Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

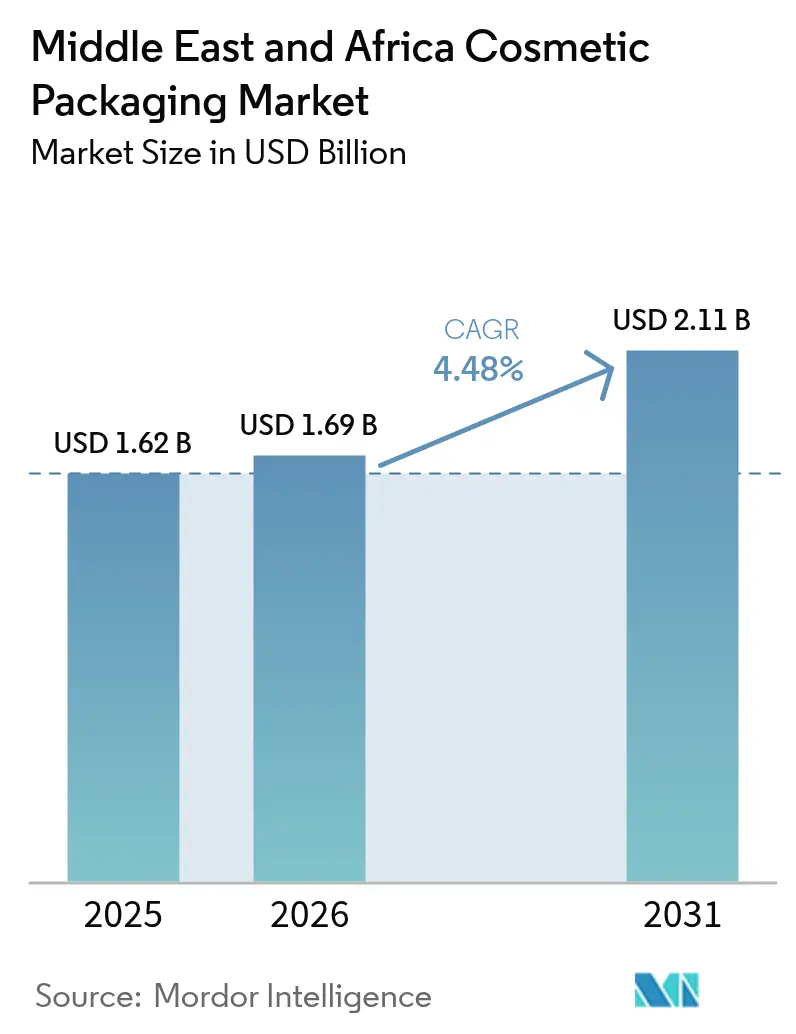

| Base Year Market Size (2025) | USD 1.62 Billion |

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Cosmetic Packaging Market Analysis by Mordor Intelligence

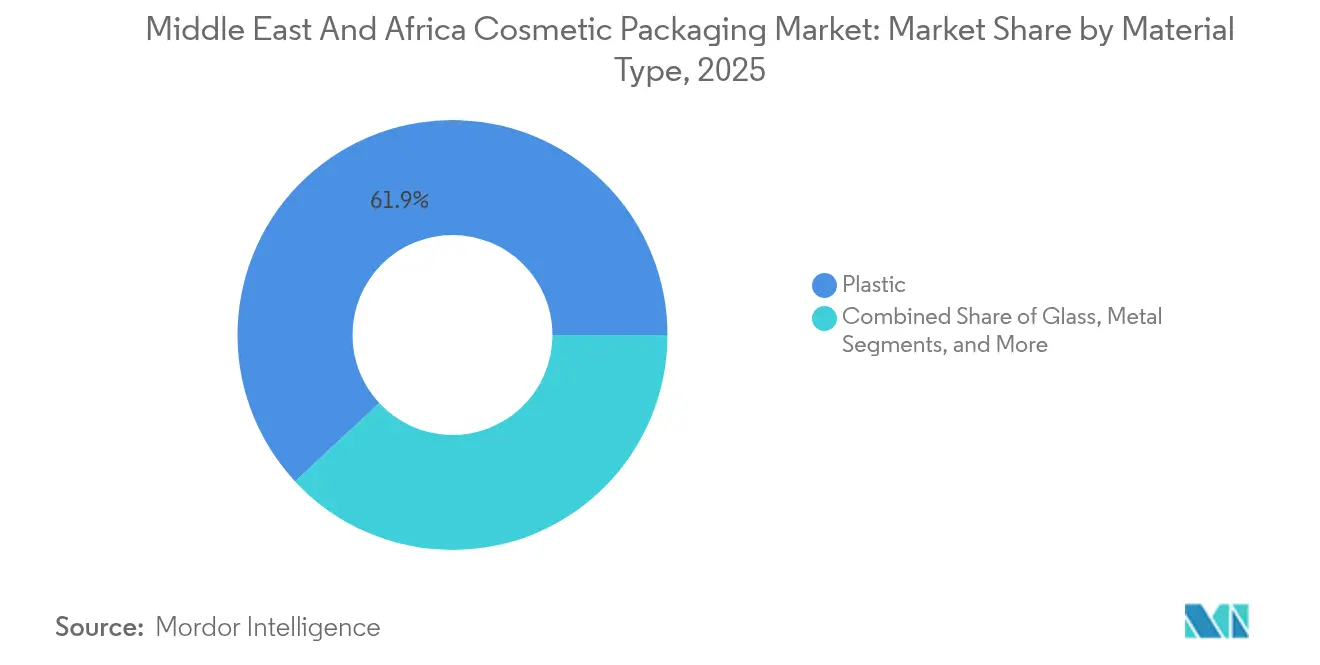

The Middle East and Africa cosmetic packaging market size was valued at USD 1.62 billion in 2025 and estimated to grow from USD 1.69 billion in 2026 to reach USD 2.11 billion by 2031, at a CAGR of 4.48% during the forecast period (2026-2031). This moderate expansion is anchored in halal-driven material selection, rising beauty consciousness across sub-Saharan Africa, and robust luxury demand in Gulf Cooperation Council economies.[1]Dubai Municipality, “Environmental Compliance and Sustainability,” dm.gov.ae Currency volatility has amplified the strategic value of localized production, encouraging manufacturers to hedge import costs by building regional plants. Plastic maintained 62.45% market share in 2024, yet bio-degradable alternatives are gaining momentum as regulators push circular-economy mandates. Saudi Arabia led the country demand at 28.43% market share in 2024, whereas South Africa’s 6.21% CAGR positions it as the fastest-growing geography. Bottles and jars captured 36.22% of product demand, but flexible pouches are growing at a 6.11% CAGR thanks to e-commerce logistics efficiency.

Key Report Takeaways

- By material, plastic held 61.92% of the Middle East and Africa cosmetic packaging market share in 2025, while bio-degradable and compostable materials are projected to expand at a 5.52% CAGR to 2031.

- By product type, bottles and jars led with 35.78% revenue share in 2025; flexible pouches and sachets are forecast to grow at a 6.01% CAGR through 2031.

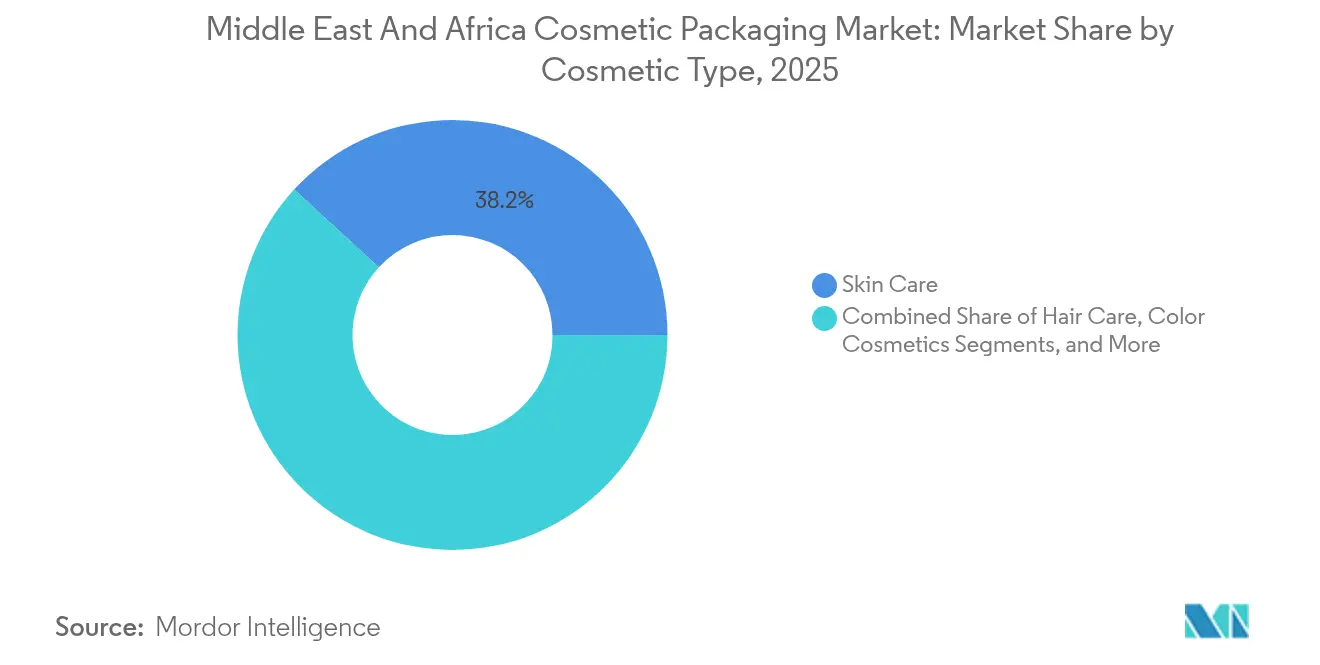

- By cosmetic type, skin care commanded 38.18% share of the Middle East and Africa cosmetic packaging market size in 2025, and hair care is advancing at a 5.86% CAGR through 2031.

- By distribution channel, direct sales dominated with 78.12% share in 2025, whereas indirect channels are projected to rise at a 5.42% CAGR to 2031.

- By geography, Saudi Arabia accounted for 28.11% of regional demand in 2025; South Africa records the highest CAGR at 6.13% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Cosmetic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Customized and luxury packs | +0.8% | Gulf countries, South Africa | Medium term (2-4 years) |

| Sustainable beauty and circular mandates | +1.2% | UAE, Egypt | Long term (≥4 years) |

| E-commerce protective designs | +0.9% | Urban MEA | Short term (≤2 years) |

| Halal and clean-label compliant packs | +0.7% | Middle East, expanding Africa | Medium term (2-4 years) |

| Premium men’s grooming and niche fragrances | +0.5% | Saudi Arabia, UAE, Nigeria | Medium term (2-4 years) |

| Tourism-led duty-free rebound | +0.4% | Dubai, Doha, Cairo airports | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Customized and Luxury Packs

Personalized packaging now differentiates brands as Gulf consumers expect culturally resonant aesthetics, such as Arabic calligraphy and heritage-inspired color palettes. Limited-edition fragrance launches with local artists have demonstrated strong engagement and loyalty.[2]Emirates Standards and Metrology Authority, “Regulatory Framework and Standards,” esma.gov.ae Suppliers are funding regional design centers and installing digital printers that deliver cost-effective small-batch runs, enabling premium pricing without inflating inventory costs. Brands leverage this agility to test micro-collections aligned with major cultural events, deepening relevance. The focus on cultural customization is also encouraging collaborations between global converters and local design houses that bring nuanced insights to premium packaging programs.

Rise of Sustainable Beauty and Circular-Economy Mandates

Extended Producer Responsibility in the UAE obligates cosmetic firms to finance waste management across the product lifecycle. Manufacturers like Pack2Earth supply compostable substrates engineered for high-temperature desert environments. Traditional resin converters face specification shifts that inflate R&D cycles and capital expenditure but create premium opportunities for sustainability specialists. Life-cycle assessment models now accompany most bid responses, introducing environmental metrics alongside price and lead time. As material accountability becomes mainstream, early adopters lock in multiyear contracts that enhance visibility on raw-material sourcing and cost structures.

E-commerce Boom Driving Protective/Omni-Channel Designs

Online beauty now exceeds 35% of cosmetic sales in major Middle Eastern metros, compelling packaging that withstands shipping shocks while still delivering a striking unboxing experience. Hybrid constructions pair rigid outer shells with premium inner trays, balancing logistics protection and shelf appeal. Tamper-evident seals and advanced cushioning foams are standard, lifting unit costs but lowering damage rates. Omni-channel consistency requires packs to transition seamlessly from store shelf to courier van without redesign. Brands also embed QR codes that redirect consumers to authentication portals, combating counterfeit risk heightened by cross-border e-commerce flows.

Growth of Halal and Clean-Label Brands Needing Compliant Packs

Halal certification now governs not only ingredients but also traceability of inks, adhesives, and secondary components. Packaging plants invest in segregated halal lines and supplier audit systems to document full material provenance. Clean-label positioning broadens appeal beyond Muslim consumers, boosting export opportunities to non-traditional markets seeking ethical sourcing. QR-enabled labels display certification details in real time, reinforcing transparency. Compliance complexity raises entry barriers, consolidating demand around converters able to furnish documentation and accommodate small-lot SKUs that target niche consumer segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics and labeling regulations | -0.6% | UAE, Saudi Arabia, Egypt | Short term (≤2 years) |

| Currency volatility and resin inflation | -0.9% | Import-dependent MEA | Short term (≤2 years) |

| Skills gap in sustainable engineering | -0.4% | Sub-Saharan Africa | Long term (≥4 years) |

| Political instability disrupting supply | -0.7% | North Africa, parts SSA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regional Plastics and Labeling Regulations

The UAE’s single-use plastic ban and Saudi Arabia’s EPR rules compel rapid design alterations, raising unit costs by 15–25% and favoring suppliers already versed in sustainable alternatives. Multilingual labeling statutes expand panel real estate, prompting larger primary packs or extended fold-out labels. Compliance complexity accelerates consolidation as smaller converters struggle to fund testing and certification. Regulators tie import permits to proof of recyclability, prompting brands to negotiate take-back programs with material recovery firms.

Currency Volatility Inflating Imported Resin Costs

Polymer price swings of 20-30% over twelve months compress margins, particularly in Nigeria, Egypt, and Kenya, where resin imports dominate supply.[3]Central Bank of Egypt, “Economic Reports and Currency Data,” cbe.org.eg Larger converters deploy commodity hedging, whereas smaller firms lean on shorter-term contracts and pass-through pricing that erodes competitiveness. Localization initiatives spur investments in regional polymer plants, yet commissioning timelines limit near-term relief. Financial turbulence also slows CAPEX for advanced machinery, delaying technology upgrades that could enhance sustainability performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Dominance Faces Sustainable Disruption

The Middle East and Africa cosmetic packaging market size for plastic substrates remained the largest in 2025 as advanced polymers met performance and cost targets pivotal to high-volume categories. Bio-degradable and compostable options, while still niche, are growing fastest at 5.52% CAGR on regulatory tailwinds that reward circular design. Glass preserves an aura of luxury, especially in perfume and prestige skincare, where tactile heft commands premium shelf pricing. Metal retains relevance in aerosol and gift SKUs that benefit from structural rigidity and upscale aesthetics. Paperboard gains share in secondary applications as barrier-coated grades improve moisture protection.

The transition toward greener substrates compels intricate supply-chain recalibration. Packaging converters pair life-cycle assessment audits with pricing proposals, enabling brand owners to quantify environmental benefits. Partnerships such as Eastman Chemical’s molecular recycling program offer drop-in resins that maintain functional parity with virgin polymers while satisfying recyclability thresholds. Paper primary packs, fortified through water-based barrier coatings, advance into skin-treatment jars and compact cases, signaling broader acceptance of fiber-based formats in traditionally plastic-centric segments.

By Product Type: Flexible Formats Gain E-commerce Traction

Bottles and jars secured the largest revenue slice in 2025, underscoring consumer familiarity and premium cues critical to skincare and fragrance. Yet flexible pouches and sachets, pivotal to cost-sensitive markets and weight-optimized logistics, are accelerating at 6.01% CAGR, capturing incremental volumes from mass hair-care and body-wash refills. Tubes and sticks hold steady as targeted applicators in lip care and medicinal skin treatments, where dosage control and portability resonate.

Retail migration online amplifies demand for flexibles that reduce dimensional weight and minimize breakage. Multilayer laminates adopt high-barrier EVOH layers, safeguarding volatile actives during long-haul shipping. Sachet innovation explores twin-chamber formats that enable mixing at the point of use, supporting customizable regimens. Pump and sprayer assemblies integrate locking collars and clip seals to comply with courier regulations, mitigating leakage during air transport.

By Cosmetic Type: Hair Care Emerges as Growth Leader

Skin care sustained dominance with a 38.18% share in 2025 as multi-step regimens boosted per-capita unit consumption. However, hair care’s 5.86% CAGR crowns it the fastest-expanding vertical, propelled by male grooming uptake and rising demand for specialized treatment masks and serums. Color cosmetics innovate around hygienic in-pack applicators to reassure consumers on product integrity. Fragrance packaging evolves via collectible flacons and refill cartridges that reinforce brand loyalty while reducing waste.

Rising disposable income elevates spending on premium scalp therapies, prompting packaging equipped with precision nozzles and opaque barriers that shield photosensitive actives. Brands cross-promote skin and hair bundles, necessitating harmonized pack aesthetics that communicate regimen coherence. Portable mini-packs cater to travel retail and gym bag usage, extending consumption occasions and driving unit velocity.

By Distribution Channel: Indirect Channels Accelerate Growth

Direct brand-owned boutiques and salons preserved 78.12% share in 2025 by delivering personalized consultations essential in prestige beauty. Indirect channels, however, gain ground as e-commerce and duty-free retail scale, recording a 5.42% CAGR through 2031. Online platforms refine beauty-specific fulfillment-temperature-controlled storage, fragile handling, and authentication workflows-unlocking cross-border demand.

Packaging now balances shelf visibility with shipment durability. Inserts brace glass flacons inside retail boxes, and collapsible void-fill solutions optimize volumetric weight. Duty-free assortments rely on bilingual artwork and security devices compatible with customs inspections. Direct channels continue to pilot refill bars and in-store personalization, leveraging exclusive pack variants to cement loyalty.

Geography Analysis

Gulf Cooperation Council countries exhibit sophisticated pack formats marrying luxury cues with halal compliance. Saudi Arabia’s sizeable 2025 market share stems from Vision 2030 policies that subsidize local packaging capacity and stimulate SME participation in beauty value chains. The UAE capitalizes on world-class logistics infrastructure, facilitating just-in-time fulfillment for both brick-and-mortar and e-commerce channels. Turkey’s consolidated converter base services European and Middle Eastern brand owners, blending competitive labor with proximity advantages to raw-material suppliers. Political stability across these markets attracts foreign direct investment into high-speed lines and digital embellishment equipment.

African demand presents heterogeneous conditions. South Africa’s growth trajectory benefits from established converting know-how, skilled labor pools, and supportive industrial financing that lowers entry barriers for advanced technologies. Egypt leverages its Suez connectivity to woo packaging investors targeting North and East African consumers. Nigeria’s populous urban centers promise scale, yet currency volatility and energy constraints elevate operational risk. Continental free-trade implementation promises to harmonize duties, easing cross-border raw-material flows and catalyzing regional supply-chain integration.

Red Sea shipping disruptions have doubled container freight rates, incentivizing freight-route diversification and higher regional safety stocks. Manufacturers respond by expanding in-country warehousing and exploring rail corridors that bypass maritime chokepoints. Currency hedging gains prominence, especially for resin importers exposed to USD invoices. Skills development initiatives, often co-funded by multinationals and development banks, target sustainable material engineering to ensure long-term innovation capacity.

Regulatory Landscape

Cosmetic packaging placed on GCC markets is shaped by harmonized Gulf requirements, with GSO 1943:2024 setting safety and labeling expectations for cosmetic and personal care products from its May 2024 approval. In the UAE, Dubai Municipality operates the Montaji system as a mandatory pre-market registration route for cosmetics and personal care products, and compliance expectations extend into packaging and pack information management, increasing the importance of documented specifications and controlled artwork workflows.

Country-level enforcement adds operational checkpoints for packaging supply. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) regulates cosmetic products and related compliance documentation, and the importation of empty cosmetic packaging is controlled through Fasah clearance and brand-authorization requirements to mitigate misuse and counterfeiting risk. In South Africa, the Foodstuffs, Cosmetics and Disinfectants Act (No. 54 of 1972) remains the primary legal framework, with labeling and packaging practices referencing standards such as SANS 289 for pre-packaged products, keeping compliance and print-readiness central to converter selection.

Value Chain Analysis

The value chain begins with petrochemical and polymer inputs for rigid and flexible packs, and it extends to glass, aluminum, paperboard, inks, and adhesive systems that must fit halal/clean-label traceability requirements and evolving recyclability expectations. Converters in the region provide molding, extrusion/blown-film, decoration (digital printing, hot-stamp, metallization), and closure/dispensing integration, then route finished packs either directly to brand owners and contract manufacturers or through distributors that support fragmented African markets. Regulatory bodies and platforms, including SFDA for cosmetic compliance in Saudi Arabia and GSO-aligned standards across the GCC, influence artwork control, documentation, and market-entry timelines, shaping how suppliers structure QA, batch traceability, and change-control.

Midstream execution increasingly depends on localized capacity and resilient logistics, as currency volatility and import exposure raise the value of regional manufacturing and warehousing. Sustainability-linked requirements, such as recycled-content and EPR-driven reporting, push upstream procurement toward PCR resins and verified material streams, while downstream channels, notably e-commerce and duty-free, pull for protective secondary packs and tamper-evident features. Brands typically concentrate sourcing among converters that can bundle primary packs with pumps/sprayers, support multilingual labeling execution, and keep audit-ready documentation for halal, recycled-content, and safety requirements.

Competitive Landscape

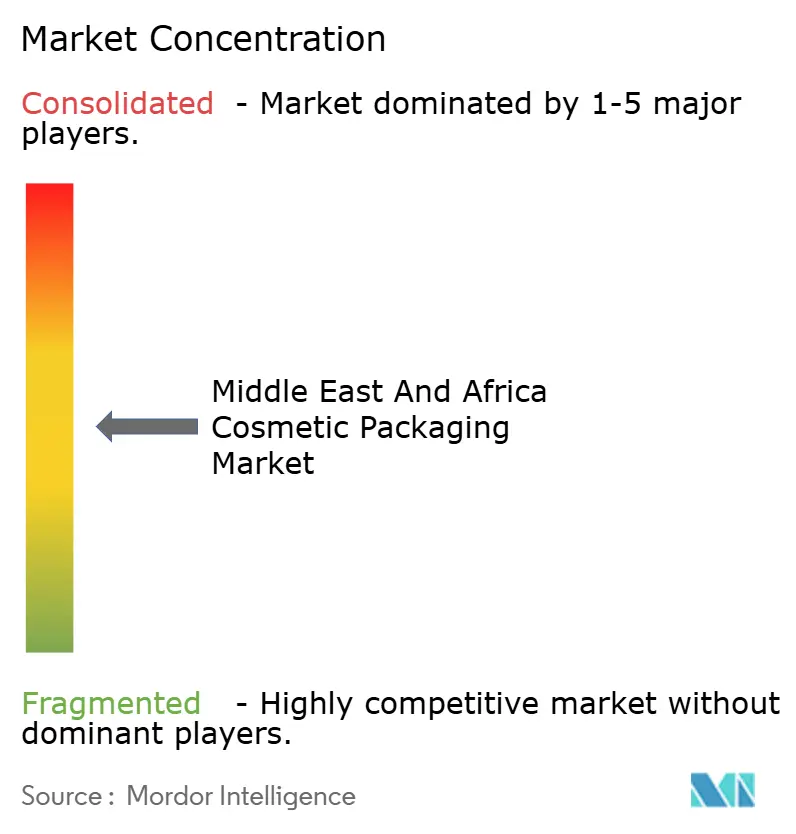

The Middle East and Africa cosmetic packaging market features moderate fragmentation as global leaders deepen regional footprints through joint ventures and acquisitions. Amcor’s USD 8.43 billion merger with Berry Global in April 2025 enlarged its flexible and rigid portfolio, enhancing service levels for beauty brands seeking material breadth and sustainability credentials. Gerresheimer’s halal-certified lines and bio-based glass offerings court premium fragrance and skincare clients. Regional converters counter with proximity benefits, faster lead times, and nuanced regulatory knowledge.

Technological differentiation intensifies competition. Digital printing accelerates customization programs, while molecular recycling collaborations, such as Eastman Chemical and Toly, produce circular content without compromising performance. Smart packaging elements-NFC chips and variable QR codes-gain traction for authentication and consumer engagement, particularly in high-value skincare. Mergers and partnerships enable cost-sharing on R&D required to meet evolving EPR thresholds and carbon footprints.

Market entrants specializing in compostable laminates and refill systems capture share from legacy rigid formats. Yet capital intensity and certification hurdles insulate incumbent converters with diversified product lines. Pricing pressure persists amid resin volatility, but sustainability premiums partly offset cost spikes. The competitive arena thus rewards scale, technical agility, and compliance infrastructure able to satisfy halal, EPR, and multilingual labeling mandates simultaneously.

Middle East And Africa Cosmetic Packaging Industry Leaders

Amcor plc

ALPLA Werke Alwin Lehner GmbH & Co KG

Napco National Company

Nioro Plastics (Pty) Ltd

Al LendOn Packaging (Pty) Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment in regional manufacturing and premium decoration is creating room for converters that can supply luxury and culturally customized formats while meeting circular-economy constraints. Tunisia is a visible example in 2026, with MYC Beauty Innovation inaugurating a packaging hub at the Monastir Technopole (USD 5.4 million) and Pusterla 1880 inaugurating a production unit in Sousse (initial EUR 4 million) aimed at luxury beauty and fragrance packaging, reinforcing North Africa as a production base for local demand and export-oriented programs.

Scale-building and compliance-linked redesign are also opening opportunities across Southern and East Africa. In South Africa, Prime Product Manufacturing acquired L'Oréal South Africa's Midrand facility in March 2026, expanding regional manufacturing and packaging capacity that can support higher-volume runs and faster replenishment for hair care and skin care packaging programs. On the regulatory side, Kenya issued the Environmental Management and Coordination (Management and Control of Plastic Packaging Materials) Regulations in February 2026, requiring manufacturers and importers to develop and implement EPR plans, which increases demand for recyclable designs, traceable materials, and pack formats that can support producer-responsibility reporting. In the UAE, KEZAD-related activity around high-end packaging manufacturing (via a 2PointZero, ISEM Packaging, and KEZAD MoU) highlights demand for local capability that reduces reliance on long-distance imports for premium packs used in GCC prestige beauty.

Recent Industry Developments

- April 2026: Mediterrania Capital Partners signed a share purchase agreement to acquire 100% of Societe Marocaine des Manufactures de Mohammedia, the holding company of Amcor Flexibles Mohammedia, from Amcor. The deal points to private-capital interest in North African flexible packaging platforms and can influence capacity access and customer coverage for beauty and personal care packaging in the region.

- April 2025: Amcor completed its all-stock merger with Berry Global, expanding its flexible and rigid packaging footprint and broadening its capabilities for beauty and personal care customers. The combined scale supports wider material and format offerings as brands shift toward circular-design requirements and omni-channel pack performance needs.

- December 2024: Gerresheimer finalized its purchase of Bormioli Pharma, strengthening molded-glass capabilities that overlap with premium cosmetic and fragrance packaging requirements. The move deepens access to high-value glass know-how and increases competitive pressure on regional suppliers serving prestige beauty formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of packaging used to pack and protect cosmetic products sold across the Middle East and Africa, counted across common materials and formats used for beauty and grooming items.

Scope exclusions: We exclude non-cosmetic end uses (such as household cleaners and pharma packs) and do not count bulk industrial transport packaging that is not meant for consumer-ready cosmetic packs.

Segmentation Overview

- By Material Type

- Plastic

- Glass

- Metal

- Paper and Paperboard

- Bio-degradable/Compostable

- By Product Type

- Bottles and Jars

- Tubes and Sticks

- Pouches and Sachets

- Other Product Types

- By Cosmetic Type

- Skin Care

- Hair Care

- Color Cosmetics

- Fragrances

- Other Cosmetic Types

- By Distribution Channel

- Direct Sales Channel

- Indirect Sales Channel

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping cosmetic demand and packaging supply signals for the Middle East and Africa, then narrowing them to what is relevant for cosmetic packs. Public sources were used to anchor the base, such as UN Comtrade for trade flows of packaging materials and articles, World Bank and IMF macro series for inflation and currency context, national statistics portals for manufacturing and consumer price indicators, and customs or port authority releases where available.

We also reviewed regulatory and standards references that affect packaging choices, such as regional sustainability directives and plastics related rules, followed by trade association publications and reputable press coverage on packaging capacity additions and recycling targets. Company annual reports, investor decks, and product packaging announcements helped validate which materials and pack formats brands are pushing in the region. A few paid database subscriptions were used only where they add structure, such as company financials and patent databases to cross-check supplier scale and innovation intensity. These desk sources are not exhaustive, and additional public references were used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions that are hard to observe in public data, especially format mix shifts, resin and glass price pass-through, and how local converting capacity is being utilized. We spoke with a mix of packaging converters, material suppliers, brand owners, and distributors across the Middle East and Africa so the model reflects on-the-ground demand signals and realistic pricing behavior. Inputs were also checked by role and region to reduce single-market bias and to confirm that the final totals match how packaging is bought and sold locally.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 53% | Functional/Unit leaders: 31% | |

| Smaller Players: 20% | Managers: 56% |

Market-Sizing & Forecasting

The core sizing was built using a top-down demand reconstruction, where regional cosmetic consumption is translated into packaging demand by applying pack intensity and format shares for key product groups (for example, skin care, hair care, and fragrances). That demand pool is then valued using average selling price ranges by material and pack type, adjusted for the region's import dependence and local converting economics.

To keep the numbers grounded, the totals were corroborated with selective bottom-up checks, such as roll-ups of converter capacity signals, sampled price quotes for bottles, tubes, and pumps, and country-level import patterns for key packaging inputs. Where company data was incomplete, gaps were handled by using peer benchmarks for utilization and by allocating the remainder to smaller converters through share-based assumptions that were verified in interviews.

For forecasting, we relied on scenario analysis supported by a light multivariate view of the drivers that respondents consistently tied to packaging demand. Key inputs include beauty and personal care output growth, shifts toward lightweight packs and pouches, resin and glass price trends, premiumization in GCC fragrance and skin care, and recycled content adoption that can move unit costs. The forecast path is then reviewed against expected currency moves and inflation so value growth is not overstated.

Data Validation & Update Cycle

Validation is done in layers so one data stream does not dominate the final answer. Model outputs are compared with independent signals like trade trends for packaging materials, observable capacity additions, and the implied packaging spend per unit of cosmetic demand by country group. When a variance is spotted, the inputs are revisited, followed by a second pass that checks whether the logic still holds across materials and pack formats.

Before sign-off, another analyst reviews the full chain from assumptions to totals, and clarifying calls are triggered when a key input moves outside the expected range. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulation changes or sharp material price movements. Right before delivery, a final review pass is completed so clients receive the most current view.

Mordor Intelligence's Middle East and Africa Cosmetic Packaging Market Size Compared Against Other Published Estimates

Published market sizes for Middle East and Africa cosmetic packaging do not always match because studies can differ on what counts as cosmetic packaging, which years are treated as the base, and how pricing is converted into USD during volatile currency periods. Even when the same geography is named, the mix of included pack formats and whether premium fragrance packaging is treated differently can change the total.

The benchmark table shows a noticeable spread, and in Mordor Intelligence's model the market is counted for cosmetic packaging across materials and pack formats in MEA with a base year of 2025 and an explicit 2026 value, while some estimates lean on a different base year and may bundle adjacent personal care packaging or apply more aggressive price escalation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.69 B (2026) | |

| Global Consultancy A | USD 2.50 B (2024) | Uses an earlier base year and appears to apply broader inclusion rules that can pull in adjacent personal care packaging, and then carries forward pricing with a higher implied escalation into the forecast. |

| Industry Publisher B | USD 0.98 B (2025) | Narrow scope limited to glass packaging for cosmetics and perfumes, which excludes plastic, paper, and metal formats that make up a large part of total cosmetic packaging demand in MEA. |

Taken together, the comparison suggests the largest gaps come from scope boundaries and base-year selection rather than a single data point. By keeping inputs tied to observable demand signals and by applying pack-format and material level pricing logic that can be rechecked, the sizing approach stays transparent and repeatable when assumptions need to be updated.

Key Questions Answered in the Report

What is the current value of the Middle East and Africa cosmetic packaging market?

The market is valued at USD 1.69 billion in 2026 and is projected to reach USD 2.11 billion by 2031.

Which material dominates cosmetic packaging demand in the region?

Plastic accounts for 61.92% of demand, although bio-degradable options are expanding fastest under circular-economy mandates.

Which country shows the highest growth potential for cosmetic packaging?

South Africa leads with a 6.13% CAGR through 2031, driven by a growing middle class and supportive manufacturing policies.

How are halal requirements influencing packaging?

Brands require certified materials and traceability, leading converters to invest in halal-compliant lines and detailed labeling that verifies ingredient sourcing.

What impact is e-commerce having on packaging design?

Online sales push demand for protective yet visually appealing packs, such as hybrid constructions that withstand shipping stress while offering premium unboxing experiences.

Which product type is gaining traction due to logistics efficiency?

Flexible pouches and sachets are growing at 6.01% CAGR because they reduce shipping weight and meet e-commerce handling needs.

Page last updated on: