Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.27 Billion |

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Glass Packaging Market Analysis by Mordor Intelligence

Saudi Arabia glass packaging market size in 2026 is estimated at USD 1.35 billion, growing from 2025 value of USD 1.27 billion with 2031 projections showing USD 1.83 billion, growing at 6.28% CAGR over 2026-2031. This expansion is anchored in Vision 2030 policies that promote domestic manufacturing, premiumization of consumer goods, and stricter sustainability standards that favor infinitely recyclable materials over single-use plastics. Localization incentives are steering beverage, pharmaceutical, and personal-care producers toward homegrown supply chains, while younger consumers in Riyadh, Jeddah, and Dammam demonstrate a clear willingness to pay more for glass containers that connote quality and eco-friendliness. At the same time, large biologics and vaccine investments, such as EVA Pharma’s Sudair complex, are catalyzing demand for ISO-compliant vials and ampules that must be sourced quickly and reliably within the Kingdom. Moderate competitive intensity and vertical integration moves by domestic players are compressing raw material risk; however, rising industrial energy tariffs and PET substitution remain the principal cost and margin challenges for glass converters.

Key Report Takeaways

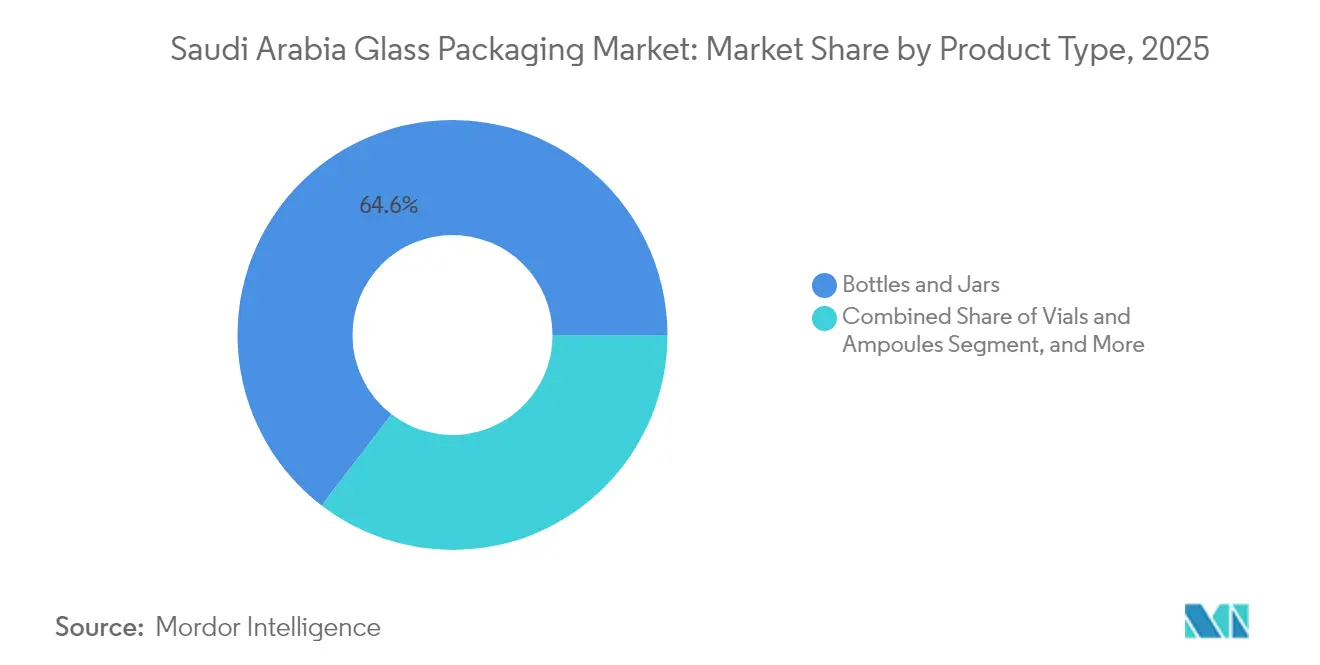

- By product type, bottles and jars led with 64.58% of the Saudi Arabia glass packaging market share in 2025, while vials and ampoules are forecast to expand at a 7.21% CAGR through 2031.

- By end-use industry, beverages commanded a 47.92% revenue share in 2025; pharmaceuticals represented the fastest-growing category at an 8.22% CAGR from 2025 to 2031.

- By color, flint glass retained 44.95% share in 2025, whereas green glass is set to post the strongest growth at 8.05% CAGR.

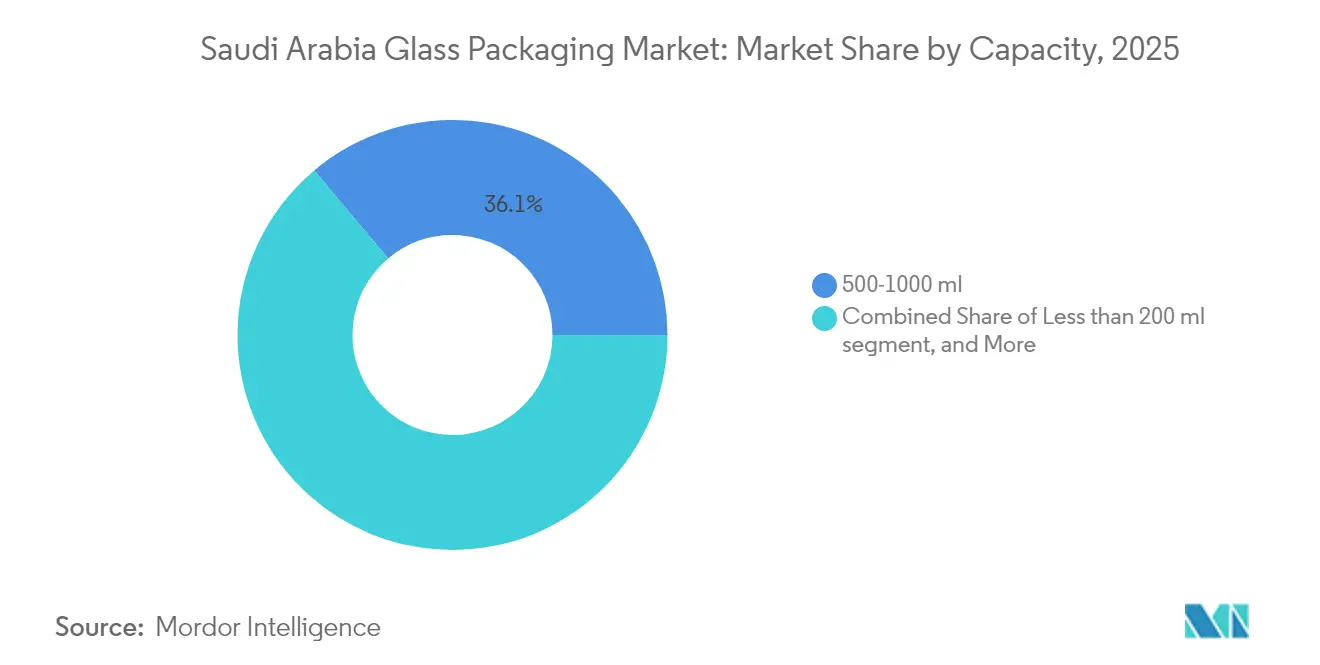

- By capacity, 500-1000 ml formats captured 36.12% of sales in 2025 and are projected to grow at 7.31% CAGR, outpacing smaller and larger alternatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income and Premiumization of Food and Beverage Products | +1.2% | National, concentrated in Riyadh, Jeddah, Dammam metropolitan areas | Medium term (2-4 years) |

| Expansion of Saudi Pharmaceutical Manufacturing Under Vision 2030 | +1.8% | National, with major hubs in Sudair, King Abdullah Economic City, Jubail | Long term (≥ 4 years) |

| Increasing Consumer Preference for Sustainable and Recyclable Packaging | +0.9% | National, early adoption in urban centers | Medium term (2-4 years) |

| Surge in Boutique Perfume and Niche Attar Brands Seeking Prestige Packaging | +0.6% | National, strongest in Western Province and Riyadh | Short term (≤ 2 years) |

| Government Mandate for Domestic Beverage Bottling Glass Content Localisation | +1.1% | National, enforced via Local Content and Government Procurement Authority | Medium term (2-4 years) |

| Rapid Growth of Medical Tourist Injectable Drug Demand Fueling Small-Volume Vial Use | +0.7% | National, concentrated in Riyadh, Jeddah medical cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of Saudi Pharmaceutical Manufacturing Under Vision 2030

EVA Pharma’s USD 265 million Sudair facility, launched in late 2025, brings an annual output of 990 million biologic and vaccine units that must be filled in ISO 8362-compliant glass containers. Domestic converter Zoujaj responded by adding a sixth line capable of 25,000 tons per year and earmarked SAR 58.5 million for a furnace upgrade that will increase total daily capacity by 2027. As government policy targets 40% local drug production by 2030, the momentum for import substitution is firmly in favor of pharmaceutical-grade vials and ampules. German specialists Gerresheimer and SCHOTT currently supply premium borosilicate formats, but local plants are fast-tracking ISO 15378 certification to capture share. The long-term demand visibility, coupled with large volume contracts, ensures stable furnace utilization and justifies investment in clean-room forming, annealing, and automated inspection systems.

Rising Disposable Income And Premiumization Of Food And Beverage Products

The average household spends on branded beverages is trending upward as Middle East consumers trade up from commodity options to locally positioned, healthier, and formulated drinks, such as Kinza and Milaf Cola, both presented in branded glass bottles that reinforce freshness and authenticity. The food and beverage sector is forecast to reach USD 27.83 billion by 2029, providing sustained volume for premium packaging. Glass offers the transparency and tactile heft that resonates with millennials seeking modern yet culturally rooted products. Higher disposable income also supports indulgence-oriented packaging, such as embossed jars for gourmet condiments, which further deepens the order book for mid-size flint containers. Premiumization thus acts as a volume and value driver, lifting average revenue per ton for domestic converters.

Increasing Consumer Preference For Sustainable And Recyclable Packaging

The Material Waste Management National Waste Management Company set an ambitious 79% recycling target by 2035, sharply above the 5% baseline in 2024. The Public Investment Fund-backed SIRC is rolling out cullet processing hubs that will enhance the availability of recycled content, reducing furnace energy use by up to 25% when cullet ratios exceed 50%. [1]Saudi Investment Recycling Company, “Cullet Processing Expansion,” SIRC, sirc.sa Urban consumers are increasingly associating glass with health, safety, and a low environmental impact, a perception strengthened by SABER certification, which verifies durability and the absence of harmful substances. While glass’s higher weight still inflates logistics costs, its infinitely recyclable nature positions it as the long-term winner once collection systems mature. Brand owners are consequently piloting “return-and-reward” programs that encourage bottle reuse and reinforce the material’s circular credentials.

Government Mandate For Domestic Beverage Bottling Glass Content Localisation

The Local Content and Government Procurement Authority grants a 10% price preference to beverages bottled in domestically produced glass, tilting sourcing decisions toward Riyadh-based operations run by Zoujaj and Obeikan Glass. [2]Local Content and Government Procurement Authority, “Price Preference Policies,” LCGPA, lcgpa.gov.sa Obeikan’s silica sand mining license, obtained in March 2025, further localizes the value chain and insulates producers from global raw-material volatility. [3]Saudi Gazette Bureau, “Obeikan Glass Secures Silica Sand Mining License,” Saudi Gazette, saudigazette.com.sa Beverage majors such as Almarai blend domestic glass with PET to hedge costs; however, the regulatory premium keeps a sizable share of high-volume carbonated soft drink contracts within the country. Medium-term, this mandate should safeguard furnace capacity utilization and support incremental capex for energy-efficient oxy-fuel systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Cost and Carbon Footprint of Glass Furnaces | -0.8% | National, acute in industrial cities | Short term (≤ 2 years) |

| Intensifying Competition from Lightweight PET and Flexible Packaging | -1.1% | National, strongest in beverage and food segments | Medium term (2-4 years) |

| Shortage of Recycled Glass Cullet Reducing Furnace Efficiency | -0.5% | National, infrastructure gaps in collection and sorting | Long term (≥ 4 years) |

| Limited Cold-Chain Infrastructure Increasing Breakage in Long-Distance Distribution | -0.4% | National, most severe in remote regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Cost And Carbon Footprint Of Glass Furnaces

Continuous melting furnaces consume 4-6 GJ per tonne at temperatures above 1,500 °C, meaning energy can represent 25-30% of finished container cost even at subsidized tariffs of 18 halalas per kWh and SAR 5.84-7.23 per MMBtu. Capital-intensive upgrades, such as hybrid oxy-fuel firing or full electrification, promise a 30-40% emissions cut but require outlays exceeding SAR 100 million per line. In comparison, PET blow molding requires barely 0.5 GJ per ton, allowing converters to undercut glass on price in mass-market beverage categories. Unless energy subsidies persist or carbon-offset mechanisms emerge, furnace operators will feel margin pressure and may defer capacity expansions beyond 2027.

Intensifying Competition From Lightweight PET And Flexible Packaging

Alesayi Beverage’s multi-format lines switch among glass, PET, and cans in a single shift, while RAFA Water has integrated PET preform and cap production to capture supply-chain margin. PET’s 80% weight advantage lowers freight costs and suits e-commerce distribution channels that struggle with glass’s fragility. High-speed PET lines at Almarai achieve a throughput of 54,000 bottles per hour (bph) for 200 ml juices, surpassing the throughput of comparable glass fillers. As retailers prioritize portability and convenience, brand owners divert incremental SKUs to PET and pouches, reducing the addressable volume for glass, particularly in entry-level carbonated drinks and bottled water.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pharmaceutical Vials Drive Fastest Growth

In 2025, bottles and jars accounted for 64.58% of the volume, reflecting their entrenched role in beverages and pantry staples. However, vials and ampules are expected to accelerate at a 7.21% CAGR through 2031, thereby elevating the Saudi Arabia glass packaging market size for injectable formats and signaling a strategic pivot toward healthcare applications. The segment’s value density is significant; unit prices for borosilicate vials exceed those for flint beverage bottles by a factor of three, resulting in a disproportionate revenue contribution. Local converter Zoujaj’s June 2025 25,000 t/y line was built specifically for ISO 8362 vials, demonstrating capital alignment with pharmaceutical localization goals.

Demand is reinforced by SCHOTT Pharma’s 22% global growth in RTU solutions and the September 2024 Alliance for RTU, which together shape buyer expectations around pre-sterilized, siliconized containers. Domestic players must meet ISO 15378 and SFDA validation to enter this supply pool. Early adoption successes would expand the Saudi Arabia glass packaging market share in the high-margin drug-delivery niche, buffering converters against beverage cyclicality and PET encroachment.

By Color: Green Glass Gains Traction In Premium Segments

Flint retained 44.95% of shipments in 2025 thanks to its compatibility with automated inspection and consumer preference for full product visibility. Yet, green containers are forecast to grow at an 8.05% CAGR and carve out a rising share of the Saudi Arabia glass packaging market. Boutique perfume houses and organic food brands deploy colored bottles to signal authenticity, UV protection, and sustainability narratives that resonate with affluent shoppers. Asgharali’s decorative green series exemplifies the potential for margin uplift when design storytelling is integrated with local cultural cues.

Amber tones remain essential for light-sensitive pharmaceuticals, although advanced coatings on flint glass now offer comparable protection, suggesting possible erosion of their market share. Custom blues and specialty tints service artisanal spirit variants and limited-edition cosmetics, where buyers accept longer lead times and higher minimum order pricing. Overall, color strategy is evolving into a branding toolkit rather than a purely functional choice, nudging converters toward flexible furnace scheduling and small-batch capability.

By Capacity: Mid-Size Formats Dominate Across Applications

Containers in the 500-1000 ml range garnered 36.12% of 2025 shipments and are advancing at 7.31% CAGR, keeping this band central to the Saudi Arabia glass packaging market. The size strikes a practical balance between single-household consumption and production-line efficiency, making it attractive for carbonated soft drinks and mid-dose pharmaceutical injectables alike. Brand owners appreciate the shelf presence and perceived value that mid-size glass provides, especially when compared to lightweight PET, which can appear commoditized.

Formats below 200 ml thrive in vials, ampoules, and luxury cosmetics, yet their aggregated tonnage is relatively modest. Above 1 L, PET dominates bottled water and family-size soft drinks for logistical reasons, limiting glass to premium niche SKUs. Consequently, glass makers treat 500-1000 ml as the defensive core: by optimizing mold inventory, closure compatibility, and label alignment, they can reduce changeover waste and maintain competitive fill-line speeds.

By End-Use Industry: Pharmaceuticals Outpace Beverage Growth

Beverages still supplied 47.92% of container demand in 2025, but the segment’s unit growth is moderating as PET and aluminum capture entry-price tiers. By contrast, pharmaceuticals are growing at an 8.22% CAGR, giving them the highest trajectory within the Saudi Arabia glass packaging market size for end-use applications. Vision 2030’s target for 40% local medicine production has already catalyzed major biologic and vaccine projects, each requiring stringent container-closure integrity that only Type I and Type II borosilicate can deliver.

Gourmet food, condiments, and spreads continue to favor glass for premium positioning, yet face volume dilution from flexible pouches in foodservice channels. Cosmetics and personal care remain a margin-rich domain, fueled by attar and oud brands that treat bottle shape and engraving as the essence of brand storytelling. Laboratory glassware and specialty items round out the portfolio, contributing small but stable amounts.

Geography Analysis

Riyadh anchors both demand and supply: Zoujaj and Obeikan Glass run their flagship furnaces in the capital, and the city’s pharmaceutical corridor consumes a growing share of vials destined for biologics and injectables. The presence of regulatory bodies and logistics infrastructure yields shorter lead times and easier SFDA inspections, concentrating high-value orders in central Saudi Arabia. Eastern Province hubs, such as Dammam and Jubail, offer a raw-material advantage by tapping nearby silica sand and soda ash sources, while leveraging King Abdulaziz Port for export to the wider Gulf.

Jeddah and the Western Province account for a disproportionate share of premium perfume, cosmetics, and gourmet beverage packaging. High tourist traffic and strong disposable income create a receptive base for decorative and colored glass, resulting in differentiated SKUs that emphasize craftsmanship. The regional channel also facilitates Red Sea exports to Egypt, Sudan, and the broader Horn of Africa. Conversely, northern and southern frontier provinces remain under-penetrated due to fragile logistics and limited chilled distribution networks, conditions that push retailers toward lighter PET and flexible alternatives.

As domestic content rules tighten, cross-border procurement is tilting inward: the 10% price preference mechanism encourages GCC bottlers to source from Riyadh furnaces rather than import blanks from Europe or Asia. This dynamic boosts furnace utilization and supports the justification for Obeikan’s silica sand mining project, which aims to cover 40% of annual feedstock needs by 2027. Overland routes to Bahrain, Kuwait, and the UAE fill backhaul lanes, optimizing truckload economics and improving regional competitiveness for Saudi producers.

Regulatory Landscape

Saudi Arabia regulates packaging through the Saudi Standards, Metrology and Quality Organization (SASO) technical regulations and conformity assessment. For regulated goods, market access is commonly routed through the SABER platform, covering product certification via SASO-notified certification bodies. Packaging environmental and safety compliance is reinforced through standards referenced in technical regulations, including packaging-and-environment requirements aligned with ISO 18602, which affects material selection, labeling readiness, and documentation for glass containers placed on the Saudi market.

For higher-risk end uses, the Saudi Food and Drug Authority (SFDA) sets tighter controls for medicinal and food-contact packaging. These include requirements that packaging materials, such as Type I glass for certain drug products, are specified in product registration files and validated in line with SFDA guidance and GCC-aligned expectations. For pharmaceutical vials and ampoules, this raises compliance stakes for converters, pushing them toward auditable quality systems, documented traceability, and fitness-for-use testing aligned with applicable SFDA and GCC guidance.

Value Chain Analysis

The Saudi Arabia glass packaging value chain starts with raw materials (silica sand, soda ash, limestone, colorants) and energy inputs into continuous-melt furnaces. It then moves through forming operations (IS machines), annealing, surface treatment, and automated inspection, followed by secondary steps such as decoration, labeling, and palletization. Domestic manufacturing is anchored by Saudi Arabian Glass Company Ltd (SAGCO), The National Company for Glass Industries (Zoujaj), and Mahmood Saeed Glass Industry Company (MSGLASSCO), with publicly stated capacities and footprints indicating scale across multiple furnaces and production lines that support both beverage bottles and jars and higher-spec formats.

Downstream, glass containers flow either through direct supply agreements to beverage, food, and pharmaceutical fillers or via packaging distributors, with logistics and breakage control influencing delivered cost across the Kingdom. Localization is an active lever in the chain: in May 2025, the National Industrial Development Center signed an MoU with Sidel to explore local services and manufacturing programs for food and beverage packaging, supporting faster line support, spares availability, and performance upgrades for filling operations that depend on consistent container quality.

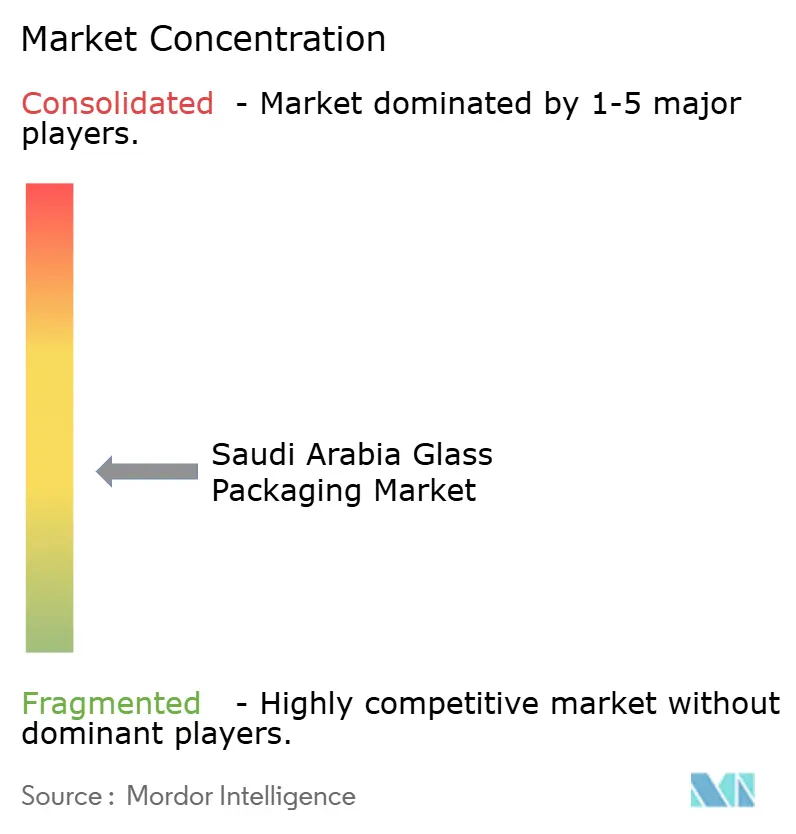

Competitive Landscape

The Saudi Arabia glass packaging industry features moderate concentration. Zoujaj and Obeikan Glass together control roughly 60-65% of the container capacity, focusing on beverage and food jars while increasing investment in pharmaceutical-grade lines. Zoujaj’s SAR 806 million float glass project and exploratory merger talks with Saudi Arabian Glass Company illustrate a drive to integrate upstream and broaden product range. Obeikan’s March 2025 silica sand license and February 2025 collaboration with Italy’s Isoclima similarly target raw material security and process technology upgrades.

European specialists Gerresheimer, SCHOTT, and Ardagh maintain a stronghold on borosilicate and ready-to-use (RTU) vials, shipping finished goods through the ports of Jeddah and Dammam, or partnering with regional distributors. Their September 2024 Alliance for RTU sets performance benchmarks that domestic players must meet to capture biotech and vaccine accounts. Meanwhile, PET bottlers such as Alesayi Beverage and RAFA Water have vertically integrated preform molding, eroding glass share in high-volume soft drinks.

Technology adoption delineates winners and laggards. Major furnaces are introducing Industry 4.0 sensors for real-time defect detection and predictive maintenance, whereas smaller regional converters lack the capital to modernize, leading to higher scrap rates. Energy cost exposure is another differentiator: the largest operators are piloting oxy-fuel burners and waste-heat recovery, cutting natural-gas demand by up to 20% and positioning themselves ahead of future carbon pricing scenarios.

Saudi Arabia Glass Packaging Industry Leaders

-

Saudi Arabian Glass Company Ltd.

-

Ardagh Group S.A.

-

Gerresheimer AG

-

Schott AG

-

SGD Pharma S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Pharmaceutical-grade glass remains a key whitespace where local conversion capacity, certification, and validated quality systems shape share capture as Saudi drug manufacturing scales under Vision 2030. EVA Pharma's Sudair complex (launched in late 2025) and the associated need for ISO-compliant primary containers create opportunities for local suppliers that can meet SFDA validation expectations, reduce time-to-supply, and provide documented container-closure integrity performance. This supports investment in clean-room capable handling, automated inspection, and ISO 15378-aligned systems for vials and ampoules, along with long-term supply arrangements with domestic drug manufacturers.

Circularity and supply security also point to opportunity linked to regulation, cost, and sustainability. The National Waste Management Company set a 79% recycling target by 2035 (from a 5% baseline in 2024), and SIRC is rolling out cullet processing hubs that increase recycled glass availability and can lower furnace energy use as cullet ratios rise. Alongside this, localization initiatives that influence sourcing decisions, including the Local Content and Government Procurement Authority price-preference mechanism for domestically produced glass in beverages, support multi-year capacity utilization and justify furnace efficiency upgrades and upstream raw-material integration steps by domestic producers.

Recent Industry Developments

- April 2026: Ardagh Group discussed business updates during its Q1 2026 earnings call, highlighting capacity utilization across its glass packaging operations and signaling ongoing supply-chain resilience for customers in the Middle East. The commentary gives downstream buyers a view of global production momentum and affects planning for Saudi import needs and multinational supplier interactions.

- December 2025: Zoujaj began commercial production on its sixth glass container line, adding 25,000 t/y dedicated to pharmaceutical vials and premium beverage bottles. The new line strengthens domestic availability for higher-spec containers and supports localization programs that reward in-Kingdom sourcing for regulated and premium end uses.

- December 2024: Zoujaj approved a SAR 58.5 million furnace expansion to lift daily output from 210 t to 280 t by Q1 2027. The project signals continued capacity and efficiency investment, helping stabilize supply for large beverage and food accounts while creating headroom to pursue more specialized container formats.

Research Methodology Framework and Report Scope

Segmentation Overview

-

By Product Type

- Bottles and Jars

- Vials and Ampoules

- Others Product Types

-

By Color

- Flint

- Amber

- Green

- Other Colors

-

By Capacity

- Less than 200 ml

- 200-500 ml

- 500-1000 ml

- More than 1000 ml

-

By End-Use Industry

- Food

-

Beverage

-

Alcoholic Beverage

- Beer

- Wine

- Spirits

- Other Alcoholic Beverages (Cider and Other Fermented Drinks)

-

Non-Alcoholic Beverage

- Carbonated Soft Drinks

- Juices

- Dairy Product Based Drinks

- Other Non-Alcoholic Beverages

-

Alcoholic Beverage

- Pharmaceuticals

- Cosmetics and Personal Care

- Other End-Use Indusry

Key Questions Answered in the Report

How large is the Saudi Arabia glass packaging market in 2026?

The market stands at USD 1.35 billion in 2026 and is forecast to reach USD 1.83 billion by 2031.

Which end-use segment is growing the fastest?

Pharmaceuticals are expanding at an 8.22% CAGR as new biologic and vaccine plants come online.

What is the main restraint facing local glass converters?

High furnace energy costs and competition from lightweight PET are the most significant challenges.

Why are green glass containers gaining popularity?

Premium perfume and organic food brands use green glass to signal authenticity and provide UV protection.

Which capacity range dominates sales?

The 500-1000 ml segment captured 36.12% of 2025 shipments and continues to post the highest growth.

Who are the leading domestic producers?

Zoujaj and Obeikan Glass collectively supply around two-thirds of container volume, benefiting from vertical integration.

Page last updated on: