Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

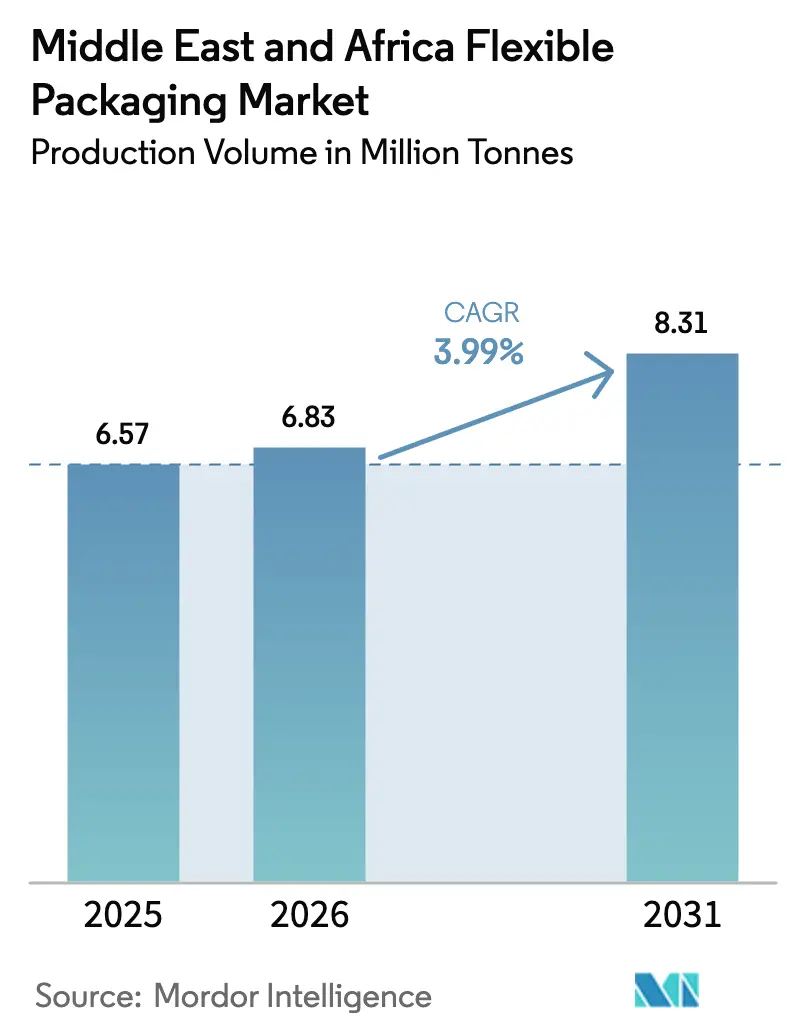

| Base Year Market Size (2025) | 6.57 Million tonnes |

| Market Volume (2026) | 6.83 Million tonnes |

| Market Volume (2031) | 8.31 Million tonnes |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Flexible Packaging Market Analysis by Mordor Intelligence

The Middle East and Africa flexible packaging market size is expected to grow from 6.57 million tonnes in 2025 to 6.83 million tonnes in 2026 and is forecast to reach 8.31 million tonnes by 2031 at 3.99% CAGR over 2026-2031. This solid up-trend mirrors an expanding processed-food base, escalating pharmaceutical serialization mandates, and a sharp rise in e-grocery logistics. Egypt’s 21% jump in 2024 processed-food exports propels demand for moisture- and oxygen-barrier pouches, while the UAE’s Federal Decree-Law No. 38 of 2024 obliges unit-dose pharmaceutical packs that require precise Arabic–English labeling and tamper evidence.[1]United Arab Emirates Legislations, “Federal Decree-Law Governing Medical Products,” uaelegislation.gov.ae Saudi Arabia slots localisation subsidies under Vision 2030, spurring resin conversion investments and renewable-energy powered plants, such as the EUR 7.6 million solar-assisted beverage facility in Jeddah. South Africa anchors the continent’s high-growth curve on the back of food-processing upgrades and the African Continental Free Trade Area, while Nigeria’s gas-to-chemicals complex opens an indigenous PE and PP stream that trims import dependence. Parallel consolidation—exemplified by the Amcor-Berry Global union—reshapes competitive intensity and speeds up innovation as converters race toward circular-economy compliance.

Key Report Takeaways

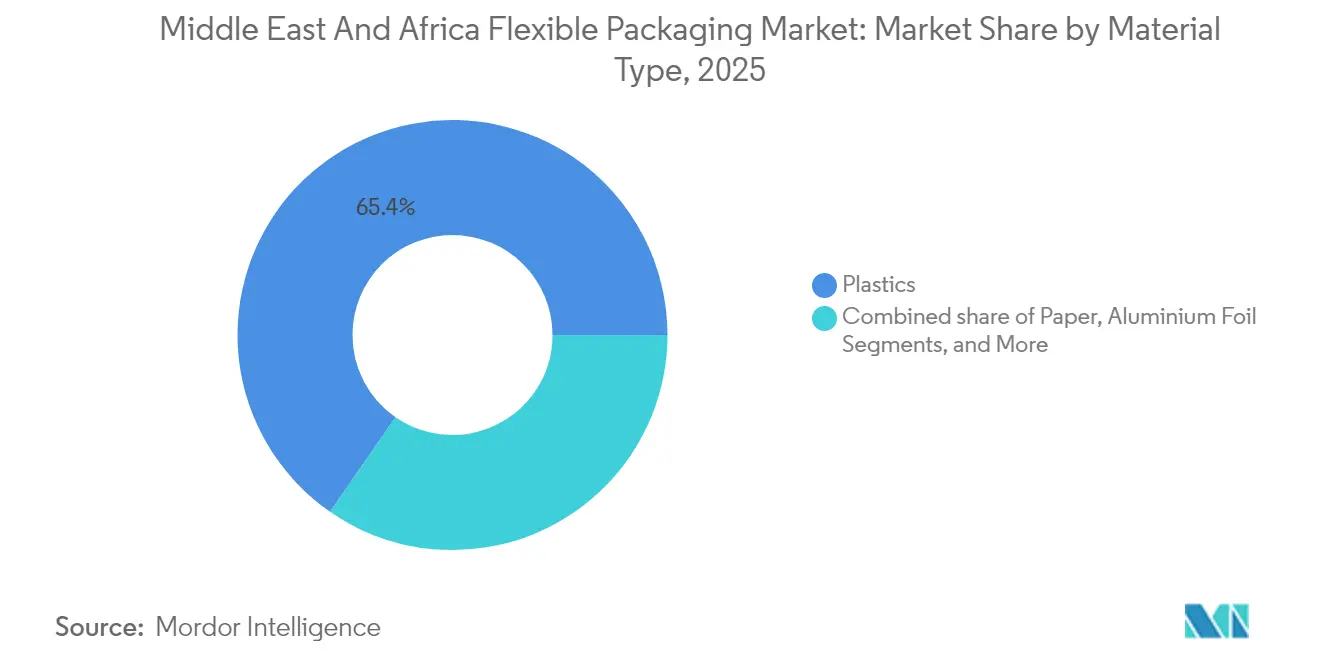

- By material type, plastics held 65.35% of the Middle East and Africa flexible packaging market share in 2025, whereas paper-based formats post the quickest 6.12% CAGR through 2031.

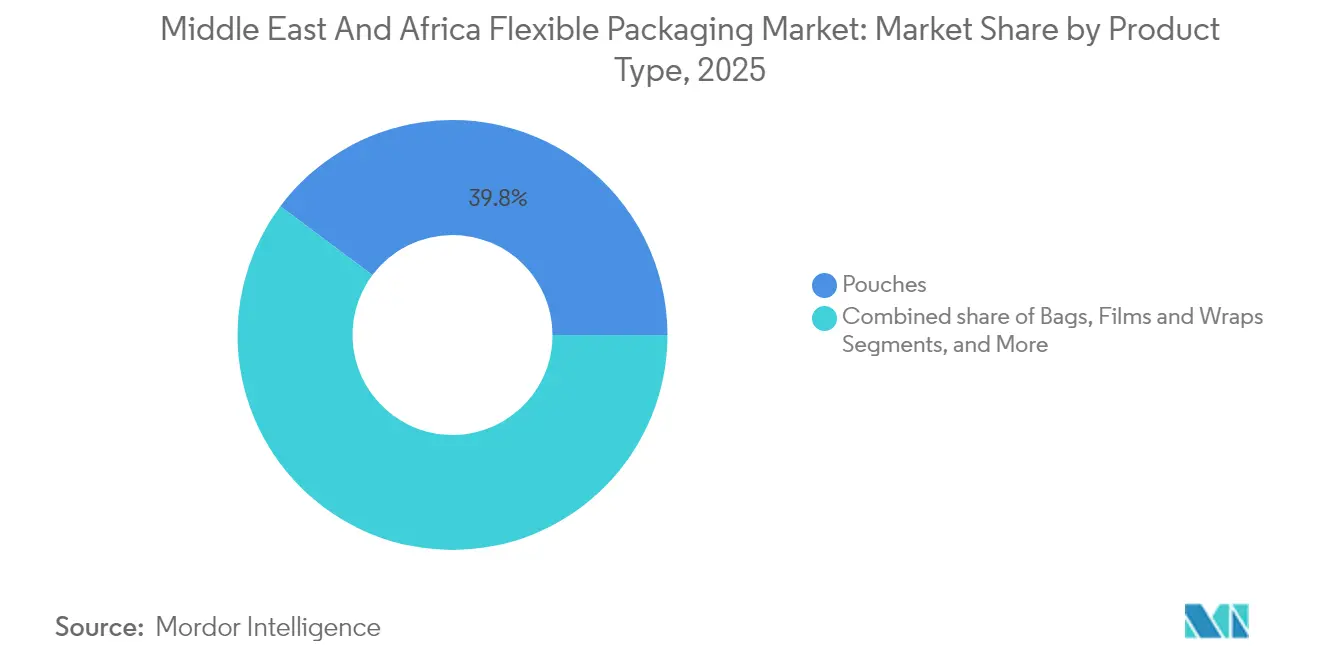

- By product type, pouches captured 39.78% of the Middle East and Africa flexible packaging market share in 2025; spouted pouches are expanding at a 7.18% CAGR for 2026-2031.

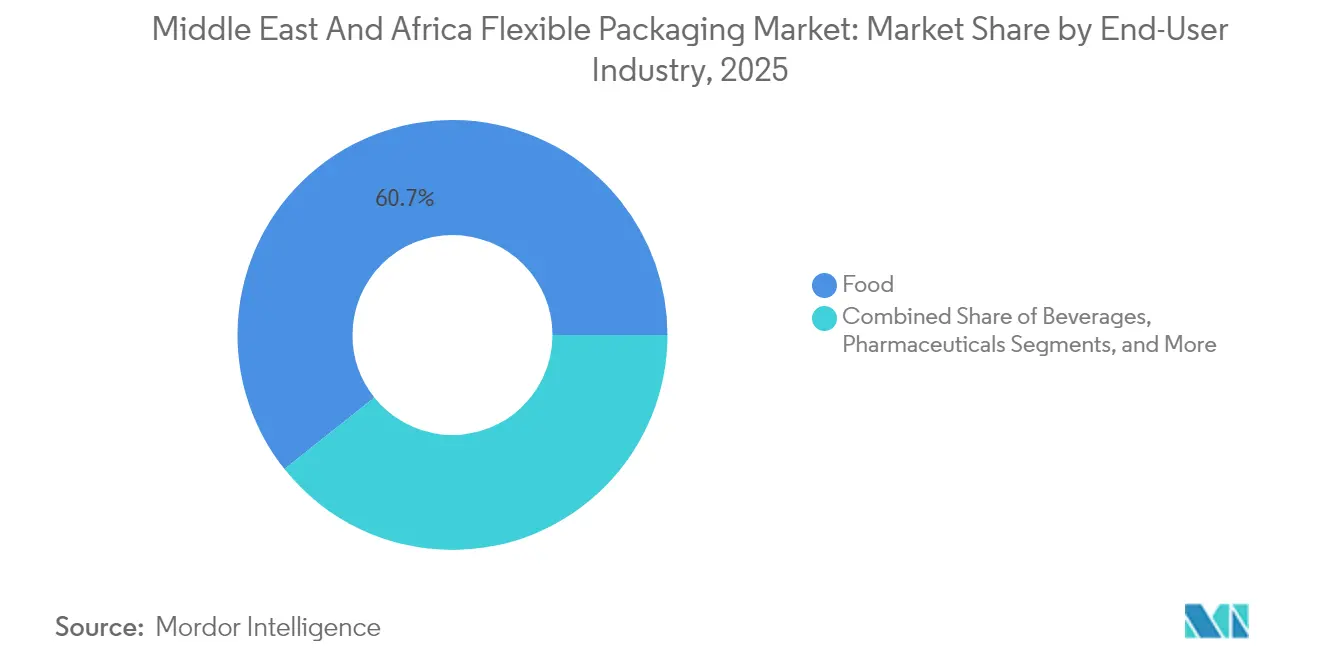

- By end-user industry, the food category accounted for 60.72% of the Middle East and Africa flexible packaging market size in 2025, while pharmaceuticals exhibit the leading 8.05% CAGR during the outlook period.

- By geography, Saudi Arabia commanded 44.98% revenue share in 2025; South Africa is set to progress at a 6.63% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC unit-dose pharma packaging mandates | +0.8% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| E-grocery boom driving mailer films | +0.6% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Halal processed-meat export expansion | +0.5% | Global focus on MEA | Medium term (2-4 years) |

| Mega food-park investments | +0.7% | Egypt, Nigeria, Africa | Long term (≥ 4 years) |

| On-the-go beverage surge | +0.4% | GCC, urban Africa | Short term (≤ 2 years) |

| FMCG localisation boosting converting capacity | +0.5% | Saudi Arabia, UAE, Egypt, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GCC Unit-Dose Pharma Packaging Mandates

The UAE’s decree-law imposes serialized, dual-language labeling that filters down to foil blisters, stick packs, and sachets. Saudi SASO halal marks add further validation layers, steering converters toward high-colour-strength CI-flexo and near-infra-red readable inks. Regionally harmonised codes mirror U.S. DSCSA rules, ensuring global alignment for biologics shipped in temperature-stable pouches. These conditions underpin persistent volume gains in the Middle East and Africa flexible packaging market.

E-Grocery Boom Driving Mailer Films in KSA and UAE

Grocery apps recorded USD 1.07 billion sales in the UAE during 2023; fulfilment centres now rely on padded mailers with ice-gel pockets for mixed ambient-chill orders.[2]U.S. Department of Agriculture, “Exporter Guide Annual: UAE,” apps.fas.usda.gov Riyadh research confirms that hybrid stores beat dark-store models on cost per order when insulated zipper pouches cut spoilage ratios by 7%. This rapid fulfilment model magnifies short-cycle demand swings that agile converters within the Middle East and Africa flexible packaging market can capture through digital print runs and late-stage customisation.

Halal Processed-Meat Export Expansion Needing Barrier Pouches

Ethiopian chilled goat carcasses now target 150 tonnes weekly to GCC retailers, yet shelf-life constraints expose outdated packaging. Multi-layer pouches with EVOH sit at the core of upgraded cold-chain compliance, enabling African suppliers to compete with Brazilian processors. Similar dynamics play out in fruit purée pouches bound for Dubai smoothie bars, where pineapple concentrate backed by a 5.3% CAGR through 2026 demands foil-free high-barrier laminates. These flows reinforce scale for the Middle East and Africa flexible packaging market.

Mega Food-Park Investments in Egypt and Nigeria

Egypt allocates USD 153 million to Suez Canal grain silos, generating orders for PE-lined woven PP sacks and FFS films. Nigeria’s USD 20 billion Ogidigben park yields cracker capacity for ethylene and propylene, lowering resin transport costs into West African pouch and sachet plants by 12%. The integrated supply architecture cements long-run competitive cost curves inside the Middle East and Africa flexible packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of food-grade recycled polymer feedstock | -0.6% | Global, acute in Africa | Long term (≥ 4 years) |

| Aluminium-foil import tariffs | -0.4% | Sub-Saharan Africa | Medium term (2-4 years) |

| Skill gap in CI-flexo high-speed printing | -0.3% | Middle East, North Africa | Medium term (2-4 years) |

| EU recyclability rules on multilayer exports | -0.5% | Export-focused MEA firms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Food-Grade Recycled Polymer Feedstock

Only 14% of worldwide plastic waste enters recycling streams; EFSA-grade PCR pellets fetch premiums of up to USD 400 per tonne above virgin levels, squeezing converter margins. EU rules that demand 70% recyclability by 2030 and rising PCR thresholds choke export lanes for multi-material laminates. UFlex’s PCR-PET line in Egypt supplies 30,000 tonnes annually but still covers less than 5% of regional laminate demand. Without scaled chemical recycling, growth in the Middle East and Africa flexible packaging market could moderate.

Aluminium-Foil Import Tariffs in Key African States

US antidumping duties on Turkish foil mirror nascent moves by East African blocs considering 5%-7% safeguard tariffs to stimulate local rolling mills. For sachet coffee and blister drugs, converters face 3%-5% unit-cost hikes, nudging them toward SiOx coated films, yet these alternatives demand new validation cycles that slow deployment. This cost friction trims near-term tonnage additions in the Middle East and Africa flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Lead, Paper Accelerates Toward Circularity

Plastics retained 65.35% dominance inside the Middle East and Africa flexible packaging market during 2025 as PE and PP deliver cost-effective moisture barriers for staples such as couscous, rice, and UHT milk. Meanwhile, coated kraft and machine-glazed paper surge at 6.12% CAGR, spurred by retailer mandates for mono-material curbside collection. Polyethylene-terephthalate laminates grow within retort soup pouches, underscoring heat-resistance advantages. The Middle East and Africa flexible packaging market size for mono-material PE/PE laminates is expected to rise once tie-layer resins unlock higher oxygen-barrier thresholds without EVOH.

PLA and PBAT blends surface in Qatar’s take-away bags, while sugar-cane PE trials emerge in South African yogurt lids. Yet cost premiums and compost-site scarcity keep market shares low. Multilayer foil structures remain indispensable in lidding for hummus and high-acid juices. At the same time, paper–film hybrids that use aqueous coatings reach moisture barrier targets, helping confectionery firms meet 25% virgin-plastic-reduction goals. Through this dynamic interplay, the Middle East and Africa flexible packaging market continuously balances economics, performance, and sustainability.

By Product Type: Pouches Dominate a Diversifying Portfolio

Pouches delivered 39.78% of 2025 shipment volume and continue to outperform with a 7.18% CAGR. Stand-up DOY pouches rule snack aisles, while quad-seal variants reinforce pet-food premiumisation. Retort pouches in Saudi halal soups illustrate thermal resilience, whereas spouted formats gain popularity in Nile Delta dairy drink launches. The Middle East and Africa flexible packaging market size for spouted pouches supporting beverage, paint, and agrochemical lines expands in tandem with filling-line flexibility. Mondi’s solvent-free re/cycle pouch line underscores the pivot to mono-material recyclability.

Films and wraps sustain bread-and-butter B2B contracts, covering stretch-hood pallets, shrink collation, and thermoform meat trays. Labels and sleeves enjoy digital-print uptake as HP Indigo 6K presses cut SKU changeover times for fast fashion yoghurt assortments. Lidding foils move toward PP-based easy-peel solutions, while zipper and slider components forge added convenience. Each development deepens product diversification in the Middle East and Africa flexible packaging market.

By End-User Industry: Food Retains Volume, Pharma Tops Growth

Food applications composed 60.72% of the Middle East and Africa flexible packaging market share in 2025, supported by stable demand for wheat, pulses, and confectionery. Egypt’s jam processors select clear PET-PE pouches targeting export gains in regions aligning with halal standards. Pharmaceuticals accelerate at an 8.05% CAGR as GCC regulators compel serialized blister packs and cold-chain sachets.

Beverage pouches flourish on school-lunch convenience, while cosmetics firms in Dubai pivot to matte-finish stand-up pouches that pair shelf impact with recyclability. Household cleaners and agrochemical sachets hold steady volumes, illustrating demand spread that shields the Middle East and Africa flexible packaging market from single-category shocks.

Geography Analysis

TSaudi Arabia’s 44.98% slice of 2025 revenue springs from beefed-up halal meat, dairy, and snack lines served by newly installed 10-colour CI-flexo presses. Solar-powered filling halls in Jeddah highlight ecological commitments that resonate across the Middle East and Africa flexible packaging market. The UAE, often the test-bed for premium designs, leverages USD 1.07 billion e-grocery turnover to push mailer films, dry-ice pouches, and insulated liners. Bahrain, Qatar, Kuwait, and Oman remain niche yet profit-rich markets thanks to strict import rules that favour high-quality multilayer films. Tamkeen-supported expansion of United Paper Industries underscores micro-market capacity gains.

Africa commands the growth narrative. South Africa tops regional CAGR at 6.63%, propelled by snack-food and ready-meal adoption and bolstered by trade corridors linking ports to hinterland supermarket chains. Egypt blends Suez Canal geography with crop field modernisation, creating anchor demand for bulk sacks, pallet hoods, and pre-made pouches tied to its USD 6.1 billion processed-food export milestone. Morocco and Tunisia align with EU recycling thresholds, refitting lamination lines toward mono-material paper–PE hybrids to sustain citrus export packaging flows.

ALPLA’s facilities in KSA, UAE, and Egypt cut lead times for PET preforms, while renewable-energy projects in Morocco and the UAE reduce carbon intensity in blown-film extrusion. The Middle East Institute notes that green-power commitments target 52% renewable grids by 2030, lowering Scope 2 emissions for converters. Such regional integration ensures growth momentum across the Middle East and Africa flexible packaging market.

Competitive Landscape

Top Companies in Middle East and Africa Flexible Packaging Market

Huhtamaki, Constantia Flexibles, and Mondi hold technology edges in retortable, high-oxygen-barrier laminates and in-house recycling loops. The Amcor-Berry merger births a USD 24 billion revenue giant with planned USD 650 million synergies that will leverage backward-integrated film and converting assets to expand its footprint in the Middle East and Africa flexible packaging market. Sonoco’s USD 3.9 billion Eviosys deal and One Rock’s Constantia buyout further raise the bar for capital efficiency and R&D outlay.

Napco National and 3P Gulf Group win local tenders on Arabic artwork fluency and 24-hour technical service. Arabian Flexible Packaging rolls out solvent-free lamination lines to cut VOC emissions, matching retailer scorecards. ePac Flexibles scales digital print clusters in Johannesburg and Dubai, offering 10-day doorway delivery for minimum 5 kg jobs that serve SME spice blenders.

Bobst’s Florence competence centre trains 200 Middle Eastern operators yearly on precision gear settings to close skill gaps in CI-flexo. Hotpack’s USD 100 million New Jersey plant marks global ambition from a Gulf base, while ALPLA’s full takeover of its Egyptian JV cements integrated resin-to-bottle offerings that reduce cost-to-serve for beverage clients. Competitive intensity spurs sustained capex flows, keeping the Middle East and Africa flexible packaging market technologically current.

Middle East And Africa Flexible Packaging Industry Leaders

Napco National

3P Gulf Group

Platinum Packaging Ltd

ENPI Group

Aalmir Plastic Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Amcor closed the Berry deal, forming a USD 24 billion packaging major with USD 650 million synergy potential.

- May 2025: Hotpack disclosed a USD 100 million United States investment to create 200 jobs and broaden its food packaging range.

- February 2025: Amcor and Berry Global shareholders approved a share-swap transaction (7.25 Amcor shares per Berry share) that finalised in June 2025.

- January 2025: Faller Packaging purchased property in Gebesee, Germany, for a new folding-carton and leaflet plant, addressing sharp demand from Gulf pharmaceutical importers.

Middle East And Africa Flexible Packaging Market Report Scope

Flexible packaging refers to any package or portion of a package that can easily change its shape when filled or being utilized. Flexible packaging is made from combinations of paper, plastic, film, aluminum foil, or other materials and consists of bags, pouches, liners, wraps, roll stock, and other flexible items.

The Middle East and Africa flexible packaging market is segmented by material type (plastics (Polyethylene (PE), Polypropylene (PP), Polyethylene terephthalate (PET), other plastics (PVC, PA, etc.)), paper, aluminum, compostable materials (PLA, PBS, PHA, PBAT, etc.), product type (pouches, films and wraps [thermoforming film, stretch films, shrink film, cling film], labels and sleeves, lidding and liners, blister packaging), end-user verticals (food, beverages, pharmaceuticals, cosmetics and personal care, household care, pet care, tobacco, other end-user industries (electronics, chemicals, agricultural products, etc.)), and Country (Saudi Arabia, United Arab Emirates, Morocco, Egypt, South Africa, and the rest of the Middle East and Africa). The report offers market forecasts and size in volume (tonnes) for all the above segments.

By Material Type

| Plastics | Polyethylene (HDPE, LDPE, LLDPE) |

| Polypropylene | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Others (EVOH, PA, etc.) | |

| Paper | |

| Aluminium Foil | |

| Bioplastics / Compostables (PLA, PBS, PHA, PBAT) |

By Product Type

| Pouches | Stand-up Pouches |

| Retort Pouches | |

| Spouted Pouches | |

| Bags | |

| Films and Wraps | Thermoforming film |

| Stretch Films | |

| Shrink Film | |

| Laminate film | |

| Cling films ( limited to B2B like restaurants, hotels , etc )] | |

| Labels and Sleeves | |

| Lidding and Liners | |

| Blister Packaging |

By End-user Industry

| Food | Meat and Poultry |

| Dairy | |

| Snacks and Confectionery | |

| Fruits and Vegetables | |

| Beverages | Alcoholic |

| Non-alcoholic | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Household and Industrial Care | |

| Tobacco | |

| Pet Food | |

| Others (Electronics, Chemicals, Agri-products) |

By Country

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | Egypt |

| Morocco | |

| Algeria | |

| Tunisia | |

| South Africa | |

| Rest of Africa |

| By Material Type | Plastics | Polyethylene (HDPE, LDPE, LLDPE) |

| Polypropylene | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride (PVC) | ||

| Others (EVOH, PA, etc.) | ||

| Paper | ||

| Aluminium Foil | ||

| Bioplastics / Compostables (PLA, PBS, PHA, PBAT) | ||

| By Product Type | Pouches | Stand-up Pouches |

| Retort Pouches | ||

| Spouted Pouches | ||

| Bags | ||

| Films and Wraps | Thermoforming film | |

| Stretch Films | ||

| Shrink Film | ||

| Laminate film | ||

| Cling films ( limited to B2B like restaurants, hotels , etc )] | ||

| Labels and Sleeves | ||

| Lidding and Liners | ||

| Blister Packaging | ||

| By End-user Industry | Food | Meat and Poultry |

| Dairy | ||

| Snacks and Confectionery | ||

| Fruits and Vegetables | ||

| Beverages | Alcoholic | |

| Non-alcoholic | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Household and Industrial Care | ||

| Tobacco | ||

| Pet Food | ||

| Others (Electronics, Chemicals, Agri-products) | ||

| By Country | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Morocco | ||

| Algeria | ||

| Tunisia | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Middle East and Africa flexible packaging market?

The market stands at 6.83 million tonnes in 2026 and is projected to reach 8.31 million tonnes by 2031, translating into a 3.99% CAGR

Which material type dominates the Middle East and Africa flexible packaging market?

Plastics remain dominant with 65.35% share in 2025, though paper-based formats are growing fastest at a 6.12% CAGR through 2031.

Why are pharmaceuticals the fastest-growing end-user segment?

GCC regulators have enforced unit-dose serialization, dual-language labeling, and halal certification, boosting demand for high-barrier blisters and sachets and driving an 8.05% CAGR in pharma packaging.

How will local resin capacity additions in Nigeria affect regional supply?

Nigeria’s Ogidigben Industrial Park introduces indigenous PE and PP streams, lowering feedstock import reliance and freight costs for West African converters.

What impact will EU recyclability rules have on Middle East and Africa flexible packaging exporters?

Exporters of multilayer structures must shift toward mono-material and recyclable laminates to meet a 70% recyclability threshold by 2030, or risk losing EU market access.

How does the Amcor-Berry Global merger influence regional competition?

The USD 24 billion revenue entity increases scale and technology reach, heightening pressure on local players yet also introducing advanced recycling and downgauging solutions into the region.

Page last updated on: