Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

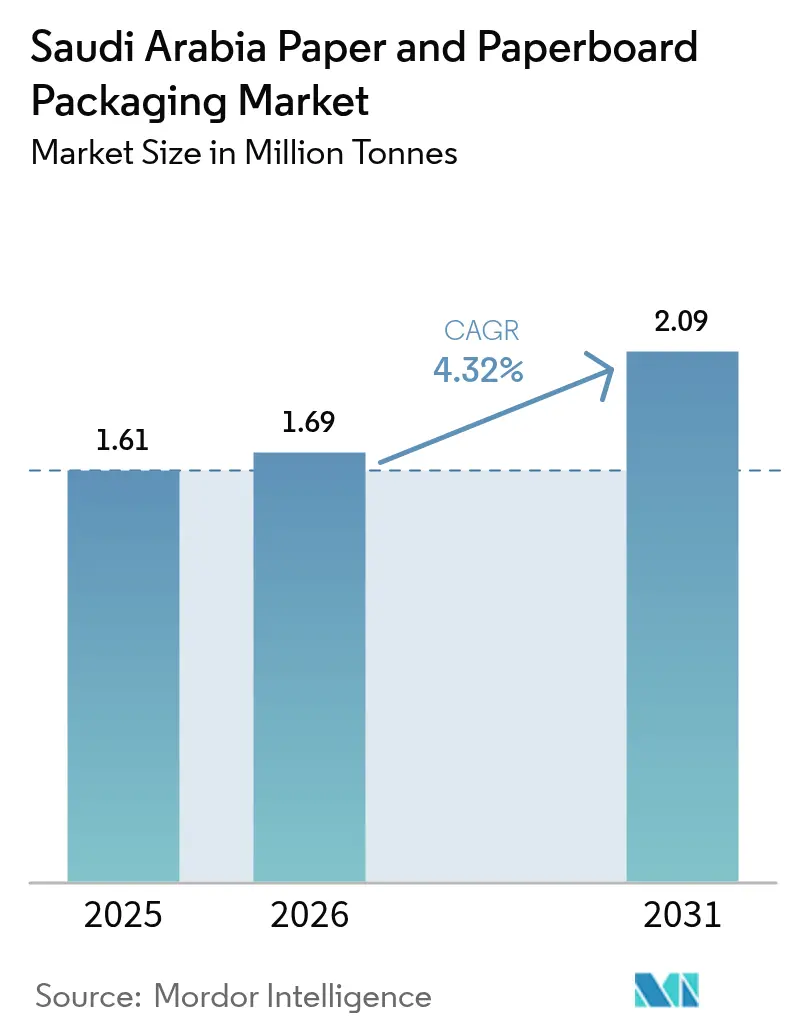

| Base Year Market Size (2025) | 1.61 Million tonnes |

| Market Volume (2026) | 1.69 Million tonnes |

| Market Volume (2031) | 2.09 Million tonnes |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

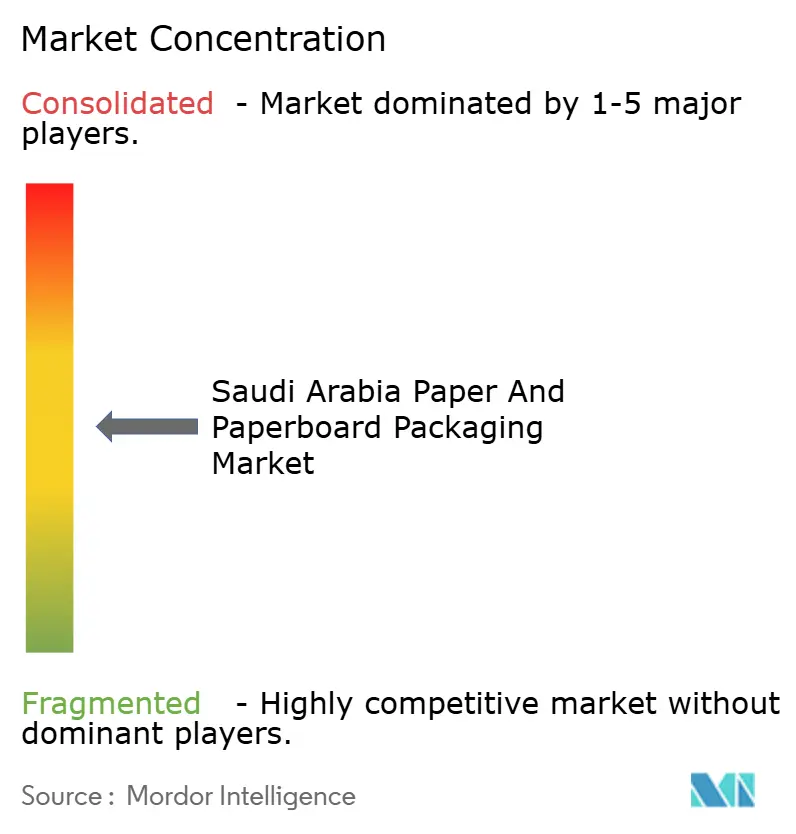

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Paper And Paperboard Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia paper and paperboard packaging market size was valued at 1.61 million tonnes in 2025 and is estimated to grow from 1.69 million tonnes in 2026 to reach 2.09 million tonnes by 2031, at a CAGR of 4.32% during the forecast period (2026-2031). Rapid urbanization, Vision 2030 localization incentives, and tightening plastic-waste rules are keeping demand on a firm upward slope even as converter margins confront higher power and water tariffs. Multinational integrators are adding local capacity to shield themselves from imported kraft-liner volatility, while digital printing is unlocking profitable short-run jobs for SKU-rich fast-moving consumer goods. At the same time, the e-commerce boom is forcing a pivot toward lightweight, mailer-friendly substrates that can survive automated sortation without inflating dimensional-weight charges. Mills that lock in long-term fiber contracts and invest in on-site renewables look best placed to navigate the cost curve and capture the extra 500,000 tonnes of volume expected this decade.

Key Report Takeaways

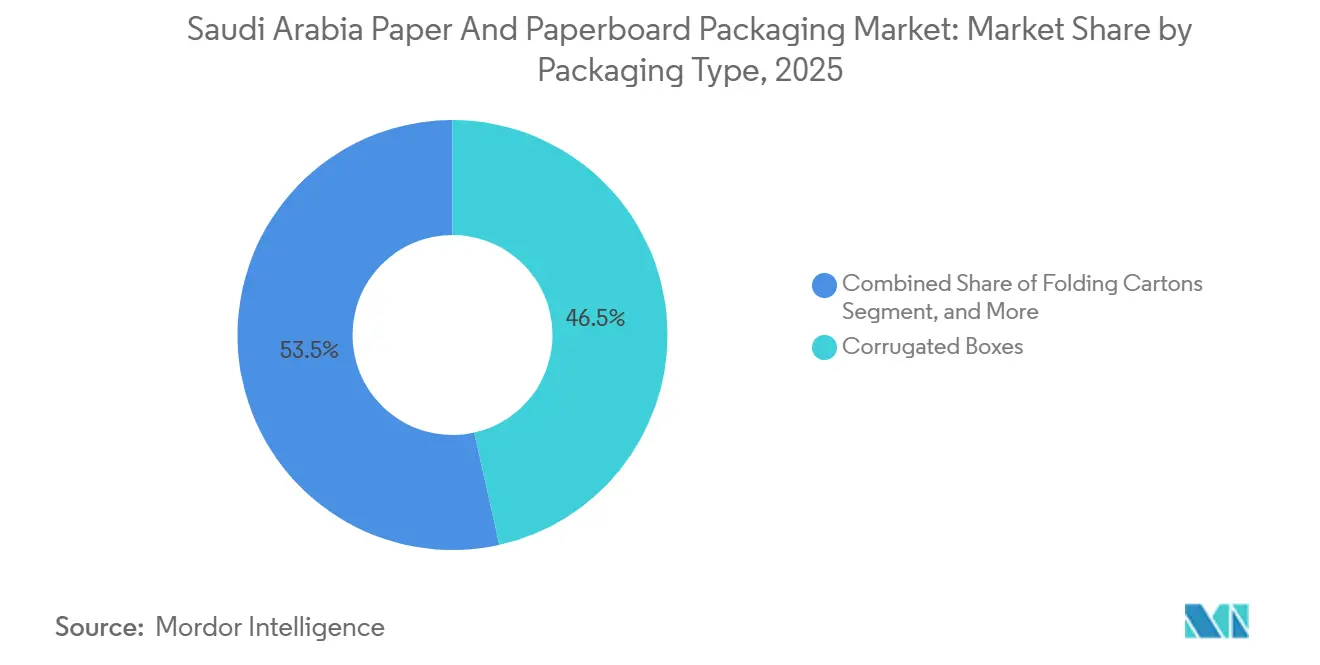

- By packaging type, corrugated boxes led with 46.51% share of the Saudi Arabia paper and paperboard packaging market size in 2025, while liquid cartons are projected to expand at a 5.31% CAGR through 2031.

- By end-user industry, food and beverage accounted for 37.14% of the Saudi Arabia paper and paperboard packaging market share in 2025, whereas e-commerce and retail are forecast to record a 5.57% CAGR to 2031.

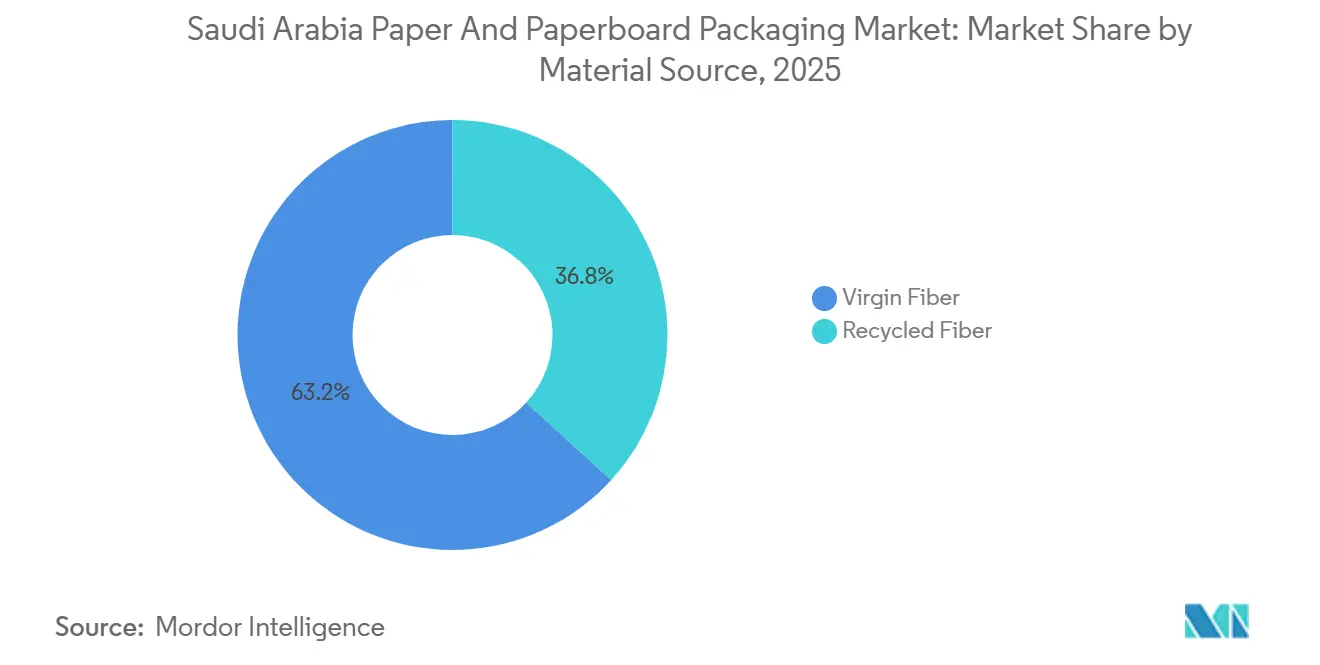

- By material source, virgin fiber dominated with 63.21% volume share in 2025, and recycled fiber is set to advance at a 4.71% CAGR during 2026-2031.

- By packaging level, secondary formats captured 48.22% of 2025 volume, and tertiary packaging is projected to rise at a 4.94% CAGR on the back of the national logistics build-out.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Paper And Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food and Beverage Demand Surge for Corrugated Transit Packaging | +0.9% | Riyadh, Jeddah, Dammam Corridors | Medium Term (2–4 Years) |

| Plastic-Ban Policies Boosting Paper Conversion Volumes | +0.7% | Riyadh and Eastern Province | Short Term (≤ 2 Years) |

| E-Commerce Same-Day Delivery Fueling Lightweight Mailers | +0.8% | National, Led by Riyadh and Jeddah | Medium Term (2–4 Years) |

| FMCG SKU Proliferation Requiring Short-Run Digital Cartons | +0.5% | Riyadh and Jeddah Retail Hubs | Long Term (≥ 4 Years) |

| Vision 2030 Localization Incentives for Paper Converters | +0.6% | Jubail, Yanbu, MODON Zones | Long Term (≥ 4 Years) |

| Expansion of Date-Export Cluster Around Al-Qassim | +0.3% | Al-Qassim, Hail Provinces | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Food and Beverage Demand Surge for Corrugated Transit Packaging

Food retail sales topped USD 50 billion in 2024 and continue to grow at an annual rate above 5% as the population and per-capita consumption rise. The Saudi Food and Drug Authority licensed 9,155 food facilities in 2025, an 18% increase that directly expanded the corrugated user base.[1]Saudi Food and Drug Authority, “SFDA Reports 18% Growth in Licensed Factories and Warehouses,” sfda.gov.sa Peak-season volumes during Ramadan and Hajj amplify short-run spikes, encouraging retailers to standardize pallet-ready cases that speed cross-docking through multimodal hubs. Because the Kingdom imports roughly 70% of its food, packaging tonnage tracks physical throughput rather than retail pricing, insulating converters from commodity deflation. Major chains such as Panda and Tamimi negotiate multi-year supply contracts that stabilize converter plant utilization but compress per-unit margins.

Plastic-Ban Policies Boosting Paper Conversion Volumes

Municipal bans on single-use plastic bags in Riyadh and Jeddah accelerate substitution to kraft paper carriers as retailers seek compliant options. Saudi Investment Recycling Company’s 81% recycling target pushes brand owners toward fiber-based formats compatible with municipal recovery streams. QSR chains including AlBaik shifted in-store cups and wraps to paper-lined composites, raising short-run flexo orders for domestic converters. Government eco-labeling pilots reward products in recyclable paperboard, nudging FMCG portfolios toward folding cartons. Early adopters gain shelf visibility, reinforcing paper’s environmental halo. The regulatory momentum shortens payback periods for new curtain coater and aqueous-barrier lines, sustaining capital expenditure by leading mills.

E-Commerce Same-Day Delivery Fueling Lightweight Mailers

Online grocery revenue hit USD 1.6 billion in 2024 and is growing above 10% annually as the number of registered e-commerce businesses passed 40,000. Same-day delivery demands mailers that cut dimensional weight yet resist rough handling, prompting converters to adopt micro-flute designs that are 20-30% lighter than legacy B-flute boxes. Smart-hub investments, such as the Jeddah Central Logistics Zone, favor bar-code-rich mailers compatible with automated sortation.[2]Nikhita Jayakumar, “Top 3 FMCG Trends in Saudi Arabia and the UAE,” Maersk, maersk.com Digital presses like HP PageWide support variable graphics and QR codes on these formats, boosting customer engagement without slowing fulfillment. The convergence of logistics speed, consumer expectations, and sustainability targets keeps this driver firmly in positive territory.

Vision 2030 Localization Incentives for Paper Converters

Tax holidays, subsidized land, and Public Investment Fund co-investment are encouraging regional and multinational players to build capacity inside the Kingdom. Middle East Paper Company’s USD 475 million fifth line will add 450,000 tonnes of containerboard by 2027, slicing dependency on imported kraft liner. Hotpack Global is spending USD 267 million on a 2.4 million square-foot plant that targets paper, biomass, and polymer substrates with Industry 4.0 automation. While industrial power now costs 18 halalas per kWh, on-site solar and heat-recovery retrofits help protect internal rates of return. As localization thresholds rise in public tenders, converters with Saudi-made credentials gain bidding preference, reinforcing the strategic pull.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Kraft-Liner Price Volatility | -0.4% | Jeddah and Dammam Port-Dependent Sites | Short Term (≤ 2 Years) |

| Power-Tariff Hikes Raising Mill OPEX | -0.3% | Energy-Intensive Mills in Jubail and Dammam | Medium Term (2–4 Years) |

| High Freshwater Footprint Amid Water Scarcity | -0.2% | Central Regions with Limited Desalination | Long Term (≥ 4 Years) |

| Slow Adoption of Recycled Fiber Due to Food-Grade Hurdles | -0.2% | National, SFDA Certification Bottleneck | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Imported Kraft-Liner Price Volatility

Global pulp supply tightness lifted kraft-liner spot prices 18% between 2023 and 2024, translating into margin compression for Saudi converters who import 92% of their linerboard. Hedging instruments remain limited on the regional commodity exchanges, exposing balance sheets to FX swings. Middle East Paper Company’s 7% net loss in 2024 showcases how price spikes erode profitability even with integrated recycling capacity. Smaller plants resort to shorter customer contracts or pass-through surcharges, risking volume loss to plastic alternatives when box prices surge.

Power-Tariff Hikes Raising Mill OPEX

Electricity at 18 halalas per kWh and industrial gas at SAR 7.23 per MMBtu lifted 2025 mill cash costs and narrowed the spread with regional peers, which are still on subsidized tariffs.[3]Saudi Electricity Company, “Tariffs and Rates,” se.com.sa Paper mills average 1.5-2.5 MWh per tonne, so a one-halala hike dents EBITDA by roughly 1.2 percentage points. Renewable energy targets promise future relief, yet grid interconnection and capital hurdles delay near-term savings. Mills' slow to decarbonize also risks carbon-border taxes when exporting to Europe, adding an external compliance cost to the domestic tariff burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Corrugated Dominance Drives Transit Solutions

Corrugated boxes owned 46.51% of 2025 tonnage in the Saudi Arabia paper and paperboard packaging market, a lead entrenched by food logistics, industrial shipment, and high-velocity e-commerce orders. The format’s stacking strength and ability to accept micro-flute lightweighting keep it resilient even as liner prices gyrate. Digital post-print solutions let converters turn corrugated into a marketing canvas, adding value beyond plain brown board. Liquid cartons, though representing a smaller base, will rise at 5.31% CAGR because UHT dairy and juice players need shelf-stable packs that travel long distances without refrigeration. Aseptic-line upgrades signed in 2025 cut water use by 36 million liters per year, easing operational cost pressures and aligning with retailer sustainability pledges.

Demand diversity supports both extremes. Corrugated gains from the National Transport and Logistics Strategy, which favors pallet-standardized secondary and tertiary cases for automated hubs. Meanwhile, liquid cartons benefit from rising health-and-wellness consumption and the export of flavored milk to GCC neighbors. The Saudi Arabia paper and paperboard packaging market continues to view corrugated as the workhorse and liquid cartons as the growth engine, a twin-track dynamic that cushions converters against cyclical swings.

By End-User Industry: Food Dominates, E-Commerce Accelerates

Food and beverage accounted for 37.14% of the 2025 volume in the Saudi Arabia paper and paperboard packaging market, reflecting the sector’s need for corrugated transit cases, folding cartons, and aseptic bricks. Retail chains handling Ramadan and Hajj surges value suppliers that can add weekend shifts without compromising quality. On the other hand, e-commerce and retail will clock a 5.57% CAGR, the fastest among end-users, propelled by 46% shopping penetration expected by 2030 and a same-day delivery culture popularized by quick-commerce apps.

Converters targeting e-commerce differentiate through padded mailers that cut dimensional weight while withstanding mechanical sorters. They also overlay QR codes for engagement, matching the omnichannel strategies of grocers like Panda and LuLu. Food converters face tighter SFDA oversight on dual-date labeling and Arabic-language compliance, raising the premium on digital presses capable of handling artwork changes overnight. As a whole, the Saudi Arabia paper and paperboard packaging market balances the steady demand for bulk food packaging with the fast-growing, customization-heavy e-commerce stream.

By Material Source: Virgin Leads, Recycled Gains Ground

Virgin fiber held 63.21% of 2025 tonnage because food-contact applications still require higher purity and strength. Imported kraft liner remains the backbone for heavy-duty corrugated, although domestic capacity additions will trim exposure from 2027 onward. Recycled fiber, now at 36.79%, is moving toward a 4.71% CAGR on the back of the National Waste Management Strategy’s 47% diversion goal. A USD 3 million liquid-carton recycling plant that came online in 2024 processes 8,000 tonnes a year, a modest but symbolic step toward circularity.

Scaling recycled content hinges on improved curbside collection outside Riyadh and Jeddah, and on de-inking lines that can meet the food-grade thresholds set by the SFDA. Until then, most recycled tonnage will feed secondary and tertiary boxes where direct food contact is not an issue. Virgin pulp will therefore continue to anchor critical applications, but the Saudi Arabia paper and paperboard packaging market is unmistakably tilting toward higher recycled ratios wherever certification hurdles are surmountable.

By Packaging Level: Secondary Commands, Tertiary Gains From Logistics Push

Secondary formats captured 48.22% of the 2025 volume, supplying shelf-ready trays and multipack wraps that speed stocking and reduce labor in hypermarkets. These packs double as marketing real estate, and digital inkjet lines let brands switch artwork in hours instead of days. Tertiary packaging, projected to grow at a 4.94% CAGR, rides the logistics infrastructure boom, which calls for pallet-optimized, RFID-capable corrugated outers.

Primary packs, liquid cartons, folding cartons, and coated paper bags, carry the regulatory load by ensuring food safety and traceability. SFDA-mandated Arabic labeling pushes brands toward pre-printed solutions over stickers to avoid compliance slips at border checks. As automated fulfillment centers proliferate, converters offering end-to-end expertise across all three levels stand to win integrated contracts, reinforcing the all-around appeal of the Saudi Arabia paper and paperboard packaging market.

Competitive Landscape

United Carton Industries floated 30% of its equity in May 2025 at a valuation of USD 533 million and controls close to 40% of national corrugated tonnage, highlighting mid-range concentration. Global majors such as Smurfit Westrock, DS Smith, Mondi, and International Paper are reinforcing Saudi footprints to hedge against freight and currency risks and to meet iktva localization quotas. Smurfit Westrock’s 2024 merger created a 23 million-tonne behemoth that can funnel scale savings and advanced digital presses into the Kingdom when demand spikes.

Regional challengers are equally active. Obeikan Investment Group, with 22 billion packs and USD 1 billion in sales, has moved into liquid packaging and partnered on an 8,000-tonne recycling facility to secure feedstock and circular credentials. Hotpack Global’s USD 267 million greenfield project will add biomass-based and polymer lines alongside its paper operations, leveraging Industry 4.0 to achieve cost and quality gains. White-space opportunities persist in post-consumer collection, food-grade recycled pulp, and cold-chain-resistant corrugated, niches that nimble local players can seize.

Digital printing is the current battleground for competition. Early adopters of HP PageWide and Xerox iGen technology now quote minimum runs of 500 cartons, winning promotional SKU work from retailers rolling out private-label ranges. Firms that integrate press data with enterprise-resource-planning systems can deliver JIT orders and real-time inventory views, a service edge that multi-plant giants sometimes struggle to match. Overall, the Saudi Arabia paper and paperboard packaging market rewards a hybrid model: global scale in raw materials married to local agility in converting and service.

Saudi Arabia Paper And Paperboard Packaging Industry Leaders

Gulf Carton Factory Company

United Carton Industries Company (UCIC)

Obeikan Investment Group

NAPCO National

Gulf East Paper & Plastic Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: United Carton Industries secured board approval to invest AED 74 million in expanding its Ras Al Khaimah corrugated-box plant, with construction slated to start in Q2 2026 and commercial production targeted for Q3 2027.

- February 2026: A follow-up market disclosure confirmed that the same Ras Al Khaimah project will lift United Carton Industries’ regional footprint and is expected to bolster group revenues once the line ramps up in 2027

- January 2026: Tetra Pak committed €60 million to build a pilot plant in Lund for paper-based barrier technology, a step that should accelerate the commercial roll-out of aluminum-free aseptic cartons and eventually benefit Saudi converters that import the company’s high-speed filling lines.

- January 2026: Tetra Pak’s Arabia newsroom outlined a programme to extend its new paper-based barrier structure to high-speed A3 filling platforms, indicating that the material will be available for large-scale dairy and juice applications supplied from the firm’s Jeddah factory once validation is complete

Saudi Arabia Paper And Paperboard Packaging Market Report Scope

The Saudi Arabia Paper and Paperboard Packaging Market Report is Segmented by Packaging Type (Folding Cartons, Corrugated Boxes, Liquid Cartons, Paper Bags and Sacks, Other Packaging Types), End-user Industry (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Household Care, Industrial Goods, E-Commerce and Retail, Other End-user Industries), Material Source (Virgin Fiber, Recycled Fiber), Packaging Level (Primary, Secondary, Tertiary). Market Forecasts are Provided in Volume (Tonnes).

By Packaging Type

| Folding Cartons |

| Corrugated Boxes |

| Liquid Cartons |

| Paper Bags and Sacks |

| Other Packaging Types |

By End-user Industry

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Household Care |

| Industrial Goods |

| E-Commerce and Retail |

| Other End-user Industries |

By Material Source

| Virgin Fiber |

| Recycled Fiber |

By Packaging Level

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| By Packaging Type | Folding Cartons |

| Corrugated Boxes | |

| Liquid Cartons | |

| Paper Bags and Sacks | |

| Other Packaging Types | |

| By End-user Industry | Food and Beverage |

| Healthcare and Pharmaceuticals | |

| Personal Care and Household Care | |

| Industrial Goods | |

| E-Commerce and Retail | |

| Other End-user Industries | |

| By Material Source | Virgin Fiber |

| Recycled Fiber | |

| By Packaging Level | Primary Packaging |

| Secondary Packaging | |

| Tertiary Packaging |

Key Questions Answered in the Report

What is the current volume of the Saudi Arabia paper and paperboard packaging market?

The market handled 1.69 million tonnes in 2026 and is on course to reach 2.09 million tonnes by 2031.

Which packaging type holds the largest share?

Corrugated boxes commanded 46.51% of 2025 volume thanks to strong demand from food, retail, and industrial users.

Which end-user segment is growing the fastest?

E-commerce and retail are projected to grow at a 5.57% CAGR as same-day delivery expands across the Kingdom.

How significant is recycled fiber adoption?

Recycled fiber represents 36.79% of 2025 tonnage and is forecast to rise at a 4.71% CAGR as collection systems improve.

What are the key cost pressures facing converters?

Imported kraft-liner price volatility and higher industrial power tariffs are the two largest cost headwinds.

Which regions outside the main metros show growth potential?

Al-Qassim and Hail provinces are emerging as clusters for date-export packaging that needs moisture-resistant corrugated formats.

Page last updated on: