Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

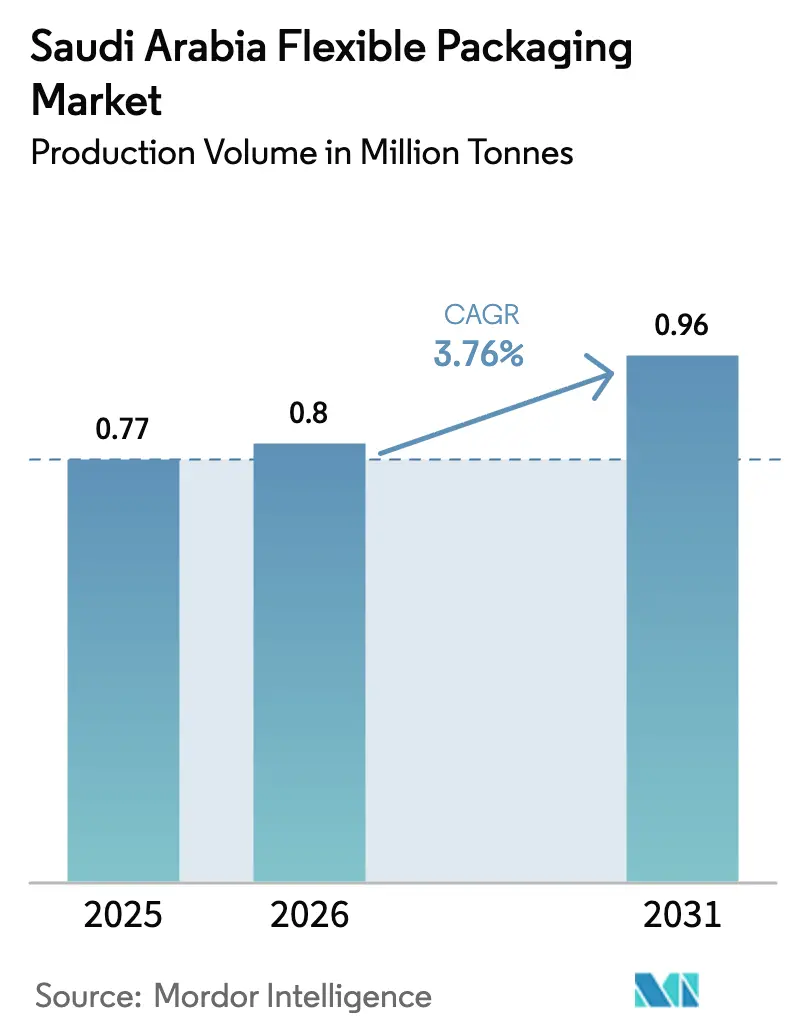

| Base Year Market Size (2025) | 0.77 Million tonnes |

| Market Volume (2026) | 0.8 Million tonnes |

| Market Volume (2031) | 0.96 Million tonnes |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

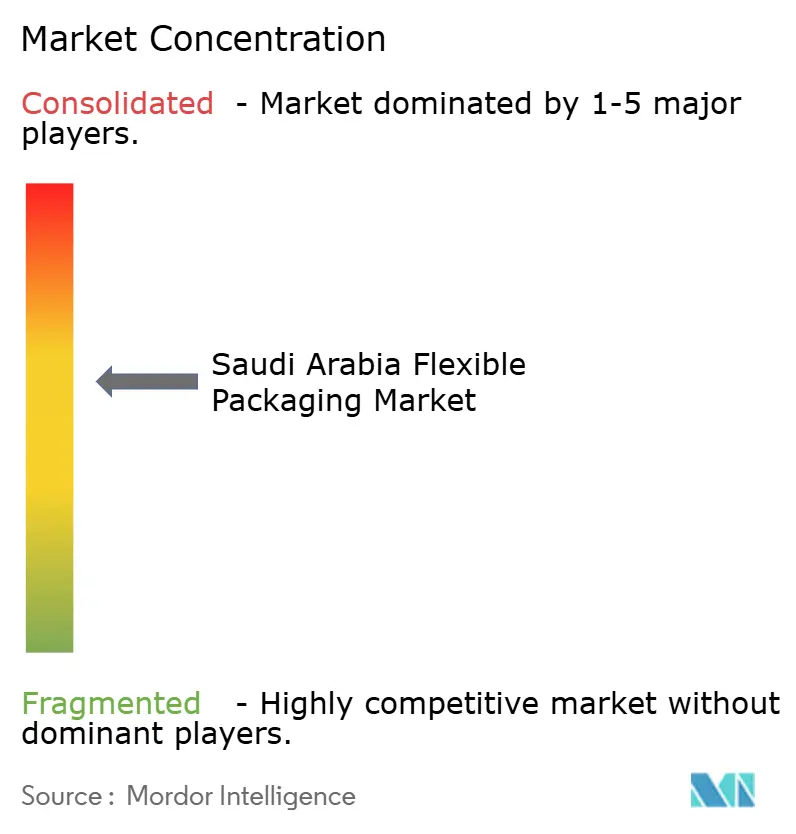

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Flexible Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia flexible packaging market size is expected to grow from 0.77 million tonnes in 2025 to 0.8 million tonnes in 2026 and is forecast to reach 0.96 million tonnes by 2031 at 3.76% CAGR over 2026-2031. Rising investments in food-processing plants, pharmaceuticals, and e-commerce logistics hubs under Vision 2030 are the primary catalysts for growth. Rapid growth in Mada card transactions, the introduction of new petrochemical feedstocks, and municipal mandates for recycled content are reshaping material choices, technology adoption, and sustainability priorities. Competitive differentiation is moving toward circular polymers, high-barrier films, and short-run digital printing as brand owners demand lighter, smarter, and greener packaging solutions. While regulatory pressure around single-use plastics and energy tariffs poses cost headwinds, long-term infrastructure commitments in waste recovery and recycling are expected to mitigate these challenges and reinforce the growth trajectory of Saudi Arabia's flexible packaging market.

Key Report Takeaways

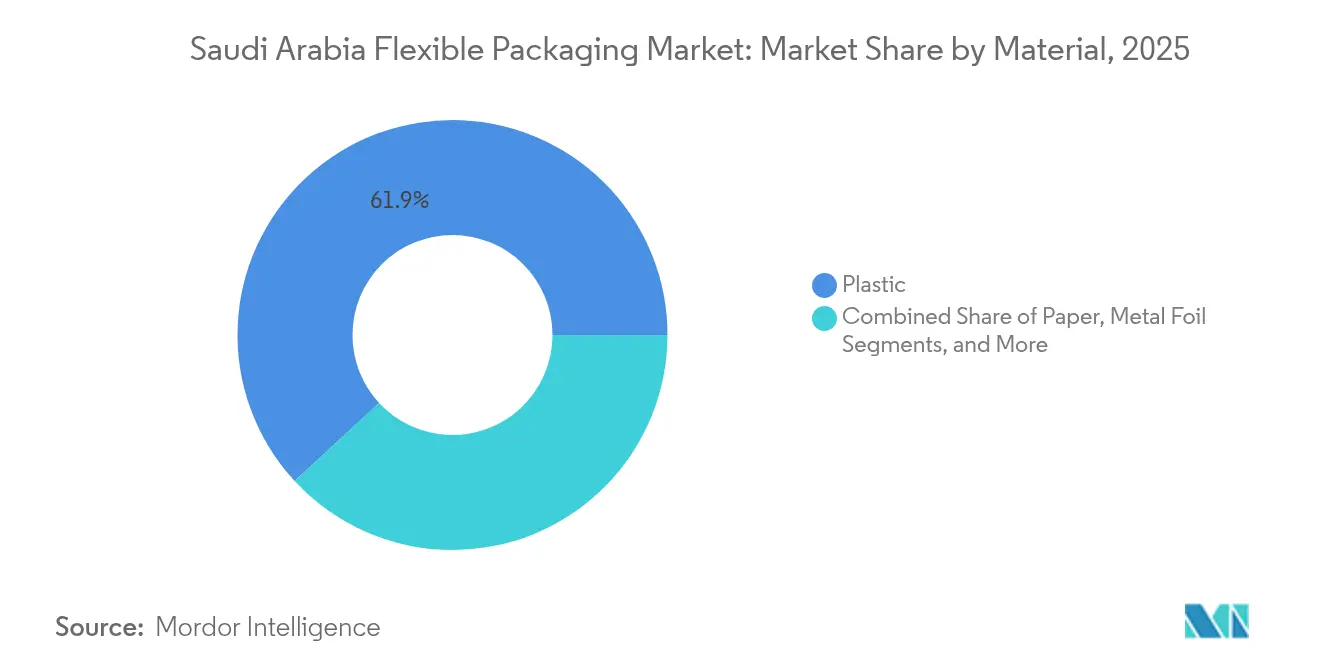

- By material, plastic led with 61.88% of the Saudi Arabia flexible packaging market share in 2025; bioplastics and compostable grades are projected to expand at a 4.95% CAGR through 2031.

- By product type, bags and pouches commanded 46.98% of the Saudi Arabia flexible packaging market size in 2025, while sachets and stick packs are forecast to grow at a 4.48% CAGR between 2026-2031.

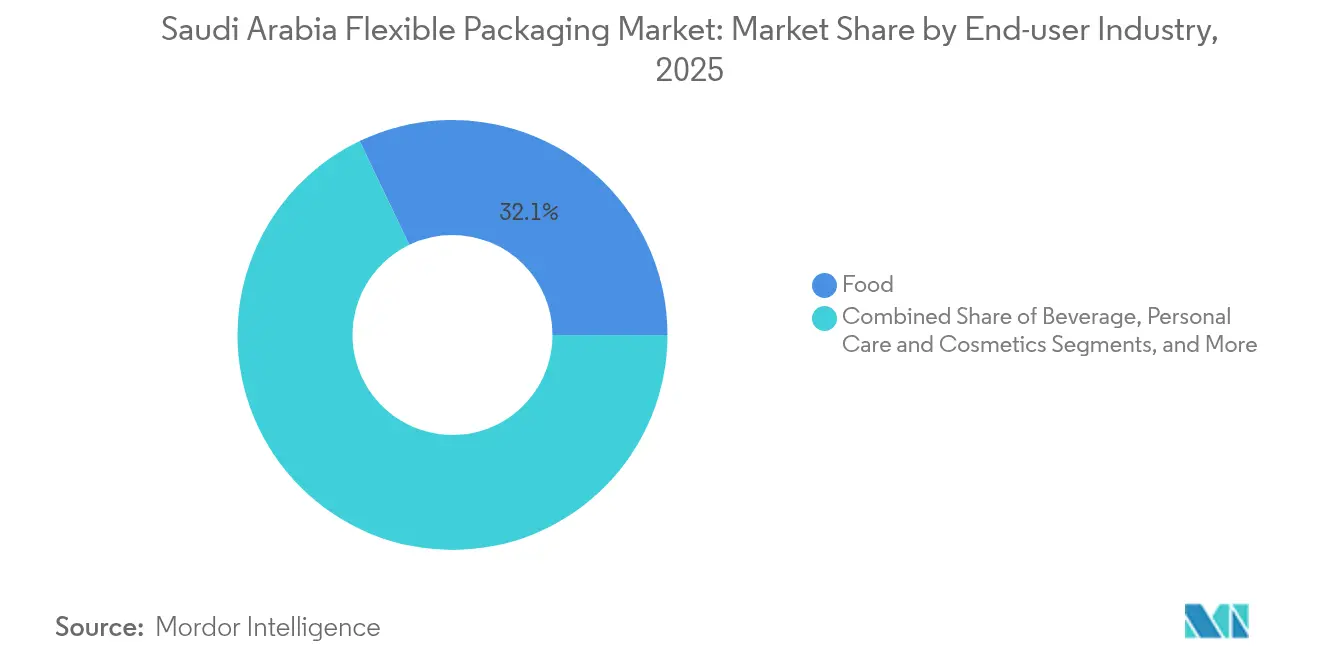

- By end-user industry, food applications accounted for 32.11% of the Saudi Arabia flexible packaging market share in 2025; the personal care and cosmetics segment is the fastest-growing, with a 4.72% CAGR through 2031.

- By printing technology, flexography held a 44.93% revenue share in 2025, whereas digital printing is expected to advance at a 4.88% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in food-processing capacity under Vision 2030 | +0.8% | National, concentrated in industrial clusters | Medium term (2-4 years) |

| Shift toward convenience foods and on-the-go formats | +0.6% | Urban centers, expanding to rural areas | Short term (≤ 2 years) |

| Expansion of local pharmaceutical manufacturing clusters | +0.5% | Riyadh, Dammam, emerging biotech zones | Long term (≥ 4 years) |

| Rapid e-commerce growth driving protective films/mailers | +0.7% | National, highest in Riyadh and Jeddah | Short term (≤ 2 years) |

| Competitive resin pricing from new petrochemical capacity | +0.5% | National, benefiting from SABIC expansions | Medium term (2-4 years) |

| Municipal recycled-content mandates in Riyadh pilot zones | +0.4% | Riyadh pilot zones, expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Food-Processing Capacity Under Vision 2030

State-backed investment is projected to reach USD 70 billion by 2030, up 59% from 2016.[1] Foreign Agricultural Service, “Saudi Arabia: Food Processing Ingredients,” usda.gov The launch of the National Grains Supply Company, with 2.7 million tonnes of storage, is expanding downstream demand for bulk liners, wicket bags, and retail pouches. Seafood output is targeted to rise to 600,000 tonnes by 2030, intensifying cold-chain packaging needs for frozen and value-added fish products. Food-grade flexible formats deliver weight savings, oxygen-barrier performance, and cost advantages over rigid alternatives, making them indispensable for processors scaling up under Vision 2030. As new plants come on-stream, contract packagers are lining up long-term supply agreements, ensuring a steady pipeline of orders for polyethylene, polypropylene, and polyamide film converters.

Shift Toward Convenience Foods and On-the-Go Formats

Urbanization and 97% smartphone penetration have mainstreamed click-and-collect meal options, elevating demand for portion-controlled sachets, stick packs, and retort pouches. Farmers’ transition to compound feed-valued at USD 3.46 billion by 2027-illustrates parallel shifts toward smaller, moisture-resistant packs for livestock nutrition.[2]Frontiers in Sustainable Food Systems, “Optimizing animal care through compound feed management in Saudi Arabia,” frontiersin.org Brand owners are investing in easy-open zippers, laser perforation, and resealable spouts to secure premium shelf space with added consumer convenience. Flexible packaging’s ability to cut food waste by offering single-serve units aligns with national food security objectives, reinforcing volume growth.

Expansion of Local Pharmaceutical Manufacturing Clusters

The Public Investment Fund’s Lifera CDMO launch and the National Biotechnology Strategy aim for 30% drug localization by 2025. Sterile barrier pouches, high-barrier lamination, and child-resistant zippers are in higher demand as insulin, vaccine, and monoclonal antibody lines scale up. The Saudi Food and Drug Authority (SFDA) rules require traceable Arabic labeling, which is accelerating the adoption of digital printing for variable data compliance. Flexible films capable of withstand 121 °C autoclave cycles are commanding premium margins as pharma buyers shift from imports to local contract packagers.

Rapid E-Commerce Growth Driving Protective Films/Mailers

Mada transactions surged 25.82% YoY to SAR 197.42 billion (USD 52.64 billion) in 2024, with government targets of 70% online retail by 2030. Lightweight mailers, bubble films, and tamper-evident pouches mitigate last-mile damage and lower volumetric shipping costs. Large e-retailers like Jarir and Amazon.sa are standardizing pack formats and driving converters to scale output. Automated sortation centers favor film grades with high slip and puncture resistance, boosting polyethylene demand from local petrochemical suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-use levies and single-use bans tightening in 2026 | -0.4% | National, pilot programs in Riyadh | Short term (≤ 2 years) |

| Weak domestic recycling infrastructure for PCR resins | -0.3% | National, acute in secondary cities | Medium term (2-4 years) |

| Rising electricity tariffs post-subsidy reforms | -0.2% | National, higher impact on energy-intensive operations | Short term (≤ 2 years) |

| Skilled-labour shortage in lamination and printing lines | -0.2% | Industrial clusters, technical job categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-Use Levies and Single-Use Bans Tightening in 2026

Municipal mandates in Riyadh require certified recycled content, echoing the UAE’s blanket ban, effective 2026. SASO’s oxo-biodegradable film rule already covers 441 factories. Corporate pledges such as Zahid Group’s single-use phase-out intensify market momentum toward bio-based or compostable substitutes. Converters face retooling costs for barrier coatings and need chain-of-custody audits under ISCC Plus, raising capex while organic waste streams for compostables remain underdeveloped.

Weak Domestic Recycling Infrastructure for PCR Resins

Saudi recycling rates sit below 15%, and 85% of waste still goes to landfill. Five city master plans cover only 60% of national waste, leaving secondary regions underserved. Multilayer film contamination complicates PET recycling, restricting PCR feedstock supply for flexible formats. SABIC’s advanced-recycling TRUCIRCLE resins offer an interim option but carry cost premiums that price-sensitive converters resist, leading to a supply-demand imbalance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Faces Sustainability Transition

Plastic held 61.88% of the Saudi Arabia flexible packaging market share in 2025. Although commodity polyolefins remain cost-competitive, bio-based resins are gaining ground at a 4.95% CAGR as policymakers introduce recycled-content rules and brand owners pledge net-zero targets. The Saudi Arabia flexible packaging market size for bioplastics is forecast to widen by 2030, supported by SABIC’s TRUCIRCLE expansion, which delivers certified circular polymers. Ethylene capacity from the USD 6.4 billion Fujian complex promises plentiful feedstock, stabilizing virgin resin prices and safeguarding converter margins.

Paper and metal foil maintain specialized niches. Recyclable kraft laminates address new produce-pack rules, while aluminum foil remains essential for oxygen-sensitive nutraceuticals. However, life-cycle analysis favors monomaterial structures, prompting lamination downgrading initiatives that open opportunities for solvent-free adhesives and inline extrusion coating.

By Product Type: Convenience Formats Drive Innovation

Bags and pouches accounted for 46.98% of the Saudi Arabia flexible packaging market size in 2025. Growth stems from stand-up pouches replacing glass jars in condiments and gusseted sacks optimizing feed storage. Sachets and stick packs are on track for a 4.48% CAGR thanks to single-serve beverage powders and instant coffee. Retailers demand see-through windows, laser-score easy-tear features, and recyclable zippers, pressing converters to adopt inline inspection and digital pre-press workflows.

Films and wraps see accelerated orders from e-commerce fulfilment centers that require downgauged yet puncture-resistant polyethylene blends. Labels and sleeves, while smaller in tonnage, command high margins through tactile varnishes and smart-label integration that tracks temperature excursions during cold-chain logistics.

By End-user Industry: Food Sector Leads While Personal Care Accelerates

Food retained 32.11% market share in 2025, buoyed by Vision 2030’s drive for self-sufficiency. Shelf-stable snacks, ready-to-eat meals, and frozen seafood drive demand for barrier films. The personal care and cosmetics segment, forecast to rise at a 4.72% CAGR, benefits from domestic production of halal-certified beauty products that require high-opacity films and metallized pouches.

Beverages leverage flexible shrink bundles around PET bottles, complementing the SAR 3.5 billion bottled-water boom. Pharma and healthcare products fetch the highest unit prices, as the SFDA mandates tamper-evident, child-resistant seals and serialized pack-level codes, all of which favor digitally printed laminates that comply with Good Manufacturing Practices.

By Printing Technology: Digital Innovation Transforms Traditional Flexography

Flexography maintained a 44.93% revenue share in 2025 , but digital presses are projected to outpace overall market growth at a 4.88% CAGR. Inkjet systems enable batch-level Arabic labeling and rapid artwork changes without the need for plates, making them suitable for personalized beauty and nutraceutical brands. Hybrid flexo-digital lines are emerging in Dammam as converters retrofit existing assets to handle variable data.

Rotogravure remains a popular choice in premium snack and confectionery wraps, where high-resolution metallic inks justify the costs of cylinder printing. Meanwhile, AI-driven color-management software and closed-loop inspection systems reduce waste, aligning with circular economy targets and energy tariff pressures.

Geography Analysis

Riyadh generates 25.8 million tonnes of municipal waste, signaling high consumption and disposal volumes for flexible packs. Integrated waste-to-resource projects and the Riyadh recycled-content mandate favor early adopter converters located near the capital.

Eastern Province clusters around Dammam and Jubail host SABIC’s petrochemical complexes, providing feedstock security and export port access to GCC nations. Austrian, Chinese, and European converters have colocated extrusion lines in these zones to leverage low logistics costs and government incentives.

Western ports at Jeddah and Yanbu facilitate Red Sea exports to Africa, while multimodal corridors linked to the USD 267 billion national logistics strategy cut transit times to Levant markets. Pilot AI-enabled collection networks debut in Jeddah, giving tech-savvy recyclers first-mover advantage in PCR feedstock aggregation.

Competitive Landscape

Competition remains moderate, with top five suppliers controlling roughly 45% of tonnage, leaving ample room for mid-tier specialists. Amcor, Mondi, and Sealed Air utilize global R&D to introduce monomaterial retort pouches, whereas Napco National and Obeikan Flexible & Film capitalize on proximity to food processors for just-in-time delivery.

Vertical integration is a growing trend: SABIC’s collaboration with Lubrizol on soft-rigid compatibilizers aims to introduce recyclable PE/PP structures into markets previously served by PET-alu laminates. Sidel’s planned local F&B equipment hub will shorten lead times for bottle-to-pouch transitions.

Investment in digital presses surged after HP confirmed its first advanced-manufacturing site in Saudi Arabia, fostering a domestic ecosystem for inks, coatings, and spare parts. Converters racing to attain ISCC Plus and BRCGS certifications differentiate on export readiness as “Saudi Made” incentives reimburse up to 20% of international marketing costs.

Saudi Arabia Flexible Packaging Industry Leaders

Napco National CJSC

Saudi Printing & Packaging Company (SPPC)

Obeikan Flexible & Film Co. Ltd.

Gulf Packaging Industries Co.

Printopack Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sidel signed an MoU with Saudi authorities to explore local F&B packaging production, focusing on advanced manufacturing and technology transfer.

- April 2025: SABIC showcased TRUCIRCLE circular materials and new compounding capacity at CHINAPLAS 2025.

- April 2025: LSINC installed a PeriQ360 direct-to-object printer at Pure Beverages, boosting digital capacity for bottled-water shrink sleeves.

- March 2025: Saudi Arabia inaugurated the National Grains Supply Company (SABIL) with 2.7 million tonnes of silo capacity, spurring demand for bulk liners.

Saudi Arabia Flexible Packaging Market Report Scope

The market study tracks the demand for flexible packaging through the revenue derived from selling bags, pouches, films, and wraps. The study also tracks the effects of regulations and market drivers on growth, along with factors hindering the market growth. The Saudi Arabian Flexible Packaging Market is segmented by material (Plastic, Metal, and Paper), product type (Bags and Pouches, Films and Wraps), and End-Users (Food, Beverages, Healthcare, and Pharmaceutical). The market sizes and forecasts regarding value (USD million) for all the above segments are provided.

By Material

| Paper |

| Plastic |

| Metal Foil |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

BY End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Paper | |

| Plastic | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| BY End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-Use Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

How large is the Saudi Arabia flexible packaging market today?

The sector processed 0.8 million tonnes in 2026 and is projected to reach 0.96 million tonnes by 2031.

What is the expected CAGR for flexible packaging demand in Saudi Arabia through 2031?

Mordor Intelligence forecasts a 3.76% CAGR for the period 2026-2031.

Which material segment is growing fastest?

Bioplastics and compostable films are set to rise at a 4.95% CAGR as sustainability mandates tighten.

Which end-use sector offers the highest growth potential?

Personal care and cosmetics are forecast to expand at 4.72% CAGR thanks to local brand manufacturing.

What impact will single-use plastic bans have on converters?

The 2026 levy will add compliance costs yet accelerate demand for recyclable and compostable alternatives.

Why are converters investing in digital printing?

Digital presses enable Arabic variable data, shorter runs, and faster artwork changes, critical for pharma and e-commerce packs.

Page last updated on: