United States Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.35 Billion |

| Market Size (2026) | USD 31.27 Billion |

| Market Size (2031) | USD 36.58 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cheese Market Analysis by Mordor Intelligence

The United States cheese market size was valued at USD 28.35 billion in 2025 and is estimated to grow from USD 31.27 billion in 2026 to reach USD 36.58 billion by 2031, at a CAGR of 4.28% during the forecast period (2026-2031). Domestic supply remains a core support for the United States cheese market, with USDA data showing 14.8 billion pounds of cheese production in 2025 across 502 plants, which gives manufacturers room to serve retail and foodservice demand at the same time. Demand conditions also remain broad, as per capita cheese consumption reached 39.2 pounds, or 17.8 kg, in 2024, and dairy guidance released in 2026 continued to support regular cheese intake, including full-fat dairy choices[1]Source: USDA National Agricultural Statistics Service, “Dairy Products 2025 Summary,” USDA, esmis.nal.usda.gov. The United States cheese market is also benefiting from stronger online grocery habits, wider deli engagement, and continued premium demand in specialty formats, which together are expanding the number of purchase occasions across households. Competitive behavior in the United States cheese market is increasingly shaped by format innovation, cold-chain investment, and targeted expansion into premium snacking and Hispanic cheese varieties rather than simple volume growth alone. At the same time, GLP-1 linked dietary shifts and plant-based alternatives are adding pressure to conventional demand patterns, which means the next phase of United States cheese market growth will favor producers that can balance scale, protein positioning, and convenience

Key Report Takeaways

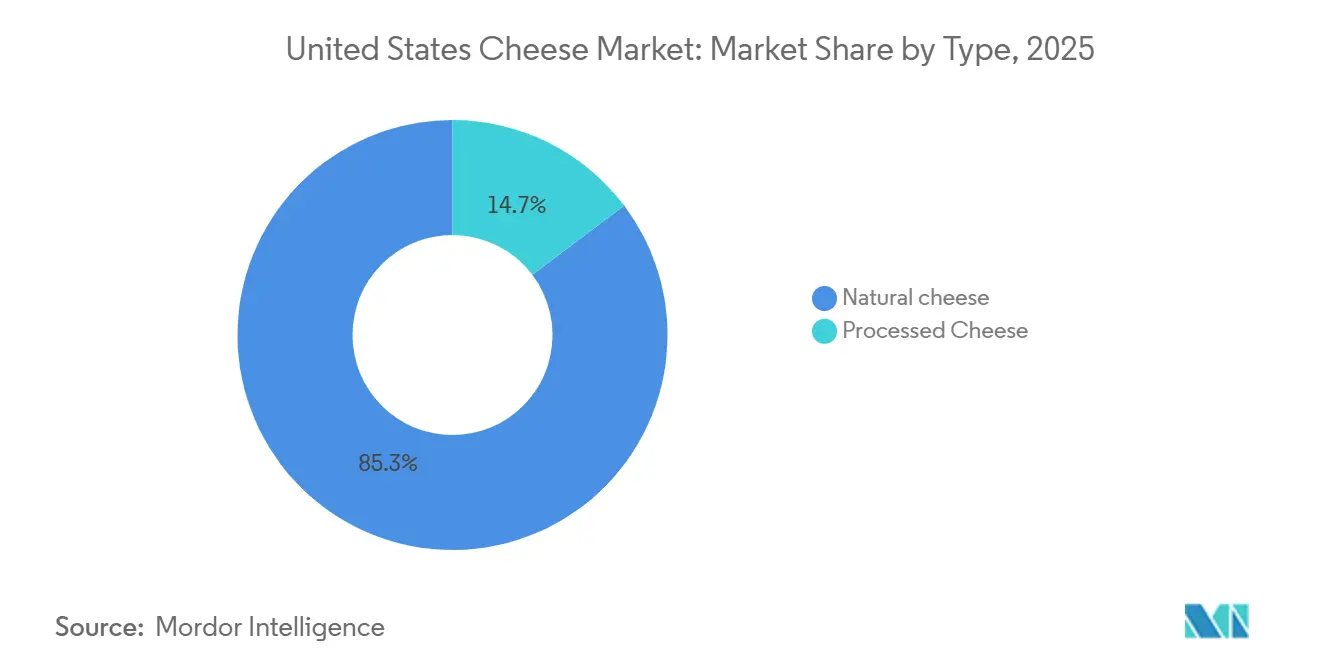

- By type, natural cheese held 85.28% of the United States cheese market share in 2025, while processed cheese is forecast to grow at a 6.25% CAGR through 2031.

- By milk source, cow milk accounted for 45.73% of the United States cheese market size in 2025, while goat milk is projected to expand at a 6.68% CAGR through 2031.

- By format, blocks and wheels represented 46.82% of the United States cheese market size in 2025, while shredded and grated cheese is projected to advance at a 5.85% CAGR through 2031.

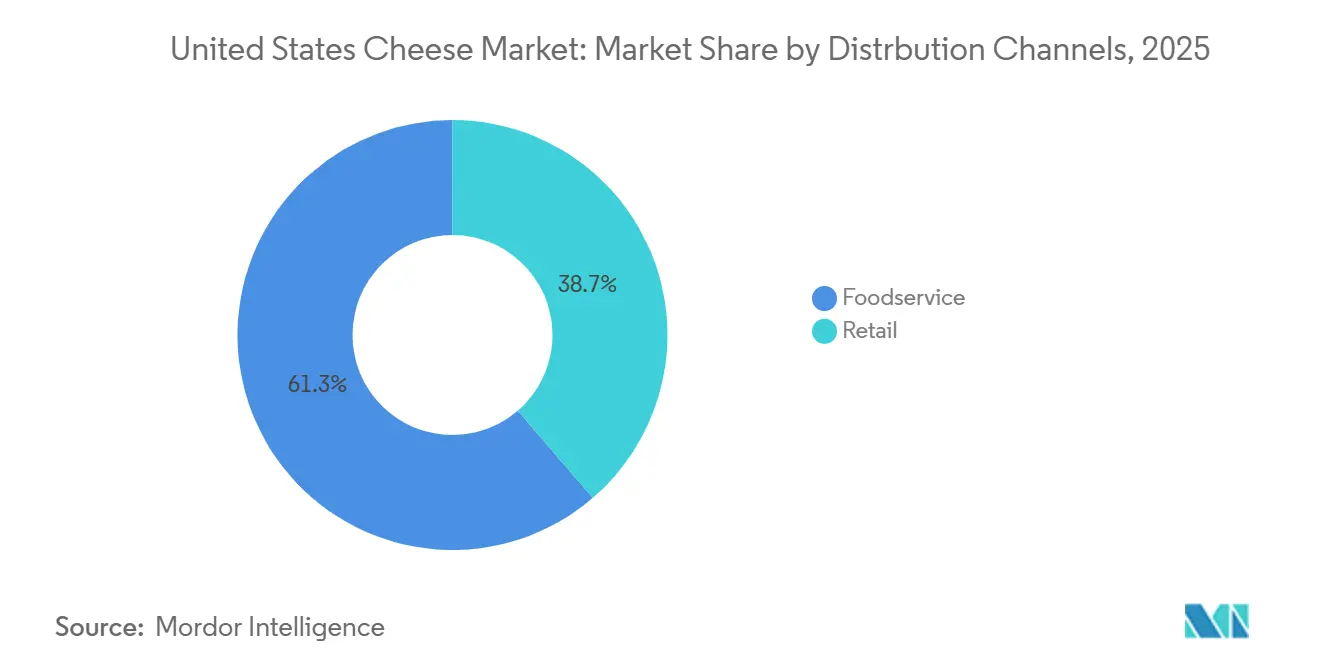

- By distribution channel, supermarkets and hypermarkets captured 38.68% share in 2025, while online retail is forecast to grow at a 6.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Cheese Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Popularity of Specialty and Artisanal Cheeses | +1.2% | National, concentrated in the Northeast, West Coast, and urban centers | Medium term (2-4 years) |

| Growth of Home Cooking and Gourmet Meal Preparation | +0.6% | National, with strongest traction in suburban and Midwest markets | Short term (≤ 2 years) |

| Growing Demand from Pizza and Fast-Food Industries | +1.0% | National, with fastest chain expansion in the Southeast and strong procurement links to the Midwest dairy corridor | Medium term (2-4 years) |

| Product Innovation in New Cheese Formats | +0.9% | National, with online retail and specialty channels widening reach | Medium term (2-4 years) |

| Long Shelf Life and Convenient Single-Serve Formats | +0.4% | National, with especially strong uptake in the South and Midwest convenience retail base | Short term (≤ 2 years) |

| Rising Consumption of Natural and Lactose-Free Cheese | +0.7% | National, with strongest adoption among health-focused consumers on the East and West Coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Popularity of Specialty and Artisanal Cheeses

Specialty and artisanal varieties are changing the revenue mix of the United States cheese market, even when total category volume does not move at the same pace. Deli cheese generated USD 9.1 billion in the 52 weeks ending April 2026, and household buying penetration reached 79.8%, which shows that specialty cheese buying is already broad rather than niche[2]Source: International Dairy Deli Bakery Association, “Trends 2026 From Brie to Brioche,” IDDBA, iddba.org. That scale gives retailers a strong reason to protect shelf space and deli counter presence for premium cheeses. The demand pattern also suggests that consumers are using specialty cheese more often in routine meals, snacks, and entertaining, which supports a better price mix across the United States cheese market. Margin pressure on smaller creameries is still present, so larger cooperatives and processors have a clearer path to add differentiated products through acquisition or brand partnerships.

Growing Demand From Pizza and Fast-Food Industries

Foodservice remains one of the most dependable demand bases for the United States cheese market because pizza chains and quick-service operators buy large volumes of mozzarella and processed blends on a repeat basis. The United States had 75,736 pizzerias in 2025, while Italian-type cheese production reached 6.3 billion pounds and mozzarella alone accounted for 5.0 billion pounds, or 79.1% of Italian-type output. Parmesan production also rose 17.9% in 2025, which shows that restaurant use is extending beyond pizza into pasta, appetizers, and dressings. These procurement patterns give the United States cheese market a stable volume floor that is less exposed to short-term shifts in household sentiment. The same trend is also favoring large processors that can meet product specification, consistency, and logistics requirements across national chain networks.

Product Innovation in New Cheese Formats

Format innovation is becoming one of the clearest competitive tools in the United States cheese market because it expands where and how cheese is consumed without requiring a new core variety. Sargento launched Hot & Spicy Sliced Cheeses and Balanced Breaks Cheese + Crunch Mixes in January 2026, showing how producers are targeting both flavor-led and protein-led demand in the same cycle. Midwest Dairy research also pointed to stronger demand for convenient and flavorful options, especially as meal occasions continue to fragment into snacks and smaller eating occasions. This shift is moving competition away from simple flavor additions and toward packaging, portability, and ready-to-use formats. As online grocery use rises, these new formats can reach consumers faster and gain visibility beyond traditional dairy aisle placement.

Rising Consumption of Natural and Lactose-Free Cheese

Natural cheese remains the core demand base of the United States cheese market because consumers continue to favor simpler ingredient lists and more familiar dairy formats. The 2025-2030 Dietary Guidelines for Americans reaffirmed the role of dairy servings, including full-fat options, which supports the position of natural cheese in everyday diets. Retail demand has also held up well, with natural cheese sales outperforming processed cheese in the user-supplied material for the latest comparable tracking period. Lactose-free cheese is also gaining attention because consumers who want dairy protein are looking for options that reduce digestive concerns without moving away from cheese entirely. Standards of identity and composition remain important in this part of the United States cheese industry because they preserve differentiation between natural cheese and analogue or highly reformulated products.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Competition from Plant-Based Cheese Alternatives | -0.9% | National, with highest penetration in West Coast urban markets and natural grocery channels | Medium term (2-4 years) |

| Lactose Intolerance and Milk Allergies | -0.4% | National, with disproportionate impact across Southeast Asian and Hispanic demographic communities | Short term (≤ 2 years) |

| Emerging Impact of Weight-Loss and Reduced-Calorie Diet Trends | -0.7% | National, with the strongest effect in urban markets with higher GLP-1 prescription rates | Long term (≥ 4 years) |

| Volatility in Milk Prices | -0.5% | Midwest and West, where cooperative members carry the highest input cost exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Competition From Plant-Based Cheese Alternatives

Plant-based cheese alternatives remain small in value terms, but they still create a meaningful competitive challenge for the United States cheese market in premium retail and natural grocery channels. In the most recent full tracking year, plant-based cheese dollar sales fell 10%, and unit sales fell 8%, yet household penetration still stood at 4% and dollar share remained near 1% of the total cheese category. That level does not threaten the full United States cheese market today, but it is large enough to keep shelf space pressure elevated in sliced and shredded formats. Commodity-oriented processors face the greatest exposure because those are the formats where plant-based offerings have advanced the most. The longer-term risk is less about total substitution and more about losing younger, convenience-driven shoppers in channels where discovery and trial happen quickly.

Emerging Impact of Weight-Loss and Reduced-Calorie Diet Trends

GLP-1-related diet changes are creating a more complex demand picture for the United States cheese market because they affect both calorie intake and product choice. Michigan State University identified cheese among the dairy categories seeing lower purchases from GLP-1 users, while the same users are often shifting toward higher-protein dairy formats instead of leaving dairy completely. CDC data showed that 26.5% of U.S. adults with diagnosed diabetes used GLP-1 injectables in 2024, and usage reached 33.3% among adults aged 50 to 64, which matters because this age group has historically been a strong cheese-consuming cohort[3]Source: Centers for Disease Control and Prevention, “Products Data Briefs Number 537,” CDC, cdc.gov. This creates a headwind for calorie-dense cheese formats that are not clearly positioned around protein value or portion control. It also means producers in the United States cheese market will need more precise messaging around nutrition, satiety, and serving size to hold demand within older and health-managed consumer groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Cheese's Premium Pull Reshapes Category Margins

Natural cheese held 85.28% of the United States cheese market share in 2025, which shows how strongly the category aligns with demand for simpler and more familiar dairy products. Mozzarella remained the largest production variety within natural cheese, with 5.0 billion pounds of output in 2025, and this kept Italian styles central to the United States cheese market across both retail and foodservice. Parmesan production rose 17.9% in 2025, which points to broader menu use and stronger household cooking demand beyond pizza alone. Natural cheese also benefits from stronger premium positioning, which helps branded and specialty players defend price even as private label gains share in mainstream supermarket shelves.

Feta, ricotta, cream cheese, and other everyday natural varieties continue to widen the category base because they serve cooking, snacking, and deli use at the same time. The United States cheese industry is also seeing higher value concentration in natural cheese because consumers are more willing to trade up on provenance, texture, and perceived freshness than they are in more processed formats. Processed cheese still remains important, and it is forecast to grow at a 6.25% CAGR through 2031, making it the fastest-growing type segment in the user supplied draft. That growth is being supported by reformulation, especially products that preserve melt performance while moving closer to natural ingredient expectations, as shown by Sargento's January 2026 launch activity.

By Milk Source: Goat Milk Gains as Specialty Channels Scale

Cow milk accounted for 45.73% of the United States cheese market size in 2025, and it remains the foundation of large-scale cheddar, mozzarella, and American cheese production. That leadership rests on the processing base in Wisconsin and California, which continues to anchor the highest output volumes in the country. Buffalo milk holds a meaningful niche in Italian-style specialties, with California's processing network supporting domestic supply for mozzarella di bufala-style applications and related premium offerings. The structure of this segment still favors cow milk because the United States cheese market depends on scale, consistent milk availability, and established procurement systems.

Goat milk is projected to grow at a 6.68% CAGR through 2031, making it the fastest-growing milk source in the user-supplied draft. Growth is tied to specialty grocers, farm-to-table menus, and direct-to-consumer channels that give smaller premium products a wider audience. Vermont Creamery, part of the Land O'Lakes portfolio, remains a relevant example because it shows how branded goat cheese can scale through authenticity and regional identity. The United States cheese industry is likely to see goat milk remain supply constrained relative to demand, which supports premium pricing but also limits how fast this segment can move into wider mass-market distribution.

By Format: Shredded and Grated Cheese' Operational Pull in Foodservice

Blocks and wheels represented 46.82% of the United States cheese market size in 2025, which reflects their role as the main upstream format for restaurants, manufacturers, and household cooking. This format stays dominant because much of the cheese sold in the United States cheese market is later sliced, shredded, melted, or portioned further downstream. Blocks also give buyers flexibility across foodservice and retail applications, so they remain the default format for procurement efficiency. Their position is especially strong in mozzarella, cheddar, and food manufacturing supply chains where uniformity matters more than direct shelf presentation.

Shredded and grated cheese is forecast to grow at a 5.85% CAGR through 2031, making it the fastest-growing format because it removes preparation steps for both restaurants and households. Pizza and flatbread use remains a major demand engine, and that keeps shredded mozzarella central to this segment's growth pattern. Slices continue to hold an important place in convenience-led retail, while spreads, cubes, and sticks are gaining from protein snacking and deli applications. The broader format direction of the United States cheese market points to more pre-portioned, ready-to-use, and single-serve products, which supports higher value capture per pound sold.

By Distribution Channel: Retail channels and gaining momentum

Retail accounted for 38.68% of the United States cheese market share in 2025, making it the largest distribution channel in the category. Its lead reflects the scale of supermarkets, hypermarkets, convenience stores, specialty retailers, and online grocery platforms that keep cheese tied to routine household purchases. Deli counters remained especially important within retail, generating USD 9.1 billion in cheese sales in the 52 weeks ending April 2026, with 79.8% household buying penetration, which shows how strongly in-store discovery supports premium and everyday cheese demand IDDBA. Retail also benefits from private label expansion, broader shelf variety, and better placement of natural, snack-sized, and specialty cheeses across multiple price points. The rise of digital grocery adds another layer of support, as U.S. retail e-commerce sales reached USD 326.7 billion in the first quarter of 2026, up 9.8% from the first quarter of 2025, helping retailers extend cold-chain access and repeat purchasing beyond physical store catchments.

Foodservice is projected to grow at a 6.42% CAGR through 2031, making it the fastest-growing distribution channel in the United States cheese market. This growth is tied to steady expansion in pizza chains, quick-service restaurants, and casual dining formats that rely on mozzarella, processed blends, parmesan, and other cooking-oriented cheese types in high volumes. Procurement in this channel is also becoming more direct, with large distributors and restaurant operators favoring processor relationships that can deliver consistent quality, specification control, and dependable supply at scale. That pattern supports larger manufacturers, especially in the Midwest and West, where production depth and logistics networks are already closely aligned with foodservice demand. As restaurant menus continue to widen across pizza, sandwiches, breakfast items, appetizers, and Hispanic offerings, foodservice is likely to remain the most expansion-oriented route for volume growth in the United States cheese market.

Geography Analysis

The Central region, which aligns with the Midwest in USDA production data, remained the leading production base of the United States cheese market in 2025 with 7.5 billion pounds, equal to 50.7% of national output. Wisconsin alone produced 3.6 billion pounds in 2025, or 24.6% of the U.S. total, which kept it as the clear production anchor for the United States cheese market. Minnesota added 841.9 million pounds, and Iowa contributed 385.6 million pounds, which shows how deeply production is clustered across the broader Midwest corridor. March 2026 data also showed Central region production rising 6.5% year on year, the strongest regional growth rate in the country. This concentration gives the region a durable role in cost-efficient supply, contract manufacturing, and large national foodservice procurement.

The Western region contributed 5.6 billion pounds in 2025, or close to 38% of national output, led by California with 2.5 billion pounds and Idaho with 1.0 billion pounds. California remains especially important for Italian-type cheese, with mozzarella output reaching 1.6 billion pounds in 2025, which supports pizza chain demand across several downstream markets. The South remains the largest consumption zone in the United States cheese market because of its population scale, quick-service restaurant footprint, and growing demand for Hispanic cheese varieties. Bel Group's March 2026 ground-breaking in South Dakota also reinforces how the Central to South supply corridor is being used to scale portion-controlled dairy snacks for large consumer markets. Taken together, the West and South combination keeps volume demand and processing logistics tightly linked across the United States cheese market.

The Atlantic region produced 1.7 billion pounds in 2025, equal to 11.3% of national output, which made it the smallest production base by volume. New York produced 892.6 million pounds and Pennsylvania added 463.7 million pounds, while Vermont remained influential in goat cheese and specialty aged categories through branded premium offerings. Atlantic region production rose 4.7% in March 2026 from March 2025, which shows that premium and artisan-oriented supply is still expanding in the Northeast. The Northeast also holds a strong position in imported and specialty distribution, so it continues to shape premium pricing and online specialty demand within the United States cheese market.

Competitive Landscape

The United States cheese market remains consolidated, with a limited group of large cooperatives and processors shaping production scale, channel access, and national brand presence. Dairy Farmers of America, Kraft Heinz, Saputo, Leprino Foods, and other large manufacturers anchor the competitive structure through broad product portfolios and established processing footprints. Leprino Foods continues to stand out in mozzarella because the United States cheese market still depends heavily on pizza-linked demand and high-volume foodservice supply chains. This structure gives large firms a clear advantage in contract fulfillment, cold-chain logistics, and product consistency across national accounts. At the same time, category growth is no longer being won by scale alone, because brands also need sharper positioning in premium snacking, natural ingredients, and specialty formats.

Strategic investment activity shows how leading players are adapting to that shift. Bel Group broke ground in March 2026 on a USD 200 million Babybel expansion in South Dakota, doubling annual output and deepening its focus on portion-controlled cheese snacks. Sargento expanded its innovation agenda in January 2026 with new sliced cheeses and snack mixes, and its March 2026 recognition for innovation reinforced how product architecture is becoming a competitive tool in the United States cheese market. Saputo's February 2026 agreement to divest an 80% stake in its Argentina Dairy Division also points to portfolio reshaping that can support future North American priorities. These moves show that the United States cheese market is increasingly defined by targeted capital deployment rather than broad expansion across every product line.

Private label is also gaining weight in natural cheese, which raises pressure on branded players that do not offer a strong story around flavor, origin, or convenience. That makes specialty and artisan positioning more important, even in a market where large-scale production still dominates total volume. Cooperative and branded firms that can combine reliable milk sourcing with differentiated end products are better placed to protect margins. Overall, the United States cheese market is concentrated but still open to niche growth at the premium edge, especially where format, snacking, and regional identity matter.

United States Cheese Industry Leaders

The Kraft Heinz Company

Dairy Farmers of America

Saputo Inc.

Land O’Lakes, Inc.

Lactalis USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kraft Natural Cheese, a brand under Lactalis Heritage Dairy, expanded its product portfolio with the launch of a new Lactose-Free Cheese Line, catering to the growing demand for digestive-friendly dairy products. The range includes Lactose-Free Mild Cheddar Shredded Cheese, Lactose-Free Mozzarella Shredded Cheese, and Lactose-Free Mozzarella String Cheese.

- November 2025: Sargento launched Natural American Cheese, a breakthrough product developed after more than a decade of research and development to replicate the taste, texture, and meltability of traditional American cheese using only five natural ingredients.

- March 2025: Sargento introduced three major product innovations, including Sargento Natural American Cheese, a first-of-its-kind sliced American cheese made from 100% natural cheese with only five ingredients.

United States Cheese Market Report Scope

| Natural Cheese | Mozzarella |

| Feta | |

| Ricotta | |

| Cottage | |

| Cream | |

| Parmesan | |

| Others | |

| Processed Cheese |

| Cow |

| Buffalo |

| Others |

| Blocks/Wheels |

| Slices |

| Shredded and Grated |

| Spreads |

| Cubes and Sticks |

| Others |

| Foodservice (HoReCa) | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Specialist Retailers | |

| Online Retail | |

| Others |

| By Type | Natural Cheese | Mozzarella |

| Feta | ||

| Ricotta | ||

| Cottage | ||

| Cream | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| By Milk Source | Cow | |

| Buffalo | ||

| Others | ||

| By Format | Blocks/Wheels | |

| Slices | ||

| Shredded and Grated | ||

| Spreads | ||

| Cubes and Sticks | ||

| Others | ||

| By Distribution Channel | Foodservice (HoReCa) | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail | ||

| Others | ||

Key Questions Answered in the Report

What is the current size of the United States cheese market?

The United States cheese market stood at USD 31.27 billion in 2026 and is forecast to reach USD 36.58 billion by 2031 at a 4.28% CAGR.

Which cheese type leads demand in the United States?

Natural cheese leads the category, holding 85.28% share in 2025, supported by strong demand for simpler ingredients and broad use across retail and foodservice.

Why is foodservice so important for cheese producers in the United States?

Pizza and quick-service restaurants provide stable volume demand, with mozzarella output reaching 5.0 billion pounds in 2025 and pizzeria count staying very high.

What are the main risks affecting future cheese demand in the United States?

The main risks are GLP-1 related dietary changes, plant-based alternatives in sliced and shredded formats, and input cost pressure tied to milk price volatility.

Page last updated on: