billion industrial GDP, reinforcing downstream packaging demand.

- May 2025: Kenya began enforcing new EPR regulations mandating producer financing of metal-packaging waste programs.

- February 2025: Gorilla Energy detailed plans for a Jebel Ali canning facility to target the USD 3.19 billion regional energy-drink market.

Middle-East And Africa Metal Cans Market Report Scope

The study analyzes the key trends and forecasts related to the Metal Can Industry in the Middle East & African region. The key aim of the study is to analyze the consumption related trends for packaging based products across several end-user verticals and providing growth forecasts by taking into account the historical trends and a wide range of macro & micro-economic base indicators relevant to the packaging domain.

The study provides a detailed perspective on the impact of COVID-19 on the demand and supply paradigm by taking into account several base scenarios in the near & medium-term basis. The report on the metal cans market studies various segments that are part of manufacturing different types of cans with applications in various end-user segments. It also analyzes the demand-supply pattern of aluminum can stock or rolled sheet in MEA.

The different applications of metal cans are in sectors, like beverages, foods, pharmaceuticals, cosmetics, and other end-users, such as paints and coatings, and chemicals, among others.

By Material Type

| Aluminium |

| Steel |

By Can Structure

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

By Capacity / Size

| ≤250 ml |

| 250-500 ml |

| 500-1,000 ml |

| >1,000 ml |

By Manufacturing Process

| Drawn and Ironed (D&I) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

By End-User Industry

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industries |

By Geography

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Aluminium | ||

| Steel | |||

| By Can Structure | Two-Piece | ||

| Three-Piece | |||

| Monobloc Aerosol | |||

| By Capacity / Size | ≤250 ml | ||

| 250-500 ml | |||

| 500-1,000 ml | |||

| >1,000 ml | |||

| By Manufacturing Process | Drawn and Ironed (D&I) | ||

| Drawn and Redrawn (DRD) | |||

| Impact Extrusion | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Paints and Industrial Chemicals | |||

| Automotive Fluids and Lubricants | |||

| Other End-User Industries | |||

| By Geography | Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Middle-East and Africa metal cans market in 2026?

It is valued at USD 4.75 billion, with a projected 4.41% CAGR to 2031.

Which material dominates metal can production across the region?

Aluminum leads with 70.76% market share, supported by strong recycling initiatives and lightweighting advantages.

Why is South Africa forecast to grow faster than other markets?

Four active can manufacturers, robust EPR recycling infrastructure and rising RTD beverage launches fuel a 6.82% CAGR.

Which end-user sector shows the highest growth momentum?

Pharmaceuticals post the fastest CAGR at 5.92% thanks to expanding aerosol drug delivery formats.

What regulatory shift most affects future packaging choices?

New EPR laws in Kenya and stricter frameworks in South Africa reward highly recyclable aluminum cans over multilayer plastics.

How are producers addressing aluminum price volatility?

Investments in regional recycling capacity, hedging strategies and alloy lightweighting help offset raw-material premium swings.

Page last updated on: