Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

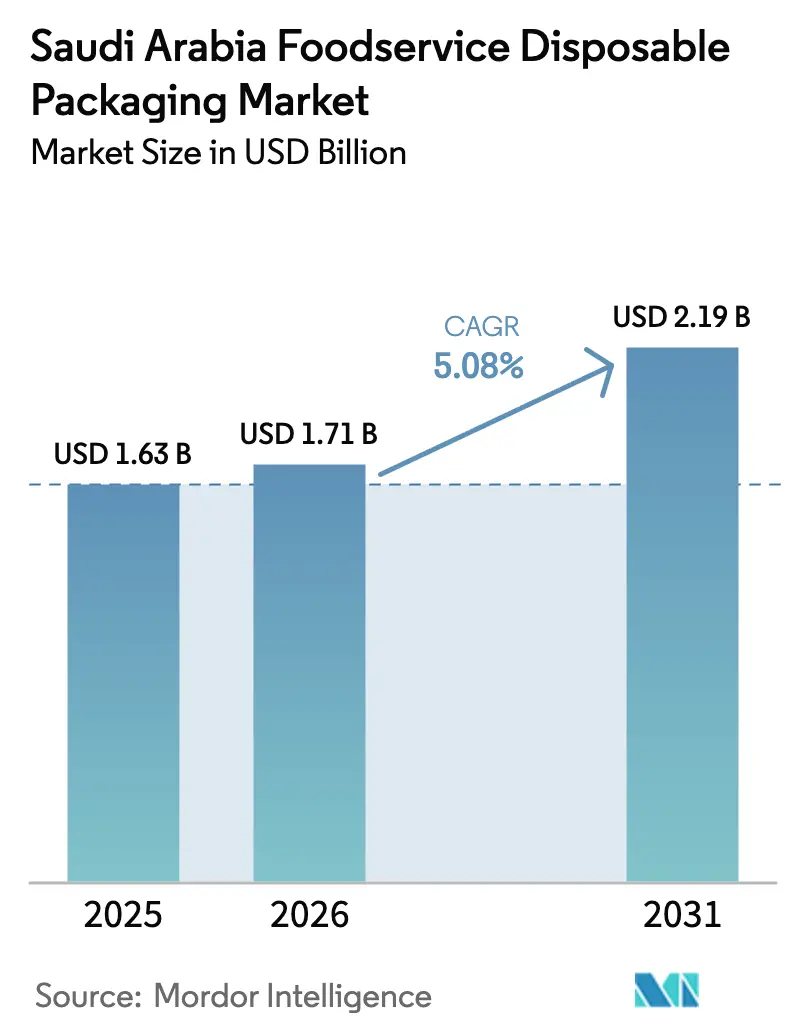

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

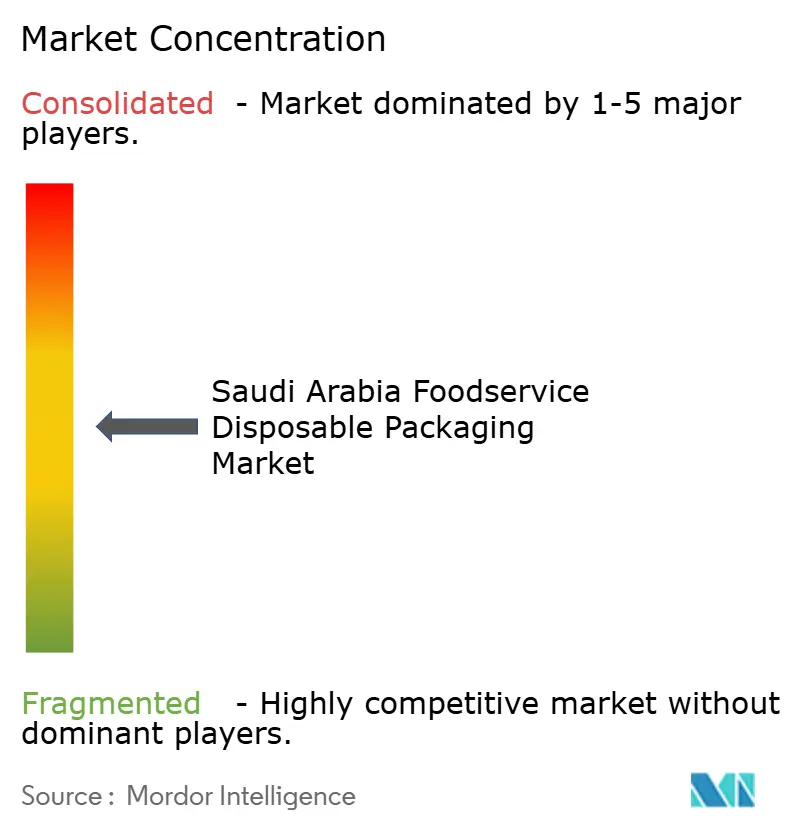

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Foodservice Disposable Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia foodservice disposable packaging market size is projected to expand from USD 1.63 billion in 2025 and USD 1.71 billion in 2026 to USD 2.19 billion by 2031, registering a CAGR of 5.08% between 2026 and 2031. The upward trajectory reflects a delivery-first culture, a swelling tourist inflow under Vision 2030, and sustained capital spending on giga-projects that embed zero-waste procurement rules. Quick-service chains continue to reshape consumer expectations for tamper-evident, logo-rich formats, while dark kitchens are erasing dine-in ware from operating models. Polypropylene feedstock volatility, a widening price gap between biopolymers and conventional resins, and infrastructure gaps in municipal recycling temper near-term profit margins but also create clear opportunities for differentiated material science and certified compostable offerings. Overall, the Saudi Arabia foodservice disposable packaging market is evolving from a cost-driven supply chain toward a value-driven ecosystem in which compliance credentials, material circularity, and delivery-optimized design carry measurable commercial weight.

Key Report Takeaways

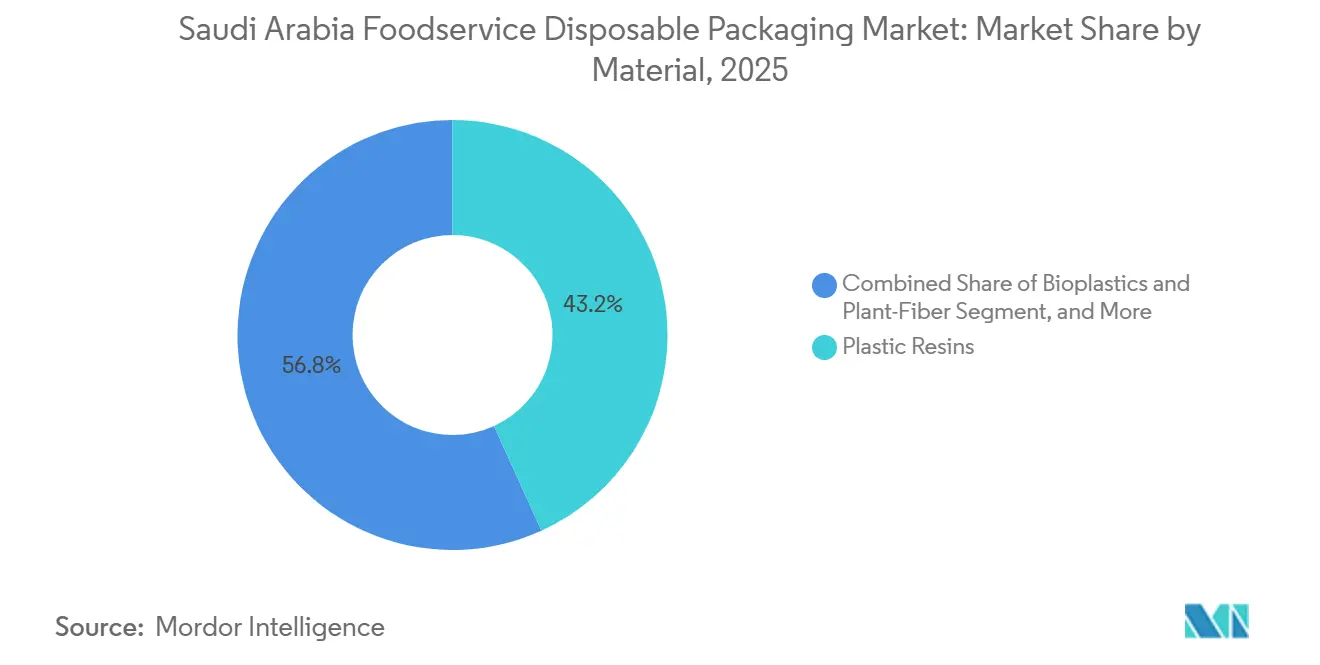

- By material, plastic resins captured 43.21% of Saudi Arabia foodservice disposable packaging market share in 2025, whereas bioplastics and plant-fiber alternatives are set to expand at a 6.21% CAGR to 2031.

- By product, cups commanded 32.12% share of the Saudi Arabia foodservice disposable packaging market size in 2025 and clamshells are projected to grow at 6.94% CAGR over 2026-2031.

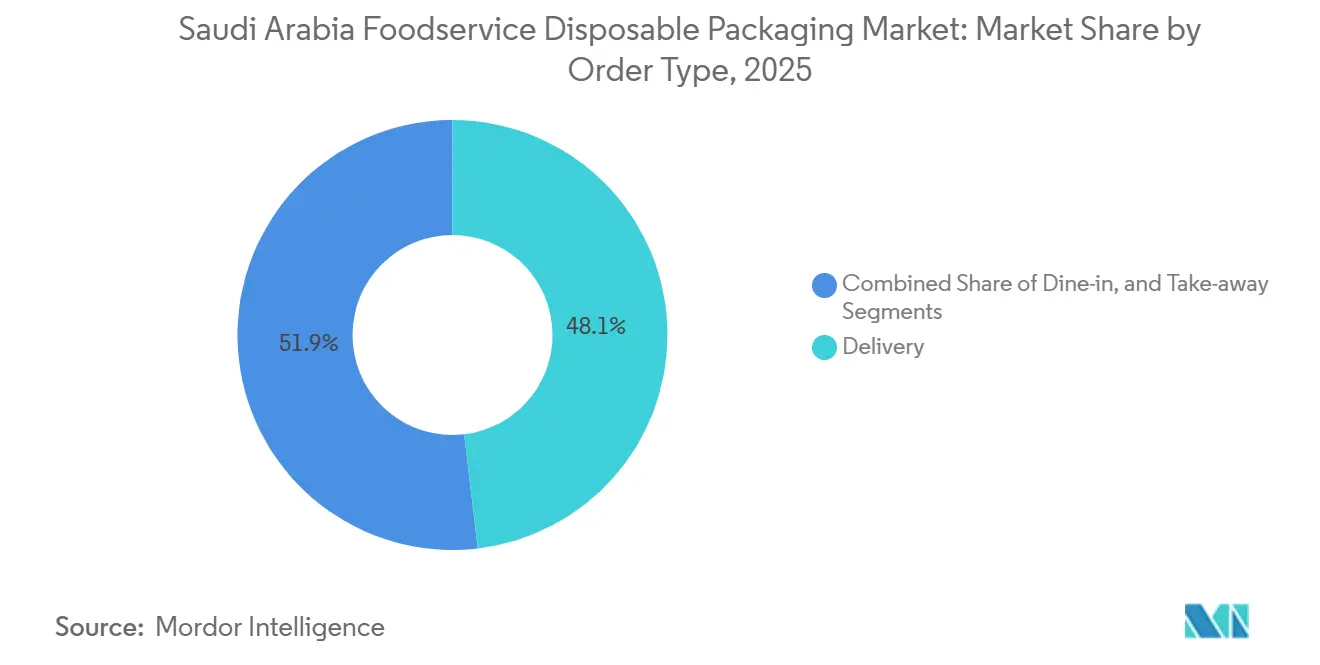

- By order type, delivery accounted for 48.12% volume in 2025 and is advancing at a 5.61% CAGR through 2031.

- By application, quick-service restaurants led with 36.21% revenue share in 2025, while catering services are forecast to record the fastest growth at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Foodservice Disposable Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In QSR And Delivery-First Formats | +1.8% | Riyadh, Jeddah, Dammam | Medium Term (2–4 Years) |

| Government Push For Oxo-Biodegradable Compliance | +1.2% | National | Short Term (≤ 2 Years) |

| Rising Tourist Inflow Under Vision 2030 Boosts On-The-Go Meals | +1.0% | National Hot Spots | Long Term (≥ 4 Years) |

| Growth Of Branded Coffee-Shop Chains | +0.7% | Urban Cores | Medium Term (2–4 Years) |

| Emergence Of Dark Kitchens Requiring Unit-Dose Packs | +0.6% | Riyadh, Jeddah, Eastern Province | Short Term (≤ 2 Years) |

| Large-Scale Giga-Projects Adopting Zero-Waste Mandates | +0.5% | NEOM, Red Sea, Qiddiya, Diriyah Gate | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Surge in QSR and Delivery-First Formats

Quick-service outlets and delivery-only brands processed more than 200 million digital orders in 2024, cementing a nationwide pivot toward single-use clamshells, leakproof cups, and grease-resistant wraps that withstand 30-45 minute transit windows. Household takeaway frequency rose to 3.2 meals per week in 2024, almost doubling the 2020 level, and each of the 200+ dark kitchens operating in the kingdom consumes roughly 10,000-15,000 disposable units per month. As delivery platforms mandate tamper-evident lids to curb refund claims, converters that master tight-tolerance thermoforming are capturing premium contracts. The Saudi Arabia foodservice disposable packaging market therefore benefits directly from structural changes in dining behavior rather than from cyclical shocks.

Government Push for Oxo-Biodegradable Compliance

SASO regulations that became fully enforceable in 2024 require that every polyethylene or polypropylene film under 250 microns incorporate oxo-biodegradable additives and display certification logos.[1]SASO, “Technical Regulation for Oxo-Biodegradable Plastics,” saso.gov.sa Although food-contact containers remain exempt, the rule has triggered plant-fiber substitution in secondary wraps and propelled converters to secure compliance marks quickly to avoid retailer penalties. Multinational QSR chains are voluntarily expanding the requirement to primary items, even paying a 20-30% premium for bagasse clamshells to maintain global sustainability scorecards. The regulation thus accelerates demand for value-added formulations and new extrusion lines calibrated for additive-laden resins.

Rising Tourist Inflow Under Vision 2030 Boosts On-the-Go Meals

Visitor numbers climbed from 100 million in 2024 toward a 150 million target for 2030, with an incremental 362,000 hotel keys under construction.[2]Saudi Tourism Authority, “Vision 2030 Tourism Targets,” visitsaudi.com Resorts at the Red Sea coast operate under mandatory plastic-free charters, driving large-volume orders for compostable bowls and paper-based wraps. Religious tourism creates seasonal peaks, as caterers in Mecca and Medina purchase 20-30 million disposable items during Hajj alone. As a result, the Saudi Arabia foodservice disposable packaging market captures both steady urban demand and pronounced event spikes.

Growth of Branded Coffee-Shop Chains

The domestic coffee sector expanded to USD 1.2 billion in 2024 and is compounding at 8-10% annually. Starbucks plans to surpass 400 Saudi stores by 2030, while specialty roasters such as % Arabica and Brew92 are rolling out 15-20 new cafés each year.[3] Starbucks Corporation, “Middle East Expansion Strategy,” starbucks.com Every site consumes up to 3,000 cups plus lids weekly, with a rising share devoted to dome-lidded PET formats for iced drinks. Consequently, high-clarity resins and double-wall paperboard benefit most, enriching the product mix and price points for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polyolefin feedstock price volatility | -0.9% | Nationwide, plastics subsectors | Short term (≤ 2 years) |

| Import dependency for specialty biopolymers | -0.6% | Premium pack segments, urban nodes | Medium term (2-4 years) |

| Municipal waste-sorting gaps limit recycling feedstock | -0.4% | Urban centers, particularly Riyadh, Jeddah, Dammam | Long term (≥ 4 years) |

| Cultural resistance to single-use items in religious events | -0.3% | Holy cities during Hajj and Umrah seasons | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polyolefin Feedstock Prices

Polypropylene quotations declined from USD 1,200 per ton in 2022 to USD 900-1,000 in 2025, creating 20-25% margin compression for converters holding higher-priced inventory, ICIS reported. Similar oscillations in polyethylene and polystyrene can create working-capital stress, especially for small processors without hedging tools. Masterbatch additives needed are often imported, so lead times stretch to 8-12 weeks, amplifying exposure to exchange-rate swings. Until feedstock pricing stabilizes, capital allocation toward new tooling or compostable lines remains cautious.

Import Dependency for Specialty Biopolymers

Saudi converters source polylactic acid and PBAT from Asia and Europe at landed costs 2.5-3.5 times higher than polypropylene, with freight and customs adding another 15-20%.[4]Bioplastics Magazine, “PLA and PBAT Imports Middle East,” bioplasticsmagazine.com Minimum container loads of 20-25 tons translate into elevated carrying costs for mid-tier firms. Emirates Biotech’s Embio launch in 2026 opens a regional option, yet volumes remain insufficient to materially lower price points. The premium pricing constrains broad substitution and caps growth of compostable formats to contracts where brand reputation outweighs cost sensitivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biopolymers Challenge Resin Dominance

Plastic resins maintained 43.21% share in 2025, driven by cost advantages and established processing lines. Within the Saudi Arabia foodservice disposable packaging market size for plastics, polypropylene remains the go-to choice for hot-beverage cups and hinge-lid containers, while PET secures cold-cup and salad-bowl applications because of its clarity and barrier properties. Paperboard retains a mid-teens slice, buoyed by domestic capacity expansion from Middle East Paper Company. Bioplastics and plant-fiber options are projected to grow 6.21% CAGR through 2031, led by bagasse plates and molded-fiber bowls that meet giga-project zero-waste criteria. However, Saudi Arabia foodservice disposable packaging market share for polylactic acid remains modest because its unit cost is 2.5-3.5 times that of polypropylene despite recent regional supply introductions.

Across 2026-2031, resin processors that integrate oxo-biodegradable additives into films can defend incumbent volumes while preparing for longer-term shifts toward certified compostables. Suppliers that hold both SASO logos for secondary wraps and third-party compostability marks for primary containers can arbitrage compliance gaps and command premiums among global QSR clients.

By Product: Clamshells Surge on Delivery Optimization

Cups dominated 32.12% of 2025 demand as café culture deepened across Saudi cities. The Saudi Arabia foodservice disposable packaging market anticipates the steepest acceleration in clamshells, forecast at a 6.94% CAGR through 2031 on the back of delivery-platform requirements for tamper-evident and stackable designs. Stackability increases thermal retention within insulated courier bags and enables drivers to deliver more orders per trip, cutting platform costs. Bowls, lids, and tubs address health-centric menus that include salads, smoothie bowls, and grain mixes.

Foam polystyrene has ceded ground to molded fiber as brands avert negative perceptions, particularly after several municipalities limited foam use in 2025. Suppliers of paper-wrapped cutlery kits and grease-resistant bagasse clamshells differentiate by embedding QR codes that verify compostability claims and support downstream waste-sorting initiatives at giga-project resorts.

By Order Type: Delivery Channel Sustains Leadership

Delivery captured 48.12% of 2025 volume and is widening its lead with a 5.61% CAGR through 2031, supported by an average revenue per user of more than USD 600, the region’s highest. Take-away retains a high-twenties slice, especially in coffee shops where consumers avoid courier fees, yet its packaging profile mirrors delivery demands for leak-proof, dual-insulated formats. Dine-in rebounds modestly post-pandemic but cannot reverse the structural tilt toward off-premise consumption.

More than 200 dark kitchens in Riyadh, Jeddah, and Dammam avoid ceramic ware altogether, converting every order into a packaging event. Converters have responded by installing digital printing units for low-minimum-order runs, enabling cloud-kitchen brands to rotate designs and seasonal promotions without excess inventory.

By Application: Catering Services Outpace QSR Growth

Quick-service restaurants secured 36.21% of 2025 value by virtue of 2,000+ operating outlets nationwide. Yet catering services will expand at a 6.61% CAGR to 2031, the fastest among applications, as NEOM, Red Sea, and Qiddiya stage hundreds of investor days, concerts, and sporting events annually, each demanding compostable or reusable packaging. FIFA World Cup 2034 and Expo 2030 Riyadh may together require 200-300 million single-use items, creating once-in-a-generation surges in procurement volumes.

Full-service restaurants, coffee outlets, and retail still furnish mid-single-digit shares, but their influence on material innovation is disproportionate because premium coffee houses specify double-wall aesthetics and custom graphics. Mobile vendors in festival zones favor ultra-lightweight trays and wrap formats to maximize vehicle payloads, underscoring the need for low-gauge, yet puncture-resistant, substrates.

Geography Analysis

Riyadh, Jeddah, and Dammam together account for roughly 70% of national demand due to dense populations, high platform penetration, and expatriate workforces seeking convenience. Riyadh’s corporate towers and government ministries underpin institutional catering volumes, while Jeddah’s Red Sea port status attracts tourism-linked hotels that prefer branded paper cups and molded-fiber bowls. Eastern Province demand skews toward oil-industry canteens serving shift workers on tight turnaround cycles.

Seasonal pilgrimage flows create acute spikes in Mecca and Medina, where catering operators order tens of millions of disposable items during Hajj, putting pressure on supply chains that already face tight resin allocations. Waste-sorting remains underdeveloped nationwide, with only 15% of post-consumer packaging entering organized streams, although the Saudi Green Initiative targets 85% landfill diversion by 2035.

Vision 2030 giga-projects are redrawing the demand map. NEOM, located in Tabuk Province, is building zero-waste hotels and smart-city districts that specify third-party compostability as a tender pre-requisite NEOM. The Red Sea Project’s 50 luxury resorts similarly reject conventional plastics, while Qiddiya, near Riyadh, will average an estimated 17 million visitors yearly, sustaining high-volume supply contracts for operators that can validate circular designs. Converters are therefore establishing regional stock points and investing in recycling partnerships to secure preferred-supplier status.

Competitive Landscape

The Saudi Arabia foodservice disposable packaging market accommodates a mid-concentration structure: the five largest players control under 40% of sales, leaving white space for regional specialists. Napco National bolstered vertical integration by acquiring Arabian Flexible Packaging in August 2025, adding 15,000 tons of flexible capacity and enabling bundle deals that combine rigid clamshells with printed wraps. Hotpack Packaging Industries committed SAR 1 billion (USD 266 million) to a Saudi mega-plant featuring Industry 4.0 automation, positioning itself to undercut imports while servicing giga-project timelines.

Huhtamaki leverages its blueloop recyclable mono-material range to win contracts with multinational QSR brands seeking to simplify post-consumer sorting. Detpak introduced AS 5810-certified sugarcane clamshells in 2024, capturing upscale coffee-chain demand. New entrants such as Emirates Biotech, with its Embio PLA series, aim to displace Asian imports and loosen price premiums on compostable grades.

Feedstock integration remains a key differentiator. Players adjacent to SABIC’s resin plants enjoy shorter lead times and insulate margins during price spikes. Conversely, niche biopolymer converters win tenders that stipulate zero-waste criteria even when their unit prices exceed polypropylene. Digital printing, QR-based authentication, and tamper-evident sealing continue to climb procurement scorecards, encouraging capital spend on specialty tooling.

Saudi Arabia Foodservice Disposable Packaging Industry Leaders

Napco National Company

Hotpack Packaging Industries L.L.C

SAQR Pack Company

Falcon Pack Industry LLC

Emirates National Factory for Plastic Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Emirates Biotech launched the Embio polylactic acid line, offering injection-mold and extrusion grades with 110 °C heat deflection, tailored for hot-beverage lids.

- August 2025: Napco National acquired Arabian Flexible Packaging, adding 15,000 tons of flexible capacity and expanding bundled rigid-flexible offerings.

- August 2025: Cortec Corporation introduced Eco Works 100 compostable film certified to ASTM D6400 and EN 13432, aimed at catering pouches.

- May 2025: Hotpack Packaging Industries invested USD 100 million in a 70,000-square-foot New Jersey facility, earmarking 30% output for export to South America.

Saudi Arabia Foodservice Disposable Packaging Market Report Scope

The Saudi Arabia Foodservice Disposable Packaging Market Report is Segmented by Material (Plastic Resins, Bioplastics and Plant-Fiber, Paper and Paperboard, Aluminum Foil, Bagasse and Moulded Fiber, Other Materials), Product (Cups, Lids, Tubs and Containers, Bowls, Trays, Clamshells, Plates, Cutlery, Bags and Wraps, Cartons, Straws), Order Type (Dine-in, Take-away, Delivery), and Application (QSR, Full-Service Restaurants, Coffee and Snack Outlets, Retail, Institutional and Hospitality, Mobile Vendors and Food Trucks, Catering Services, Other Applications). Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastic Resins | PP |

| PET | |

| PE | |

| PS | |

| PLA | |

| Other Plastic Resins | |

| Bioplastics and Plant-Fiber | |

| Paper and Paperboard | |

| Aluminum Foil | |

| Bagasse and Moulded Fiber | |

| Other Materials |

By Product

| Cups |

| Lids |

| Tubs and Containers |

| Bowls |

| Trays |

| Clamshells |

| Plates |

| Cutlery |

| Bags and Wraps |

| Cartons |

| Straws |

By Order Type

| Dine-in |

| Take-away |

| Delivery |

By Application

| Quick-Service Restaurants (QSR) |

| Full-Service Restaurants |

| Coffee and Snack Outlets |

| Retail Establishments |

| Institutional and Hospitality |

| Mobile Vendors and Food Trucks |

| Catering Services |

| Other Applications |

| By Material | Plastic Resins | PP |

| PET | ||

| PE | ||

| PS | ||

| PLA | ||

| Other Plastic Resins | ||

| Bioplastics and Plant-Fiber | ||

| Paper and Paperboard | ||

| Aluminum Foil | ||

| Bagasse and Moulded Fiber | ||

| Other Materials | ||

| By Product | Cups | |

| Lids | ||

| Tubs and Containers | ||

| Bowls | ||

| Trays | ||

| Clamshells | ||

| Plates | ||

| Cutlery | ||

| Bags and Wraps | ||

| Cartons | ||

| Straws | ||

| By Order Type | Dine-in | |

| Take-away | ||

| Delivery | ||

| By Application | Quick-Service Restaurants (QSR) | |

| Full-Service Restaurants | ||

| Coffee and Snack Outlets | ||

| Retail Establishments | ||

| Institutional and Hospitality | ||

| Mobile Vendors and Food Trucks | ||

| Catering Services | ||

| Other Applications |

Key Questions Answered in the Report

How large will disposable packaging demand become by 2031 in Saudi Arabia?

The Saudi Arabia foodservice disposable packaging market is on track to reach USD 2.19 billion by 2031, expanding at a 5.08% CAGR from 2026.

Which product format is growing the fastest?

Clamshells are projected to grow at a 6.94% CAGR through 2031, benefitting from delivery-platform requirements for tamper-evident, stackable designs.

Why are biopolymers gaining share despite higher prices?

Giga-project zero-waste mandates and voluntary sustainability commitments by multinational QSR chains are driving 6.21% CAGR growth in bioplastics and plant-fiber packaging.

What restrains broader adoption of compostable materials?

Import dependency keeps polylactic acid and PBAT prices 2.5-3.5 times higher than polypropylene, limiting mass-market substitution until regional capacity scales.

Which order channel leads volume growth?

Delivery captured 48.12% of 2025 volume and is forecast to rise at a 5.61% CAGR as average revenue per user tops USD 600.

How fragmented is the competitive landscape?

The top five suppliers hold under 40% share, yielding a moderate concentration level that favors innovation-focused niche players.

Page last updated on: