Market Overview

| Study Period | 2020 - 2031 |

|---|---|

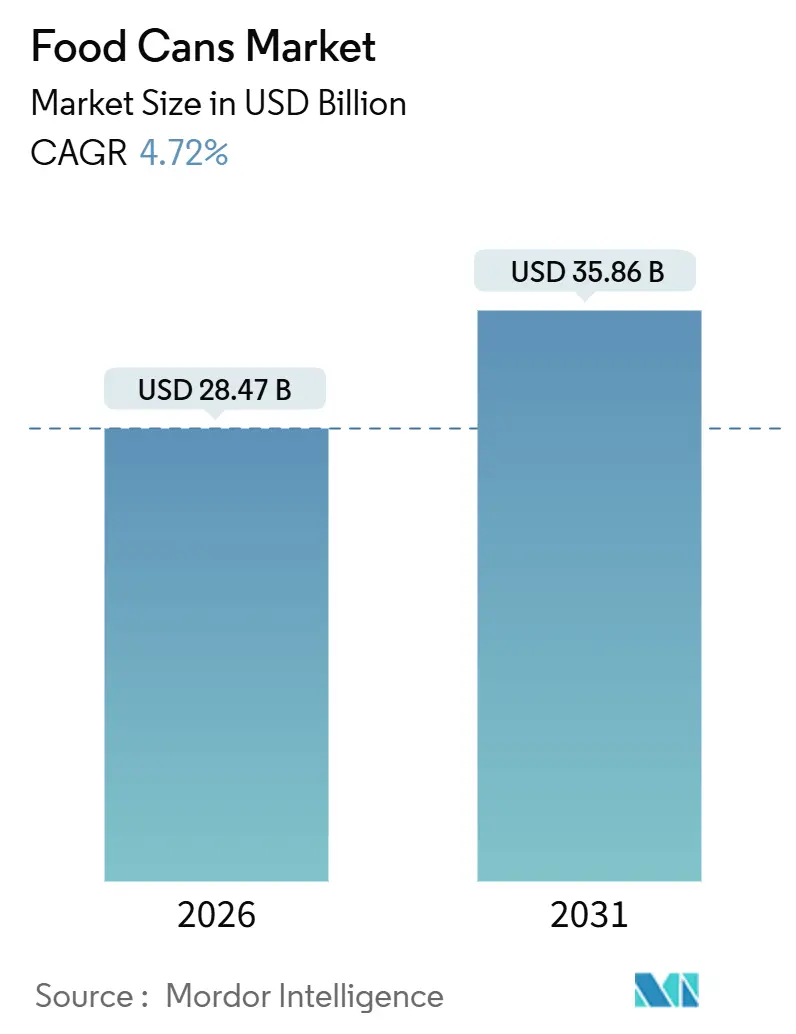

| Market Size (2026) | USD 28.47 Billion |

| Market Size (2031) | USD 35.86 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

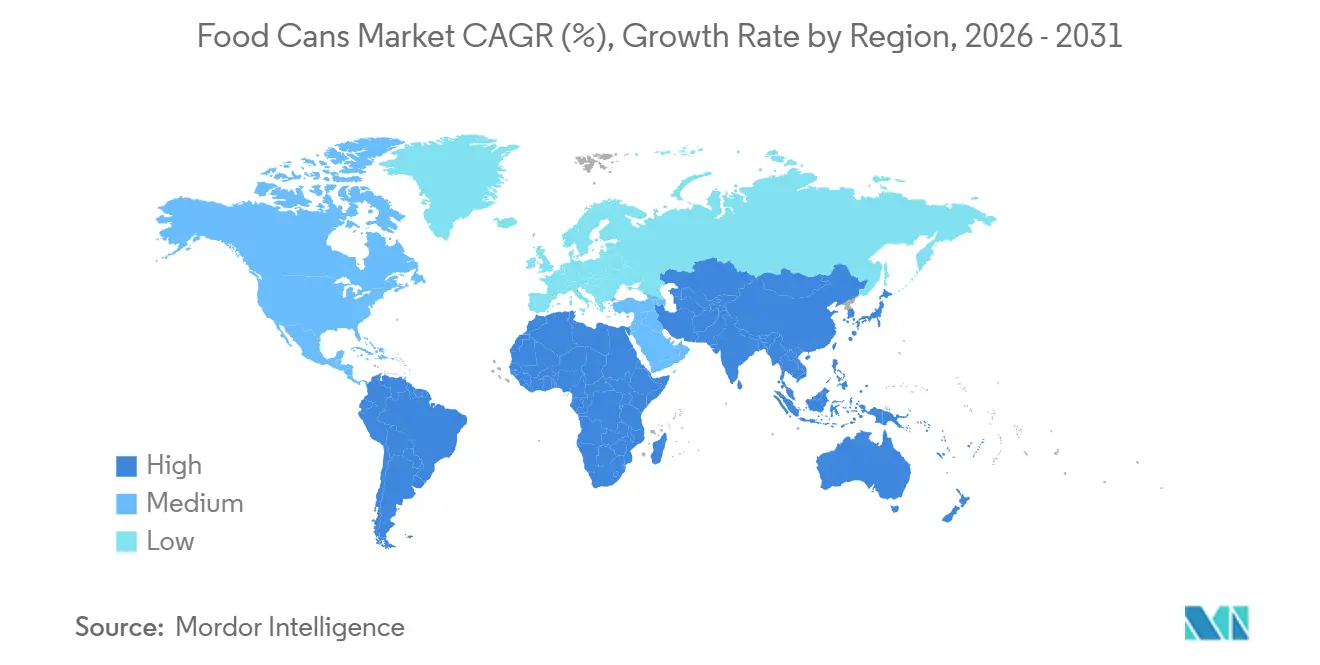

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Cans Market Analysis by Mordor Intelligence

The food cans market size stands at USD 28.47 billion in 2026 and is forecast to reach USD 35.86 billion by 2031, progressing at a 4.72% CAGR. Growth is anchored by resilient demand across shelf-stable proteins, vegetables, and premium wet pet food, even as raw material price swings and coating regulation changes compress converter margins. Lightweight aluminum is gaining ground because brand owners are under extended producer responsibility mandates, while medium-format SKUs fit the rise in single-person households. Investments in high-speed two-piece lines across the Asia-Pacific region illustrate a strategic pivot toward faster-growing geographies, and sustainability-focused retailers are pushing for BPA-free interiors to future-proof their private-label assortments.

Key Report Takeaways

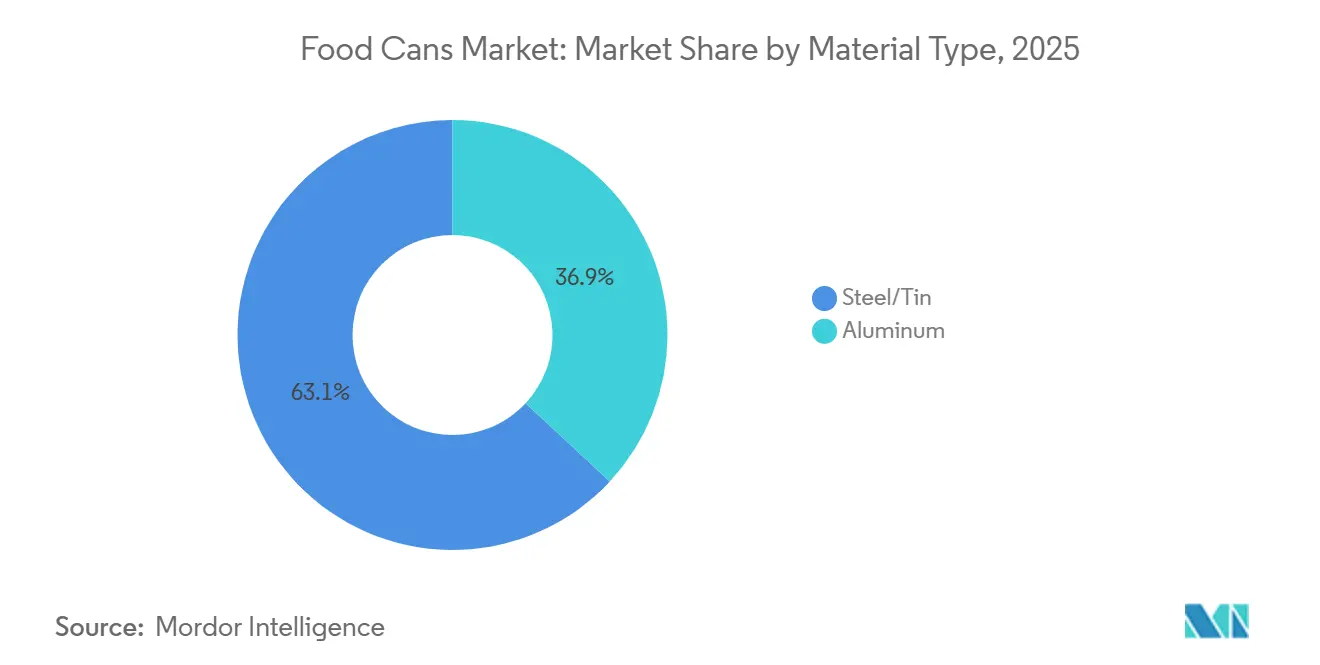

- By material type, steel and tin-based cans held 63.06% of the food cans market share in 2025, and aluminum variants are advancing at a 5.43% CAGR through 2031.

- By can type, three-piece welded formats commanded 58.63% revenue share in 2025, while two-piece drawn-and-ironed cans are expanding at a 5.32% CAGR to 2031.

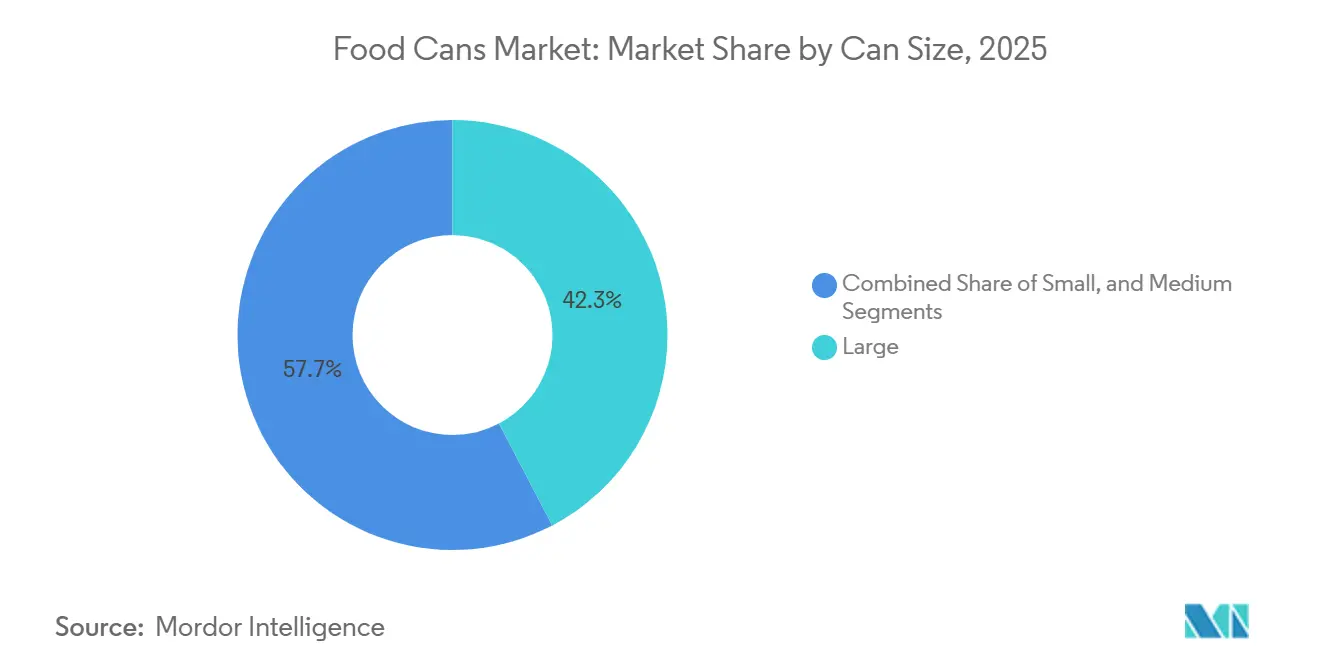

- By can size, large (more than 500 g) commanded 42.32% of the food cans market share in 2025, while medium formats between 201 grams and 500 grams are projected to grow at a 5.87% CAGR from 2026-2031, outpacing both small and large formats.

- By application, ready meals led with a 34.32% revenue share in 2025; however, pet food is the fastest-growing segment at a 6.21% CAGR through 2031.

- By geography, North America retained 39.87% of global revenue in 2025, while the Asia-Pacific region is set to grow at a 6.42% CAGR and narrow the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Cans Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Incomes and Urbanization Boosting Packaged Food Consumption | +0.9% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Expansion of Modern Retail and E-commerce Grocery Channels | +0.7% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Superior Barrier Properties and Shelf Life Extension Compared to Flexible Packaging | +0.6% | Global | Long term (≥ 4 years) |

| Increasing Pet Ownership Driving Demand for Wet Pet Food in Metal Cans | +0.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Increased Adoption of High-speed Two-piece Can Manufacturing Lines in Emerging Markets | +0.5% | Asia-Pacific, South America | Medium term (2-4 years) |

| Growing Use of Smart Can QR Codes Enabling Traceability and Consumer Engagement | +0.3% | North America and Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Urbanization Boosting Packaged Food Consumption

Rapid migration to cities across India, Indonesia, and Brazil is shrinking the window for home cooking, so households are stocking shelf-stable proteins, fruits, and vegetables that require no refrigeration. India’s Reliance Consumer Products has committed INR 40,000 crore (USD 4.8 billion) to integrated food parks, with the inaugural plant in Kurnool focusing on canned produce. This signals that processors view metal packaging as a first wave before cold-chain infrastructure matures.[1]Press Information Bureau, Government of India, “World Food India 2025 Investment Commitments,” pib.gov.inBrazil’s retail turnover reached USD 183 billion in 2024, with consumers trading down into value-priced canned staples rather than exiting categories, a pattern replicated in secondary cities across South America.

Expansion of Modern Retail and E-commerce Grocery Channels

Direct-to-consumer grocery models rely on packaging that can withstand last-mile bumps without refrigeration, giving metal cans a structural advantage over glass. Mexico’s modern retail sector captured more than 50% of household food expenditures in 2024, with e-commerce sales reaching USD 542 million, thereby widening shelf space for private-label canned beans and chilies.[2]Mexican Association of Retail Executives, “Mexico Retail Market Report 2024,” antad.netThe United Arab Emirates banned several single-use plastic items in 2026, prompting quick-service restaurants to adopt ambient-stable canned soups for delivery platforms.[3]UAE Ministry of Climate Change and Environment, “Single-Use Plastic Ban Phase 2,” moccae.gov.ae

Superior Barrier Properties and Shelf Life Extension Compared to Flexible Packaging

Metal cans block oxygen, light, and moisture, extending shelf life to as much as five years without the need for preservatives or refrigeration, an advantage in regions with erratic power supplies. The European Union banned BPA in food-contact articles in December 2024, steering converters toward polyester and acrylic coatings that preserve barrier performance and eliminate regulatory overhang. U.S. regulators are reviewing similar petitions, prompting processors to pre-emptively specify BPA-free linings and de-risk export compliance.

Increasing Pet Ownership Driving Demand for Wet Pet Food in Metal Cans

The United States pet food sector reached USD 58.5 billion in 2024 and is projected to reach USD 68.6 billion by 2029, with wet formulations in cans securing a premium position, as owners associate hermetic sealing with freshness. European single-person households tend to favor 200-gram and 400-gram cans, which reduce spoilage. Novelis recycled more than 82 billion used cans in fiscal 2024 and is building a USD 4.1 billion mill in Alabama, where over half of the capacity will be dedicated to food and beverage packaging, underscoring aluminum’s closed-loop value.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Flexible Plastic Pouches and Cartons Due to Cost and Weight Advantages | -0.6% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Volatility in Aluminum and Steel Prices Affecting Profit Margins | -0.5% | Global | Short term (≤ 2 years) |

| Stringent Regulations Against BPA-based Epoxy Linings | -0.4% | Europe, emerging in North America | Medium term (2-4 years) |

| Limited Recycling Infrastructure for Multilayer Polymer-Coated Steel Cans in Developing Economies | -0.3% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Flexible Plastic Pouches and Cartons Due to Cost and Weight Advantages

Flexible pouches weigh up to 40% less than equivalent cans, so brand owners chasing lower transport emissions adopt them for fruit cups and gravy toppers. Toyo Seikan reported share gains for its retort-pouch line in 2024 as private labels sought cheaper single-serve options. Carton suppliers such as SIG use thin aluminum laminate to approximate metal-can barrier properties, challenging ambient soup SKUs across Europe.

Volatility in Aluminum and Steel Prices Affecting Profit Margins

The London Metal Exchange's aluminum traded above USD 2,525 per metric ton in June 2025, while the U.S. Producer Price Index for steel cans rose about 2% in early 2025, squeezing converters locked into fixed-price contracts. Crown Holdings said raw-material inflation clipped gross margin by 150 basis points in Q3 2024 despite operating-efficiency gains.

Segment Analysis

By Material Type: Aluminum Builds Momentum on Sustainability

Steel and tin-based cans generated 63.06% of food cans market revenue in 2025, yet aluminum posted the fastest 5.43% CAGR through 2031. The food cans market size for aluminum formats is widening because lightweight alloys allow 10%-15% thinner walls that reduce freight cost without compromising burst strength. Novelis delivered 63% recycled content across its rolled-product mix in 2024, validating closed-loop economics that reduce carbon intensity by more than 90% relative to primary production. Aluminum’s malleability enables seamless two-piece designs that attract premium pet food and ready-meal brands, while steel stays dominant in price-led categories where deep-draw tooling amortizes over high volumes.

Converters favor aluminum when shipping to e-commerce warehouses that bill by dimensional weight, and the material’s non-ferrous nature avoids corrosion in acidic tomato bases. Still, magnetic steel simplifies municipal sortation, an edge in mature North American recycling systems. In emerging markets, limited remelt capacity caps aluminum uptake, so steel maintains hold in staple canned vegetables. The dual-material landscape means processors often dual-source to hedge price swings, further advancing the food cans market as players align substrate to channel and geography.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Can Type: Two-Piece Formats Gain Traction

Three-piece welded cans captured 58.63% of revenue in 2025, but two-piece drawn-and-ironed designs are expanding at a 5.32% CAGR through 2031. Krones filling lines now process more than 120,000 units per hour, allowing converters to amortize higher tooling costs faster and achieve a sub-USD 0.30 cost for a standard 400-gram can. Seamless bodies eliminate side welds, reducing coating needs and enhancing shelf appeal, which boosts adoption in premium pet food and microwavable ready meals.

The food cans market share for two-piece formats climbs fastest in the Asia-Pacific region, where greenfield plants often skip legacy welding altogether. Ball Corporation will invest USD 60 million in Andhra Pradesh to add two-piece capacity, in line with India’s double-digit growth in metal packaging demand. Three-piece technology remains favored for institutional cans weighing above 500 grams because deep draws would require more costly tooling. As processors balance cost, speed, and material intensity, both formats coexist, giving the food cans market resilient substrate diversity.

By Can Size: Medium Formats Fit Changing Lifestyles

Large cans, above 500 grams, still account for 42.32% of the 2025 volume, as foodservice and multi-person households value bulk economics. However, medium cans, weighing between 201 grams and 500 grams, register the quickest 5.87% CAGR to 2031. Single-person households, now comprising more than 30% of urban dwellings in the United States, tend to gravitate toward portion-controlled SKUs that minimize leftovers. Mexican retailers have widened shelf space for 300-gram beans and tomatoes that anchor meal-kit recipes.

The food cans market size allocated to medium formats benefits from e-commerce: smaller units fit parcel constraints and reduce kerbside waste. Small cans under 200 grams stay niche, yet command high per-unit prices in infant nutrition or gourmet tuna. Bulk institutional formats will persist, especially in school meal programs and catering, but their lower growth tempers overall demand, prompting converters to retool lines toward agile, mid-size production runs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Pet Food Surges Ahead of Ready Meals

Ready meals contributed 34.32% of segment revenue in 2025, but pet food is sprinting at a 6.21% CAGR through 2031. Humanization trends mean owners buy wet food cans with human-grade meats, trusting the metal’s hermetic seal for freshness. The food cans market size tied to pet food will therefore outstrip that for some traditional center-store items. Tuna, salmon, and sardine processors rely on cans to secure three-year shelf lives for export corridors from Southeast Asia to Europe, thereby reinforcing the relevance of metal for protein preservation.

Vegetable and fruit canning remains a pantry staple, yet growth is modest as fresh and frozen alternatives gain retail end-caps. Processed soup and sauce brands defend their share with BPA-free tins and QR-code engagement. The diverse application matrix sustains the food cans market by pairing mature center-store categories with ascendant premium pet food.

Geography Analysis

North America held 39.87% of the global revenue in 2025, as entrenched canning lines, established supply chains, and high per-capita consumption sustain baseline volumes. Growth lags behind the global CAGR as the population plateaus, yet operational upgrades support margins. Crown Holdings sold its European tinplate arm to reallocate capital toward North American specialty food cans, underscoring a shift to higher-margin niches. Steel price volatility and a 43% aluminum-can recycling rate in 2023 have tightened scrap supply, nudging converters to pass through surcharges.

The Asia-Pacific region expands at the fastest rate, with a 6.42% CAGR, driven by urbanization, increased disposable income, and investment in local supply chains. Ball’s Sri City and Taloja expansions demonstrate how global majors are localizing two-piece lines to cater to multinational food processors entering India. China’s tinplate mills and Southeast Asian tuna corridors attract joint ventures blending Japanese coating know-how with local distribution. India’s World Food India summit drew INR 1.02 trillion (USD 12.2 billion) in pledges, pivoting toward canned produce to circumvent limited cold chains.

Europe advances at roughly 4.3% CAGR, a pace dampened by slow demographic growth but energized by sustainability rules. The December 2024 BPA ban forces converters to adopt next-generation linings, amplifying capital needs yet giving early movers a marketing edge. Private-label penetration continues to rise as discounters promote value-oriented canned assortments. South America and the Middle East and Africa grow at mid-single digits; Brazil’s USD 183 billion retail market shows resilience and the UAE plastic-ban shift adds incremental can volumes in foodservice settings.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The food cans market features a top-five cohort, including Crown Holdings, Silgan Holdings, Trivium Packaging, Ardagh Metal Packaging, and Ball Corporation, which controls approximately 55%-60% of global revenue, with no single player holding a share above 20%. Crown’s Q3 2024 net sales reached USD 3.0 billion, yet segment income increased because operational efficiency offset the impact of soft volumes. The firm’s exit from European tinplate underlines a pivot away from commodity lines toward specialty formats.

Ardagh trimmed wall gauges by 15% on select SKUs, cutting per-unit alloy consumption and logistics cost, and reinforcing its sustainability pitch. Silgan’s USD 1.025 billion Weener Plastik deal broadens closures and dispensing capabilities, allowing the company to bundle cans and caps for sauces, an approach that secures contracts and counters flexible-pouch threats. Ball bets on Asia-Pacific, committing fresh capital to India, while Trivium leans on recycled-content messaging to win European tenders.

Start-ups in flexible packaging are eroding share in price-sensitive gravies and fruit cups, so incumbents deploy smart-code printing and rapid changeover lines to defend shelf presence. The competitive focus for 2026-2031 rests on material efficiency, regional capacity balancing, and digital engagement. This environment keeps pricing discipline tight and underscores why converters pursue vertical integration into coatings, lids, and logistics.

Food Cans Industry Leaders

Crown Holdings, Inc.

Toyo Seikan Group Holdings Ltd.

CANPACK S.A.

Ardagh Metal Packaging

Ball Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: The United Arab Emirates fully enforced Phase 2 of its single-use plastic ban, prohibiting cups, lids, cutlery, and expanded polystyrene food containers, which is steering institutional caterers toward canned soups and stews.

- November 2025: Ball Corporation allocated USD 60 million to expand Sri City, India, adding two-piece food can capacity in response to projected 10% annual demand growth.

- March 2025: Reliance Consumer Products agreed with the Government of India to build canned-food complexes totaling INR 40,000 crore (USD 4.8 billion) under the World Food India initiative.

- December 2024: The European Union enacted Regulation 2024/3190, banning BPA in food-contact materials with staggered transition periods, compelling converters to switch to polyester and acrylic linings.

Global Food Cans Market Report Scope

Food cans are among one of the packaging options for the mobile lifestyle. These can be carried easily to outdoor sporting events, festivals, and more, whereas glass is typically forbidden because of its breakability. The affordability and recyclability of cans, the rising popularity of canned food, and the launch of new food products are expected to contribute to the market growth in the future.

The Food Cans Market Report is Segmented by Material Type (Steel/Tin, and Aluminum), Can Type (2-piece Cans, and 3-piece Cans), Can Size (Small ≤200 g, Medium 201-500 g, and Large >500 g), Application (Ready Meals, Fish and Seafood, Fruits and Vegetables, Processed Food, Pet Food, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Steel/Tin |

| Aluminum |

By Can Type

| 2-piece Cans |

| 3-piece Cans |

By Can Size

| Small (Less than Equal to 200 g) |

| Medium (201-500 g) |

| Large (More than 500 g) |

By Application

| Ready Meals |

| Fish and Seafood |

| Fruits and Vegetables |

| Processed Food |

| Pet Food |

| Other Applications |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Steel/Tin | ||

| Aluminum | |||

| By Can Type | 2-piece Cans | ||

| 3-piece Cans | |||

| By Can Size | Small (Less than Equal to 200 g) | ||

| Medium (201-500 g) | |||

| Large (More than 500 g) | |||

| By Application | Ready Meals | ||

| Fish and Seafood | |||

| Fruits and Vegetables | |||

| Processed Food | |||

| Pet Food | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the global food cans market in 2026?

The food cans market size is USD 28.47 billion in 2026 and is forecast to grow to USD 35.86 billion by 2031 at a 4.72% CAGR.

Which material is growing fastest in food can production?

Aluminum cans are advancing at a 5.43% CAGR because lightweighting and high recycled content align with retailer sustainability goals.

Why are medium-size cans gaining traction?

Units between 201 grams and 500 grams fit single-serve meal planning and e-commerce parcel limits, driving a 5.87% CAGR through 2031.

What is the leading application segment in revenue terms?

Ready meals lead with 34.32% of 2025 revenue, although pet food is expanding faster at 6.21% CAGR.

Which region will add the most incremental volume by 2031?

Asia-Pacific, growing at 6.42% CAGR, will add the largest share of new food can demand due to urban population and local capacity investments.

How are regulations shaping coating technology?

The European Union’s BPA ban effective from December 2024 is pushing converters toward polyester and acrylic linings, a change likely to influence other regions.