Cheese Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

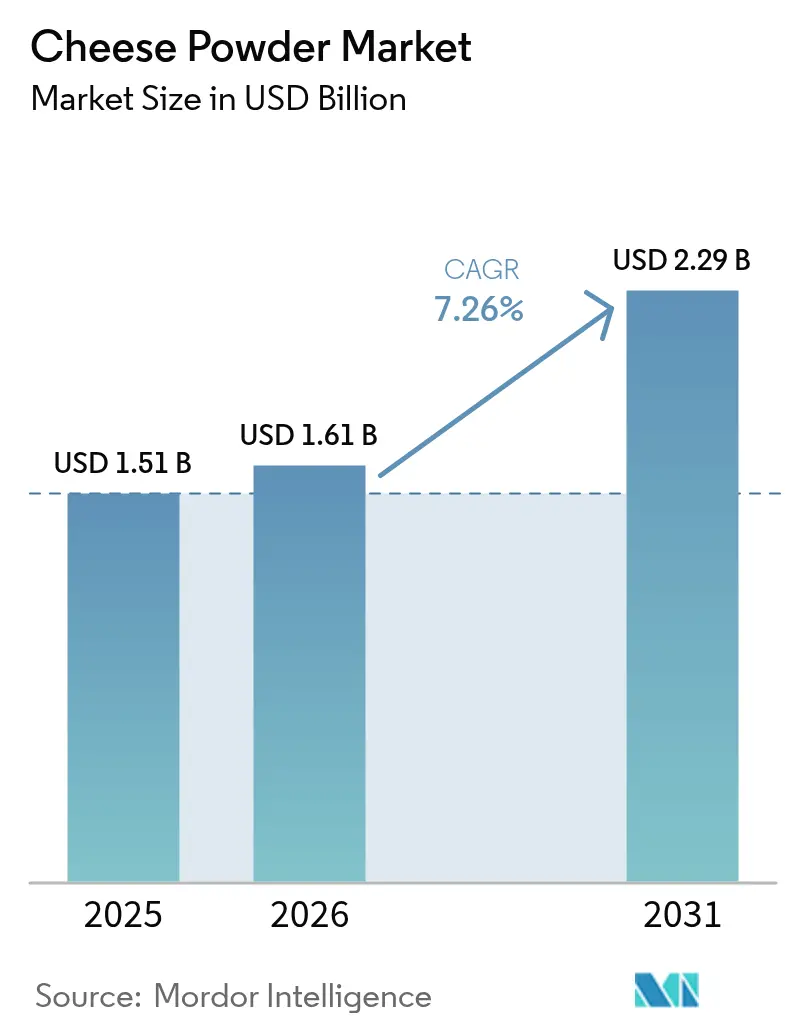

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cheese Powder Market Analysis by Mordor Intelligence

The cheese powder market size was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.61 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). Demand is climbing as manufacturers balance volatile dairy prices with shelf-stable, flavor-intense ingredients, while foodservice chains adopt powder formats to lower labor and refrigeration costs. North America retained leadership thanks to decades-old snack-seasoning infrastructure, yet capacity additions in Asia-Pacific will accelerate regional uptake as multinational quick-service restaurants enter secondary cities. Technology breakthroughs in electrostatic and pulse spray-drying safeguard delicate sulfur volatiles, broadening premium applications such as aged-parmesan and blue-cheese powders. Meanwhile, clean-label reformulations that replace artificial colors with natural annatto and enzyme-modified bases cater to health-conscious consumers and support sustained value growth.

Key Report Takeaways

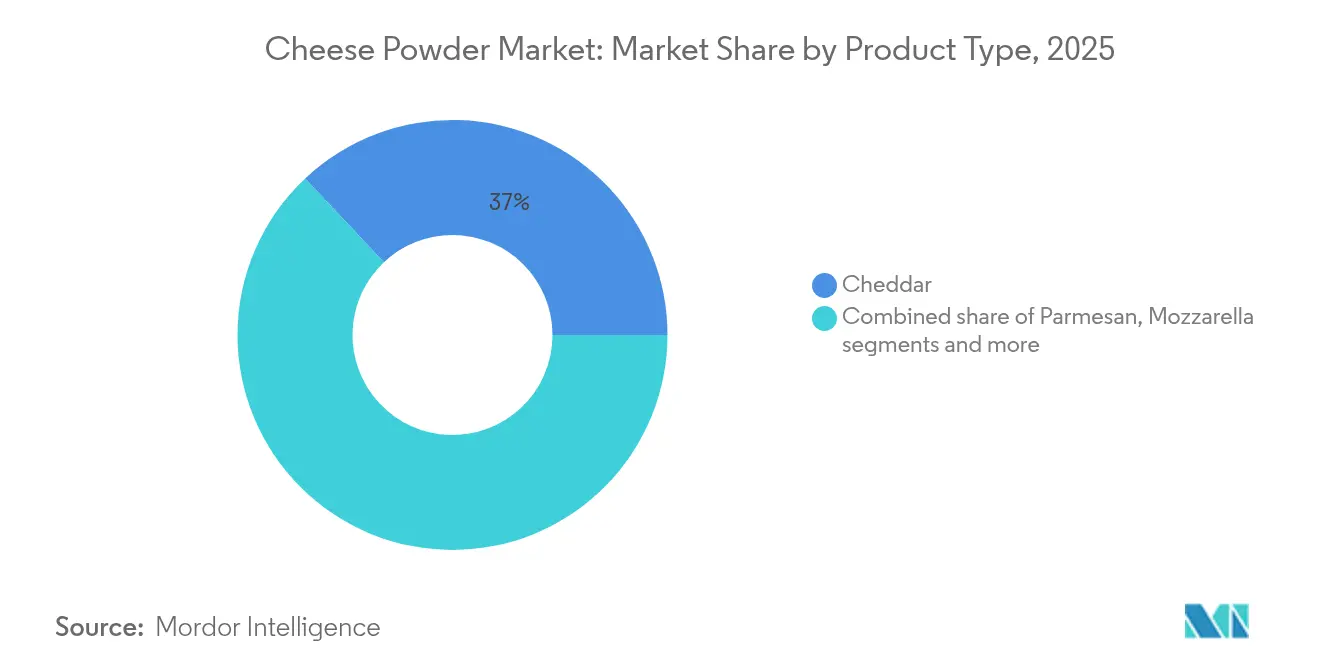

- By product type, cheddar led with 37.08% of the cheese powder market share in 2025, whereas mozzarella is projected to post the fastest 9.89% CAGR to 2031.

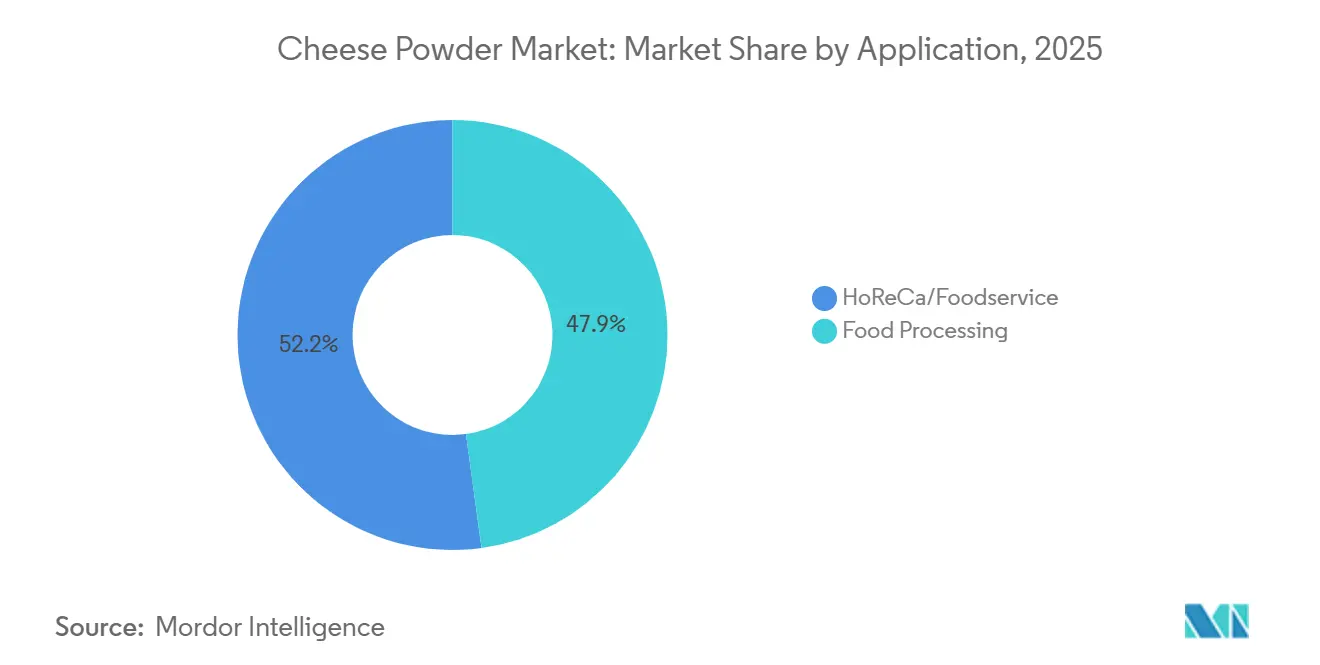

- By application, HoReCa/Foodservice captured 52.15% revenue share of the cheese powder market in 2025; whereas, food processing is forecast to expand at a 7.84% CAGR through 2031.

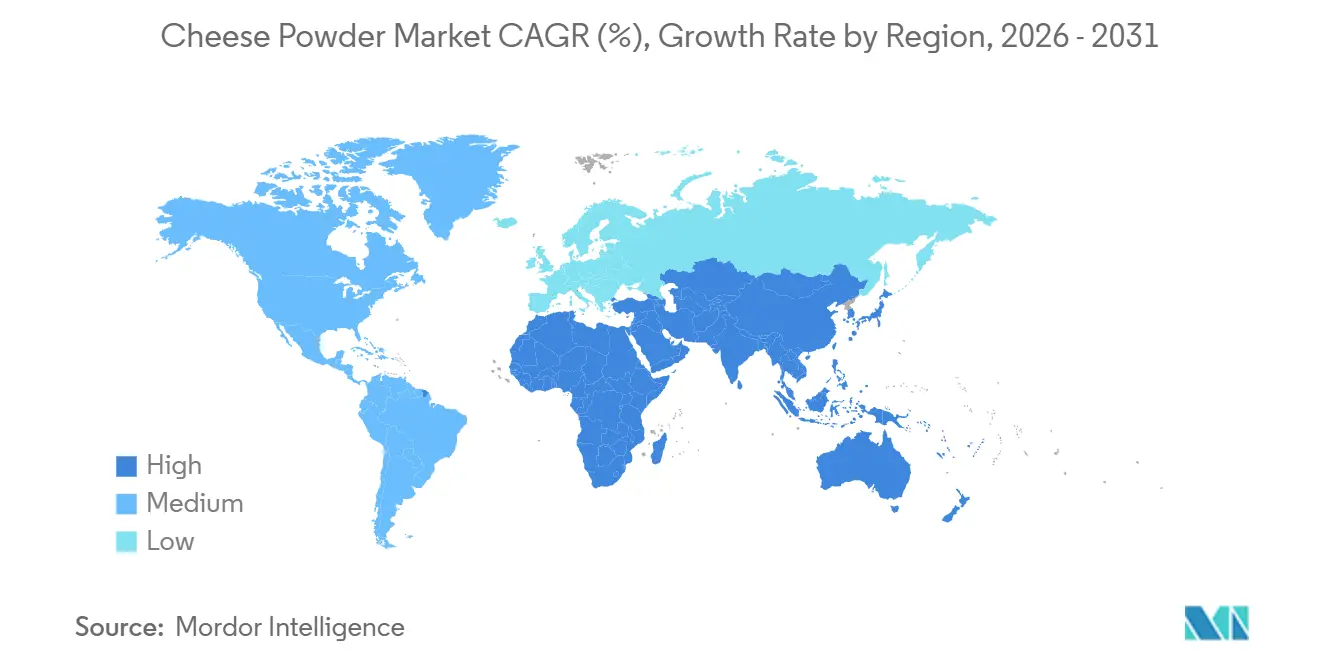

- By geography, North America held 36.24% of sales in 2025, while Asia-Pacific is set to climb at a 8.91% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cheese Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience foods and snacks | +1.8% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of foodservice and HoReCa industry use | +1.5% | Asia-Pacific core, spill-over to Middle East and South America | Medium term (2-4 years) |

| Long shelf life and easy storage benefits | +0.9% | Global, particularly emerging markets with fragmented cold-chain infrastructure | Long term (≥ 4 years) |

| Technological advances in drying and flavor retention | +1.2% | North America and Europe, with technology transfer to Asia-Pacific | Long term (≥ 4 years) |

| Clean-label and natural formulation trends | +1.0% | North America and Europe, early adoption in urban Asia-Pacific | Short term (≤ 2 years) |

| Growing adoption in sauces, dips, and bakery applications | +0.8% | Global, led by North America and Europe bakery sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience foods and snacks

Rising demand for convenience foods and snacks is a significant driver of the cheese powder market, as manufacturers increasingly incorporate cheese powders into ready-to-eat meals, savory snacks, sauces, and seasoning blends to enhance flavor, texture, and nutritional appeal. Cheese powder offers a versatile, shelf-stable, and easy-to-use ingredient that allows snack producers to deliver consistent taste and creamy profiles without relying on fresh cheese, supporting mass production and extended shelf life. According to the 2024 IFIC Food & Health Survey, nearly three in four Americans snack at least once a day, with 73% consuming snacks daily and 14% snacking three or more times per day, highlighting the growing consumer preference for convenient, flavorful, and on-the-go food options[1]Source: Food Insight, "2024 IFIC Food & Health Survey", foodinsight.org. This trend encourages manufacturers to innovate with cheese-flavored chips, popcorn, seasoning mixes, and meal kits, further increasing demand for powdered cheese ingredients.

Expansion of foodservice and HoReCa industry use

The expansion of the foodservice and HoReCa (Hotels, Restaurants, and Catering) industry is a key driver of the cheese powder market, as these sectors increasingly rely on versatile, shelf-stable ingredients to streamline kitchen operations and ensure consistent product quality. Cheese powders provide a convenient and cost-effective alternative to fresh cheese, enabling chefs and foodservice operators to create a wide range of menu items, including sauces, soups, baked goods, and snack toppings, without the challenges of refrigeration or rapid spoilage. The growing number of quick-service restaurants, casual dining chains, and catering services has intensified demand for ingredients that are easy to store, measure, and integrate into high-volume production. Additionally, the adoption of standardized recipes and portion-controlled preparations in the HoReCa segment further reinforces the need for powdered cheese to maintain flavor consistency across outlets.

Long shelf life and easy storage benefits

Long shelf life and easy storage are important drivers of the cheese powder market, as these characteristics make it a highly convenient ingredient for both food manufacturers and end-users. Unlike fresh cheese, cheese powder does not require refrigeration, reducing storage costs and simplifying logistics across production, distribution, and retail channels. Its extended shelf stability allows manufacturers to produce, transport, and store large quantities without the risk of spoilage, supporting consistent supply for year-round demand. The powder form also enables precise portioning and easy integration into sauces, snacks, seasonings, and ready-to-eat meals, improving operational efficiency in both industrial and foodservice applications. These benefits are particularly valuable for markets with limited cold-chain infrastructure or for small-scale producers seeking cost-effective ingredient solutions.

Clean-label and natural formulation trends

Clean-label and natural formulation trends are driving growth in the cheese powder market, as consumers increasingly demand products with transparent, minimally processed, and recognizable ingredients. Manufacturers are responding by developing cheese powders that avoid artificial flavors, colors, and preservatives while maintaining taste and functionality in a variety of applications such as snacks, sauces, and ready-to-eat meals. According to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, up from 52% in 2021, reflecting the strong shift toward natural and trustworthy product formulations[2]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," cbi.eu. This trend encourages the use of dairy-derived or plant-based cheese powders that align with consumer expectations for authenticity and simplicity. Clean-label positioning not only strengthens brand credibility but also supports marketing claims related to health, wellness, and sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile dairy raw material prices | -1.2% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Health concerns related to sodium and fat content | -0.7% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Stringent food safety and regulatory compliance | -0.5% | Global, with heightened enforcement in EU and India | Long term (≥ 4 years) |

| Supply chain disruptions and raw material shortages | -0.8% | Global, concentrated in Southern Hemisphere export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile dairy raw material prices

Volatile dairy raw material prices represent a significant restraint on the cheese powder market, as the cost of production is closely tied to commodities such as milk, whey, and cheese curds, which are highly susceptible to seasonal fluctuations, weather events, and changes in trade policy. These price swings directly impact manufacturers’ margins, especially for large-scale production of powdered cheese used in snacks, sauces, and ready-to-eat meals. USDA data showed U.S. cheddar-block prices averaging USD 1.85 per pound in early 2025, up from USD 1.62 in 2024, driven by tighter milk supplies resulting from dairy-farm consolidation and a reduced national herd count[3]Source: United States Department of Agriculture, “PUTTING AMERICAN FARMERS FIRST”, usda.gov. Such volatility can lead to increased product costs for both foodservice operators and retail brands, potentially affecting pricing strategies and product accessibility. Manufacturers must frequently adjust procurement plans, hedge against market fluctuations, or explore alternative suppliers to maintain stable production.

Health concerns related to sodium and fat content

Health concerns related to sodium and fat content pose a notable restraint on the cheese powder market, as consumers and regulatory authorities increasingly scrutinize processed foods for nutritional quality. Cheese powders, particularly those derived from full-fat cheeses, can contain elevated levels of saturated fat and sodium, which are associated with cardiovascular risks and other diet-related health issues. Growing awareness about obesity, hypertension, and heart disease has prompted consumers to limit intake of high-sodium and high-fat products, affecting demand for traditional cheese-flavored ingredients. Food manufacturers are therefore under pressure to reformulate products with reduced-fat or low-sodium alternatives, which may alter taste, texture, and functionality in applications such as snacks, sauces, and ready-to-eat meals. These concerns can slow market growth, as producers balance consumer expectations for flavor with the need to comply with health-conscious trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cheddar Dominance Anchored in Snack Infrastructure

Cheddar accounted for 37.08% of the global cheese powder market share in 2025, establishing itself as the dominant segment within the category. Its leading position is primarily driven by widespread consumer familiarity and strong preference across both retail and foodservice channels. Cheddar cheese powder is extensively used in snack seasonings, ready-to-eat meals, bakery products, sauces, and convenience foods due to its sharp flavor profile and versatile functionality. The segment benefits from strong demand in processed and packaged food applications, particularly in flavored chips, popcorn, pasta mixes, and instant meal kits. Additionally, manufacturers favor cheddar powder for its consistent taste, stable shelf life, and compatibility with large-scale production processes.

Mozzarella cheese powder is projected to expand at a CAGR of 9.89% through 2031, making it the fastest-growing segment in the market. This accelerated growth is largely attributed to the increasing global popularity of Italian-style cuisine, particularly pizza, pasta, and baked dishes. The rising demand for convenience foods that replicate authentic mozzarella flavor in powdered form is further supporting segment expansion. Mozzarella powder is increasingly being incorporated into ready-to-cook mixes, seasoning blends, and snack coatings to meet evolving consumer taste preferences. Moreover, rapid urbanization and changing dietary habits in emerging economies are driving higher consumption of Western-style food products, which often feature mozzarella-based flavors.

By Application: Food Processing Gains on HoReCa Leadership

The HoReCa channel generated 52.15% of the cheese powder market revenue in 2025, driven by high-volume purchases from quick-service restaurants and institutional caterers. These businesses value cheese powder for its storage stability and ability to maintain consistent menu quality. The ingredient helps streamline kitchen operations, reduce waste, and maintain uniform taste across multiple locations. However, the segment's growth is moderating due to fluctuations in consumer foot traffic during economic cycles.

The food processing segment is expected to grow at a 7.84% CAGR, surpassing HoReCa's growth rate. This growth is driven by increasing demand for frozen entrées, soups, sauces, and shelf-ready meal kits, particularly among remote workers. The trend reflects a growing consumer preference for convenient, protein-rich packaged foods in middle-income households. Small and medium processors incorporate cheese powder in regional seasonings and instant noodles, benefiting from reduced product development cycles. The bakery sector utilizes the ingredient's heat stability to add cheddar or parmesan flavors to biscuits while maintaining product texture. Ready-meal manufacturers combine mozzarella powder with air-dried basil to create premium products with authentic pizza flavors. Plant-based food manufacturers use cheese powder with vegetable ingredients to appeal to flexitarian consumers. This shift would significantly reshape the cheese powder market landscape.

Geography Analysis

North America dominated the global cheese powder market in 2025, accounting for 36.24% of the total market share. The region’s leadership position is supported by strong consumption of processed and convenience foods, particularly in the United States and Canada. High demand for flavored snacks, ready-to-eat meals, and packaged food products continues to drive substantial usage of cheese powder across multiple applications. The presence of well-established food processing industries and advanced distribution networks further strengthens regional market penetration. Additionally, consumers in North America exhibit a strong preference for cheese-based flavors, particularly cheddar and specialty blends, which boosts product innovation and portfolio expansion.

Asia-Pacific is projected to register the fastest growth in the cheese powder market, expanding at a CAGR of 8.91% through 2031. The region’s growth is primarily driven by rapid urbanization, rising disposable incomes, and increasing adoption of Western dietary habits. Expanding quick-service restaurant chains and growing consumption of bakery, snack, and convenience food products are significantly contributing to demand. Countries such as China, India, Japan, and Southeast Asian nations are witnessing rising popularity of cheese-flavored snacks and ready-to-cook meals. Additionally, the increasing penetration of modern retail formats and e-commerce platforms is improving product accessibility across urban and semi-urban areas.

Europe represents a mature yet steadily expanding market for cheese powder, supported by strong dairy production capabilities and established consumer preference for cheese-based products. The region benefits from a well-developed food processing sector and consistent demand from bakery, snack, and ready meal segments. South America is experiencing gradual growth, driven by expanding urban populations and increasing consumption of processed foods in countries such as Brazil and Argentina. Meanwhile, the Middle East & Africa region is emerging as a promising market due to rising disposable incomes, growing young populations, and expanding retail infrastructure. Increasing adoption of convenience foods and Western-style fast food chains is contributing to higher demand for cheese powder products in these regions.

Competitive Landscape

The cheese powder market is moderately fragmented. Global dairy giants, including Fonterra, Kerry Group plc, and Lactosan A/S, adopt vertical integration strategies, overseeing everything from milk collection to the production of finished powder. This approach helps them manage cost fluctuations and ensure traceability. While the capital-intensive nature of spray-drying equipment poses entry barriers, medium-sized regional firms carve out niches with specialized offerings, such as provenance-based flavors and religious certifications. Technological competition in the industry centers on innovations like microencapsulation for aroma retention, sodium reduction, and energy-efficient drying systems that cut emissions and operational costs.

Recent strategic moves underscore the competitive landscape and capability enhancements within the industry. In December 2024, Fonterra bolstered its ingredients operations with a USD 150 million investment in warehouse facilities, adding a 26,000-tonne cheese storage capacity. In 2024, Leprino Foods teamed up with Fooditive to pioneer precision-fermented casein, targeting a reduction in dairy farming emissions and broadening protein sourcing avenues. Responding to the EU's carbon pricing regulations, which heighten the race for energy efficiency, companies are channeling investments into heat-pump dryers and solar-integrated evaporators.

Small-scale producers are innovating with enzyme-modified powders for a richer umami flavor and crafting low-fat alternatives. In the U.S., regional cooperatives have banded together to form Integrated Dairy Ingredients, collectively marketing rbST-free specialty powders. These maneuvers are reshaping the competitive dynamics of the cheese powder market. Companies eyeing opportunities in the burgeoning snack and ready-meal sectors recognize that success hinges on technical prowess, a secure supply chain, and strict regulatory adherence.

Cheese Powder Industry Leaders

-

Lactosan A/S

-

Land O’Lakes Inc.

-

Kerry Group PLC

-

Fonterra Co-operative Group Limited

-

Royal FrieslandCampina N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Daiya Foods expanded its product portfolio with the launch of two spicy dairy-free cheese innovations Chipotle Cheddar Shreds and Pepper Jack Slices made with its proprietary Oat Cream™ blend and now available in North American retail outlets to meet growing consumer demand for bold, plant-based options.

- April 2024: Butter Buds Inc. launched its Cheese Buds Simple Cheddar Cheese Concentrate, a new powdered ingredient designed to deliver rich cheddar flavour at very low inclusion levels while supporting cleaner labels for food manufacturers and simplifying ingredient declarations.

- April 2024: Food scientists at the University of Copenhagen, in collaboration with Lactosan A/S, investigated cheese powder's ability to enhance umami flavor and kokumi (mouthfeel) in plant-based dishes. The research examined the umami and kokumi characteristics of selected mature Danish cheeses and cheese powder to drive plant-based food consumption.

Global Cheese Powder Market Report Scope

Cheese powder is a dehydrated form of cheese processed into a fine, powdered texture. It is commonly used as a flavoring agent and ingredient in various food products, including snacks, sauces, seasonings, and baked goods. The scope of the study covers the type of cheese powder and its application in the food processing industry and food service sector. The cheese powder market is segmented by product type, application, and geography. By product type, the market is segmented into cheddar, parmesan, mozzarella, and other product types. By application, the market is segmented into bakery and confectionery, sweet and savory snacks, sauces, dressings, dips and condiments, ready meals, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).

| Cheddar |

| Parmesan |

| Mozzarella |

| Blue Cheese |

| Other Types |

| Food Processing | Bakery and Confectionery |

| Dairy | |

| Soups, Sauces and Condiments | |

| Ready Meals | |

| Other Applications | |

| HoReCa/Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Cheddar | |

| Parmesan | ||

| Mozzarella | ||

| Blue Cheese | ||

| Other Types | ||

| By Application | Food Processing | Bakery and Confectionery |

| Dairy | ||

| Soups, Sauces and Condiments | ||

| Ready Meals | ||

| Other Applications | ||

| HoReCa/Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the cheese powder market?

The market is valued at USD 1.61 billion in 2026 and is projected to reach USD 2.29 billion by 2031, reflecting a 7.26% CAGR.

Which cheese type dominates sales?

Cheddar powder leads with a 37.08% cheese powder market share in 2025, benefiting from established demand in North America and Europe.

Why is mozzarella powder growing faster than other varieties?

Global pizza consumption and broader Italian-cuisine adoption push mozzarella powder to a 9.89% CAGR through 2031 within the cheese powder market.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to post a 8.91% CAGR, driven by urbanization, higher disposable income, and rapid QSR expansion.

Page last updated on: