Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

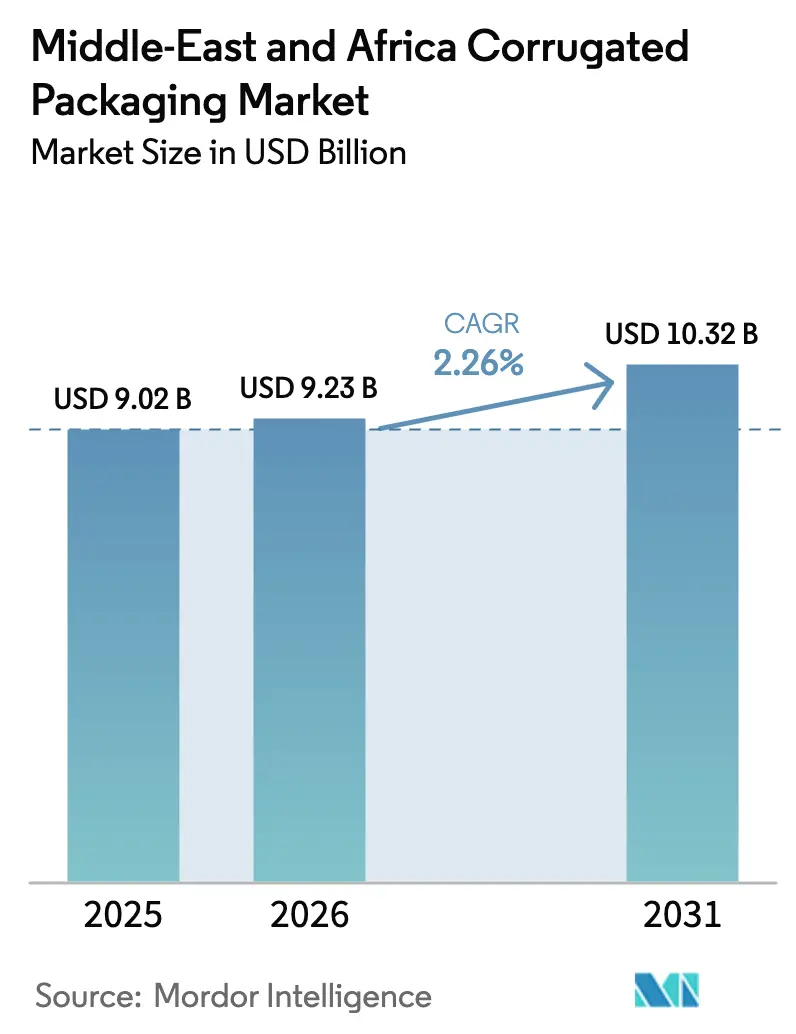

| Base Year Market Size (2025) | USD 9.02 Billion |

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 10.32 Billion |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Corrugated Packaging Market Analysis by Mordor Intelligence

The Middle East and Africa corrugated packaging market size is projected to expand from USD 9.02 billion in 2025 and USD 9.23 billion in 2026 to USD 10.32 billion by 2031, registering a CAGR of 2.26% between 2026 and 2031. The measured trajectory conceals a strategic shift as converters pivot toward digitally enabled e-commerce logistics, extended-producer-responsibility frameworks, and AfCFTA-linked trade lanes. Local brand owners are demanding board grades that balance water efficiency with recyclability, while fast-growing online retailers in Saudi Arabia, the United Arab Emirates, Egypt, and South Africa push converters to invest in die-cut designs and micro-flute substrates. Heavy industry, fresh-produce exporters, and Government incentives for closed-loop recycling further shape procurement decisions. Competitive strategies hinge on backward integration into kraft-liner capacity, adoption of digital printing for micro-runs, and alliances with waste-management firms that secure recycled fiber.

Key Report Takeaways

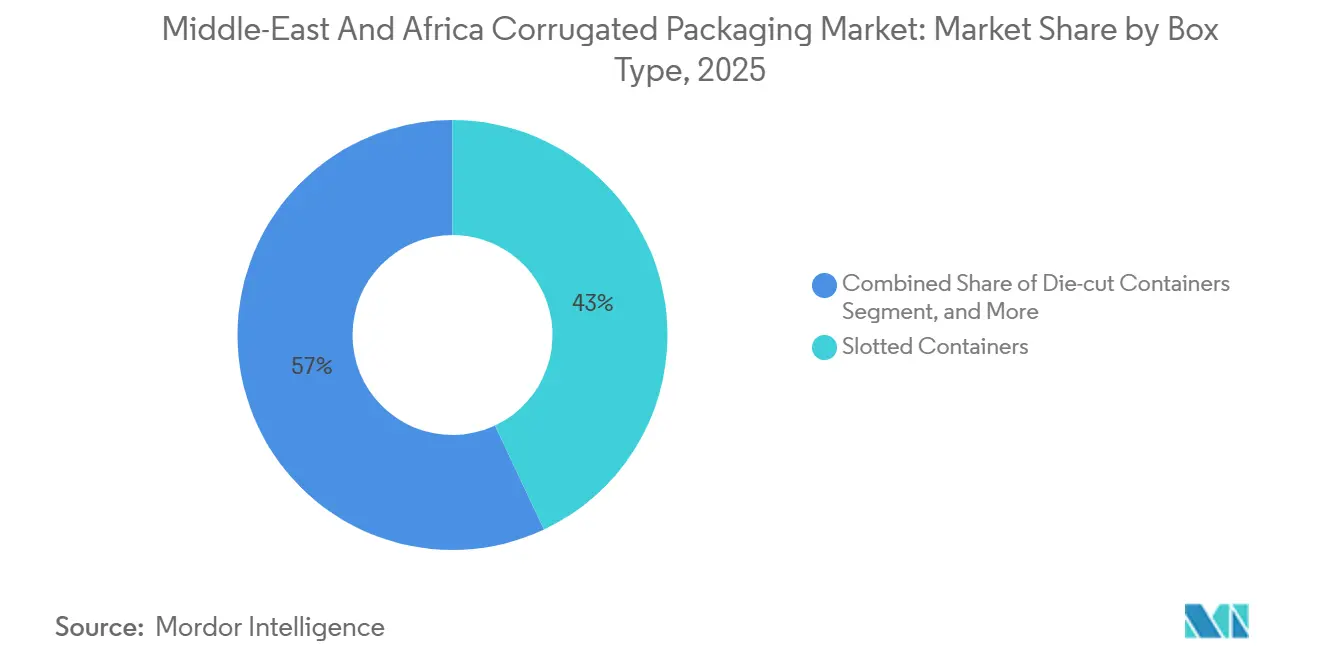

- By box type, slotted containers led with 43.0 % revenue share in 2025; die-cut containers are forecast to rise at a 3.11 % CAGR through 2031.

- By board grade, single-wall board accounted for 48.2 % of the Middle East and Africa corrugated packaging market share in 2025, while triple-wall board is advancing at a 3.89 % CAGR through 2031.

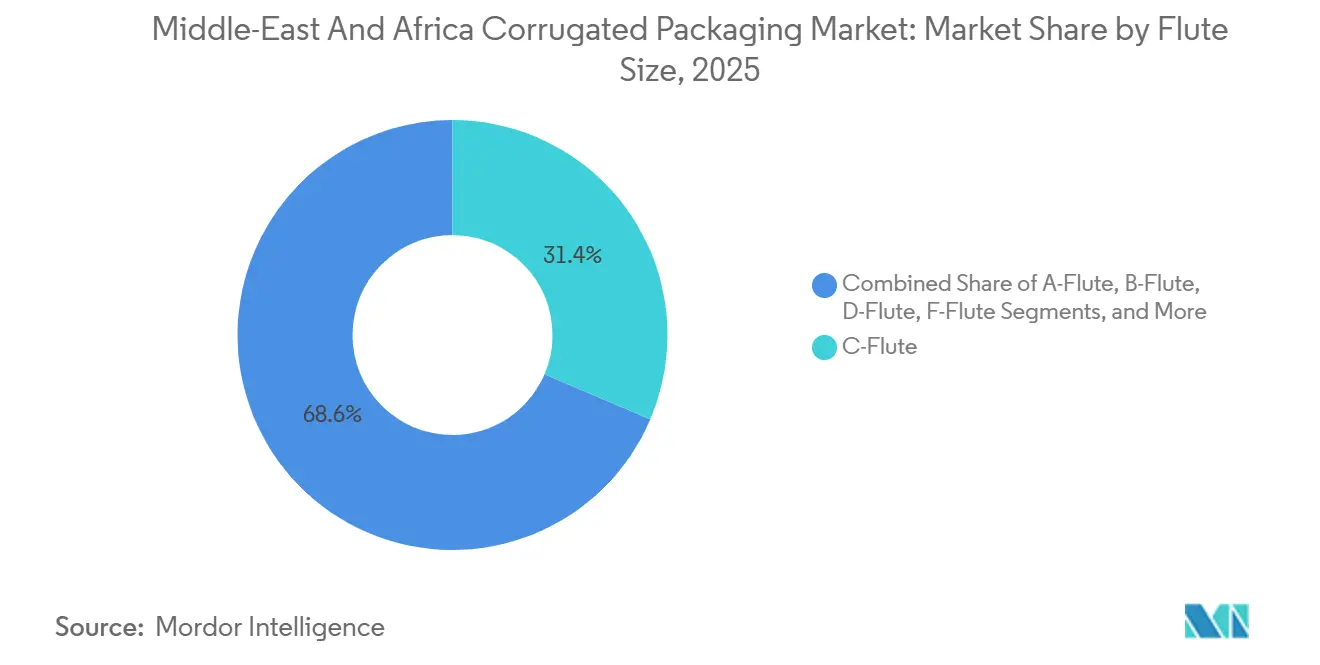

- By flute size, C-Flute captured 31.4 % share in 2025, and F-Flute is projected to grow at a 2.85 % CAGR to 2031.

- By end-user, the food segment commanded 24.6 % share of the Middle East and Africa corrugated packaging market size in 2025; e-commerce and retail is expanding at a 2.78 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom Driving Last-Mile-Friendly Packaging | +0.80% | GCC core (Saudi Arabia, UAE), Egypt, South Africa | Short term (≤ 2 years) |

| Rapid Expansion of FMCG and Organised Retail | +0.60% | Saudi Arabia, UAE, Egypt, Nigeria, South Africa | Medium term (2-4 years) |

| Government Incentives for Local Manufacturing and Recycling | +0.50% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| Export-Oriented Fresh-Produce Logistics Growth | +0.40% | Morocco, Egypt, South Africa, Kenya | Long term (≥ 4 years) |

| Inter-African Trade Surge Under AfCFTA | +0.30% | Pan-African, early gains in East Africa and Southern Africa | Long term (≥ 4 years) |

| Digital Printing Adoption for Micro-Brands | +0.20% | GCC, Egypt, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom Driving Last-Mile-Friendly Packaging

Online retail in the region expanded by 30% in 2024, boosting demand for die-cut cartons that slash dimensional-weight fees and withstand reverse-logistics handling.[1]World Bank Group, “Middle East and North Africa Overview,” worldbank.org Saudi Arabia’s digital-payment adoption lifted e-commerce penetration in tier-2 cities, prompting converters to specify F-Flute and micro-flute profiles for 20-30% material savings.[2]Saudi Arabian Monetary Authority, “Retail Sector Data,” sama.gov.sa In the United Arab Emirates, cross-border marketplaces require tamper-evident, multilingual graphics, intensifying interest in variable-data digital printing.[3]UAE Ministry of Economy, “Economic Performance Reports,” moec.gov.ae Inline hybrid presses shown at drupa 2024 allow runs of 500 units, letting micro-brands personalize graphics without plate lead times. Collectively, these shifts lead converters to retool for shorter order cycles, narrower flutes, and interactive QR-codes that double as returns portals.

Rapid Expansion of FMCG and Organised Retail

Hypermarket chains in Saudi Arabia, the United Arab Emirates, and Egypt are scaling into secondary cities where summer temperatures top 45 °C. Corrugated shippers must comply with Saudi Food and Drug Authority labelling, carry Arabic text, and survive high-humidity distribution. Egypt’s grocery modernisation brings ISO 22000 food-grade board to the forefront. Nigeria, while promising, contends with port congestion and currency swings that suppress cold-chain investment. Still, Gulf Cooperation Council paper-packaging output is forecast to hit USD 12.8 billion by 2032, signalling sustained retail-led demand.[4]GSO Secretariat, “GCC Paper Packaging Market Outlook,” gso.org.sa

Government Incentives for Local Manufacturing and Recycling

Egypt’s EPR levy of EGP 37.5 per kilogram on non-recycled packaging raises landed costs on virgin-fiber imports, favouring local mills with recycled-content lines. Kenya’s May 2025 EPR rules compel brand owners to underwrite collection schemes, lifting demand for baled, easily repulped corrugated. Dubai’s pilot pushes for 75 % landfill diversion by 2030, rewarding converters that secure recycled fiber and closed-loop logistics. Saudi Arabia’s Vision 2030 ties water allocation to closed-loop recycling; WASCO collected 500,000 tonnes of paper in 2024, lowering virgin-fiber dependence.

Export-Oriented Fresh-Produce Logistics Growth

South Africa shipped 31.75 million citrus cartons to Middle East buyers in the 2023-2024 season, necessitating moisture-resistant, ventilated corrugated that preserves cold-chain integrity. Morocco and Egypt export berries and dates to the European Union in wax-coated cartons fitted with modified-atmosphere liners. Kenya’s limited cold storage delays adoption of advanced boxes, yet AfCFTA tariff preferences encourage investment in durable triple-wall shippers for cross-border trucks. Converters targeting produce logistics often bundle RFID tags for traceability, feature EU importers increasingly require.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Kraft Paper Supply and Prices | -0.40% | Egypt, Nigeria, Kenya, smaller Gulf markets | Short term (≤ 2 years) |

| Competition from Flexible Plastic Packaging | -0.30% | Nigeria, Kenya, smaller North African markets | Medium term (2-4 years) |

| Import-Dependent Raw-Material Logistics Risk | -0.20% | Egypt, Nigeria, Kenya | Short term (≤ 2 years) |

| Water-Scarcity-Driven Mill Regulations | -0.10% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Kraft Paper Supply and Prices

Egypt imports 60 % of its kraft liner, so a 10 % pound-euro slide in 2024 pushed up landed costs equivalently. Nigerian converters faced 15-20 % surcharges tied to naira depreciation and Lagos port congestion. Red Sea diversions extended Kenyan lead times from 30 to 50 days, forcing recycled-fiber substitution that compromised burst strength. Investments like Middle East Paper Company’s SAR 1.78 billion mill expansion aim to offset such volatility via regional capacity.

Competition from Flexible Plastic Packaging

Flexible pouches weigh 40-50 % less than comparable corrugated cartons, a decisive advantage in logistics-cost-heavy markets such as Nigeria and Kenya. Single-use plastic bans in Nigeria, Ethiopia, and Ghana are spurring substitution, yet inconsistent enforcement keeps plastics in play. Gulf producers lobby for transition extensions while digital-print-ready pouch lines court FMCG marketers with high-gloss graphics. Corrugated converters must match visual appeal and invest in barrier coatings to defend share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Box Type: Die-Cut Containers Unlock Custom Fit for E-Commerce

Slotted containers retained a 43.0 % share of the Middle East and Africa corrugated packaging market in 2025, testament to their cost efficiency and compatibility with case erectors. They remain the default for high-volume food and beverage shipments across Saudi Arabia, the United Arab Emirates, Egypt, and South Africa. Die-cut containers, however, chart a 3.11 % CAGR to 2031, outpacing the overall Middle East and Africa corrugated packaging market. E-commerce platforms mandate custom-fit packaging that trims void space and lowers dimensional-weight charges, while enhancing the unboxing moment. Inline digital-printing systems unveiled at drupa 2024 enable converters to add QR-coded graphics in runs as low as 500 units, meeting micro-brand aesthetics without tooling delays. Five-panel folders aid flat-packed apparel exports, whereas telescopic boxes serve automotive and heavy-machinery spares where two-piece construction ensures crush resistance. Bliss boxes and self-erecting containers sit in niche pharmaceutical and electronics channels that prize tamper evidence, cushioning, and rapid fulfilment.

The Middle East and Africa corrugated packaging market size for die-cut designs is projected to expand steadily as last-mile networks deepen. Converters in Gulf Cooperation Council cities are adding laser-die lines that sharpen crease tolerance, enabling self-locking flaps which reduce tape usage. This engineering shift also aligns with extended-producer-responsibility rules that penalize non-recyclable void-fill. As a result, die-cut adoption will rise fastest in markets where digital payments, reverse logistics, and smartphone penetration intersect.

By Board Grade: Triple-Wall Board Rises on Heavy-Duty Exports

Single-wall board accounted for 48.2 % of Middle East and Africa corrugated packaging market share in 2025. Its 200-300 psi burst strength, ample for ambient grocery distribution, and its smooth printable surface make it the workhorse across food, beverage, and FMCG lines. Double-wall board supports mid-weight consumer electronics and appliances, offering 400-500 psi while still cutting weight relative to wood crates. Triple-wall board, boasting over 1,000 psi, shows the sharpest growth at 3.89 % CAGR, propelled by AfCFTA cross-border machinery and chemicals trade. The Middle East and Africa corrugated packaging market size for triple-wall applications will accelerate as exporters seek fumigation-free, lighter alternatives to wooden crates. Middle East Paper Company’s fifth machine is tailored for heavy-duty liner grades, a signal that regional mills expect sustained demand for triple-wall capacity. Solid fiber board, despite ultimate rigidity, stays relegated to high-value electronics due to its weight premium.

Price-sensitive African corridors may initially resist triple-wall’s 30-40 % cost premium, yet total landed-cost analysis shows freight savings and damage reduction offsetting upfront spend. Trans- Sahel Road upgrades and rail links within the Horn of Africa will further underscore triple-wall’s durability advantage in rough-handling environments.

By Flute Size: F-Flute Captures Freight-Sensitive Categories

C-Flute, at 31.4 % share in 2025, balances cushioning and printability, anchoring the grocery and beverage verticals. B-Flute optimizes canned goods and bottled beverages where carton count per sheet drives economics. E-Flute and the ultrathin F-Flute target electronics, cosmetics, and rapid-turn textiles. F-Flute’s 2.85 % CAGR surpasses the overall Middle East and Africa corrugated packaging market, driven by consumer electronics importers in Dubai and personal-care exporters in Egypt who prize reduced dimensional weight. Metsä Board’s 2024 micro-flute launch demonstrates technical feasibility for moisture-resistant thin walls. A-Flute lingers in fragile ceramics and glass, while emerging N- and K-Flutes service specialized cushioning profiles.

Fine-screen digital print pairs well with micro-flute surfaces, allowing 150-line-per-inch resolution that rivals folding cartons. That capability gives brand owners marketing latitude without migrating to costlier solid-bleached-sulfate cartons. Consequently, micro-flutes will see the fastest uptake where unit economics and brand aesthetics converge.

By End-User Industry: Online Retail Surges Past Mature Food Base

The food category maintained a 24.6 % share in 2025, anchored by population growth, urban grocery formats, and ISO 22000 compliance. Beverage shippers rely on reinforced partitions to prevent bottle breakage in the Gulf’s high-heat logistics chain. Yet e-commerce and retail, advancing at 2.78 % CAGR, will emerge as the pivotal growth engine for the Middle East and Africa corrugated packaging market. As digital platforms scale, converters must integrate return-ready tear strips and smart-label numbering to accommodate reverse flows. Consumer electronics brands adopt E- and F-Flutes, pairing electrostatic-discharge coatings with narrow caliper to trim airfreight costs. Personal-care marketers leverage digitally printed corrugated for influencer-friendly unboxing; variable graphics embed sustainability messages that resonate with Gen-Z buyers.

Industrial and chemicals exporters shift from wooden crates to triple-wall to meet fumigation-free rules and slash freight weight. Agriculture and fresh produce rely on ventilated boxes lined with wax or polymer coatings to keep citrus and berries market fresh. Other verticals pharma, textiles, building supplies maintain stable but smaller demand tied to infrastructure and healthcare spending across the continent.

Geography Analysis

Saudi Arabia and the United Arab Emirates collectively anchor the Middle East quadrant of the Middle East and Africa corrugated packaging market, fuelled by retail modernization, e-commerce adoption, and Vision 2030 manufacturing incentives. Saudi retail sales hit USD 85 billion in 2024, necessitating standardized slotted cartons that endure 45 °C summer warehousing. The United Arab Emirates, a re-export nexus, ships corrugated-boxed goods onward to East Africa and South Asia, so cartons must satisfy multi-jurisdictional customs codes. Middle East Paper Company’s capacity doubling to 900,000 tpa by 2027 underlines Riyadh’s import-substitution drive. Turkey bridges European and Gulf demand but faces currency gyrations that ralent investment. Oman, Kuwait, Bahrain, and Jordan represent smaller yet steady pockets, buoyed by demographic expansion and logistics-free-zone incentives.

Africa’s crown markets are Egypt and South Africa. Mondi’s EGP 5.5 billion expansion in Sadat City capitalizes on Egypt’s proximity to Mediterranean lanes and North African FMCG clusters. Egypt’s EPR surcharge nudges converters toward domestic linerboard, reducing 60 % kraft-liner import exposure. South Africa’s citrus chain shipped 31.75 million cartons to GCC buyers in the 2023-2024 season, validating demand for cold-chain-grade cartons. Nigeria’s potential is partially constrained by port delays and naira volatility, yet January 2025 plastic bans provide corrugated tailwinds. Kenya, Ethiopia, and Ghana follow with EPR rules and plastic prohibitions that accelerate paper substitution, though enforcement varies by county. Morocco leverages EU produce demand, packaging berries in RFID-tagged, wax-coated cartons to satisfy phytosanitary checkpoints. Investments by Middle East Paper Company in Zimbabwe, Malawi, and Mozambique reveal confidence that AfCFTA lanes will elevate localized carton demand in landlocked Southern African states.

Competitive Landscape

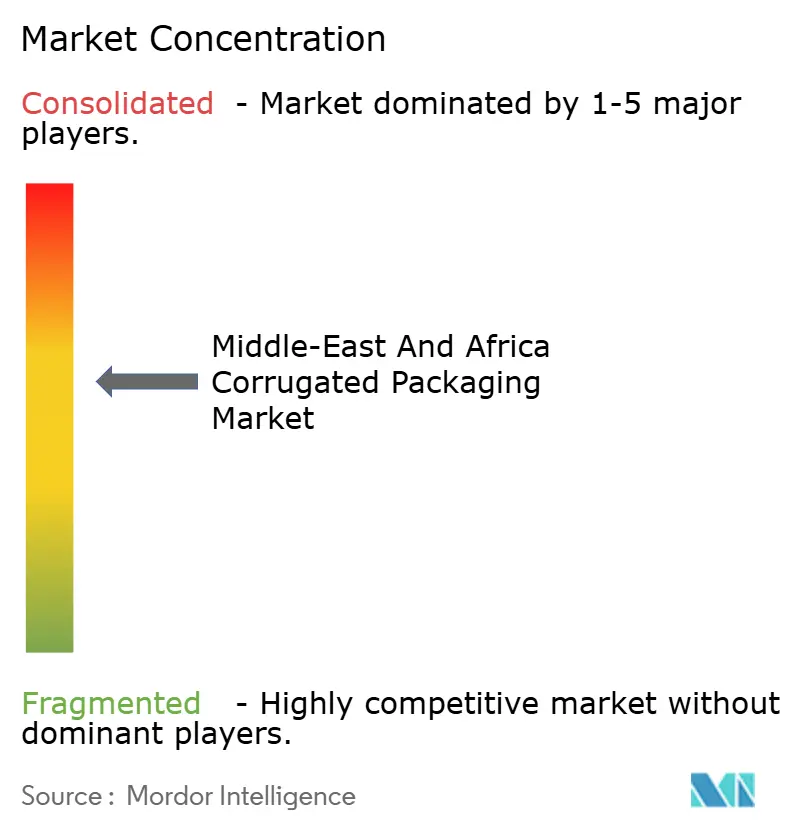

The Middle East and Africa corrugated packaging market features moderate concentration. Multinationals Mondi, Smurfit Kappa, and International Paper pair scale economics with integrated kraft capacity. Regional champions Middle East Paper Company, INDEVCO, Obeikan, Arabian Packaging, and Napco capitalize on agility, local languages, and regulatory familiarity. Mondi’s USD 180 million Sadat City phase-up focuses on food-grade linerboard for North African and EU outlets. Middle East Paper Company’s SAR 1.78-billion-line targets 30 % Saudi share and eastern-Africa exports, supplied in part by WASCO’s 500,000-tonne recovered fiber harvest. Extended-producer-responsibility levies in Egypt, Kenya, and Dubai penalize single-use plastics, positioning corrugated integrators with recycling muscle for share gains.

White-space opportunities include digital print for micro-brands, die-cut boxes tuned to e-commerce, and triple-wall board substituting wooden crates in AfCFTA corridors. Gulf plants roll out inline inkjet units showcased at drupa 2024, allowing 48-hour turnarounds on QR-coded cartons. Smaller African mills still rely on two-colour flexography, limiting their bids for premium jobs. Waste-management joint ventures like WASCO are vertically integrating into corrugation, threatening incumbents reliant on imported kraft. In the Gulf, only 10 % of 9 million tonnes of annual packaging waste is recycled, prompting likely consolidation of under-invested mills as EPR fees bite.

Middle-East And Africa Corrugated Packaging Industry Leaders

Arabian Packaging Co. LLC

Queenex Corrugated Carton Factory LLC

United Carton Industries Company (JSC)

Napco National CJSC

Cepack Group SARL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: No public announcements of material scale have been recorded to date.

- October 2026: Middle East Paper Company confirmed its fifth paper machine remains on schedule for Q4 2027 start-up, doubling capacity to 900,000 tpa and targeting 30 % domestic share while expanding exports to Zimbabwe, Malawi, and Mozambique.

- September 2025: Mondi completed phase one of its Sadat City expansion, adding 30,000 tpa of containerboard, with the second 30,000 tpa tranche slated for mid-2026.

- June 2025: Ethiopia enforced a nationwide ban on single-use plastic bags and polystyrene food containers, accelerating adoption of corrugated alternatives in food service and retail.

Middle-East And Africa Corrugated Packaging Market Report Scope

The Middle-East and Africa Corrugated Packaging Market Report is Segmented by Box Type (Slotted Containers, Die-cut Containers, Five-panel Folder Boxes, Telescopic Boxes, Other Box Types), Board Grade (Single-wall Board, Double-wall Board, Triple-wall Board, Solid Fiber Board), Flute Size (A-Flute, B-Flute, C-Flute, E-Flute, F-Flute, Other Flutes), End-User Industry (Food, Beverage, Consumer Electronics and Electrical Appliances, Personal Care and Household Care, Industrial and Chemicals, Agriculture and Fresh Produce, E-commerce and Retail, Other End-Users), and Geography (Middle East: Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East; Africa: Egypt, South Africa, Nigeria, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Box Type

| Slotted Containers |

| Die-cut Containers |

| Five-panel Folder Boxes |

| Telescopic Boxes |

| Other Box Types |

By Board Grade

| Single-wall Board |

| Double-wall Board |

| Triple-wall Board |

| Solid Fiber Board |

By Flute Size

| A-Flute |

| B-Flute |

| C-Flute |

| E-Flute |

| F-Flute |

| Other Flutes |

By End-User Industry

| Food |

| Beverage |

| Consumer Electronics and Electrical Appliances |

| Personal Care and Household Care |

| Industrial and Chemicals |

| Agriculture and Fresh Produce |

| E-commerce and Retail |

| Other End-Users |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | Egypt |

| South Africa | |

| Nigeria | |

| Rest of Africa |

| By Box Type | Slotted Containers | |

| Die-cut Containers | ||

| Five-panel Folder Boxes | ||

| Telescopic Boxes | ||

| Other Box Types | ||

| By Board Grade | Single-wall Board | |

| Double-wall Board | ||

| Triple-wall Board | ||

| Solid Fiber Board | ||

| By Flute Size | A-Flute | |

| B-Flute | ||

| C-Flute | ||

| E-Flute | ||

| F-Flute | ||

| Other Flutes | ||

| By End-User Industry | Food | |

| Beverage | ||

| Consumer Electronics and Electrical Appliances | ||

| Personal Care and Household Care | ||

| Industrial and Chemicals | ||

| Agriculture and Fresh Produce | ||

| E-commerce and Retail | ||

| Other End-Users | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle-East and Africa corrugated packaging market in 2031?

The market is forecast to reach USD 10.32 billion by 2031, reflecting a 2.26 % CAGR between 2026 and 2031.

Which board grade is growing fastest in regional demand?

Triple-wall board leads, registering a 3.89 % CAGR on the back of heavy-duty industrial and AfCFTA export shipments.

How are extended-producer-responsibility rules influencing packaging choices?

EPR fees in Egypt, Kenya, and Dubai raise costs on non-recycled or plastic formats, steering brand owners toward locally sourced, recyclable corrugated boxes.

Why are die-cut containers gaining share over slotted containers?

E-commerce platforms need custom-fit cartons that reduce void space, cut dimensional-weight charges, and deliver branded unboxing experiences.

Which countries are key growth hubs for corrugated packaging in Africa?

Egypt and South Africa lead in consumption and capacity, while Nigeria, Kenya, and Ghana show rising demand fueled by plastic bans and organized retail expansion.

How does digital printing impact the corrugated sector in the region?

Inline inkjet hybrids enable short-run, variable graphics, allowing converters to serve micro-brands and e-commerce sellers without expensive plates or long lead times.

Page last updated on: