Middle East Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

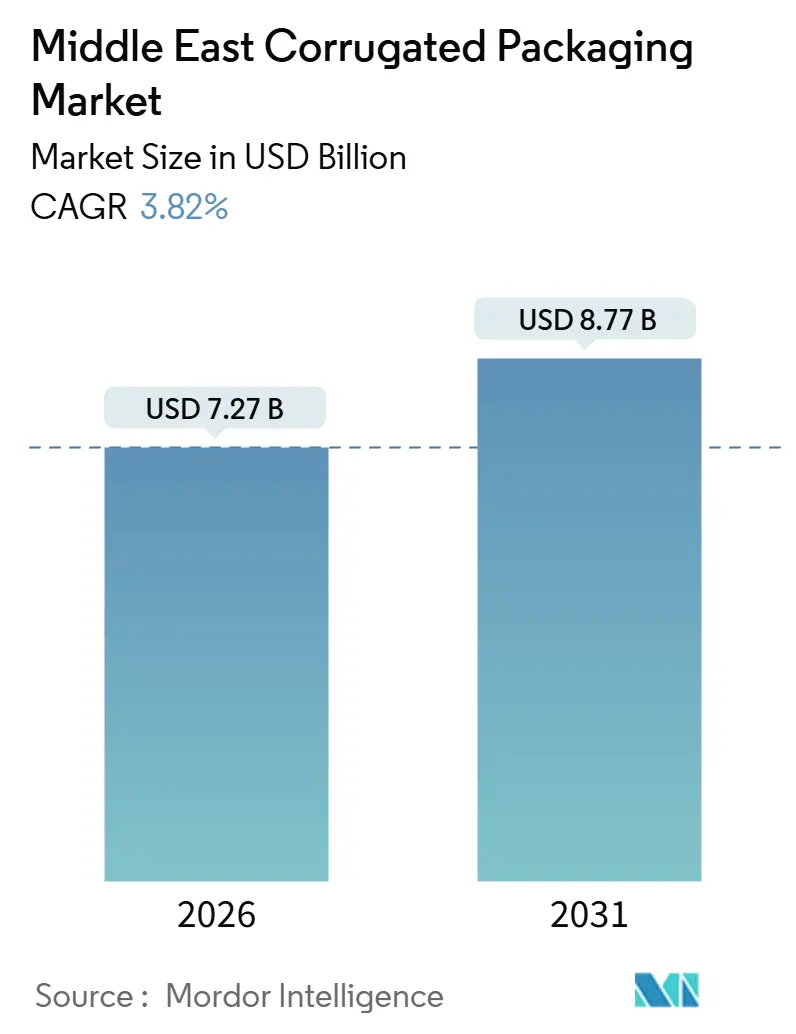

| Market Size (2026) | USD 7.27 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

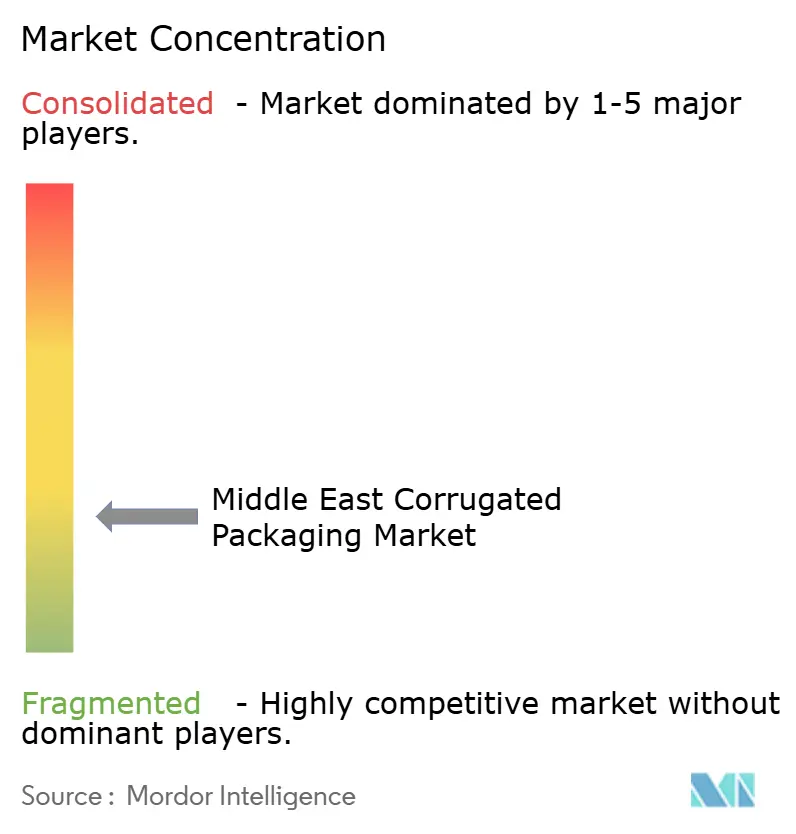

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Corrugated Packaging Market Analysis by Mordor Intelligence

The Middle East corrugated packaging market size stands at USD 7.27 billion in 2026 and is projected to reach USD 8.77 billion by 2031, expanding at a 3.82% CAGR, according to Mordor Intelligence data. Rising e-commerce penetration, government-backed industrial diversification, and investments in regional cold-chain infrastructure continue to reshape demand, moving the market beyond its traditional food and beverage core. Online retailers demand lightweight, digitally printed boxes that can be produced in variable runs, while manufacturers in Saudi Arabia and the United Arab Emirates (UAE) are specifying heavy-duty, triple-wall formats for export shipments. Micro-flute profiles that save shelf space and improve graphics are gaining share in premium consumer goods, and converters investing in hybrid digital-flexographic presses are securing short-run orders at premium margins. Currency shifts and pulp volatility have raised operating risk, yet backward-integrated mills enjoy cost protection and are building capacity in lightweight liner grades to serve the next wave of e-commerce growth.

Key Report Takeaways

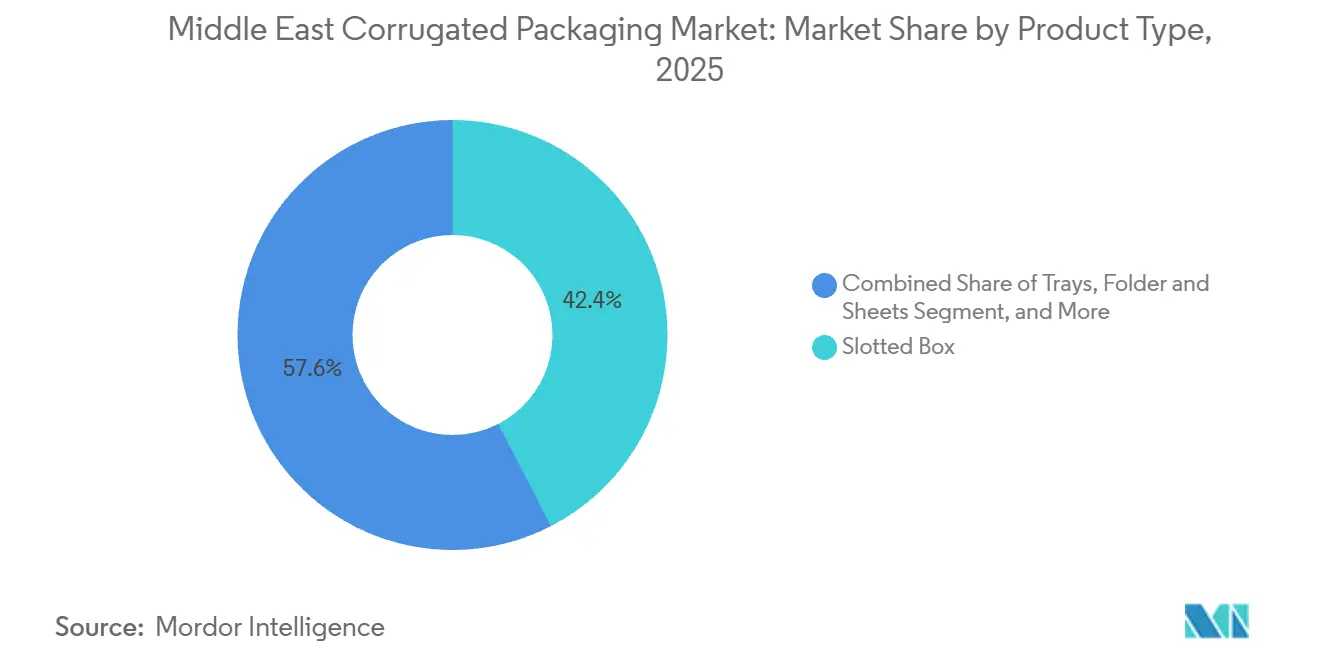

- By product type, slotted boxes led with 42.43% of the Middle East corrugated packaging market share in 2025, while trays and folders recorded the highest projected CAGR at 5.66% through 2031.

- By board type, single-wall held 38.32% of the Middle East corrugated packaging market share in 2025 and triple-wall is forecast to expand at 4.32% CAGR to 2031.

- By flute profile, C-flute captured 32.54% share of the Middle East corrugated packaging market size in 2025 and F-flute is advancing at a 4.65% CAGR through 2031.

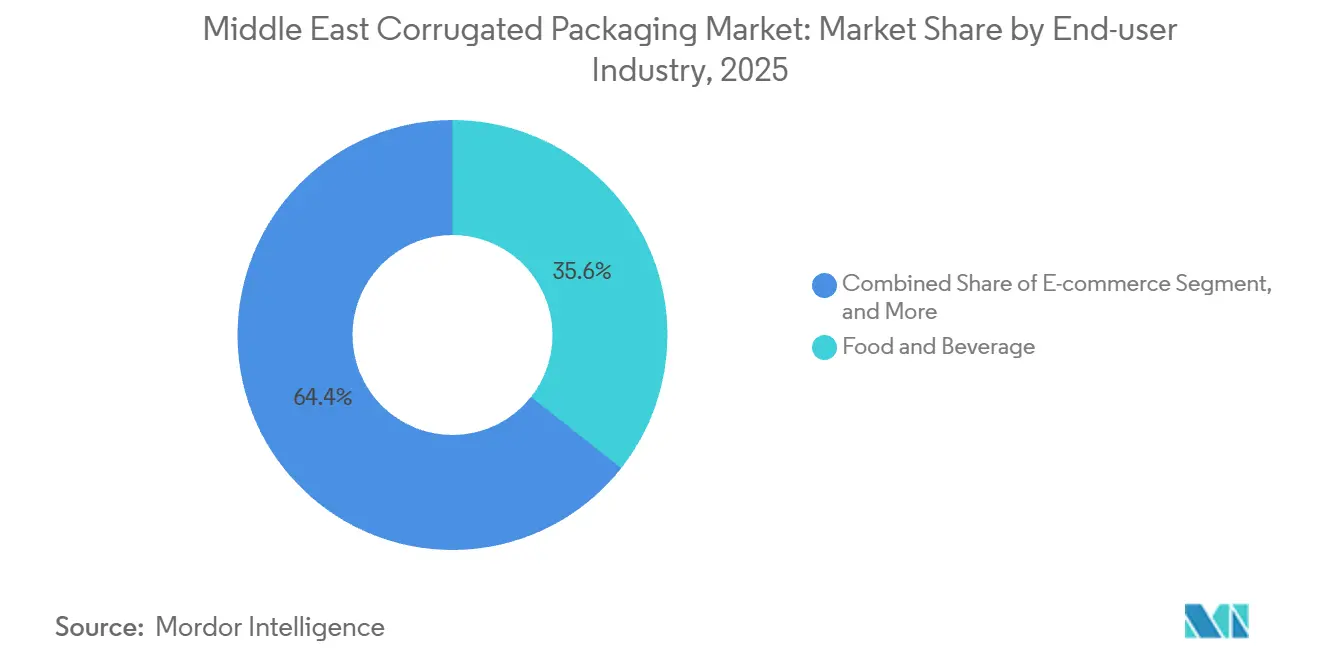

- By end user, food and beverage commanded 35.63% share in 2025, whereas e-commerce posts the fastest 4.73% CAGR through 2031.

- By print technology, flexography accounted for 28.54% of the Middle East corrugated packaging market share in 2025 and digital printing shows a 4.54% CAGR outlook to 2031.

- By geography, Saudi Arabia dominated with 32.34% share in 2025 and Jordan is the fastest growing country at 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom accelerating corrugated demand | +1.2% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Food delivery growth in GCC nations | +0.8% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Government-led industrial diversification projects | +0.9% | Saudi Arabia, UAE, Jordan | Long term (≥ 4 years) |

| Shift toward lightweight high-strength boards | +0.5% | Regional, strongest in UAE and Saudi Arabia | Medium term (2-4 years) |

| Digital printing adoption for short-run packaging | +0.4% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Temperature-controlled date export packaging | +0.3% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Accelerating Corrugated Demand

Gulf Cooperation Council (GCC) online sales reached USD 50 billion in 2025, up 30% year-over-year, and every additional parcel shipped translates into at least one corrugated unit consumed. Brand owners demand custom graphics, return-ready tear strips, and pack-to-fit algorithms that reduce freight costs, pushing converters toward digital presses capable of printing lots as small as 500 units. Saudi Arabia’s National Industrial Development and Logistics Program earmarked USD 427 billion for delivery hubs and automated sortation centers, each standardized around dimensional-weight optimized box footprints.[1]Saudi Vision 2030 Secretariat, “National Industrial Development and Logistics Program,” VISION2030.GOV.SA Local converters that still rely on long-run flexographic lines risk losing share to agile plants that offer 48-hour turnaround and variable-data printing. Cross-border sellers from China and India have already set the benchmark for lightweight, high-graphic packaging, raising regional customer expectations.

Food Delivery Growth in GCC Nations

The GCC food-delivery channel is projected to generate USD 30 billion by 2028, with Saudi Arabia and the UAE accounting for 70% of orders and driving corrugated demand toward moisture-resistant single-wall boxes.[2]Morgan Stanley Analysts, “GCC Food-Delivery Outlook,” MORGANSTANLEY.COM Cloud kitchens and dark stores, which numbered over 1,200 in the region by end-2025, insist on packaging that maintains temperature for at least 45 minutes while surviving condensation. Converters coat boards with polyethylene or wax emulsions, raising material cost 8-12% but enabling restaurant chains to charge premium delivery fees. Subscription meal-kit providers use vented trays that extend the shelf life of fresh produce by up to 3 days, thereby reducing food waste. So far, GCC regulators have issued few binding rules on food-delivery packaging, leaving performance standards to competitive differentiation rather than compliance.

Government-Led Industrial Diversification Projects

Saudi Arabia’s Public Investment Fund invests USD 40 billion per year in industrial cities such as Jazan and Ras Al-Khair, attracting export-oriented factories that will consume an extra 1.2 million tons of corrugated annually by 2031. The UAE’s Operation 300bn strives to lift industrial gross domestic product (GDP) to AED 300 billion (USD 81.7 billion) by 2031, which requires clean-room-compatible corrugated dunnage for aerospace parts and medical devices. Jordan’s free-trade zones extend duty-free access to U.S. and European markets, inviting multinational brands to source competitively priced boxes that meet ISO 9001 and ISO 14001 standards. Over time, the region moves from import-dependent retail consumption toward export-oriented manufacturing, rewarding converters that certify quality systems and offer heavyweight triple-wall formats.

Shift Toward Lightweight High-Strength Boards

Hybrid fiber formulations, including nano-cellulose coatings, enable a 15-20% basis-weight reduction while holding edge-crush values above 32 pounds per square foot, cutting both material and freight cost. International Paper and WestRock license these formulations to regional mills, and Saudi plants are adding refining lines that make lightweight liner grades locally, displacing imports that carry 5-7% tariffs. For e-commerce shippers, lighter boxes avoid higher dimensional-weight charges and lower Scope 3 carbon emissions by up to 18% for every ton-mile transported. Retailers increasingly choose suppliers able to document such carbon savings, giving technical innovators a clear margin edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft paper price volatility | -0.6% | Regional, strongest impact in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Water scarcity impact on paper mills | -0.4% | Saudi Arabia, UAE, Jordan | Long term (≥ 4 years) |

| Import tariffs on recovered paper | -0.3% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Rise of reusable plastic crates in produce sector | -0.2% | UAE, Oman, Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Kraft Paper Price Volatility

Northern Bleached Softwood Kraft (NBSK) pulp prices fell from USD 1,400 per ton in 2022 to USD 800-900 in 2024, yet containerboard prices slipped only 15-20%, compressing converter margins by up to 300 basis points. The Middle East imports 60% of its kraft liner, leaving converters exposed to freight surcharges during Red Sea disruptions and dollar strength cycles. Domestic mills tie prices to global benchmarks, so tariffs give limited shelter. Backward-integrated players, such as Obeikan Industrial Investment Group, enjoy a 150-200 basis-point cushion, and they continue to invest in capacity while smaller firms defer automation.

Water Scarcity Impact on Paper Mills

Paper production requires 15-20 gallons of water per pound of output, a challenge in Saudi Arabia, where non-renewable aquifers are declining by 2-3% per year.[3]World Bank MENA Division, “Water Scarcity in the Middle East,” WORLDBANK.ORG Desalinated water costs USD 1.50-2.00 per cubic meter, adding USD 30-40 to the cost of every ton of containerboard made in coastal mills. The UAE recovers up to 90% of process water through closed-loop systems, but at upfront costs of USD 5-8 million per mill, beyond the reach of many family-owned converters. Jordan’s per-capita renewable-water availability slipped below 100 cubic meters in 2024, ensuring that future containerboard capacity will cluster near seawater-fed locations, while inland converters will rely on imported parent rolls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Trays and Folders Gain Share in Retail-Ready Formats

Slotted boxes maintained 42.43% of 2025 revenue, anchoring shipments in bulk logistics and general merchandise. Trays, folders, and sheets, however, show a 5.66% CAGR through 2031, propelled by club-store merchandising and direct-to-consumer (DTC) models that prefer open-top or self-display formats. The Middle East corrugated packaging market benefits when supermarket operators demand shelf-ready designs that avoid secondary handling, reducing labor cost up to 30%. Digital print capability allows rapid artwork changes for seasonal promotions, and converters report margin uplifts of 15% on specialty trays versus commodity regular slotted containers. Telescope and multi-piece boxes occupy heavy-duty niches, such as industrial machinery, where two-piece designs reduce corner-crush failures. Corrugated pallets and die-cut shapes serve pharmaceuticals and electronics, delivering high protective performance in compact footprints.

Trays and folders also align with cold-chain expansion, carrying vented produce that reaches retail coolers faster, cutting spoilage by 2-3 days. Meal-kit providers prefer folded mailers that fit standard courier lockers, a format boosted by food-delivery growth. As a result, the Middle East corrugated packaging market size allocated to trays and folders will rise steadily. Converters that master quick-change die-cutting and high-resolution graphics look set to capture this incremental volume, especially in the UAE, where e-grocery shipments already exceed 1 million orders per week.

By Board Type: Triple-Wall Demand Rises with Industrial Exports

Single-wall accounted for 38.32% share in 2025, dominating e-commerce, fast food, and light industrial uses where unit cost drives specification. Double-wall satisfies mid-weight appliances and consumer electronics, offering improved stacking without high material expense. Triple-wall grows 4.32% CAGR through 2031 on the back of Saudi and UAE heavy machinery exports, which require crush resistances above 1,000 pounds. Industrial estates such as King Salman Energy Park ship gas turbines in triple-wall cartons fitted with polyethylene vapor barriers, preventing corrosion during sea voyages.

Regional converters expand heavy-duty corrugator lines capable of laminating three mediums in a single pass, cutting production time by 30-40%. Triple-wall producers that certify ISO 9001 quality systems command price premiums, because multinational buyers stipulate global standards. Over time, the Middle East corrugated packaging market share for triple-wall aligns closely with capital-goods export growth. Although raw material costs are higher, unit economics are protected by specialized design fees and value-added cushioning inserts.

By Flute Profile: F-Flute Advances in Premium Consumer Goods

C-flute held 32.54% share in 2025 owing to its general-purpose balance of cushioning and stacking strength. E-flute continued to gain in cosmetics and ready-to-display snacks, offering lithographic print quality and 10-15% volume savings. F-flute, at only 0.03 inch flute height, leads growth at 4.65% CAGR, locked into premium chocolates, perfumes, and smartphones sold in the UAE luxury retail channel. Its fine profile bridges the gap between folding carton appearance and corrugated durability, a key selling point in brand-conscious segments.

Converters adopting F-flute must invest in precision rotary scoring and laser die-cutting to avoid flute-tip crush, adding USD 200,000-300,000 to each line. Despite the capex, payback generally occurs within 24 months, given the 20-25% margin uplift that micro-flute formats fetch. The Middle East corrugated packaging market size in F-flute remains small relative to mainstream C- and B-flute, yet its faster growth signals a structural shift toward premiumization, especially in channels influenced by tourism and duty-free retail.

By End-User Industry: E-Commerce Outpaces Traditional Segments

Food and beverage dominated with 35.63% of revenue in 2025, spanning fresh produce, dairy, and processed foods that ship daily across the region. E-commerce, however, posts a 4.73% CAGR outlook and represents the single largest incremental opportunity, because every online order needs a branded shipper that also serves as a return package. Saudi pharmaceutical production is targeted to reach USD 8 billion by 2030, requiring tamper-evident boxes, while personal-care brands demand grease-proof liners and high-graphic lids to support in-store visibility.

Industrial manufacturers exporting auto parts and construction modules specify double- and triple-wall boxes with reinforced corners. Electronics assemblers insist on anti-static coatings and custom foam inserts, creating niche value pools. As online retail and localized manufacturing advance in parallel, converters able to toggle between short-run customized jobs and regular commodity orders will outperform the market. Consequently, the Middle East corrugated packaging market benefits from a diversified demand base that mitigates cyclical risk in any single sector.

By Print Technology: Digital Gains Ground in Short-Run Applications

Flexography retained 28.54% share in 2025 due to its high speed and low cost per thousand at run lengths above 10,000 units. Lithography remains the gold standard for photographic graphics but incurs a 20-30% cost premium because sheets must be laminated to board. Digital printing, growing 4.54% CAGR, eliminates plates and enables same-shift artwork changes, a capability prized by e-commerce merchants and small and medium enterprises (SMEs) marketing limited-edition products. The UAE alone processed 1.2 million e-commerce parcels per day in 2025, each of which was a candidate for personalized messaging.

Converters installing HP Indigo, EFI Nozomi, or Durst platforms secure orders that flexo operators decline, boosting average selling prices by 15-20%. Hybrid workflows that gang digital and flexo on the same line maximize asset utilization and keep per-unit cost competitive. Ultimately, the Middle East corrugated packaging market will reflect a dual-print landscape, flexo for bulk, digital for agility. Plants that master both technologies are best positioned to meet volatile customer lead-time needs.

Geography Analysis

Saudi Arabia led the Middle East corrugated packaging market with 32.34% share in 2025, lifted by USD 1 trillion in Public Investment Fund allocations across manufacturing zones, logistics corridors, and export-oriented industries. Containerboard capacity reached 1.2 million tons, and domestic mills are shifting to lightweight liner grades that align with parcel-delivery growth. Date exporters shipped 133,000 tons in 2024, generating box demand for moisture-barrier cartons fitted with ventilation features, extending shelf life by up to 15 days during voyages to Europe and Asia.

The UAE functions as the region’s cold-chain and digital-commerce hub, leveraging Jebel Ali port and free-zone incentives to re-export boxes to Africa and South Asia. Operation 300bn aims to lift industrial GDP to AED 300 billion (USD 81.7 billion) by 2031, growing demand for clean-room-compatible corrugated dunnage. Dubai processed 450 million parcels in 2025, and leading online platforms prefer digital print formats with batch sizes under 5,000. Abu Dhabi’s Khalifa Industrial Zone is attracting food processors that insist on halal-certified packaging, driving converters toward traceability software investments.

Jordan, while smaller, is the fastest-growing market at 5.01% CAGR through 2031, benefiting from free-trade agreements that permit duty-free exports to the United States and the European Union. Food processors require grease-resistant cartons for olive oil and confectionery, and the kingdom’s pharmaceutical sector demands child-resistant structures. The Rest of Middle East bloc, covering Oman, Bahrain, Kuwait, and Iraq, registers steady volume as each government pivots from oil reliance toward localized food processing and light manufacturing, creating incremental box demand that favors converters willing to establish satellite plants.

Competitive Landscape

The Middle East corrugated packaging market remains fragmented, with more than 20 regional converters and no firm exceeding 10% share. Obeikan Industrial Investment Group and Saudi Paper Manufacturing Company benefit from backward-integrated pulp capacity, preserving margins when kraft prices swing. They also extend 30-45-day payment terms, a hurdle for smaller operators. Yet niche converters armed with digital presses capture high-margin, short-run orders in the e-commerce and premium food sectors, where branded unboxing and 48-hour lead times command price premiums.

Technology adoption marks the competitive fault line. Plants adding automated die-cutters and real-time tracking systems secure pharmaceutical and electronics contracts that mandate lot-level traceability. International Paper’s hybrid-board licensing accelerates the shift to lightweight, high-strength grades, handing early adopters a 10-15% material-cost edge. Quality benchmarks also rise after the Gulf Standards Organization adopted ISO 12048 edge-crush testing in 2024, a move that favors mills with in-house laboratories.

White-space opportunities exist in temperature-controlled corrugated for cold-chain produce, triple-wall formats for heavy industrial exports, and micro-flute boxes for premium consumer goods. Converters that build specialized lines and secure sustainability certifications, such as ISO 14001, are poised to differentiate as multinational brands raise environmental requirements.

Middle East Corrugated Packaging Industry Leaders

Arabian Packaging Co. LLC

Queenex Corrugated Carton Factory

United Carton Industries Company (UCIC)

Napco National

Falcon Pack Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Saudi Paper Manufacturing Company announced a SAR 800 million (USD 213 million) expansion at its Dammam mill, adding 150,000-ton lightweight containerboard capacity, with commissioning set for Q3 2027.

- October 2025: Obeikan Industrial Investment Group partnered with HP Inc. to install a USD 12 million digital corrugated press in Riyadh, enabling 48-hour turnaround on 500-unit orders.

- August 2025: United Carton Industries Company JSC won a USD 25 million supply contract for triple-wall boxes to King Salman Energy Park, covering gas turbines and compressors.

- June 2025: Napco National CJSC invested AED 40 million (USD 10.9 million) in automated die-cutting at its Sharjah plant, lifting capacity 30% to 120,000 tons.

Middle East Corrugated Packaging Market Report Scope

A corrugated box is a suitable secondary or tertiary packaging solution for various end-user industries, including electrical goods, food, personal care, and cosmetics. Furthermore, the corrugated box ships goods to a retailer, where the boxes deliver vegetables or other foodstuffs. The study covers the corrugated packaging market, tracked by consumption and sales of different corrugated packaging products offered by various vendors.

The Middle East Corrugated Packaging Market Report is Segmented by Product Type (Slotted Box, Telescope/Multi-Piece Boxes, Trays, Folder and Sheets, and Other Product Types), Board Type (Single Wall, Double Wall, and Triple Wall), Flute Profile (A Flute, B Flute, C Flute, E Flute, F Flute, and Other Flute Profile), End-user Industry (Food, Beverages, Pharmaceuticals, Personal Care and Household, Industrial, Electrical and Electronics, and Other End-user Industries), Print Technology (Flexography, Digital, Lithography, and Other Print Technology), and Country (Saudi Arabia, United Arab Emirates, Qatar, Jordan, and Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| Slotted Box |

| Telescope/Multi-Piece Boxes |

| Trays, Folder and Sheets |

| Other Product Types |

| Single Wall |

| Double Wall |

| Triple Wall |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Other Flute Profiles |

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Household |

| Industrial |

| Electrical and Electronics |

| Other End-user Industries |

| Flexography |

| Digital |

| Lithography |

| Other Print Technology |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Jordan |

| Rest of Middle East |

| By Product Type | Slotted Box |

| Telescope/Multi-Piece Boxes | |

| Trays, Folder and Sheets | |

| Other Product Types | |

| By Board Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| By Flute Profile | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| Other Flute Profiles | |

| By End-user Industry | Food |

| Beverages | |

| Pharmaceuticals | |

| Personal Care and Household | |

| Industrial | |

| Electrical and Electronics | |

| Other End-user Industries | |

| By Print Technology | Flexography |

| Digital | |

| Lithography | |

| Other Print Technology | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Jordan | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East corrugated packaging market?

The market stands at USD 7.27 billion in 2026 and is forecast to reach USD 8.77 billion by 2031.

Which segment is growing fastest in regional corrugated demand?

E-commerce boxes post the highest 4.73% CAGR, overtaking traditional food and beverage applications.

Why are triple-wall boxes gaining popularity?

Heavy-machinery exports from Saudi Arabia and the UAE require crush resistance above 1,000 pounds, driving 4.32% CAGR growth in triple-wall formats.

How are converters coping with kraft paper price swings?

Backward-integrated mills offset pulp volatility, while smaller firms invest in lightweight boards and digital presses to protect margins.

Which country leads consumption, and which grows fastest?

Saudi Arabia held 32.34% market share in 2025, whereas Jordan leads growth at a 5.01% CAGR outlook.

What technology is transforming short-run packaging orders?

Digital printing enables economical runs as small as 500 units with 48-hour turnaround, capturing premium e-commerce and promotional work.

Page last updated on: