Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

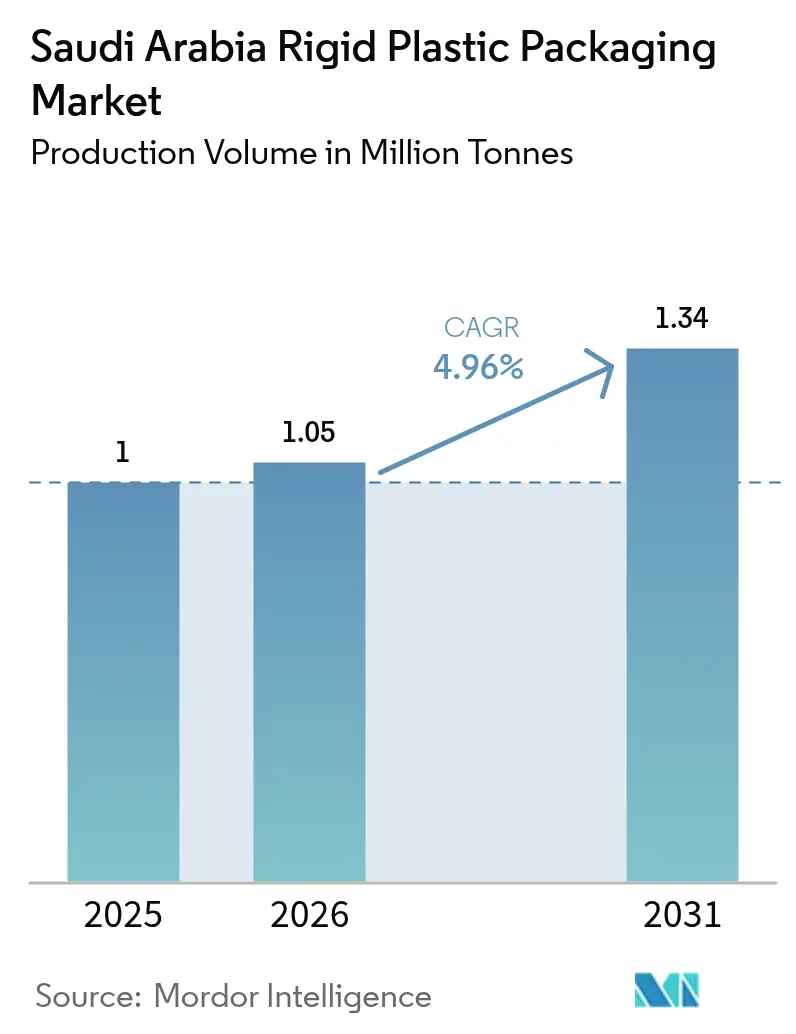

| Base Year Market Size (2025) | 1 Million tonnes |

| Market Volume (2026) | 1.05 Million tonnes |

| Market Volume (2031) | 1.34 Million tonnes |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

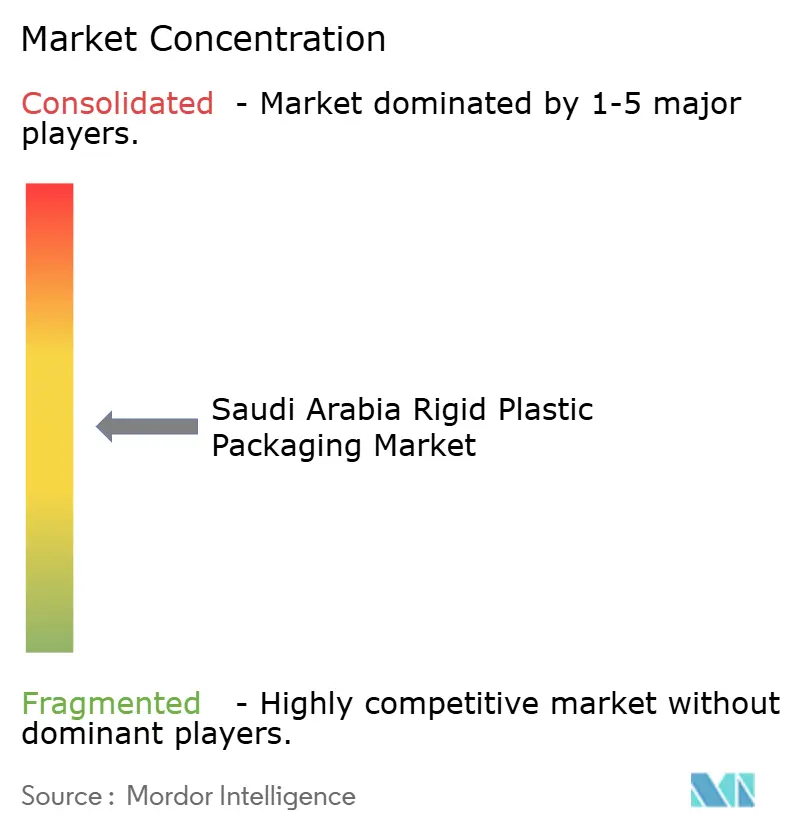

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia Rigid Plastic Packaging Market size in terms of production volume is expected to increase from 1 Million tonnes in 2025 to 1.05 Million tonnes in 2026 and reach 1.34 Million tonnes by 2031, growing at a CAGR of 4.96% over 2026-2031. Vision 2030’s push for downstream value capture, preferential ethane pricing, and localization mandates are steering converters toward higher-margin finished goods. Domestic resin expansions, serialization rules in healthcare, and the growth of quick commerce collectively expand end-market avenues while tightening quality requirements. Converter margins depend on the rapid adoption of automation and light-weighting as crude-linked resin swings compress spreads. Regulations on single-use formats, water scarcity levies, and carbon border taxes spur investments in chemical recycling and renewable energy certificates, keeping sustainability at the core of capital-spending roadmaps.

Key Report Takeaways

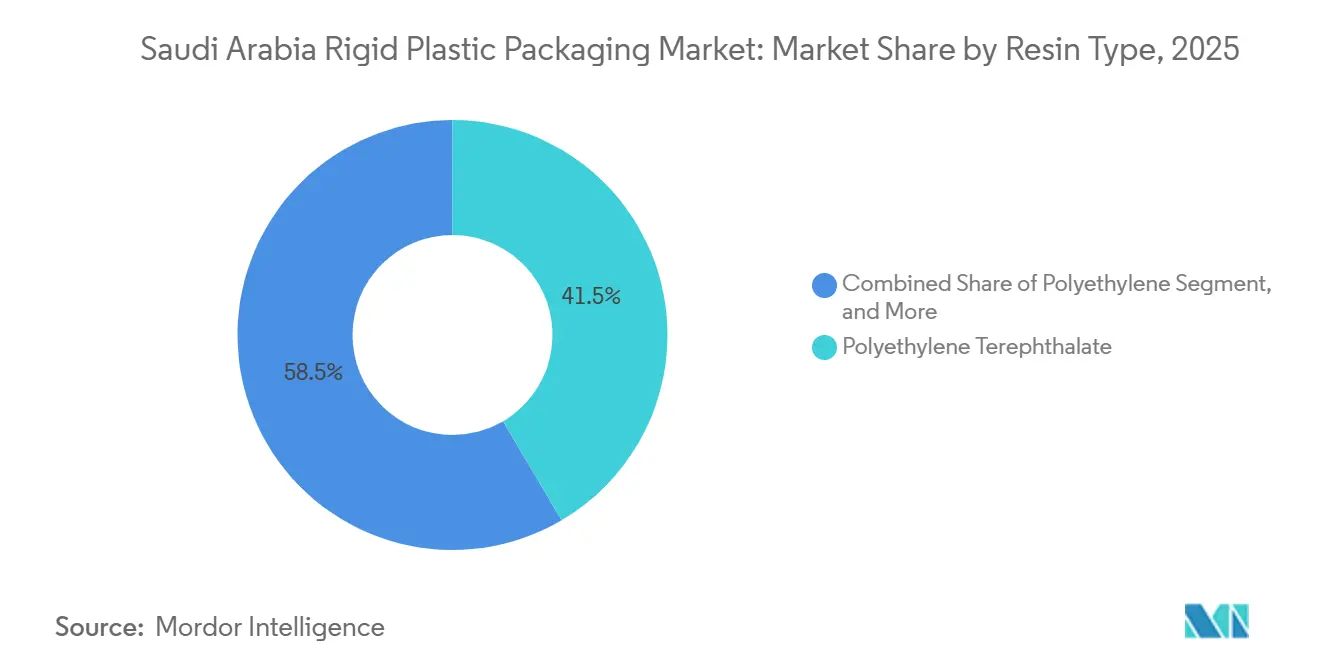

- By resin type, polyethylene terephthalate led with 41.53% of the Saudi Arabian rigid plastic packaging market share in 2025, while polypropylene is projected to post the fastest growth at 5.93% CAGR through 2031.

- By product type, bottles and jars accounted for 47.43% of the Saudi Arabia rigid plastic packaging market in 2025; caps and closures are forecast to expand at a 6.07% CAGR between 2026-2031.

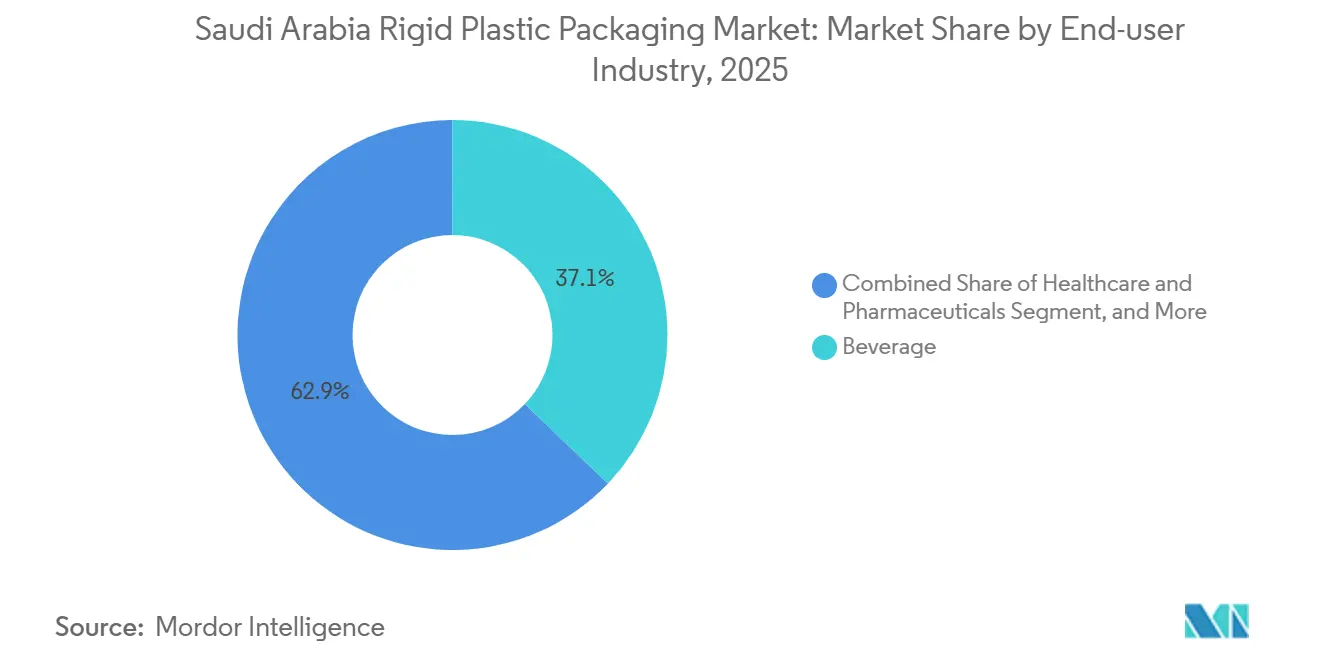

- By end user, beverages accounted for 37.13% of volume in 2025, whereas healthcare is advancing at a 6.26% CAGR through 2031.

- By manufacturing process, injection molding held 41.62% volume share in 2025, but blow molding is projected to grow at 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saudi Vision 2030 Investment in Downstream Plastics Manufacturing | +1.8% | Jubail, Yanbu, Ras Al-Khair | Long Term (≥ 4 Years) |

| Surge in Bottled Water Consumption Amid Desert Climate | +1.2% | Eastern Province, Riyadh | Short Term (≤ 2 Years) |

| Mandate for Pharma Track-and-Trace Serialized Rigid Packs | +0.9% | Nationwide | Medium Term (2–4 Years) |

| Rapid Expansion of Food-Service and Quick-Commerce Channels | +0.7% | Riyadh, Jeddah, Dammam | Medium Term (2–4 Years) |

| Carbon Border Tax Preparedness Driving Local Sourcing | +0.5% | Export-Oriented Hubs | Long Term (≥ 4 Years) |

| In-Kingdom Total Delivered Cost Policy Favoring Domestic Converters | +0.6% | Nationwide | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Saudi Vision 2030 Investment in Downstream Plastics Manufacturing

Saudi Industrial Development Fund disbursements of SAR 12 billion (USD 3.2 billion) in 2025 streamlined brownfield upgrades and greenfield plants, shrinking equipment lead times to under 12 months.[1]Saudi Industrial Development Fund, “Financing Programs for Industrial Projects,” SIDF.GOV.SA Advanced Polyolefins’ 800 kt polypropylene unit and upcoming Amiral ethylene complex guarantee local converters resin at netback pricing, anchoring the Saudi Arabia rigid plastic packaging market to a cost-leadership position. Mandatory 70% local-content thresholds push multinationals to set up onshore capacities or risk vendor-list exclusion, elevating domestic employment and technology transfer. Compliance with ISO 9001 and IKTVA certification has become table stakes; converters that fail to demonstrate 70% local content by 2026 face exclusion from Aramco's vendor list, which channels roughly 40% of Saudi Arabia's industrial procurement spend.

Surge in Bottled Water Consumption Amid Desert Climate

Saudi per capita bottled water intake reached 274 liters in 2024, double the global average. Heat waves above 45 °C and Hajj pilgrim influx create seasonal peaks that raise polyethylene terephthalate demand for single-serve and 5-gallon formats. Oxo-biodegradable additive rules add USD 0.02-0.03 per bottle, nudging converters to integrate additive-dosing systems while exploring mechanical-recycling partnerships. A proposed SAR 0.10-per-liter surcharge on megaplants aims to bankroll aquifer recharge but squeezes the three largest bottlers, who command 60% of shelf space. The Ministry of Environment, Water and Agriculture is piloting a water-scarcity surcharge of SAR 0.10 (USD 0.027) per liter on high-volume production lines that exceed 500 million bottles annually, a levy designed to fund aquifer-recharge projects but one that disproportionately affects the three largest bottlers, Nestlé Waters, Hana, and Al Ain, who together command 60% of retail shelf space.

Mandate for Pharma Track-and-Trace Serialized Rigid Packs

The GS1 DataMatrix requirement, effective January 2026, compelled pharmaceutical converters to spend SAR 800 million on laser etching and inspection modules.[2]Saudi Food and Drug Authority, “Pharmaceutical Track and Trace System Guidelines,” SFDA.GOV.SA Rigid containers now carry unique codes linking to national databases, blocking non-compliant imports and funneling share to domestic ISO 15378-certified molders. Real-time visibility cuts hospital stockouts by up to 15%, creating pull-through demand for serialization-ready caps and closures in the Saudi Arabia rigid plastic packaging market. Track-and-trace adoption also enables real-time inventory visibility, reducing hospital stockouts by an estimated 12-15% and cutting distributor working capital by 8-10 days, according to a 2025 McKinsey study on Middle Eastern pharmaceutical supply chains.

Rapid Expansion of Food-Service and Quick-Commerce Channels

Jahez and Hungerstation extended cloud-kitchen footprints to over 200 locations, each requiring tamper-evident polypropylene trays that endure microwave reheating. Quick-commerce grocers promise 15-minute windows, so single-serve rigid packs replaced bulk pouches, adding 35 kt in 2025 volume. Municipal recycling captures only 9% of rigid plastics, heightening regulator threat of deposit-return schemes that could pivot demand toward reusable designs anchored in high-density polyethylene. However, municipal waste-collection systems in Riyadh and Jeddah remain fragmented; only 9% of rigid plastics entered mechanical-recycling streams in 2025, compared to a 40% target for 2040, raising the risk that regulators will impose deposit-return schemes or outright bans on non-recyclable formats MEWA.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Crude-Derived Resin Pricing Cycles | -0.8% | Nationwide | Short Term (≤ 2 Years) |

| Stringent Single-Use-Plastic Regulations and Oxo-Biodegradable Logos | -0.6% | Nationwide | Medium Term (2–4 Years) |

| Water-Scarcity Surcharge on High-Volume Bottle Lines | -0.3% | Eastern Province, Qassim | Medium Term (2–4 Years) |

| Shift Toward Glass and Metal Premium Formats in Gifting | -0.4% | Riyadh, Jeddah, Khobar | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Derived Resin Pricing Cycles

Spot polyethylene fell 12% between January and October 2025 alongside Brent gyrations, trimming converter spreads by up to 250 basis points.[3]AlJazira Capital, “Saudi Petrochemicals Monthly Report - Oct 2025,” ALJAZIRACAPITAL.COM Smaller processors reliant on spot trades absorb month-to-month price shocks that complicate fixed tenders. China’s first-quarter 2026 release of 200 kt of strategic polyethylene reserves further suppressed Far-East benchmarks, intensifying import pressure on Saudi producers. Polypropylene spreads over propane feedstock compressed to USD 355-370 per tonne in late 2025, down from USD 450 per tonne in early 2024, eroding gross margins for injection molders by 200-250 basis points. Converters with long-term offtake agreements from SABIC or Tasnee enjoy 60-90 day price stability, but smaller players purchasing spot cargoes face monthly volatility that complicates fixed-price contracts with brand owners.

Stringent Single-Use-Plastic Regulations and Oxo-Biodegradable Logos

The mandatory additive logo forces dual inventory for domestic and export sales as the European Chemicals Agency classifies Oxo-agents as microplastic precursors.[4]European Chemicals Agency, “Microplastics Restriction Proposal,” ECHA.EUROPA.EU Draft extended-producer-responsibility levies of SAR 0.15-0.25 per kg raise landed costs, favoring scale players able to bankroll collection schemes and accelerating merger talk among mid-tier converters. Compliance timelines remain uncertain, but industry associations anticipate phased implementation starting in 2027, giving converters roughly 18 months to establish reverse-logistics partnerships with waste-management operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polypropylene Advances Through Heat-Resistant Lightweighting

Polyethylene terephthalate retained 41.53% of resin volume in 2025, yet polypropylene’s ability to withstand hot-fill above 85 °C positions it to grow at a 5.93% CAGR. Advanced Polyolefins’ new 800 kt line supplies melt-flows optimized for thin-wall injection, letting converters shave 10-12% in weight while preserving top-load integrity. Polyethylene variants cover detergents and lube oils, tracking construction upticks. Rigid applications of polystyrene face municipal bans, redirecting roughly 9 kt toward polypropylene shells. Chemical-recycling pilots under SABIC’s TRUCIRCLE broaden the sources of certified circular feedstock, signaling a future in which the Saudi Arabian rigid plastic packaging market balances the economics of virgin and recycled resins.

Post-consumer polyethylene terephthalate collection lingered at 9% in 2025; SIRC’s 2030 roadmap targets 10-fold expansion in washing capacity. The resulting cascade of recycled pellets will feed bottle-to-bottle loops once food-grade approvals are in place. Polyvinyl chloride and polycarbonate remain niche, but substitution pressure favors streamlining around polyolefins to hit recycling quotas at lower complexity.

By Product Type: Caps and Closures Gain Momentum on Serialization Needs

Bottles and jars accounted for 47.43% of output in 2025; caps and closures are outpacing at a 6.07% CAGR, as each serialized pack now demands a matched, coded closure. Induction-seal liners and under-2.5 g closure weights sharpen design requirements, pushing converters to multi-cavity hot-runner molds with tighter tolerances. Tray demand climbs with ready-meal expansion, while intermediate bulk containers ride chemical and food-ingredient growth tied to Vision 2030 megaprojects.

Aseptic blow-molding lines costing over USD 5 million favor incumbents such as Obeikan, allowing them to secure multi-year contracts with juice and dairy brands. Clamshells and blisters remain but face rising competition from molded fiber, so converters bundle rigid-flexible portfolios post-Napco’s 2025 acquisition to defend volume in the Saudi Arabia rigid plastic packaging market.

By End-User Industry: Healthcare Surges as Compliance and Demographics Align

The beverage segment captured 37.13% of the Saudi Arabia rigid plastic packaging market share in 2025, led by bottled water, carbonated drinks, and long-life juices that depend on high-clarity polyethylene terephthalate bottles and polypropylene caps. Brand owners downsized multipacks into single-serve formats for quick-commerce baskets, lifting demand for tamper-evident lids and lightweight trays. Food manufacturers followed a similar path, adopting modified-atmosphere polypropylene containers that stretch shelf life by three days, an edge that limits waste in the Kingdom’s long desert logistics chain. Cosmetics and personal-care brands switched from glass to polypropylene jars, trimming freight costs by 25% and reducing breakage claims, while industrial chemicals continued to rely on high-density polyethylene drums and intermediate bulk containers tied to construction activity.

Healthcare and pharmaceuticals are forecast to post the fastest 6.26% CAGR through 2031, elevating their share of the Saudi Arabia rigid plastic packaging market size as serialization rules lock in domestic supply. Every prescription pack now carries a GS1 code, so converters install laser-etch modules on bottles, closures, and blister backers, creating a pull-through effect for high-precision injection molding. Aging demographics double the over-60 population to 3.6 million by 2035, expanding chronic-disease medication volumes that favor child-resistant polypropylene closures.

By Manufacturing Process: Automation Lifts Output and Margins

Injection molding commanded 41.62% of total manufacturing volume in 2025, supplying caps, closures, and thick-wall jars that require tight dimensional tolerances. Servo-driven presses trimmed cycle times by 18% and cut scrap rates below 2%, conserving resin during periods of volatile feedstock costs. Real-time cavity-pressure sensors now detect wall-thickness variances within 0.05 millimeters, letting converters shave gram weights without risking burst failures. Thermoforming retained a foothold in bakery and produce trays, while compression and extrusion served niche pails and profile-based containers where rigidity outweighs weight concerns.

Blow molding is projected to grow at a 6.11% CAGR between 2026-2031, outpacing all other processes as bottled-water producers drop preform weights from 23 grams to 18 grams without sacrificing top-load strength. Two-stage stretch-blow units equipped with robotic preform loaders boost overall equipment effectiveness toward 90%, aligning output with peak summer demand spikes. Converters add in-line bottle inspection and leak-testing systems that isolate defects in under two seconds, preserving brand reputation and minimizing downstream recalls.

Geography Analysis

Eastern Province, Riyadh, and Makkah collectively house about 70% of capacity, leveraging Jubail’s ethane crackers to price resin 10-15% below parity. Riyadh’s 7.6 million residents drive year-round beverage and pharma demand, while Jeddah sees pilgrimage-induced surges. Yanbu’s upcoming Amiral complex positions the Red Sea corridor to target East African export lanes once 1.65 million tpa ethylene streams on in 2027.

Northern Border and Southern regions depend on trucked-in packs, raising landed expenses by up to 8%. The Ministry of Industry’s 50% capital grants aim to seed converters in Tabuk and Jazan, yet power reliability and distance from feedstock limit uptake. Duty-free Gulf exports absorb 15-20% of Saudi output, but the United Arab Emirates’ cheaper electricity lures new builds from global majors, pressuring domestic players to differentiate on low-carbon resin.

The EU Carbon Border Adjustment Mechanism, effective in 2026, adds EUR 53-85 per tonne on plastics entering Europe. Export-oriented processors, therefore, rush to adopt renewable certificates and recycle content to cut embedded emissions. SIRC’s plan for 12 material-recovery facilities will support regional feedstock loops, adding resilience against virgin-resin price shocks and securing supply for the Saudi Arabia rigid plastic packaging market.

Competitive Landscape

Converter concentration is moderate; the five leaders hold roughly 45-50% of the 2025 volume. Obeikan’s January 2026 term sheet with Northern Graphite for a USD 200 million anode plant signals hedging beyond packaging and anticipates localization of the electric-vehicle supply chain. Napco’s August 2025 takeover of Arabian Flexible Packaging forms an integrated rigid-flexible platform, enabling one-stop bids for quick-commerce clients.

Technology adoption is pivotal: servo injection presses, stretch-blow robots, and real-time thickness sensors cut scrap to below 2% and raise overall equipment effectiveness toward 90%. SABIC’s ISCC-certified TRUCIRCLE resins allow brand owners to claim recycled content without segregating molecules. Mid-sized converters face capital hurdles in complying with emerging extended producer responsibility levies, accelerating consolidation or strategic alliances to shield margins in the Saudi Arabia rigid plastic packaging market.

Large players pursue geographic and product diversification. Zamil’s automation push targets 10% gains in material yield, whereas Takween’s 2024 recapitalization unlocked funding for pharma-grade expansion. Contract molding specialists bypass traditional converters by offering toll services, saving brand owners up to 10% via direct resin procurement, a model gaining traction amid resin-price volatility.

Saudi Arabia Rigid Plastic Packaging Industry Leaders

Obeikan Investment Group

Takween Advanced Industries Company

Arabian Plastic Industrial Company Ltd.

Plastic Products Company (3P)

Saudi Plastic Factory Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Obeikan Investment Group signed a USD 200 million joint venture term sheet for a battery anode with Northern Graphite.

- December 2025: Riyadh Municipality issued a draft rule proposing a ban on expanded-polystyrene takeaway containers, prompting food-service converters to test polypropylene and molded-fiber replacements.

- November 2025: The Ministry of Environment, Water and Agriculture released a consultation paper on extended-producer-responsibility for rigid plastics, outlining levies of SAR 0.15-0.25 per kilogram and a phased rollout starting 2027.

- September 2025: Zamil Plastic Industries announced a USD 45 million automation program for servo-driven injection and blow-molding lines, targeting a 25% labor-cost reduction by 2027.

Saudi Arabia Rigid Plastic Packaging Market Report Scope

The Saudi Arabia Rigid Plastic Packaging Market Report is Segmented by Resin Type (Polyethylene [HDPE, LDPE, LLDPE], PET, Polypropylene, Polystyrene and EPS, Other Resins), Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, IBCs, Drums, Other Products), End-User Industry (Food [Candy, Dairy, Meat, Rest], Beverage, Healthcare, Cosmetics, Industrial Chemicals, Building, Other End Users), and Manufacturing Process (Injection, Blow, Thermoforming, Compression, Extrusion, Other Processes). Market Forecasts are Provided in Terms of Volume (Tonnes).

By Resin Type

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polyethylene Terephthalate (PET) | |

| Polypropylene | |

| Polystyrene and Expanded Polystyrene (EPS) | |

| Other Resin Types |

By Product Type

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Other Product Types |

By End-User Industry

| Food | Candy and Confectionery |

| Dairy and Frozen | |

| Meat, Poultry and Seafood | |

| Rest of Food Types | |

| Beverage | |

| Healthcare and Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Industrial Chemicals | |

| Building and Construction | |

| Other End-user Industries |

By Manufacturing Process

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Compression Molding |

| Extrusion |

| Other Manufacturing Process |

| By Resin Type | Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polyethylene Terephthalate (PET) | ||

| Polypropylene | ||

| Polystyrene and Expanded Polystyrene (EPS) | ||

| Other Resin Types | ||

| By Product Type | Bottles and Jars | |

| Trays and Containers | ||

| Caps and Closures | ||

| Intermediate Bulk Containers (IBCs) | ||

| Drums | ||

| Other Product Types | ||

| By End-User Industry | Food | Candy and Confectionery |

| Dairy and Frozen | ||

| Meat, Poultry and Seafood | ||

| Rest of Food Types | ||

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Industrial Chemicals | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Manufacturing Process | Injection Molding | |

| Blow Molding | ||

| Thermoforming | ||

| Compression Molding | ||

| Extrusion | ||

| Other Manufacturing Process | ||

Key Questions Answered in the Report

How fast is demand for polypropylene packs growing in Saudi rigid plastics?

Polypropylene volumes are forecast to increase at 5.93% CAGR through 2031, powered by dairy, juice, and lightweight yogurt cups.

Which region houses most of the Kingdom’s rigid plastic converting capacity?

Eastern Province, along with Riyadh and Makkah, accounts for about 70% of installed capacity thanks to proximity to Jubail feedstock and major demand centers.

What is driving the surge in caps and closures volumes?

Pharmaceutical serialization rules now require unique codes on both bottles and their closures, lifting caps and closures demand at 6.07% CAGR to 2031.

How are converters mitigating resin price volatility?

Leading players lock long-term offtake contracts with SABIC, invest in chemical recycling feedstocks, and hedge using renewable-energy certificates to lower embedded emissions subject to carbon levies.

What sustainability regulations are on the horizon?

Draft extended-producer-responsibility rules may levy SAR 0.15-0.25 per kg on rigid plastics from 2027, while oxo-biodegradable logos remain mandatory for bottles under 25 g.

How concentrated is the competitive landscape?

The top five players hold 45-50% share, yielding a moderate concentration that still leaves room for niche and regional specialists.

Page last updated on: