Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.86 Billion |

| Market Size (2031) | USD 12.56 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Food Packaging Market Analysis by Mordor Intelligence

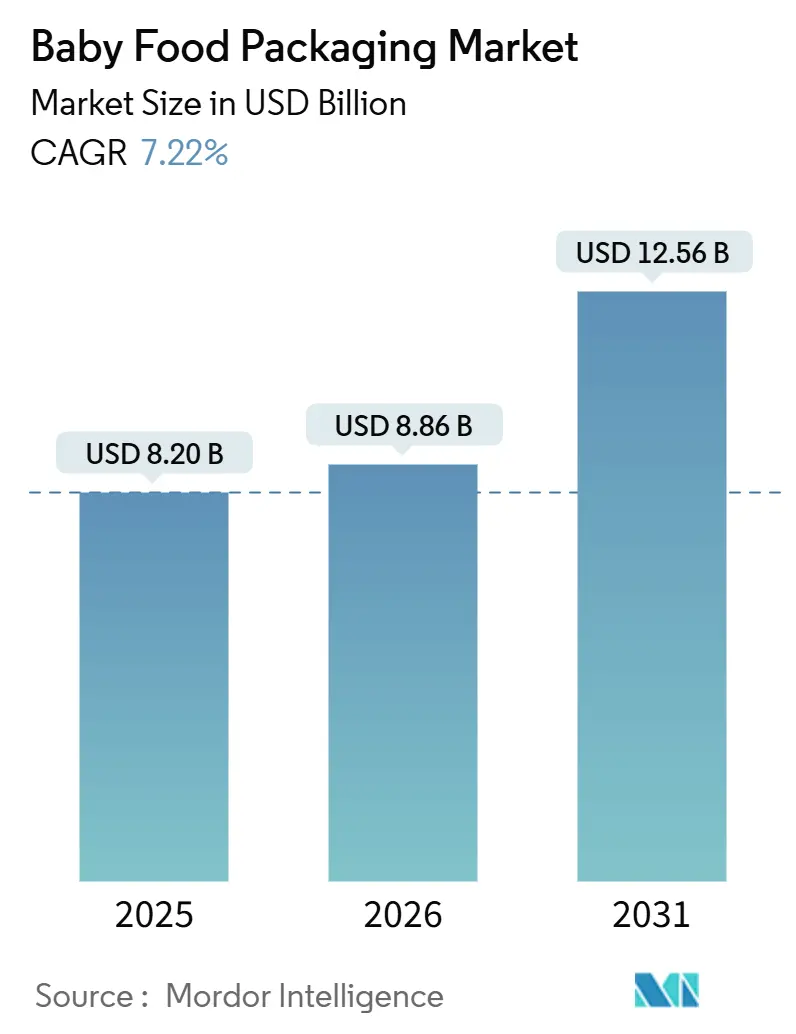

The Baby Food Packaging Market size was valued at USD 8.20 billion in 2025 and is estimated to grow from USD 8.86 billion in 2026 to reach USD 12.56 billion by 2031, at a CAGR of 7.22% during the forecast period (2026-2031).

Heightened regulatory scrutiny, rising dual-income urban households, and the rapid uptake of aseptic spouted-pouch technology are reshaping material choices and filling-line layouts. Pouches continue to displace rigid jars because they are light, resealable, and compatible with high-throughput aseptic equipment, while paperboard gains ground as Extended Producer Responsibility (EPR) fees penalize non-recyclable laminates. Brand owners are also adding smart labels and QR codes to reassure parents on provenance and cold-chain integrity. Meanwhile, compliance costs linked to Bisphenol A substitutes and phthalate-free adhesives are squeezing mid-tier converter margins, intensifying competition for cost-efficient, fully recyclable formats.

Key Report Takeaways

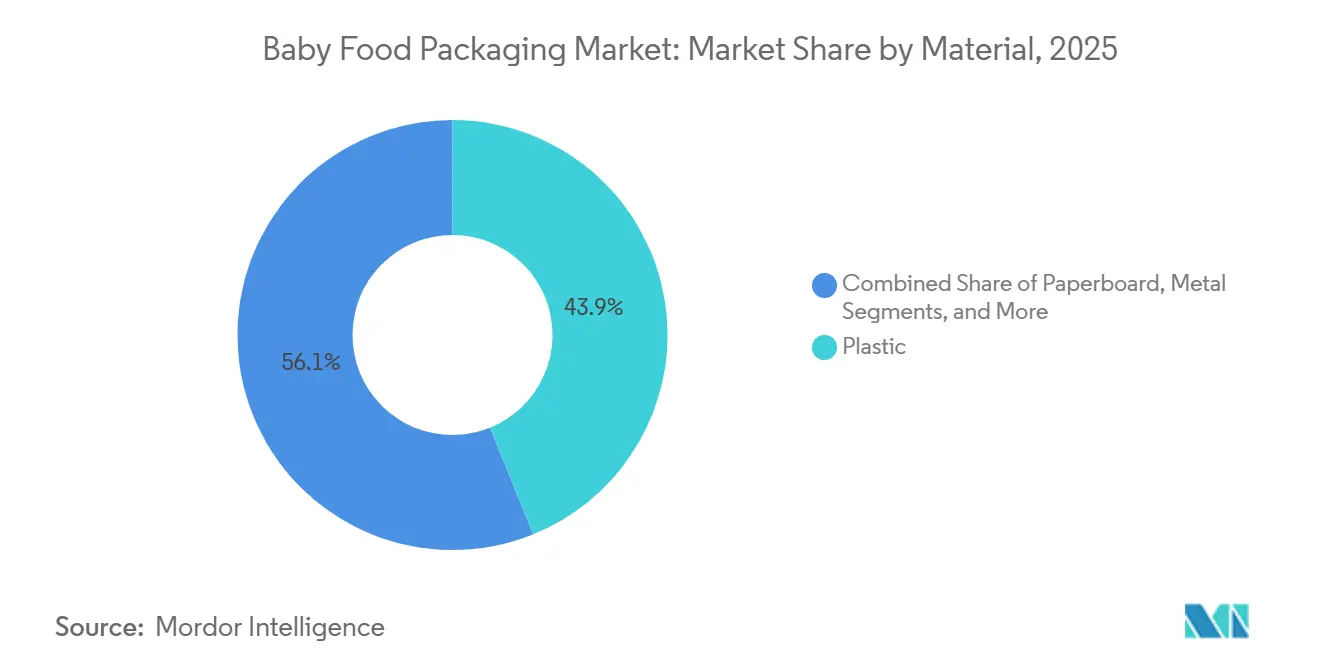

- By material, plastic retained a 43.87% share in 2025, yet paperboard is set to expand at 8.21% as EPR fee structures reward fiber-based substrates.

- By package type, pouches led with 37.15% of 2025 global volume and will post the fastest CAGR of 8.18% through 2031.

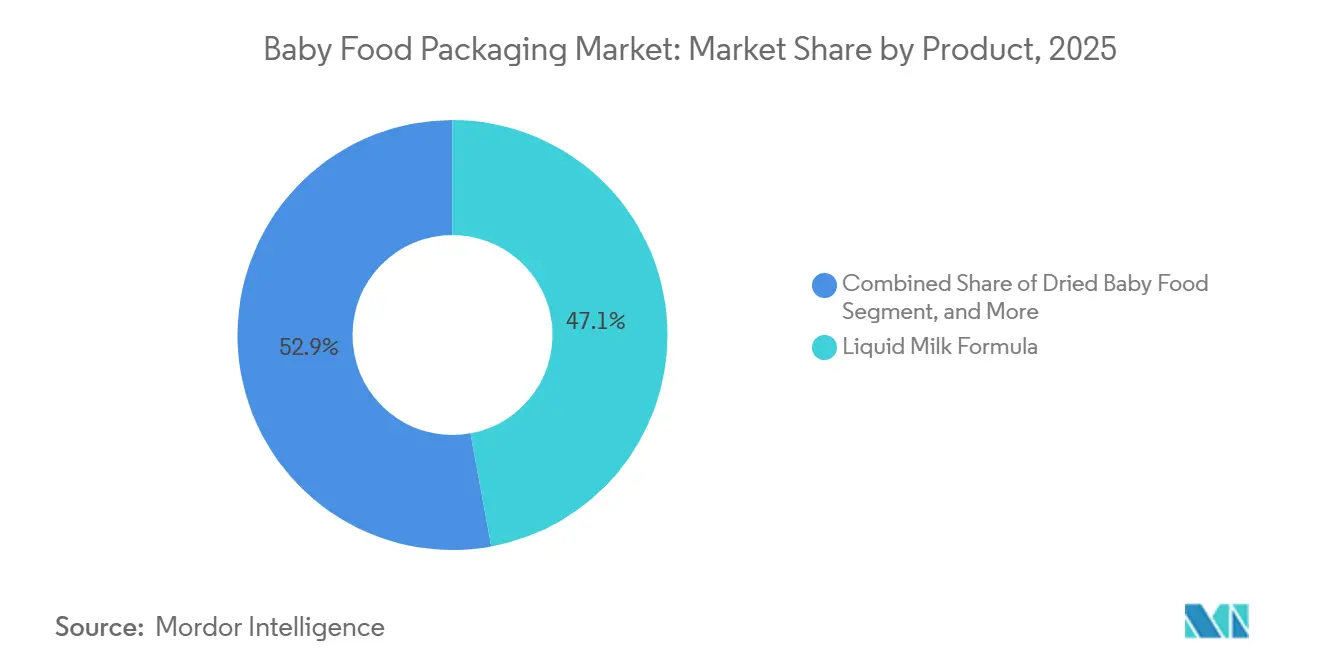

- By product, powder milk formula commanded 47.12% of the 2025 value, while prepared baby food is projected to grow the quickest at 8.31% over 2026-2031.

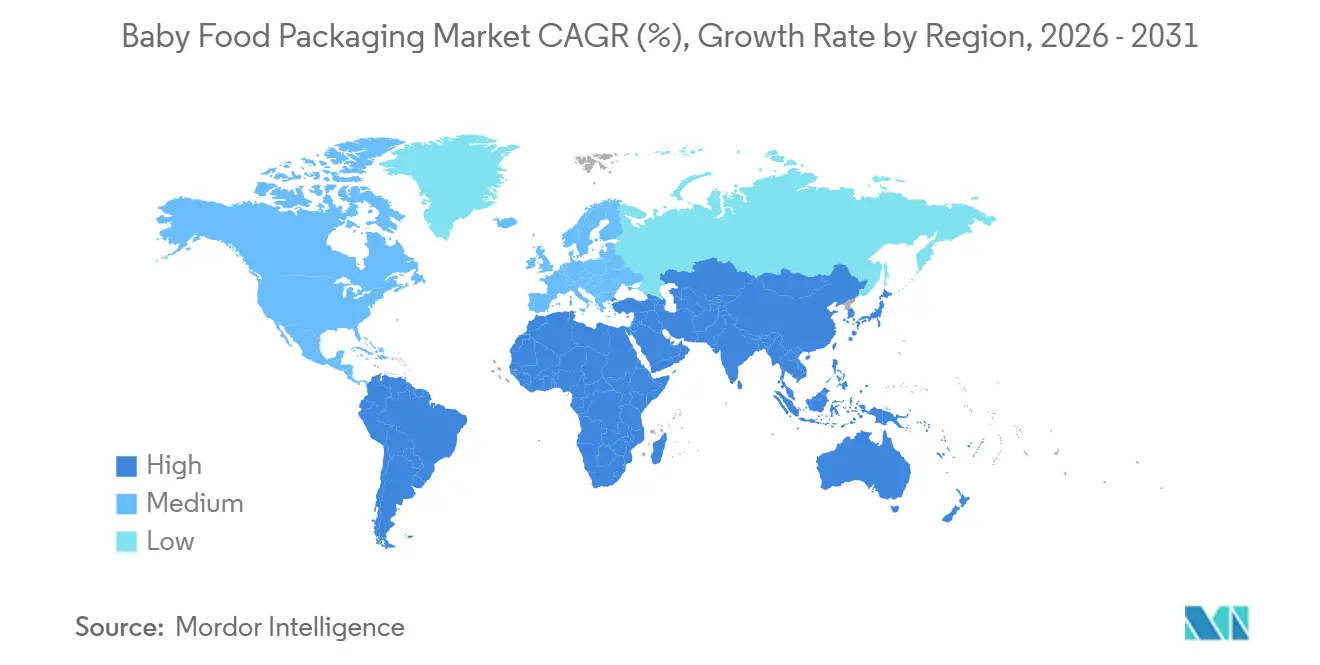

- By geography, Asia-Pacific accounted for 42.52% of 2025 revenue and is on track for the highest regional CAGR of 8.14% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Baby Food Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-Driven Adoption of Baby Food Pouches | +1.8% | Global with focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Urban Dual-Income Households Demanding Time-Saving Formats | +1.5% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| Stricter Infant-Safety Regulations Expanding Premium Packaging | +1.2% | North America and Europe, cascading to Asia-Pacific | Long term (≥ 4 years) |

| Aseptic Spouted-Pouch Filling Lines Gaining Ground | +1.0% | Global, led by Europe and Asia-Pacific | Short term (≤ 2 years) |

| Extended-Producer-Responsibility Incentives for Recyclability | +0.9% | Europe and United Kingdom, emerging in Asia-Pacific | Long term (≥ 4 years) |

| AI-Led Personalised-Nutrition Pack Design Innovations | +0.5% | North America and Europe, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-Driven Adoption Of Baby Food Pouches

Lightweight, resealable pouches have become the default format for on-the-go feeding in urban markets because caregivers value portability and portion control. SIG Combibloc’s Prime 55 in-line aseptic system, launched in 2024, combines spout attachment and sterile filling in one pass, trimming line complexity and third-party sterilization steps.[1]SIG Combibloc, “Prime 55 In-Line Aseptic System,” SIG.biz IMA Group’s FillShape equipment, adopted by several European converters in 2025, enables upright-shaped pouches that command front-of-shelf visibility.[2]IMA Group, “FillShape Technology for Shaped Pouches,” Imagroup.com Retail chains in Japan and South Korea reported double-digit growth in pouch sales in 2025 as single-parent families and grandparents sought formats that minimize preparation time. Online retailers also favor pouches because lower weight reduces freight costs and breakage claims versus glass jars.

Urban Dual-Income Households Demanding Time-Saving Formats

China’s National Bureau of Statistics recorded that 68% of urban households with infants had two working parents in 2025, up from 54% in 2020. The time squeeze is steering shoppers toward ambient-stable pouches and cartons that need no refrigeration, especially in tier-2 and tier-3 cities where cold-chain gaps persist. Tetra Pak debuted a 200-milliliter aseptic carton with a twist cap in India in 2025 to meet this need.[3]Tetra Pak, “200 ml Aseptic Carton Launch in India,” Tetrapak.com Similar behavior is emerging in Brazil and Mexico, where urbanization rates topped 85% in 2025, and supermarket penetration of baby food pouches doubled since 2023. Although pouch units carry a 15-20% price premium over jars in Southeast Asia, velocity remains higher because shoppers equate the format with convenience

Stricter Infant-Safety Regulations Expanding Premium Packaging

The European Union’s Regulation 2024/3190 banned Bisphenol A (BPA) in all food-contact materials as of January 2025, compelling converters to shift to BPA-free linings, which add USD 0.02-0.04 per unit to material costs. The U.S. Food and Drug Administration tightened guidance on infant formula packaging in 2024, lengthening the toxicology testing cycle. China capped phthalate content at 0.1 ppm in 2025 and mandated third-party certification for sub-36-month products. These rules raise barriers to entry and consolidate projects around converters with in-house labs, while smaller players struggle to fund extended validation.

Aseptic Spouted-Pouch Filling Lines Gaining Ground

Aseptic processing grants 12-18 month shelf life without preservatives, avoiding cold-chain costs in hot climates. Capital spending on such lines surged in 2025 as converters in Europe and Asia-Pacific ordered equipment from IMA, Scholle IPN, and ALCA. ALCA’s integrated sterilization cycle trims energy use by 30% versus legacy gear. Mondi validated a recyclable mono-material polyethylene pouch for aseptic filling in 2024, easing EPR fee exposure in the European Union. Organic brands unable to add synthetic preservatives see the technology as a route to broader distribution.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics Sustainability Backlash and Legislation | -1.2% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| BPA/Chemicals Compliance Cost Pressures | -0.8% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Supply Bottlenecks of Pharma-Grade Spout Resins | -0.6% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| DIY Baby-Food Trend Reducing Packaged Demand | -0.5% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastics Sustainability Backlash And Legislation

France imposed a EUR 0.50 per kilogram tax on virgin plastic in 2024, lifting pouch resin costs by 8-12%. The United Kingdom’s EPR scheme, launched in 2025, levies surcharges of up to GBP 1,000 per tonne on non-recyclable laminates. German and Dutch retailers have begun delisting baby-food brands that lack mono-material solutions, and a 2025 European Environmental Bureau survey found that 72% of parents are willing to pay a 10% premium for fiber- or glass-based packaging. These dynamics accelerate the shift to paperboard cartons, recyclable pouches, and glass jars despite cost and weight downsides.

BPA/Chemicals Compliance Cost Pressures

Replacing epoxy-phenolic can linings with polyester or acrylic coatings lifts per-square-meter material cost by 20-30% and forces adhesive reformulation. Lead times for BPA-free laminating resins stretched to nine months in 2025, delaying commercial launches and pushing converters to pay premium freight for alternative supplies. Each stock-keeping unit now requires USD 15,000-25,000 in migration testing, a burden that mid-size brands often pass to consumers. The European Food Safety Authority cut the tolerable daily intake for BPA by a factor of 20,000 in 2024, prompting several brands to exit metal formats rather than requalify coatings.[4]European Food Safety Authority, “Revised BPA Intake Opinion 2024,” Efsa.europa.eu

Segment Analysis

By Material: Paperboard Gains As Plastic Faces Scrutiny

Plastic captured 43.87% of 2025 revenue, yet paperboard is forecast to expand at 8.21%, the highest among materials, as EPR schemes reward substrates that can demonstrate high fiber recovery rates. Tetra Pak cartons already achieve 90% recyclability in European mills, qualifying for reduced EPR fees, while SIG Combibloc’s plant-based polymer barrier further lowers fossil content. The baby food packaging market for paperboard is projected to reflect this momentum, especially in regions with mature municipal sorting infrastructure.

Converters continue to trial water-based coatings and plasma-deposited barriers that give paperboard sufficient moisture resistance for acidic purees. Metal cans remain a niche for premium retort products but face price erosion from BPA-free coatings. Glass maintains a purity halo but suffers weight and breakage penalties in e-commerce. Bioplastics, though attractive for their compostability claims, cost 40-60% more than polyethylene and lack widespread collection systems, limiting their immediate impact on the baby food packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Package Type: Pouches Dominate Convenience Segment

Pouches held 37.15% of 2025 volume and will outpace all other types at 8.18% through 2031. Their lightweight structure lowers freight costs, while resealable spouts support partial feeding, two factors that resonate with mobile caregivers. Inverted dispensing fitments from Scholle IPN blur lines with traditional bottles, giving the category additional versatility. Bottles remain essential for powder-formula reconstitution, yet growth lags as ready-to-feed offerings gain shelf space.

Jars, once dominant in North America and Europe, are conceding space to pouches in urban supermarkets with tight planograms. Aseptic cartons are expanding in Asia-Pacific where domestic formula brands invest in brick-pack lines. Bag-in-box finds a foothold in institutional channels but lacks consumer acceptance. Overall, pouches will continue to set the pace for baby food packaging market share gains because of equipment compatibility and EPR-driven recyclability improvements.

By Product: Prepared Baby Food Outpaces Formula

Powder milk formula retained 47.12% of the 2025 value due to its premium positioning and shelf stability, while prepared baby food will advance the fastest at 8.31% between 2026 and 2031. Dual-income parents gravitate toward spoon-free purees, blended meals, and finger foods packaged in squeeze pouches or lightweight jars that bypass cooking. The baby food packaging market, linked to prepared foods, reflects this shift as retailers allocate more shelf space to ready-to-eat options.

Baby snacks in the prepared category are growing rapidly, driven by demand for texture-rich products that encourage self-feeding. Liquid formula commands a 30-40% premium over its powder equivalents but still accounts for a smaller slice of spending. Dried cereals move in line with overall market growth yet face substitution from fortified adult oatmeal. Packaging innovation, such as Amcor’s ultra-thin film, which reduces pouch weight by 20%, supports brand efforts to maintain margins while meeting corporate plastic-reduction targets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific accounted for 42.52% of 2025 revenue and is projected to expand at 8.14%, the fastest regional pace. E-commerce majors in China have embraced QR-code traceability, reinforcing parent confidence in authenticity. India’s tier-2 cities post double-digit growth as government cold-chain programs improve last-mile reliability. Mature markets such as Japan and South Korea sustain premium glass-jar sales, whereas Indonesia, Thailand, and Vietnam lean on pouches compatible with ambient logistics.

North America ranks second in size, underpinned by stringent regulatory oversight and widespread organic labeling. Growth moderates as a do-it-yourself baby-food movement gains traction: parents invest in countertop blenders and reusable silicone pouches, trimming demand for packaged purees. Canada mirrors U.S. safety rules but layers bilingual labeling requirements; Mexico chalks up brisk pouch adoption as supermarket chains widen infant-nutrition assortments in major cities.

Europe balances tough sustainability mandates with high organic penetration. Germany, France, and the United Kingdom prioritize mono-material pouches to curb EPR fees, while Italy and Spain still favor transparent glass jars. Eastern European countries transition toward portion-controlled pouches as incomes rise. South America, led by Brazil and Argentina, is witnessing pouch-driven expansion in urban hubs with patchy refrigeration, and the Middle East and Africa are following Western feeding habits as expatriate populations and middle classes grow.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five converters, Amcor PLC, Tetra Laval Group, Mondi Group, Berry Global Inc., and Silgan Holdings Inc., command an estimated 38-42% of 2025 revenue, leaving meaningful share for regional specialists. Competition revolves around aseptic expertise, recyclability credentials, and control of fitment production. Amcor’s 2024 purchase of Moda Systems strengthened its closure portfolio and helped secure long-term spout supply agreements. Tetra Laval protects its dominant carton installed base, while SIG Combibloc and Elopak tempt brand owners with modular lines that accept a range of formats.

Regional challengers in India and China exploit lower labor costs to supply commodity pouches at 15-25% discounts, fragmenting price-sensitive segments. UFlex boosted domestic aseptic-pouch capacity by 40% in 2025, signaling local intent to serve both South Asia and export markets. Technology investments differentiate leaders: Huhtamaki deployed artificial intelligence for quality control, cutting seal defects by 30% and enabling blockchain traceability. ISO 22000 and Global Food Safety Initiative benchmarks are now table stakes for converters courting multinational brands.

Strategic alliances are expanding across Southeast Asia and Sub-Saharan Africa to dodge import tariffs on finished packaging. Mondi’s partnership with a chemical-recycling consortium produced a pouch incorporating 25% post-consumer recycled polyethylene without losing barrier performance, helping brands contain EPR levies. Silgan’s 2025 acquisition of a specialty closure maker added child-resistant caps essential for iron-fortified powder formula. Expect further vertical integration as converters race to shore up supply chain security for pharma-grade resins and fitments.

Baby Food Packaging Industry Leaders

Ardagh Group

Amcor PLC

Mondi Group

Tetra Laval Group

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Amcor PLC committed EUR 120 million (USD 128 million) to scale recyclable mono-material pouch capacity in Poland, complete with in-line spout attachment and aseptic filling.

- December 2025: Tetra Laval Group finalized a USD 95 million upgrade of its Jiangsu, China, carton plant, adding 200 milliliter and 250 milliliter formats with plant-based barriers.

- November 2025: Mondi Group and a European chemical-recycling consortium validated baby-food pouches with 25% recycled polyethylene.

- October 2025: Berry Global Inc. released an 18% lightweighted spouted pouch that trims material cost by USD 0.015 per unit.

Global Baby Food Packaging Market Report Scope

Baby food packaging products are specially designed for packaging food material for infants and toddlers. A wide variety of packaging materials, such as glass jars, plastic containers, metal cans, folding cartons, and other solutions, are used for packaging baby food products, including dried foods, prepared foods, and milk formula. The report offers the latest study about the present worldwide market development strategy of the baby food packaging market based on the segmentations such as material type, packaging type, product type, and geography.

By Material

| Plastic |

| Paperboard |

| Metal |

| Glass |

| Bioplastics |

By Package Type

| Bottles |

| Cartons |

| Jars |

| Pouches |

| Bag-in-Box |

By Product

| Liquid Milk Formula |

| Dried Baby Food |

| Powder Milk Formula |

| Prepared Baby Food |

| Baby Snacks |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Material | Plastic | |

| Paperboard | ||

| Metal | ||

| Glass | ||

| Bioplastics | ||

| By Package Type | Bottles | |

| Cartons | ||

| Jars | ||

| Pouches | ||

| Bag-in-Box | ||

| By Product | Liquid Milk Formula | |

| Dried Baby Food | ||

| Powder Milk Formula | ||

| Prepared Baby Food | ||

| Baby Snacks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the baby food packaging market?

It stands at USD 8.86 billion in 2026 and is forecast to reach USD 12.56 billion by 2031.

Which package type is growing the fastest?

Pouches are advancing at an 8.18% CAGR during 2026-2031, outpacing all other formats.

Why is paperboard gaining share against plastic?

Extended Producer Responsibility fees reward easily recyclable fiber materials, making paperboard cartons more cost-effective over time.

Which region offers the highest growth opportunity?

Asia-Pacific leads with an 8.14% regional CAGR, propelled by urbanization and rising disposable incomes.

How are regulations influencing packaging choices?

Bans on Bisphenol A and taxes on virgin plastic are pushing converters toward BPA-free coatings, mono-material laminates, and fiber-based solutions.

What technology trends are reshaping the sector?

Aseptic spouted-pouch lines and smart labels that track temperature excursions are enabling brand owners to extend shelf life and assure supply-chain integrity.