Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

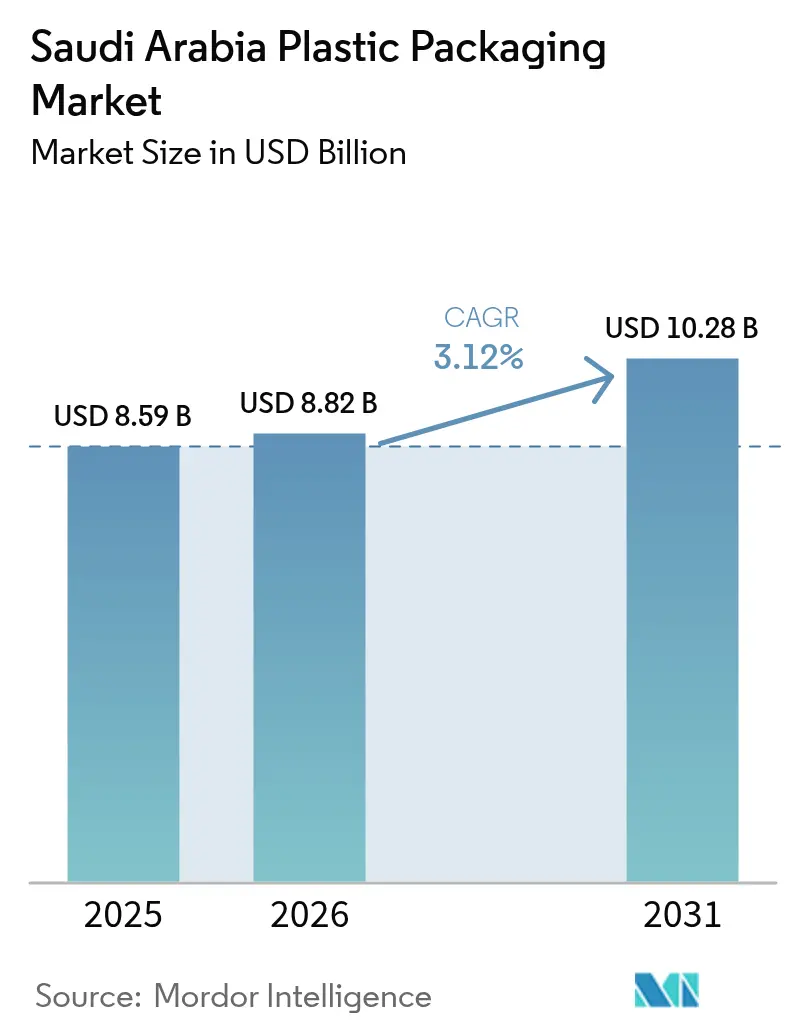

| Base Year Market Size (2025) | USD 8.59 Billion |

| Market Size (2026) | USD 8.82 Billion |

| Market Size (2031) | USD 10.28 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

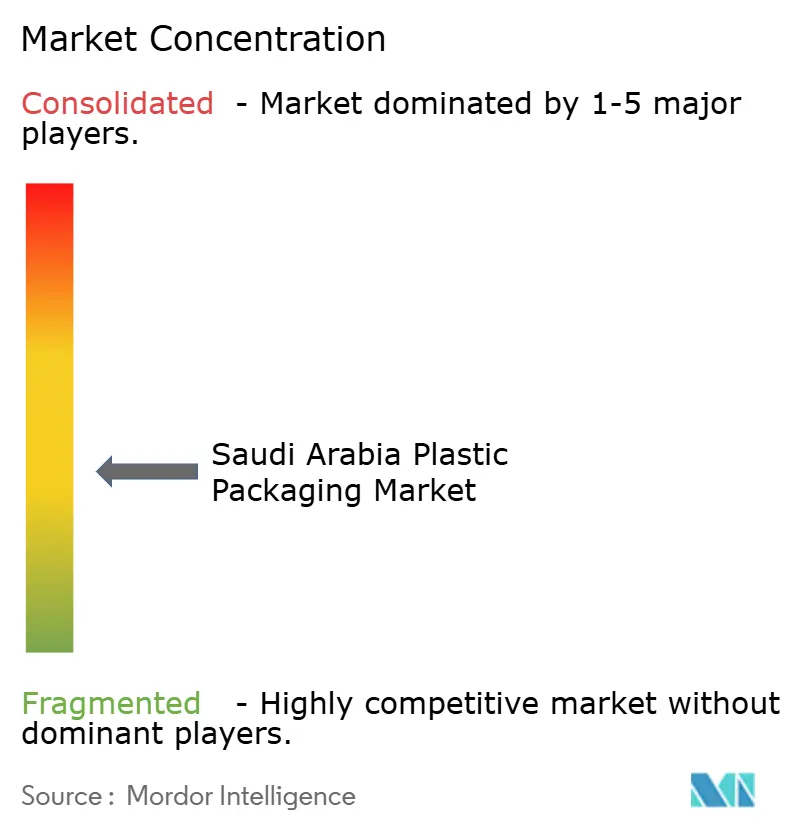

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Plastic Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia plastic packaging market size is expected to grow from USD 8.59 billion in 2025 to USD 8.82 billion in 2026 and is forecast to reach USD 10.28 billion by 2031 at a 3.12% CAGR over 2026-2031. Vision 2030’s push for downstream industrialization is redirecting resin streams from bulk export toward higher-value packaging, moderating volume growth while lifting value capture. Converters are accelerating capital spending on multilayer blown film, stretch-blow molding, and lightweight preforms as e-commerce, modern retail, and the hospitality sector scale demand for portion-controlled packs. Brand owners now favor certified recycled content that meets food-contact regulations, reshaping procurement and strengthening the negotiating power of converters able to secure rPET and rPE supply. Although crude-linked resin volatility threatens small players' margins, subsidized energy, land, and financing in the Ras Al Khair and NEOM clusters partially offset this risk and underpin the next wave of capacity additions.

Key Report Takeaways

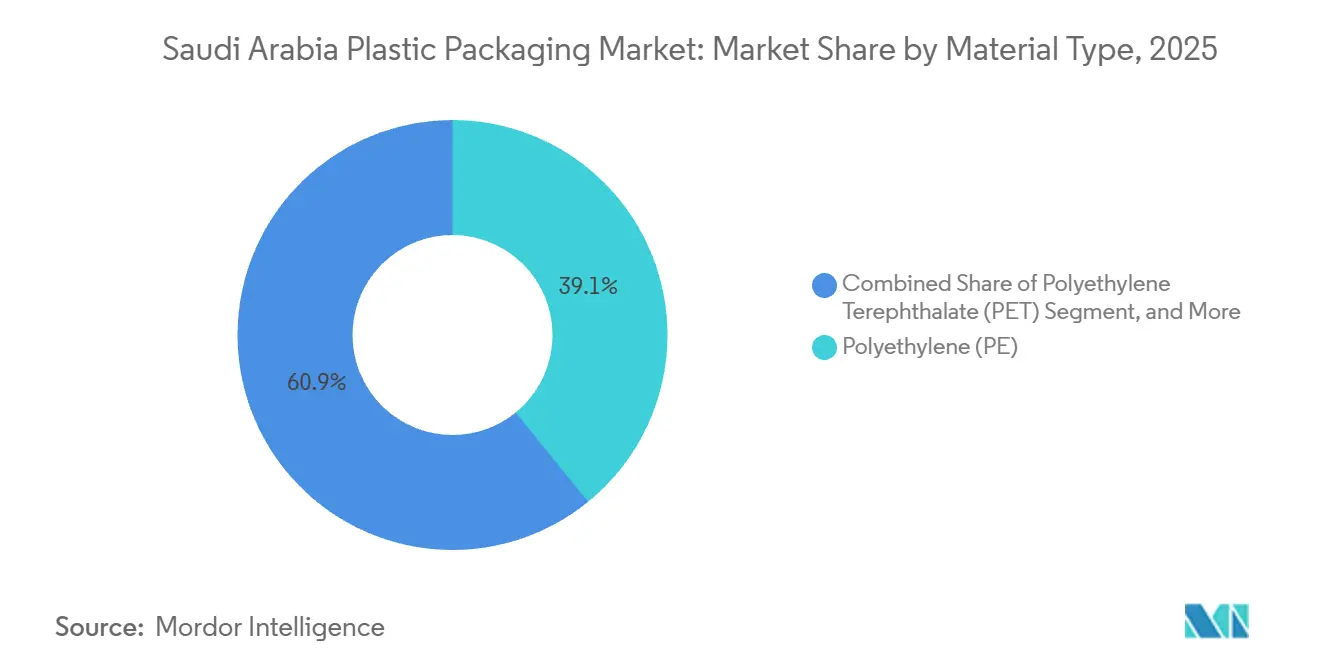

- By material type, polyethylene commanded 39.13% of the Saudi Arabia plastic packaging market share in 2025, while polyethylene terephthalate is forecast to expand at a 4.31% CAGR through 2031.

- By packaging type, flexible formats led with 54.56% of the market share in 2025 and is projected to advance at a 4.26% CAGR to 2031.

- By product form, films and wraps held 32.31% of the Saudi Arabia plastic packaging market size in 2025 and will post the fastest 4.67% CAGR through 2031.

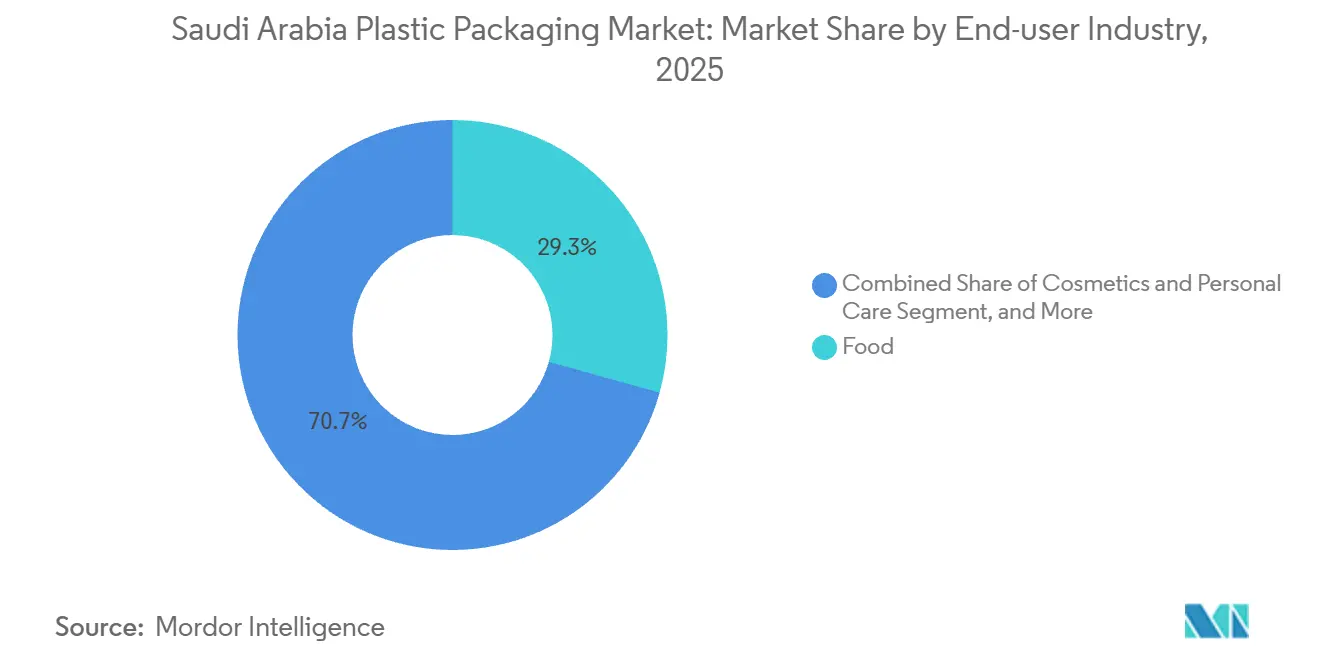

- By end-user industry, food led with 29.32% of the market share in 2025, whereas cosmetics and personal care segment is expected to record the highest 5.12% CAGR during 2026-2031.

- By manufacturing process, extrusion accounted for 30.14% share of the Saudi Arabia plastic packaging market size in 2025 and is set to grow at a 5.41% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from Food and Beverage Sector for Convenient Lightweight Packaging | +0.9% | National, with concentration in Riyadh, Jeddah, Dammam metro clusters | Medium term (2-4 years) |

| Expansion of E-Commerce and Modern Retail Accelerating Flexible Packaging Uptake | +0.7% | National, with early gains in Riyadh, Jeddah, and Eastern Province | Short term (≤ 2 years) |

| Government Regulations Promoting Oxo-Biodegradable Plastics Compliance | +0.5% | National, enforced through Ministry of Environment, Water and Agriculture oversight | Long term (≥ 4 years) |

| Growing Pharmaceutical Manufacturing Under Vision 2030 Boosting Sterile Packaging | +0.4% | National, with pharmaceutical clusters in Riyadh and Jeddah | Medium term (2-4 years) |

| Localization Incentives for Polymer Conversion in Ras Al Khair and NEOM Clusters | +0.3% | Regional, focused on Ras Al Khair Industrial City and NEOM | Long term (≥ 4 years) |

| Surge in Date Exports Driving High-Barrier Multilayer Pouch Adoption | +0.2% | National, with production concentrated in Al-Ahsa, Qassim, and Madinah regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Food And Beverage Sector for Convenient Lightweight Packaging

Saudi food retail surpassed USD 64.7 billion in 2024 and continues to gain from snacks, dairy, and ready-meal formats that rely on portion-controlled pouches. Domestic processors still import multilayer barrier films because much of the local base is limited to three-layer lines, opening prospects for converters installing seven- and nine-layer equipment. The Ministry of Environment, Water, and Agriculture now enforces tamper-evident closures and oxygen scavengers for chilled products, lifting the technical hurdle for new entrants. Brand owners willingly pay premiums of 10-15% to secure packaging containing ISCC PLUS-certified rPET when food-contact compliance is assured. Lighter packs that cut freight costs have become a decisive differentiator as fuel subsidies decline and third-party logistics rates harden.

Localization Incentives for Polymer Conversion in Ras Al Khair and NEOM Clusters

Ras Al Khair and NEOM offer subsidized land, discounted utilities, and access to deepwater ports, yet converter response stays cautious without firm off-take contracts from anchor tenants. The Saudi Industrial Development Fund extends below-market loans for projects over SAR 50 million, favoring large-scale extrusion and molding investments.[1]“Vision 2030 Industrial Development Financing Programs,” Saudi Industrial Development Fund, sidf.gov.sa NEOM’s circular economy blueprint obliges applicants to demonstrate closed-loop feedstock plans, adding complexity and up-front cost for smaller converters. Proximity to Saudi Aramco and SABIC petro-complexes trims feedstock haulage, giving investors a delivered-resin advantage over imported pellet scenarios. Nevertheless, shortages of skilled technicians and limited vocational programs mean many firms still rely on expatriate labor, partly offsetting cost savings from incentives.

Government Regulations Promoting Oxo-Biodegradable Plastics Compliance

The Ministry of Environment, Water and Agriculture introduced additive requirements for single-use plastics, but product-by-product timelines remain uneven.[2]“Circular Economy Regulations and Initiatives,” Ministry of Environment, Water and Agriculture (KSA), mewa.gov.sa Multinational brands demand ASTM D6954 or ISO 17088 validation, whereas domestic value brands often adopt lower-cost blends lacking independent proof of degradation. Municipal audits uncover non-compliant bags, yet inconsistent testing protocols mean that enforcement success varies widely across governorates. Saudi participation in the Global Plastics Treaty talks signals eventual convergence toward EU-style single-use directives, likely introducing extended producer responsibility fees that reward certified packs. Converters investing early in PLA or PBAT formulations face short-term cost headwinds but position themselves for long-run regulatory tailwinds once subsidy schemes mature.

Growing Pharmaceutical Manufacturing Under Vision 2030 Boosting Sterile Packaging

Vision 2030 aims to raise local drug production to 40% of domestic demand by 2030, up from 20% in 2024, which stimulates blister, vial, and sterile pouch requirements. Converters must retrofit cleanrooms and qualify under FDA and EMA-aligned GMP, increasing capex but locking in above-average margins. Medical-grade polypropylene and polyethylene supplied by SABIC shorten lead times and stabilize resin cost, allowing local players to displace imports in primary packs.[3]“SABIC TRUCIRCLE Portfolio Targets 1 Million Tonnes of Circular Materials by 2030,” SABIC, sabic.com Rapid uptake of biologics and temperature-sensitive medicines is driving demand for cold-chain shippers with phase-change linings that maintain 2-8 °C for 48 hours, an area currently dominated by foreign specialists. ISO 15378 certification becomes a commercial gatekeeper, capping market entry and supporting a premium pricing structure across sterile packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Crude-Derived Resin Prices Squeezing Converter Margins | -0.6% | National, affecting all polymer-dependent converters | Short term (≤ 2 years) |

| Low Domestic Plastic Recycling Infrastructure Limiting Circular Packaging Adoption | -0.4% | National, with acute gaps in collection and sorting infrastructure | Long term (≥ 4 years) |

| Water Rationalization Initiatives Reducing Bottled-Water Demand | -0.2% | National, with strongest impact in municipal water service areas | Medium term (2-4 years) |

| Import Duty Exemptions for Paper-Based Substitutes Eroding Plastic Share | -0.3% | National, affecting dry food and non-food packaging categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Derived Resin Prices Squeezing Converter Margins

When Brent crude dips below USD 70 per barrel, Saudi ethane-based crackers lose part of their cost edge versus Asia’s naphtha units, lifting domestic PP and PE quotes by 20-30% in weeks. Converters, which typically run on 8-12% gross margins, struggle to re-price contracts with FMCG customers locked into quarterly tenders. Premium recycled resins often command higher premiums during supply squeezes, further compressing margins for converters servicing sustainability-minded brands. SABIC offers quarterly pricing for local clients, but export-oriented converters buying spot specialty grades face even sharper swings. To cope, larger players deploy hedging or resin swap agreements; small converters lacking treasury capacity defer upgrades, perpetuating technology and profitability gaps within the Saudi Arabia plastic packaging market.

Low Domestic Plastic Recycling Infrastructure Limiting Circular Packaging Adoption

Only 5% of the kingdom’s 53 million tonnes of solid waste is recycled, producing a chronic shortage of high-quality post-consumer feedstock. The 300,000 tpa PET facility commissioned in 2024 must still import baled bottles from Europe and North America, exposing operations to freight spikes and FX risk. Without deposit-return schemes, collection purity lags European curbside standards, undermining yields and raising rPET prices above virgin resin in some months. Informal collectors cherry-pick clear PET and HDPE, leaving mixed streams that demand high-cost re-sortation, eroding economics for food-grade output. Until extended producer responsibility programs materialize, converters will rely on imports for rPET and rPE, limiting circular content penetration despite brand ambition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PET Gains On Lightweight Beverage Shift

Polyethylene led with 39.13% of the market share in 2025, anchored in shopping bags and stretch film, yet its earnings remain sensitive to commodity swings and margin pressure from duty-free LDPE imports. Polyethylene terephthalate will post the strongest 4.31% CAGR to 2031 as bottled-water and carbonated-drink producers opt for lighter PET bottles that cut freight costs and align with recycling goals. The Saudi Arabia plastic packaging market size linked to PET rises further as rPET integration boosts demand for food-grade flake certified under EFSA rules. Polypropylene preserves share in dairy tubs and microwaveable ready meals where heat resistance and stiffness justify its premium. Specialty barrier resins such as EVOH, PA, and PVDC remain small but strategic, enabling converters to win high-margin export pouches for dates and processed meat.

In the next five years, resin use is expected to shift toward higher-performance grades such as mLLDPE and rPET, which allow downgauging without sacrificing mechanical properties, thereby lowering total system cost. Converters investing in twin-screw extruders that compound tie-layer additives on-site achieve formulation agility and faster turnaround on custom film structures. Domestic suppliers are working with research centers to scale bio-based PE derived from ethanol, a development that could diversify feedstock sources if commercial economics improve. Material selection decisions will increasingly weigh life-cycle assessment results as brand owners publish scope-3 carbon targets covering packaging. As these pressures converge, smaller converters with limited technical bandwidth may exit commodity PE to focus on contract tolling or niche PVC blisters where competition is lighter.

By Packaging Type: Flexible Formats Capture E-Commerce Gains

Flexible packaging owned 54.56% share in 2025 and is expected to expand at a 4.26% CAGR through 2031 because retailers migrate from rigid jars to laminated pouches that improve cube efficiency. Stand-up pouches with zippers, spouts, and laser-score openings enhance convenience for sauces and baby foods, securing shelf visibility in crowded aisles. Rigid PET bottles remain essential in beverages and household cleaners, but aggressive lightweighting trims grams per unit, tempering revenue. Recyclable mono-material PE and PP films debut in snack food, narrowing the sustainability gap with rigid containers and positioning flexible packs for deposit-return inclusion. ISO 22000 audit requirements steer volume toward certified converters, pruning informal laminators from modern-retail supply chains.

Through 2031, the Saudi Arabia plastic packaging market will also observe quick-commerce firms demanding pouch formats optimized for belt-sortation and robotic picking, prompting redesign of gusset structures to prevent roll-off. Multi-layer laminates with EVOH or PVDC will face scrutiny as regulators push for single-polymer solutions that simplify recycling streams, forcing converters to invest in high-barrier PE coatings. Flexible formats gain another edge as rising electric-vehicle logistics fleets prioritize payload efficiency to maximize range, rewarding every gram saved in primary packs. On the rigid side, tethered caps mandated by EU import markets drive molding upgrades that integrate hinge components, marginally raising cost but improving post-consumer collection. Consequently, converters operating both flexible and rigid lines diversify revenue while hedging regulatory and substrate risk.

By Product Form: Films And Wraps Lead On Automation Investments

Films and wraps segment is projected to grow at 4.67% CAGR to 2031 as dairy and snack makers automate with high-speed horizontal form-fill-seal lines requiring tight-tolerance rolls. Saudi Arabia plastic packaging market share for pouches and sachets already sits at 32.31%, but capacity additions in Dammam and Jeddah will escalate rivalry and push down tolling spreads. Bottles continue dominating beverages, edible oils, and condiments, though 500 ml water preforms now weigh only 18 grams versus 23 grams in 2019. Thermoformed PET and PP trays win in fresh produce and baked goods, offering microwave-safe clarity that flexible packs cannot replicate. Converters look to value-added liners and resealable lidding to differentiate amid growing commoditization of mono-layer film supply.

Over the forecast horizon, pallet-stretch wrap demand will benefit from warehouse automation that favors machine-grade films offering consistent elongation and puncture resistance. Multi-lane vertical form-fill-seal systems in spice and coffee plants will sustain sachet volumes, though recyclability mandates push vendors toward mono-material laminates. Label-stock films gain importance as beverage brands adopt shrink-sleeve decorations supporting intricate graphics for limited-edition runs tied to sports sponsorships. In the bottle segment, advanced nucleation additives allow faster PET preform cooling, lifting line throughput and partially offsetting the revenue impact of lightweighting. High-moisture-barrier wraps for fresh meat capitalize on rising protein consumption among affluent households and become a niche growth pocket for EVOH-based coextrusions.

By End-User Industry: Cosmetics Outpaces Food On Premiumization

Food accounted for 29.32% of market share in 2025, yet household price sensitivity curtails growth as VAT hikes and subsidy rationalization squeeze disposable income. Cosmetics and personal care will grow fastest at 5.12% CAGR to 2031, reflecting a rise in female workforce participation and social-media influence that lifts premium skincare and fragrance volumes. Premium brands require airless pumps, metallized labels, and small-run SKUs, favoring converters with injection-molding precision and digital printing. Beverage demand tracks tourism expansion; hotels and restaurants fuel PET bottle uptake, partially offsetting municipal tap-water campaigns that dampen urban bottled-water consumption. Pharmaceutical packs capture high margins under Vision 2030 localization, while industrial sacks and liners trail as they face substitution by woven polypropylene and bulk containers.

Looking ahead, nutraceutical gummies and functional beverages marketed toward wellness-focused youth are expected to generate incremental volume requiring moisture-barrier pouches and light-blocking bottles. Halal-certified cosmetics slated for export to Southeast Asia demand tamper-evident labeling and dual-language inserts, raising complexity for pack design. Pharma demand will shift toward unit-dose formats for chronic-disease therapies, intensifying call for blister webs with advanced push-through strength and foil-seal integrity. Foodservice chains experimenting with home-compostable cutlery and condiment sachets could gradually erode commodity PP utensil orders but open an avenue for PLA and PHA plastics. In industrial chemicals, stricter UN transport regulations push for durable HDPE drums with RFID tags that track reuse cycles, adding an electronics component to traditional plastic packaging.

By Manufacturing Process: Extrusion Leads On Multilayer Demand

Extrusion secured 30.14% share in 2025 and will climb 5.41% CAGR through 2031 as converters invest in nine-layer film lines that integrate EVOH and tie layers for date export pouches. Stretch-blow molding supports lighter PET bottles that save up to 22% resin versus 2019 norms and help beverage fillers hit carbon-reduction targets. Injection molding’s growth aligns with surge in cosmetics and personal-care closures, requiring high-cavity molds and in-mold labeling know-how. Thermoforming holds niche but profitable ground in high-clarity trays for ready meals and pharma blister-lidding, yet must contend with mono-material flexible packs that lower total pack mass. Rotational and compression molding remain marginal, servicing specialty industrial items where cycle times and part counts cannot justify large capital outlays.

In the medium term, blown-film lines equipped with online thickness mapping and melt-pump control will lower scrap rates, enhancing competitiveness of the Saudi Arabia plastic packaging market against imports from UAE and Egypt. Extrusion-coating of paperboard with bio-based PE emerges as a hybrid solution replacing wax-coated cartons in takeaway food, offering recyclability in mixed paper streams. Stretch-blow molders are trialing rPET percentages above 50% without haze penalties by adopting advanced drying systems and chain-extender additives. Injection-molded thin-wall containers gain from high-speed robots that reduce labor while achieving gate-to-gate cycle times under 3.5 seconds, unlocking new snack and deli applications. Across processes, plants adopting predictive maintenance based on vibration analytics report uptime gains above 8%, freeing capacity for higher-margin short-run jobs.

Geography Analysis

Riyadh, Jeddah, and Dammam together generate more than 70% of national converter capacity, anchored by dense consumer populations, international airports, and seaports that streamline raw-material and finished-goods flows. These metros house most FMCG and pharmaceutical plants, guaranteeing stable pull for both flexible and rigid formats servicing daily consumption categories. Eastern Province benefits from immediate access to cracker output at Jubail, allowing converters to secure feedstock at lower delivered cost than inland rivals and strengthening the regional competitiveness of the Saudi Arabia plastic packaging market. Retail chains cluster distribution centers around Riyadh for same-day fulfillment across central provinces, increasing throughput of stretch film, pallet wrap, and e-commerce mailers. Government urbanization programs that extend public transport and mixed-use developments further enlarge packaged-goods demand in these flagship cities.

Ras Al Khair and NEOM industrial zones promise subsidized land leases, utility discounts, and streamlined customs, yet several prospective projects remain in memorandum stage because long-term offtake agreements with anchor tenants are still under negotiation. Converters considering entry must weigh the incentive savings against start-up risks tied to labor availability, infrastructure readiness, and uncertain demand timing linked to phased NEOM population targets. Nevertheless, proximity to deepwater King Salman Global Maritime Complex and planned rail corridors offers long-run export leverage once production stabilizes. Investors also eye NEOM’s circular mandates that require closed-loop solutions, giving early movers in mechanical and chemical recycling a potential regulatory moat. Training partnerships with technical institutes are expected to narrow the skilled-labor gap, though imports of expatriate engineers remain essential during ramp-up.

Rural regions such as Al-Ahsa, Qassim, and Madinah command fewer converters but feature concentrated agribusiness activities such as date processing, dairy, and poultry that necessitate barrier pouches, stretch film, and rigid HDPE crates. Limited municipal recycling services in these areas force processors to truck scrap to urban balers, increasing logistics cost and complicating attainment of recycled-content targets. Informal waste-picker networks dominate collection of high-value PET and HDPE, creating unpredictable bale quality that challenges consistent rPET and rPE supply for rural fillers. Government plans to introduce deposit-return schemes nationwide could lift collection rates, but success depends on harmonized rollout and adequate reverse-logistics capacity. Improved road links under the National Transport Strategy will shorten lead times between rural packhouses and central distribution centers, indirectly boosting demand for transport-protective films and insulated shippers.

Competitive Landscape

The Saudi Arabia plastic packaging market operates in moderately fragmented structure where SABIC sets the tone through resin pricing, application development, and preferential allocation of TRUCIRCLE certified circular streams. Large converters such as Napco National, Obeikan, and Al Watania hold multi-plant footprints that span blown film, injection molding, and label conversion, enabling integrated supply across food, beverage, and pharmaceutical verticals. International majors like Amcor and Sealed Air leverage global R&D to introduce active-barrier coatings, ultra-thin PE sealing layers, and mono-material laminates that local rivals often license rather than replicate. Equipment suppliers from Europe and Asia compete to install state-of-the-art nine-layer and stretch-blow lines, with many deals bundled into Saudi Industrial Development Fund financing packages that lower project payback. Sustained capital inflows underpin a pipeline of upgrades that sharpen domestic competitiveness against neighboring UAE converters.

Joint ventures proliferate as foreign groups comply with 30% local-content regulations; these structures accelerate technology transfer but dilute foreign equity returns, sometimes slowing board approvals for capex. Partnerships often assign downstream converting to Saudi partners while upstream printing and design know-how remains with multinational parents, creating complex royalty agreements. Meanwhile, mid-tier firms serving commodity films and bags face mounting compliance costs related to food-safety audits and oxo-biodegradable testing, which squeeze thin margins and may spur consolidation. E-commerce marketplaces disrupt the traditional distributor model as micro-brands bypass wholesalers to source printed pouches directly from converters, appropriating margin that previously resided in the middle of the chain. On balance, scale, certification credentials, and digital readiness emerge as decisive factors for long-term survival in the Saudi Arabia plastic packaging market.

Sustainability now determines tender eligibility; brand owners demand verifiable chain-of-custody documentation to prove rPET or chemically recycled feedstock origin and conduct surprise audits to validate declarations. Converters with integrated recycling back-loops or long-term rPET supply contracts secure price premiums and win multiyear agreements, whereas those lacking access to certified circular resin risk relegation to price-fighting commodity categories. Technology adoption remains uneven; while leading plants deploy IoT sensors on extruders and predictive maintenance on compressors, smaller facilities still rely on manual gauge checks and reactive troubleshooting. Over the medium term, plants embracing ERP-linked scheduling, digital twin simulation, and closed-loop process control will post higher asset turns and customer-service scores. These operational gains, combined with recycled-content credibility, are expected to widen the competitive gap and consolidate market share among the top ten players.

Saudi Arabia Plastic Packaging Industry Leaders

Napco National

Zamil Plastic Industries Co.

Sealed Air Saudi Arabia Co. Ltd

Takween Advanced Industries

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SABIC and Alpek produced the first commercial batch of food-grade rPET derived from chemical-recycling oil at a pilot unit in Jubail, validating closed-loop supply for domestic beverage brands.

- January 2026: The Ministry of Environment, Water and Agriculture launched a nine-month deposit-return pilot covering PET bottles in Riyadh and Jeddah, offering SAR 0.10 refunds per container and installing 600 reverse-vending machines across both cities.

- October 2025: Napco National started up a digital-printing flexible-packaging line based on HP Indigo 25K technology, enabling economic production of runs below 5 000 m² for e-commerce and promotional SKUs.

- September 2025: Takween Advanced Industries signed an MoU with PIF-backed Green Saudi Recycling to secure 25 000 tpa of food-grade rHDPE from 2027, locking in traceable circular feedstock for personal-care bottles.

Saudi Arabia Plastic Packaging Market Report Scope

Plastic packaging is a part of the multi-faceted system for providing products, from the point of manufacture to the point of consumption. Its principal purpose is to guard and ensure the safe and secure delivery of the product in flawless and perfect condition to the end user (manufacturer of product or consumer). Its role in a circular economy is to sustain the value of a product for as long as required and to help remove product waste.

The Saudi Arabia Plastic Packaging Market Report is Segmented by Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene and EPS, and Other Material Types), Packaging Type (Flexible Plastic Packaging, and Rigid Plastic Packaging), Product Form (Bottles and Jars, Trays and Containers, Pouches and Sachets, Bags and Sacks, Films and Wraps, and Other Product Forms), End-User Industry (Food, Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Industrial, and Other End-user Industries), Manufacturing Process (Extrusion, Injection Molding, Blow Molding, Thermoforming, and Other Manufacturing Processes). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| Other Manufacturing Processes |

Key Questions Answered in the Report

What is the current value and projected size of the Saudi Arabia plastic packaging market by 2031?

The market is valued at USD 8.82 billion in 2026 and is forecast to reach USD 10.28 billion by 2031, reflecting a 3.12% CAGR over 2026-2031.

How quickly will flexible-pack demand rise in the kingdom?

Flexible formats are forecast to grow at a 4.26% CAGR over 2026-2031 as e-commerce and modern retail expand portion-controlled and logistics-friendly packs.

Which resin is set to gain the most share by 2031?

Polyethylene terephthalate will grow at a 4.31% CAGR, helped by tourism-driven bottled-water demand and new domestic rPET supply.

What restricts wider recycled-content use today?

Only 5% of national waste is recycled, so converters must import high-grade rPET and rPE until deposit-return and source-separation programs scale up.

How is Vision 2030 shaping pharmaceutical packaging?

Localization goals push blister and sterile-pouch demand higher, rewarding ISO 15378-certified converters with long-term contracts.

Where are the best incentives for new converting plants?

Ras Al Khair and NEOM offer discounted utilities and land, though investors still await anchor-tenant commitments before finalizing projects.

What is the biggest short-term risk to converter profits?

Crude-linked PP and PE price volatility that can move 20-30% in a quarter compresses margins for converters with limited hedging capacity.

Page last updated on: