GCC Corrugated Box Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

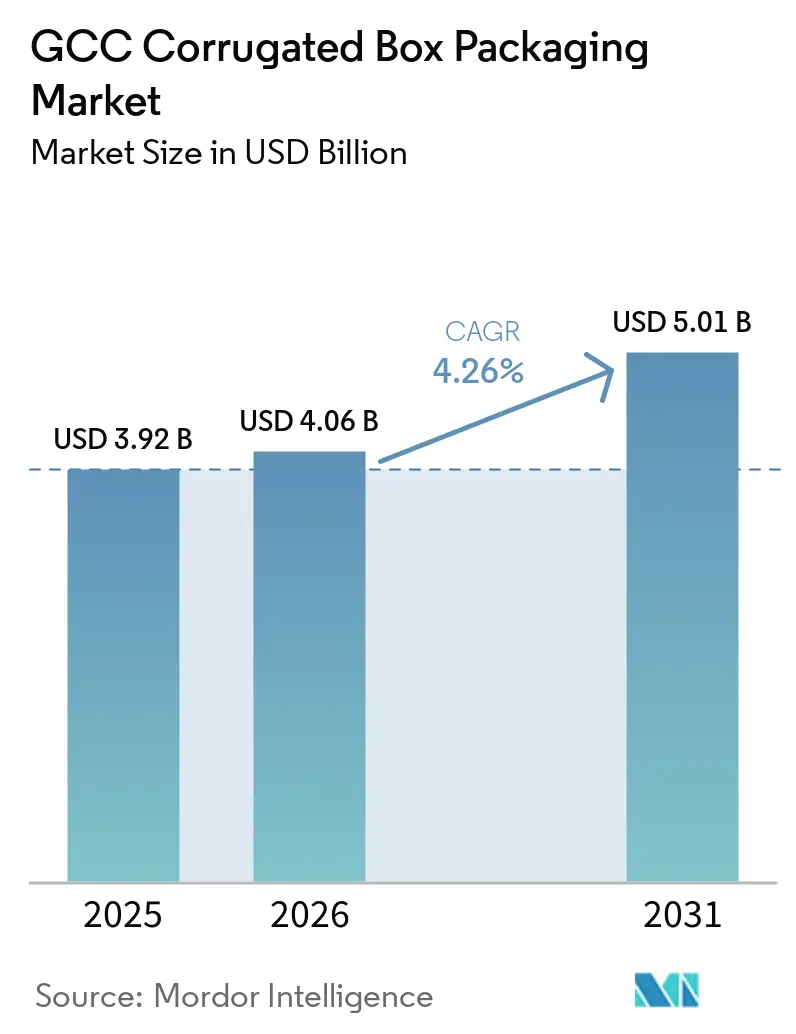

| Base Year Market Size (2025) | USD 3.92 Billion |

| Market Size (2026) | USD 4.06 Billion |

| Market Size (2031) | USD 5.01 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

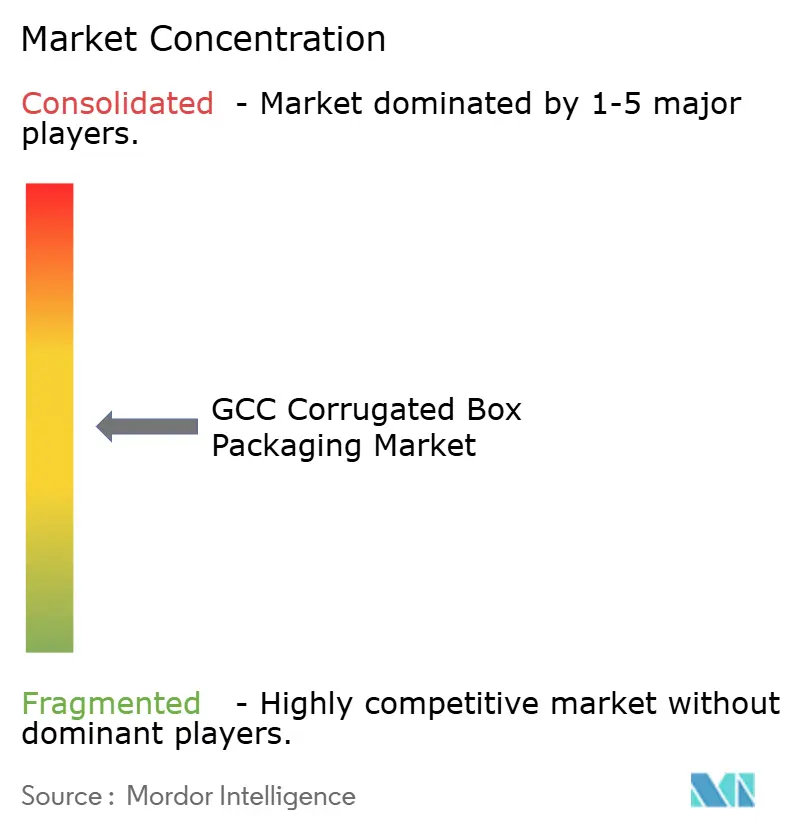

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Corrugated Box Packaging Market Analysis by Mordor Intelligence

The GCC corrugated box packaging market size is projected to be USD 3.92 billion in 2025, USD 4.06 billion in 2026, and reach USD 5.01 billion by 2031, growing at a CAGR of 4.26% from 2026 to 2031. Structural reforms across Saudi Arabia and the United Arab Emirates are shifting the region from import-reliant supply toward self-sufficient, vertically integrated packaging ecosystems. Rapid e-commerce penetration, zero-waste mandates, and Vision 2030 capital incentives are stimulating investments in containerboard mills, high-speed corrugators, and digital print lines that cut lead times and enable short-run customization. Sustainability targets are accelerating a pivot from plastic to fiber-based secondary packaging, while automated case-packing lines and warehouse expansions are compressing order cycles to under 48 hours. Converters that combine lightweight high-strength substrates, just-in-time logistics, and variable-data printing are capturing premium margins, signaling a transition from commodity boxes to engineered, value-added solutions.

Key Report Takeaways

- By product type, regular slotted containers led with 39.43% of GCC corrugated box packaging market share in 2025, while die-cut display boxes are advancing at a 5.53% CAGR through 2031.

- By board type, single-wall formats held 58.32% share of the GCC corrugated box packaging market size in 2025, and triple-wall board is projected to expand at a 5.62% CAGR to 2031.

- By flute profile, the C-flute captured 32.54% in 2025, whereas the F-flute is forecast to rise at a 5.78% CAGR between 2026-2031.

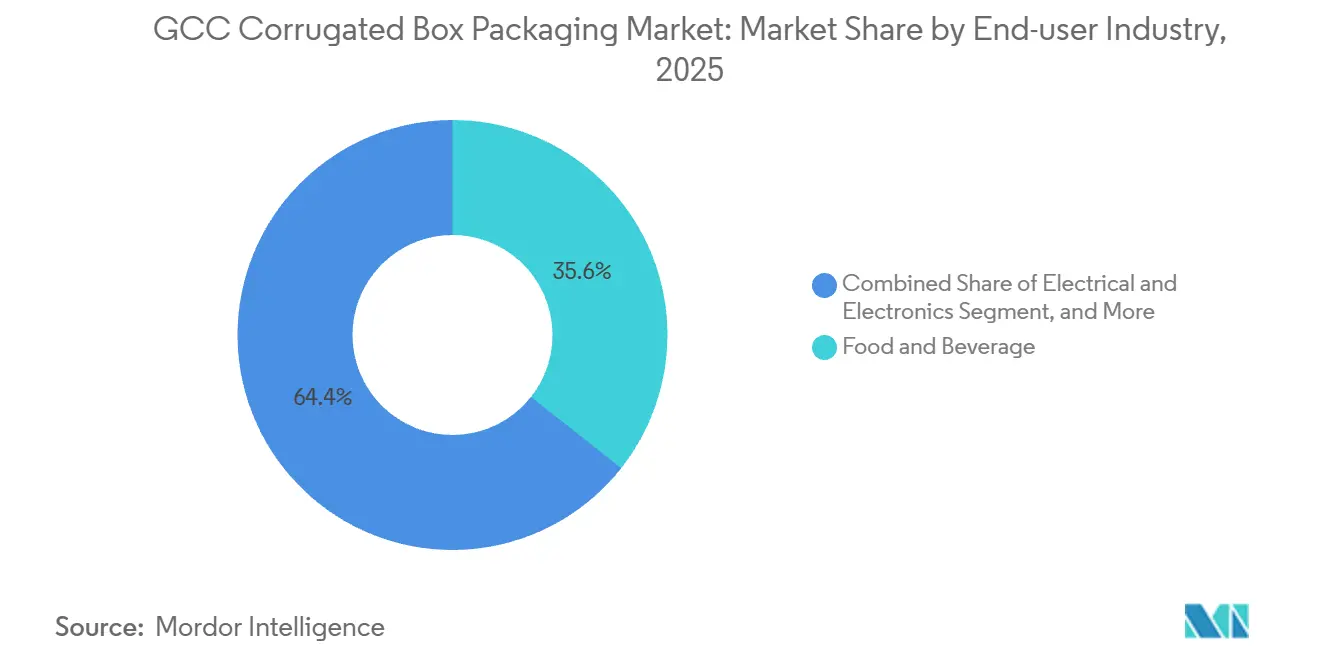

- By end-user industry, food and beverage commanded 35.63% share in 2025, yet electrical and electronics packaging is the fastest-growing segment with a 6.21% CAGR through 2031.

- By print technology, flexographic presses dominated with 71.54% share in 2025, and digital printing is set to grow at a 6.01% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Corrugated Box Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce Fulfillment Centers | +1.2% | Saudi Arabia, UAE (Riyadh, Dubai, JAFZA, KEZAD) | Short term (≤ 2 years) |

| Shift Toward Lightweight High-strength Containerboard | +0.8% | GCC-wide, led by Saudi Arabia and UAE | Medium term (2-4 years) |

| GCC Government Zero-waste Initiatives | +0.7% | UAE (Abu Dhabi, Dubai), Saudi Arabia (Riyadh, Jeddah) | Medium term (2-4 years) |

| Retailers Switch to Plastic-free Secondary Packaging | +0.6% | UAE, Saudi Arabia, Qatar (retail and FMCG sectors) | Short term (≤ 2 years) |

| Automated High-speed Case-packing Lines Adoption | +0.5% | Saudi Arabia (KAEC, Jubail), UAE (Dubai Industrial City) | Long term (≥ 4 years) |

| Vision 2030 Localisation of Corrugated Supply Chains | +0.9% | Saudi Arabia (national), spillover to Oman and Bahrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Fulfillment Centers

Amazon and regional 3PLs have built fifteen automated hubs across Riyadh, Dubai, and KEZAD that require bar-coded corrugated cases calibrated for high-speed sortation systems.[1]Amazon, “Frustration-Free Packaging Guidelines,” aboutamazon.com Warehouse occupancy in Riyadh reached 98% in Q4 2025, prompting developers to fast-track 2.5 million m² of Grade-A logistics space in Sudair and King Abdullah Economic City. Jebel Ali Port and Abu Dhabi’s KEZAD now prioritize tenants that co-locate converting lines to cut dwell time, effectively embedding box production inside fulfillment chains. While quick-commerce players test reusable totes, corrugated remains the default for non-food SKUs because hygiene and reverse logistics costs tilt the economics toward single-use fiber.

Shift Toward Lightweight High-strength Containerboard

A 450,000-tonne recycled containerboard line coming online in Jeddah will supply 70-140 gsm grades that allow 10-15% basis-weight reduction without losing edge-crush strength. Air-cargo shippers already realize freight savings of USD 0.08 per parcel on Dubai-London lanes after adopting lighter boxes, driving rapid converter uptake. Global players have introduced design platforms that eliminate internal partitions and cut material usage by almost one-fifth, aligning with brand-owner carbon scorecards. However, recycled OCC sourced locally contains higher contaminant levels, necessitating extra screening that lifts production costs and compresses margins. Even with this headwind, lightweighting remains a net positive driver because every kilogram removed from packaging directly lowers freight, carbon, and landfill liabilities.

GCC Government Zero-waste Initiatives

Abu Dhabi’s 2030 landfill-diversion target and Saudi Arabia’s parallel Vision 2030 goals have ushered in extended producer responsibility schemes requiring mandatory recycled-content thresholds. Large converters are responding by co-investing in municipal collection networks to secure feedstock and by switching to water-based inks and starch adhesives that simplify fiber recovery. Compliance documentation and annual waste-reporting obligations favor vertically integrated players with robust traceability systems, further accelerating industry consolidation. These policies also push brand owners to drop mixed-material laminates, steering demand toward mono-material corrugated solutions. Over the medium term the regulatory push is expected to hard-wire recycling discipline into regional packaging supply chains.

Retailers Switch to Plastic-free Secondary Packaging

Supermarket chains eliminating single-use plastics have shifted tens of thousands of tonnes of produce packaging into coated corrugated trays. Government levies on plastic bags and clamshells have shortened the payback period for fiber alternatives to under eighteen months, making substitution financially attractive. Quick-service restaurants are piloting grease-resistant corrugated clamshells that displace foam containers in takeaway channels. Moisture and humidity remain technical challenges along coastal zones, prompting a surge in barrier-coated liners that raise per-square-meter costs but still undercut reusable crate systems when reverse logistics is impractical. The net effect is a durable uplift in demand for specialty grades within the GCC corrugated box packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled OCC Import Costs | -0.6% | GCC-wide, acute in UAE and Kuwait (high import dependency) | Short term (≤ 2 years) |

| Scarcity of Water for Kraft Pulping in GCC | -0.4% | Saudi Arabia, UAE, Kuwait (arid regions) | Long term (≥ 4 years) |

| Rising Adoption of Reusable Plastic Crates in Produce | -0.3% | UAE, Saudi Arabia (retail and fresh-produce supply chains) | Medium term (2-4 years) |

| Limited Availability of Skilled Packaging Engineers | -0.2% | GCC-wide, most acute in Saudi Arabia and Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled OCC Import Costs

GCC converters imported 1.8 million tonnes of OCC in 2025, with spot freight rising from USD 85 to USD 142 per tonne after Red Sea detours extended transit by two weeks.[2]Drewry Maritime Research, “Container Freight Rate Analysis,” drewry.co.uk European exporters rerouted 400,000 tonnes to the Gulf after China’s National Sword ban, depressing prices to USD 95 in 2024 before a Q4 2025 rebound to USD 128. These swings squeezed converter margins to 8-12%, down from 14-18% in 2019. High contamination in Saudi OCC collections adds USD 18-22 per tonne in reprocessing costs. Abu Dhabi’s new materials recovery facility is still operating 30% below nameplate capacity due to feedstock variability.

Scarcity of Water for Kraft Pulping in GCC

Desalinated process water costs USD 1.20-1.80 per m³, making virgin-fiber kraft mills uncompetitive versus recycled lines that use 60-70% less water.[3]International Desalination Association, “Desalination Costs and Industrial Water Tariffs in the GCC,” idadesal.orgSaudi regulators added a 15% surcharge on industrial withdrawals beyond 500,000 m³ per year in 2024, further deterring kraft investments. Water stress indices exceed 900% in the UAE and 500% in Saudi Arabia, compared with a global average of 9%. Consequently, 92% of GCC containerboard used OCC feedstock in 2025, compared with 58% worldwide. MEPCO’s AquaLine system now recycles 85% of process water but adds more than USD 12 million to capex and demands scarce technical talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Die-cut Displays Capture Retail Marketing Spend

Regular slotted containers accounted for 39.43% of the market share in 2025, supported by standardized pallet footprints that favor automated case packing and e-commerce fulfillment. Die-cut display boxes are forecast to grow at 5.53% as retailers redirect in-store budgets to recyclable corrugated fixtures that qualify for extended producer responsibility credits. Half-slotted designs remain popular in automotive and electronics assembly lines, where open tops speed kitting, and telescopic formats are emerging in pharmaceutical cold chains that need nested boxes for temperature-controlled shippers. Variable-data digital printing now allows point-of-sale campaigns tailored to micro markets, reinforcing brand preference with minimal setup waste. The widening gap between utility cartons and engineered displays is reshaping converter portfolios toward higher-value-added offerings in the GCC corrugated box packaging market.

Brand owners increasingly use die-cut displays as a marketing medium, embedding NFC tags and augmented-reality triggers that bridge physical shelves to online engagement. Digital presses installed in Dubai print at seventy-plus meters per minute, producing store-specific artwork without the plate costs of flexography. Wrap-around cases and self-locking trays collectively serve frozen foods and serialized pharmaceuticals where tamper evidence is critical and buyers pay premium mark-ups. The emphasis on retail theater is likely to maintain double-digit growth for display formats even if macro demand softens in commodity segments. This product mix evolution supports tighter margins and higher resilience for converters that diversify beyond standard RSCs.

By Board Type: Triple-wall Solutions Meet Heavy-duty Export Needs

Single-wall board accounted for 58.32% of the GCC corrugated box packaging market in 2025, driven by parcels under 20 kilograms that dominate e-commerce flows. Triple-wall board is set to rise at 5.62% as automotive parts exporters and machinery shippers demand burst strengths above 1,000 kPa to comply with global transit standards. Double-wall grades remain the mid-range workhorse for bulk foods and building materials, where cost and stacking strength must be balanced. Exporters switching from wooden crates to heavy-duty corrugated boxes avoid ISPM-15 heat-treatment delays, cutting lead times by up to 1 week.

Only a handful of GCC corrugators currently run triple-wall at scale, conferring a supply advantage that supports gross margins of 18% versus 12% for single-wall. Recent investor presentations highlight triple-wall as a strategic pivot aligned with Vision 2030 ambitions to triple non-oil exports. Pharmaceutical and cold-chain regulations further reinforce demand for double- and triple-wall boxes that retain thermal mass during long-haul transport. Although equipment and skill barriers slow new capacity, incremental additions scheduled through 2028 should relieve bottlenecks while sustaining premium pricing power.

By Flute Profile: F-flute Optimizes Last-mile Logistics

C-flute held 32.54% of the market share in 2025, balancing cushioning and printable surface for mainstream food and beverage cartons. F-flute, at just 1.5-2 mm, is forecast to grow by 5.78% as online merchants minimize dimensional-weight fees and favor smoother substrates for high-resolution graphics. E-flute secures a niche in cosmetics and retail-ready packages that sit directly on the shelf, while B-flute supports heavier chemical drums and agricultural inputs. A-flute remains a legacy option for bulky furniture and appliances, yet is gradually being replaced by hybrid double-wall solutions.

Amazon’s frustration-free guidelines now specify F-flute for parcels under five kilograms, accelerating converter retooling to finer profiles. Micro flutes below one millimeter are moving from pilot to commercial scale in pharmaceutical blister cards and electronics trays, where dimensional precision is paramount. Improved ink laydown on fine flutes cuts consumption by up to 15% and allows four-color graphics without pre-print linerboard, shrinking turnaround times to three days. This logistics-first mindset underscores how flute selection is evolving from mere protection toward supply-chain optimization.

By End-user Industry: Electronics Emerges as High-margin Growth Engine

Food and beverage dominated with a 35.63% share in 2025, backed by national food-security agendas and deep-chilled supply chains. Electrical and electronics packaging, however, posts the fastest 6.21% CAGR as sovereign technology zones build semiconductor fabs and consumer device assembly lines that require static-dissipative corrugated trays. Pharmaceutical boxes, though lower in tonnage, command superior margins due to GDP compliance, serialized printing, and validated cold-chain liners. E-commerce continues to grow from a smaller base, yet the rising adoption of reusable totes in online grocery shopping tempers its long-term volume.

Saudi technology funds exceeding USD 6 billion, combined with the UAE's free-zone tax holidays, create a pipeline of electronics projects that require highly engineered packaging. Converters that capture this opportunity upgrade to ISO 15378-quality systems and invest in conductive coatings that protect microchips from electrostatic discharge. Cold-chain pharmaceuticals add further upside as GCC vaccine and biosimilar production scales, reinforcing demand resiliency even when consumer goods cycles fluctuate.

By Print Technology: Digital Presses Enable Hyper-local SKUs

Flexography accounted for 71.54% of the market share in 2025, thanks to low per-unit costs at runs above 10,000 boxes. Digital presses are forecast to climb at a 6.01% CAGR as HP and EFI platforms deliver 1,200 dpi resolution at industrial speeds, making short-run, variable-data campaigns economically feasible. Lithographic offset holds a premium niche in luxury goods where metallic finishes justify higher price points, while screen printing and hot stamping remain limited to tamper-evident or security applications.

A newly installed digital flexo line in Jeddah slashed makeready time from 45 to 8 minutes, cut waste to under 2%, and achieved payback in less than 2 years. Brand managers now rotate seasonal artwork every few weeks, compressing SKU lifecycles and demanding converters able to switch designs overnight. While flexo remains entrenched in high-volume, fast-moving consumer goods, digital’s share will continue to rise as equipment costs fall and sustainability audits favor plate-free workflows.

Geography Analysis

Saudi Arabia supplied a significant share in the market, leveraging domestic demand and Vision 2030 incentive pools that compress greenfield payback to a shorter period. The United Arab Emirates is projected to experience steady growth, driven by plans to expand warehouse capacity and enforce zero-waste mandates that favor fiber-based solutions. Kuwait remains import-heavy due to limited local converting, while Oman, Bahrain, and Qatar together offer cost-effective hubs within the GCC customs union.

The United Arab Emirates leads regional growth due to port infrastructure that shortens Asian feedstock transit and facilitates re-exports into East Africa and South Asia. The upcoming plastic ban accelerates substitution toward moisture-barrier corrugated trays, especially for fresh produce, while tax holidays in Dubai Industrial City and KEZAD attract converters that embrace Industry 4.0 automation. High humidity along coastal zones adds technical complexity, yet barrier-coated liners maintain performance with modest cost premiums, protecting converter margins. Rapid warehousing expansion and on-site packaging integration support sustained volume gains across Abu Dhabi and Dubai.

Smaller GCC members contribute niche dynamics. Kuwait’s VAT exemption encourages gradual in-market capacity additions, but the country still imports most boxes from Saudi Arabia and the UAE. Oman and Bahrain market lower operating costs to attract satellite plants, leveraging tariff-free GCC access to feed larger neighbors’ just-in-time needs. Qatar’s recycled-content mandate in government procurement fosters opportunities for converters that certify fiber sourcing. Together, these geographies enhance supply-chain redundancy and spread risk, reinforcing stability across the wider GCC corrugated box packaging market.

Competitive Landscape

The market structure remains moderately fragmented. United Carton Industries Company, operating eight plants across Saudi Arabia and the UAE, reported FY 2024 revenue of USD 358 million and on-time delivery rates above 98%, leveraging automation on a scale that smaller firms struggle to match. The 2024 WestRock-Smurfit merger created a USD 34 billion global leader whose Middle East units focus on high-margin display and specialty cartons priced twenty percent above commodity equivalents.

Strategic patterns revolve around vertical integration, either backward into containerboard mills or forward into finished boxes, to secure feedstock and capture additional margin. Middle East Paper Company is doubling recycled containerboard capacity and erecting an adjacent converting complex, while Arabian Packaging co-invests in OCC collection to de-risk raw-material procurement. Technology remains a key differentiator; scale players deploy IoT-enabled corrugators that reach 18,000 sheets per hour and computer-vision quality controls that slash waste to below 2%. Smaller job shops, limited to legacy equipment, survive by serving niche artisanal runs but risk displacement as digital presses lower the economic threshold for short runs.

Certification and sustainability credentials increasingly dictate tender wins. FMCG majors require ISO 14001 plants and FSC chain-of-custody audits, tilting volume toward converters capable of meeting stringent reporting requirements. Consolidation is accelerating as mid-size players acquire flexible-film specialists to cross-sell hybrid packaging suites, while sustainability startups introduce compostable fiber blends that pressure conventional grades. Despite these shifts, the GCC corrugated box packaging industry retains headroom for new entrants that offer specialty coatings, cold-chain expertise, or near-shoring advantages around emerging logistics hubs.

GCC Corrugated Box Packaging Industry Leaders

Arabian Packaging Co. LLC

Napco National CJSC

Queenex Corrugated Carton Factory LLC

United Carton Industries Company

Cepack Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: RA International signed a distribution deal with Gaia Biomaterials to launch limestone-based compostable packaging across the GCC, with first deliveries slated for Q1 2026.

- August 2025: Napco National acquired Arabian Flexible Packaging, adding flexible films and pouches to its corrugated portfolio to enhance cross-selling in food and beverage channels.

- April 2025: Middle East Paper Company broke ground on its PM5 recycled containerboard line in Jeddah, a USD 474 million project that will double site capacity to 900,000 tonnes by Q4 2027.

- April 2025: United Carton Industries Company announced plans to float thirty percent of its equity on the Saudi Exchange, earmarking proceeds for Oman expansion, solar energy, and further automation.

GCC Corrugated Box Packaging Market Report Scope

Corrugated box packaging is a popular material used for shipping, storing, and displaying products. Made from corrugated fiberboard, it consists of a fluted corrugated sheet and one or two flat linerboards. The fluted sheet provides strength and cushioning, making the boxes durable and able to withstand handling and transport.

The GCC Corrugated Box Packaging Market Report is Segmented by Product Type (Regular Slotted Container, Half-slotted Container, Die-cut Display Box, Telescopic Box, Folder-type Box, and Other Product Types), Board Type (Single Wall, Double Wall, and Triple Wall), Flute Profile (A Flute, B Flute, C Flute, E Flute, F Flute, and Other Flute Profiles), End-user Industry (Food, Beverages, Pharmaceuticals, Personal Care and Household, Industrial, E-commerce, Electrical and Electronics, and Other End-user Industries), Print Technology (Flexography, Digital, Lithography, and Other Print Technologies), and Country (Saudi Arabia, United Arab Emirates, Kuwait, and Rest of GCC). The Market Forecasts are Provided in Terms of Value (USD).

| Regular Slotted Container (RSC) |

| Half-slotted Container (HSC) |

| Die-cut Display Box |

| Telescopic Box |

| Folder-type Box |

| Other Product Types |

| Single Wall |

| Double Wall |

| Triple Wall |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Other Flute Profiles |

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Household |

| Industrial |

| E-commerce |

| Electrical and Electronics |

| Other End-user Industries |

| Flexography |

| Digital |

| Lithography |

| Other Print Technologies |

| Saudi Arabia |

| United Arab Emirates |

| Kuwait |

| Rest of GCC |

| By Product Type | Regular Slotted Container (RSC) |

| Half-slotted Container (HSC) | |

| Die-cut Display Box | |

| Telescopic Box | |

| Folder-type Box | |

| Other Product Types | |

| By Board Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| By Flute Profile | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| Other Flute Profiles | |

| By End-user Industry | Food |

| Beverages | |

| Pharmaceuticals | |

| Personal Care and Household | |

| Industrial | |

| E-commerce | |

| Electrical and Electronics | |

| Other End-user Industries | |

| By Print Technology | Flexography |

| Digital | |

| Lithography | |

| Other Print Technologies | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Rest of GCC |

Key Questions Answered in the Report

How fast is e-commerce influencing box demand in the GCC corrugated box packaging market?

New fulfillment hubs and quick-commerce platforms are adding more than 1.2% to forecast CAGR, driving short-run, bar-coded box orders that elevate overall volume.

Which board type is gaining popularity for heavy-duty exports from the GCC?

Triple-wall board is the fastest riser, projected to grow at 5.62% as machinery and auto-parts shippers pivot from wooden crates to compliant corrugated solutions.

Why are retailers shifting toward corrugated displays in Gulf supermarkets?

Zero-waste policies and extended producer responsibility fees make recyclable die-cut displays cheaper than permanent fixtures while supporting rapid marketing changes.

What limits virgin-fiber kraft mill investments in Saudi Arabia and the UAE?

High desalinated water tariffs of USD 1.20-1.80 per cubic meter and new withdrawal surcharges render kraft pulping uneconomic, entrenching recycled-fiber dependence.

How does digital printing benefit regional brand owners?

Digital presses eliminate plate costs, cut makeready time to minutes, and support variable data, enabling hyper-local SKUs and reduced inventory for short campaigns.

Which GCC country shows the fastest growth in corrugated demand?

The United Arab Emirates, buoyed by warehouse expansion and a plastic-ban policy, is forecast to post a 6.13% CAGR through 2031.

Page last updated on: