Cream Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

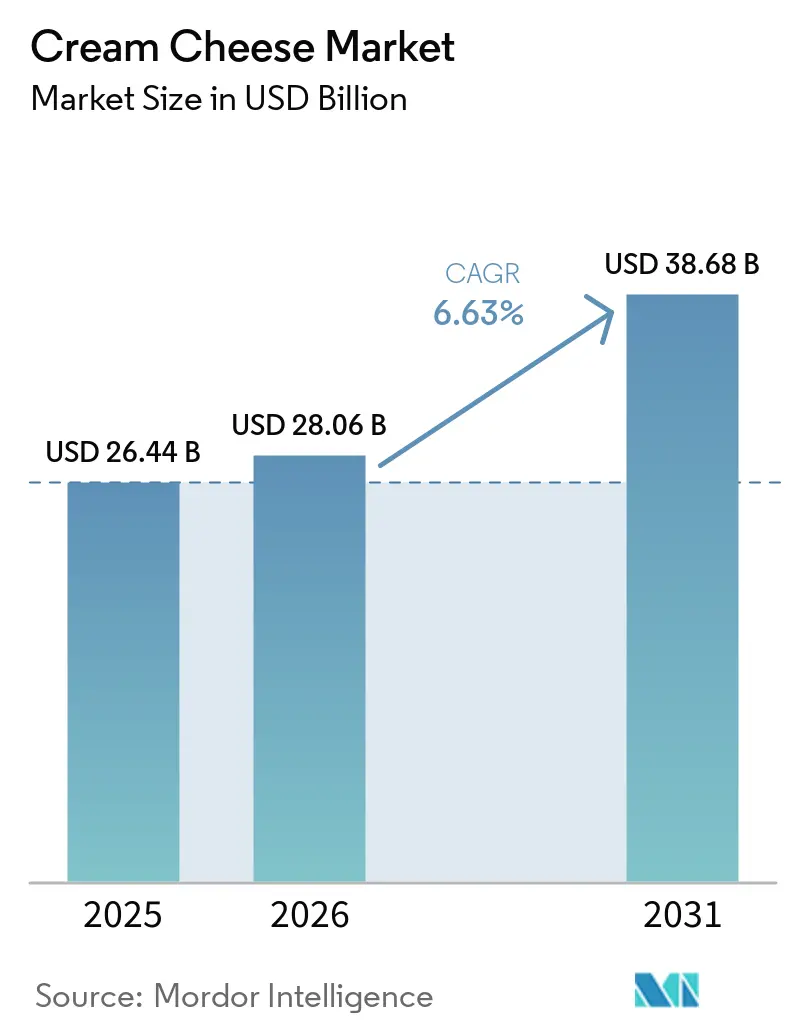

| Market Size (2026) | USD 28.06 Billion |

| Market Size (2031) | USD 38.68 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cream Cheese Market Analysis by Mordor Intelligence

The global cream cheese market was valued at USD 26.44 billion in 2025, reached USD 28.06 billion in 2026, and is projected to attain USD 38.68 billion by 2031, growing at a CAGR of 6.63% during the forecast period. This growth is primarily attributed to shifting consumer preferences toward indulgent, creamy, and premium dairy-based foods that offer both convenience and rich sensory appeal. The rising demand for versatile dairy products with smooth texture, spreadability, and adaptable flavors is driving market expansion across both household and commercial consumption. Consumers increasingly prioritize foods that provide comfort, authenticity, and enhanced eating experiences, positioning cream cheese as a preferred choice in modern dietary habits. Additionally, the market benefits from ongoing innovations in product formulations, flavor development, and texture enhancement technologies, which enhance product quality, shelf life, and overall consumer appeal.

Key Report Takeaways

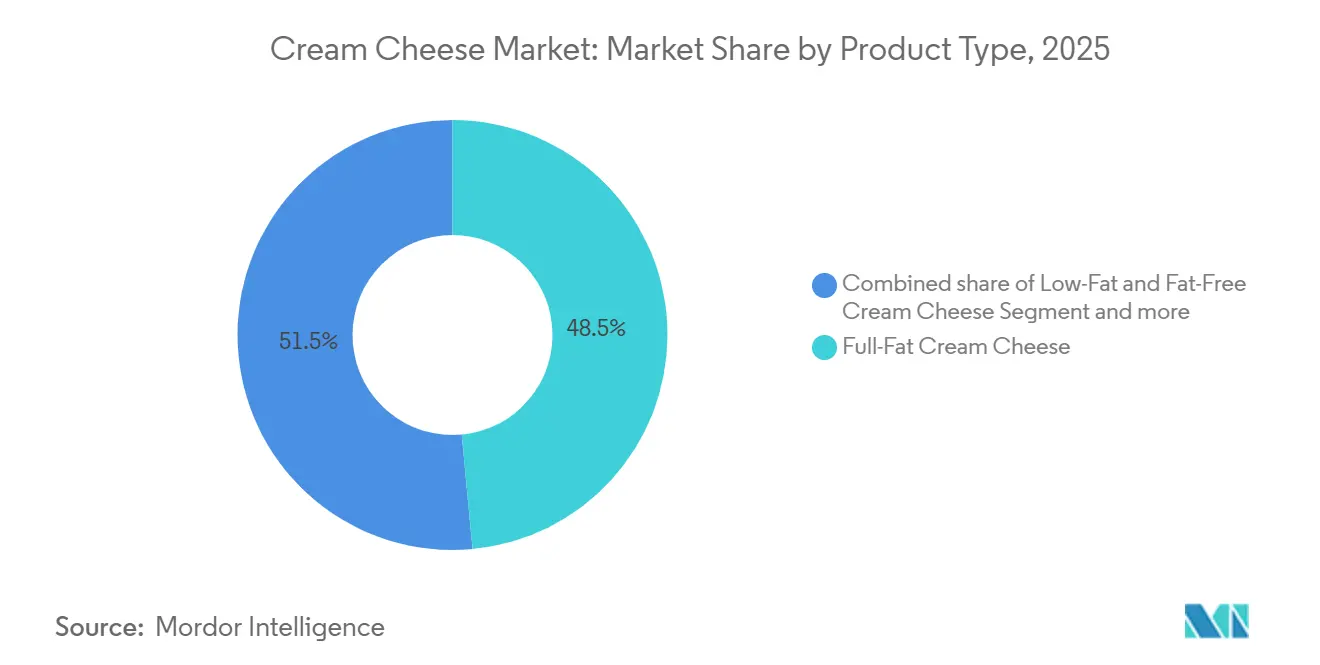

- By product type, Full-Fat Cream Cheese led with a 48.52% share in 2025, while Low-Fat and Fat-Free is projected to grow at a 6.71% CAGR through 2031.

- By source, Dairy held 87.21% share in 2025, while Dairy-Free is forecast to expand at a 7.89% CAGR through 2031.

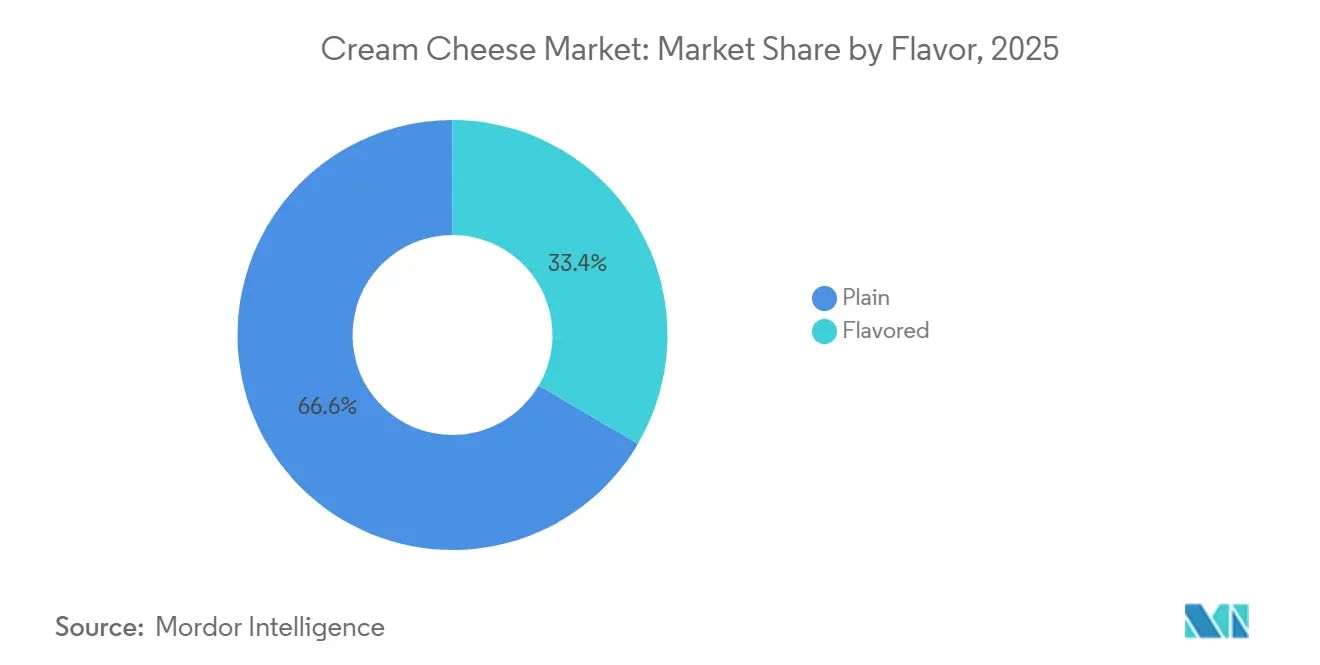

- By flavor, Plain accounted for 66.56% share in 2025, while Flavored is projected to advance at a 7.09% CAGR through 2031.

- By distribution channel, Retail captured 56.87% share in 2025, while Commercial is forecast to grow at a 6.87% CAGR through 2031.

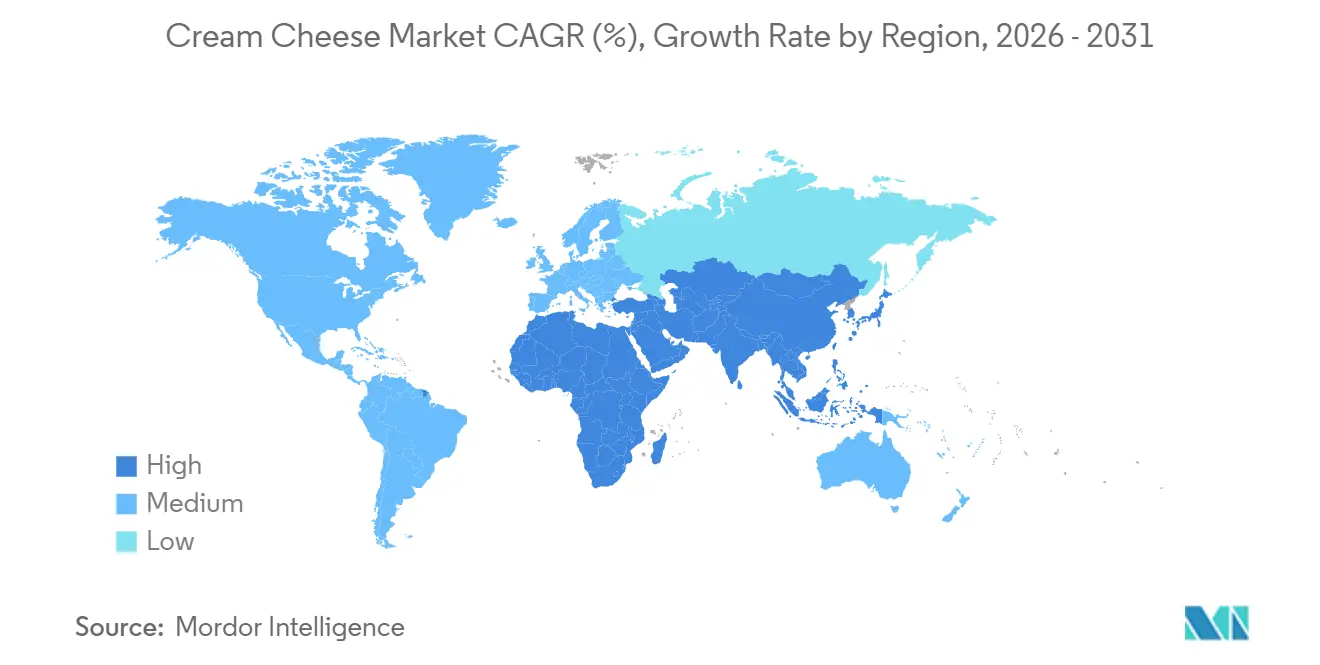

- By geography, North America held 33.21% of the cream cheese market share in 2025, while Asia-Pacific is projected to grow at a 7.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cream Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for clean-label and natural dairy products | +1.3% | Global; highest intensity in North America and Western Europe | Medium term (2–4 years) |

| Growth of Western-style fast food and café culture globally | +1.2% | Asia-Pacific core; spill-over to Middle-East and Africa and South America | Long term (≥ 4 years) |

| Increasing innovation in flavored and specialty cream cheese variants | +0.9% | Global; led by North America and Europe with Asia-Pacific adoption | Medium term (2–4 years) |

| Growth in demand for low-fat, lactose-free, and plant-based alternatives | +0.8% | North America and Europe; expanding to Asia-Pacific | Short to medium term (≤ 4 years) |

| Consumer preference for high-protein and dairy-based foods | +0.7% | North America and Europe; early-stage in Asia-Pacific | Short term (≤ 2 years) |

| Rising popularity of premium and artisanal cheese products | +0.6% | Europe, North America, and urban Asia-Pacific | Medium to long term (2–5 years) |

| Source: Mordor Intelligence | |||

Increasing demand for clean-label and natural dairy products

The rising demand for clean-label and natural dairy products is a significant driver of the global cream cheese market. Consumers are increasingly prioritizing transparency, minimal processing, and recognizable ingredients in their food choices. They seek dairy products that are fresh, authentic, preservative-free, and made with simple ingredient compositions. This shift is prompting manufacturers to reformulate cream cheese products with cleaner labels and a more natural positioning. According to the International Food Information Council (IFIC), around 36% of Americans prefer foods labeled as natural, organic, or healthy, highlighting the growing trend toward wellness-focused purchasing behavior [1]Source: International Food Information Council (IFIC), "2024 IFIC Food & Health SURVEY", ific.org. In response, cream cheese producers are introducing products made with natural cultures, hormone-free milk, reduced additives, and organic dairy ingredients to enhance consumer trust and premium appeal.

Growth of Western-style fast food and café culture globally

The global growth of Western-style fast food and café culture is significantly driving the demand for cream cheese, as it has become a key ingredient in modern quick-service dining, premium café offerings, and convenience-focused food trends. The expansion of cafés, bakery chains, quick-service restaurants, and casual dining establishments has led to increased use of cream cheese in food formats that highlight creamy textures, indulgent flavors, and premium dairy experiences. Younger demographics, in particular, are adopting Western-inspired eating habits and café-based social dining, fueling the demand for dairy-rich products associated with comfort, convenience, and premium quality. In response, manufacturers are developing cream cheese products with improved texture stability, spreadability, and flavor consistency to meet the requirements of commercial food preparation environments.

Increasing innovation in flavored and specialty cream cheese variants

Innovation in flavored and specialty cream cheese variants is a significant driver for the global cream cheese market. Manufacturers are increasingly focusing on premiumization, flavor diversification, and evolving consumer preferences for experiential dairy consumption. Consumers are seeking unique, indulgent, and globally inspired flavor profiles, prompting producers to expand beyond traditional plain cream cheese to include herb-infused, spicy, savory, and regionally inspired varieties. This focus on flavor innovation helps manufacturers differentiate their products, attract younger consumers, and encourage repeat purchases through limited-edition launches and premium product positioning. For example, in July 2024, Puck introduced its first limited-time flavor, Puck Zaatar Cream Cheese, in a modern 450 g packaging format. This launch highlights the industry's growing emphasis on localized flavors, innovative packaging, and culturally relevant taste profiles aimed at enhancing consumer engagement.

Growth in demand for low-fat, lactose-free, and plant-based cream cheese alternatives

The growing demand for low-fat, lactose-free, and plant-based cream cheese alternatives is driving the development of the global cream cheese market. Consumers are increasingly focusing on health-conscious, digestive-friendly, and lifestyle-oriented food options. Greater awareness of lactose intolerance, dairy sensitivities, calorie control, and wellness-focused nutrition is prompting a shift toward cream cheese products with improved nutritional profiles, without sacrificing taste or texture. In response, manufacturers are expanding their offerings to include reduced-fat, lactose-free, and plant-based cream cheese products with enhanced creaminess, better spreadability, and improved sensory attributes. Advances in ingredient technologies, fermentation processes, and plant-based fat structuring are enabling the creation of alternatives that closely mimic the texture and mouthfeel of traditional dairy cream cheese.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life and refrigeration dependency | -1.1% | Global; highest structural impact in South America and Middle-East and Africa | Long term (≥ 4 years) |

| Stringent food safety and dairy processing regulations | -0.8% | North America, Europe, and developed Asia-Pacific (Australia, Japan, South Korea) | Medium to long term (2+ years) |

| Intense competition from alternative spreads and dairy products | -0.9% | North America, Western Europe, and urban Asia-Pacific | Short to medium term (≤ 4 years) |

| Volatility in raw milk supply and dairy ingredient quality | -0.7% | Global; most acute in import-dependent South Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Short shelf life and refrigeration dependency

Short shelf life and refrigeration dependency are key challenges for the global cream cheese market. Cream cheese products are highly perishable, requiring consistent cold-chain management across production, transportation, storage, and retail distribution. The high moisture content and dairy-based composition make cream cheese particularly susceptible to spoilage, texture degradation, and microbial contamination when exposed to temperature fluctuations. These factors pose significant logistical and operational difficulties for manufacturers, distributors, and retailers, especially in regions with inadequate refrigeration infrastructure or unreliable cold-chain systems. Ensuring optimal storage temperatures increases transportation complexity, warehousing demands, and energy consumption, thereby impacting operational efficiency and product handling.

Stringent food safety and dairy processing regulations

Stringent food safety and dairy processing regulations present a significant restraint for the global cream cheese market. Manufacturers are required to adhere to rigorous standards concerning dairy sourcing, pasteurization, microbial safety, labeling, storage, and production hygiene. As a highly perishable dairy product with high moisture content, cream cheese is particularly vulnerable to bacterial contamination and spoilage, necessitating strict regulatory oversight across global markets. Regulatory authorities enforce comprehensive compliance requirements, including temperature control, sanitation practices, ingredient traceability, shelf-life validation, and quality assurance systems, to ensure consumer safety and product consistency. These regulations increase operational complexity for manufacturers, necessitating continuous investments in advanced processing equipment, quality-control laboratories, cold-chain systems, and food safety certifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Fat Anchors Volume While Health Variants Drive Incremental Growth

Full-Fat Cream Cheese accounted for 48.52% of the global cream cheese market in 2025, driven by its superior texture, rich mouthfeel, creamy consistency, and authentic dairy flavor. These attributes align closely with evolving consumer taste preferences. Manufacturers are increasingly focusing on full-fat formulations as consumers associate higher fat content with premium quality, indulgence, freshness, and enhanced sensory performance. This segment benefits from the rising demand for minimally processed dairy products, as full-fat variants are often perceived as more natural and less altered compared to reduced-fat alternatives, which may require stabilizers, gums, or texture-enhancing additives. This perception supports purchasing behavior among consumers seeking clean-label and traditional dairy experiences.

Low-Fat and Fat-Free Cream Cheese variants are projected to grow at a CAGR of 6.71% through 2031, driven by the global shift toward health-conscious and calorie-aware dietary preferences. Increasing awareness of obesity management, cardiovascular health, cholesterol reduction, and balanced nutrition is prompting consumers to choose dairy products with reduced fat content while maintaining familiar taste and texture. Manufacturers are advancing this segment through innovations in formulation technologies that enhance creaminess, spreadability, and mouthfeel in low-fat products, addressing traditional concerns about texture and taste compromises.

By Source: Dairy Retains Structural Dominance, Dairy-Free Commands Highest Growth Momentum

The Dairy segment's projected 87.21% market share in 2025 highlights the strong integration of dairy cream cheese into global consumer preferences, manufacturing processes, and traditional dairy consumption patterns. Dairy-based cream cheese maintains its dominance due to its authentic flavor, naturally rich texture, smooth mouthfeel, and functional properties that are challenging to replicate with alternative formulations. Consumers associate dairy cream cheese with attributes such as freshness, indulgence, quality, and traditional culinary experiences, ensuring its continued acceptance in everyday consumption. Manufacturers are advancing this segment through innovations in milk processing, culturing techniques, texture optimization, and product stabilization technologies. These advancements enhance consistency, creaminess, and shelf life while preserving the sensory characteristics expected from dairy products.

The Dairy-Free sub-segment's forecasted CAGR of 7.89% through 2031 reflects the growing shift in consumer dietary preferences toward plant-based, allergen-friendly, and wellness-focused food options. Increasing awareness of lactose intolerance, dairy sensitivities, digestive health, and ethical food consumption is driving demand for non-dairy cream cheese alternatives. Manufacturers are fostering growth in this segment through innovations in plant-based ingredient technologies, utilizing almonds, cashews, oats, soy, coconut, and blended plant proteins to replicate the creamy texture, spreadability, and flavor traditionally associated with dairy cream cheese. Advances in formulation science are addressing earlier challenges related to taste, consistency, and mouthfeel, making dairy-free cream cheese products increasingly competitive with conventional options.

By Flavor: Plain Retains Utility Dominance as Flavored Redefines the Category's Value Ceiling

Plain cream cheese is projected to hold a 66.56% market share in 2025, underscoring its position as the most preferred and widely accepted flavor format in the global cream cheese market. This segment maintains its leadership due to its versatile flavor profile, neutral taste, and compatibility with diverse consumer preferences. Consumers favor plain cream cheese for its authentic creamy dairy experience, free from overpowering flavors, making it suitable for both traditional and modern consumption patterns. Manufacturers contribute to the segment's dominance by enhancing texture smoothness, creaminess, freshness retention, and sensory consistency, ensuring consistent product quality and fostering repeat purchases. The simplicity and familiarity of plain cream cheese further enhance its appeal, particularly among consumers seeking classic dairy products with minimal flavor complexity.

The flavored cream cheese segment is expected to grow at a CAGR of 7.09% through 2031, driven by increasing consumer demand for differentiated and indulgent dairy products. Consumers are seeking unique taste experiences, premium sensory appeal, and greater variety in their food choices, prompting manufacturers to expand their flavored cream cheese offerings. This segment benefits from ongoing innovation in flavor development, including herb-infused, garlic, spicy, smoked, honey-based, fruit-inspired, and dessert-style variants that cater to evolving consumer tastes and lifestyle changes. Manufacturers are utilizing flavor diversification as a strategy to enhance product differentiation, strengthen brand identity, and drive higher purchase frequency among consumers seeking novelty and premium options.

By Distribution Channel: Retail Anchors Volume, Commercial Outpaces on Structural Foodservice Growth

In 2025, the retail channel accounted for 56.87% of the market share, underscoring its role as the primary access point for cream cheese products globally. This segment maintains its leadership due to factors such as widespread availability, strong product visibility, and high consumer purchasing frequency. Consumers prefer retail outlets for cream cheese purchases because these channels provide broad product assortments, convenient access, various packaging formats, and opportunities for easy product comparison. Manufacturers are actively supporting the retail segment by enhancing shelf presence, optimizing in-store merchandising strategies, and introducing new product varieties to align with evolving consumer preferences. The dominance of retail channels is further bolstered by the growing availability of premium, flavored, low-fat, lactose-free, organic, and plant-based cream cheese products in mainstream stores, offering consumers a diverse range of options within a single shopping environment.

The commercial channel, encompassing hotels, bakeries, cafés, and full-service restaurants, is projected to grow at a CAGR of 6.87% through 2031. This growth is supported by the rapid expansion of global foodservice activities, the rise of premium dining trends, and increasing demand for high-quality dairy ingredients in professional culinary settings. According to the United States Department of Agriculture (USDA), food sales at foodservice outlets reached approximately USD 1.52 trillion in 2024, reflecting the robust growth of the commercial food industry and its rising use of dairy-based ingredients like cream cheese [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov. The segment's growth is further driven by the integration of cream cheese into premium menu innovations, gourmet bakery products, artisanal desserts, and customized dining experiences that emphasize rich textures and indulgent flavors.

Geography Analysis

North America held a dominant 33.21% share of the global cream cheese market in 2025, supported by its well-established dairy industry, mature cold-chain infrastructure, and strong consumer preference for creamy dairy-based products. The region benefits from advanced milk processing capabilities, robust dairy farming systems, and the widespread availability of high-quality cream cheese across retail and commercial channels. Cream cheese consumption remains structurally strong due to the region's familiarity with dairy-rich diets and its integration into everyday food consumption patterns. Additionally, North America maintains a competitive advantage as cream cheese production primarily relies on cow’s milk and cream, both of which are abundantly available through the region’s large-scale dairy production ecosystem.

Asia-Pacific is projected to achieve a forecast CAGR of 7.59% through 2031, making it the most dynamic region in the global cream cheese market. This growth is driven by the modernization of dairy consumption habits, the expansion of foodservice industries, and the increasing acceptance of Western-style dairy products. The region is witnessing significant growth in dairy processing capabilities and milk production, creating a favorable supply environment for cream cheese manufacturers. According to the Ministry of Fisheries, Animal Husbandry & Dairying, milk production in India reached over 239.3 million metric tons in fiscal year 2024, up from 230.5 million metric tons in the previous year, underscoring the rapid expansion of the regional dairy sector [3]Source: Ministry of Fisheries, Animal Husbandry & Dairying, " Volume of milk production in India", minfahd.gov.in. The growing availability of cow’s milk and cream is enabling increased local production of cream cheese and strengthening regional supply chains.

Europe continues to hold a strong position in the global cream cheese market due to its long-standing dairy traditions, advanced cheese manufacturing expertise, and strong consumer preference for premium dairy products. The region benefits from highly developed dairy farming systems, strict quality standards, and growing demand for artisanal and clean-label cream cheese varieties. The Middle East and South America are emerging as steadily growing regions in the cream cheese market, supported by improving dairy processing infrastructure, expanding organized retail sectors, and rising consumer demand for premium dairy-based foods. Manufacturers in these regions are increasingly investing in product diversification, refrigeration networks, and premium dairy innovations to enhance long-term market penetration and consumer engagement.

Competitive Landscape

The global cream cheese market is moderately consolidated, featuring a mix of multinational dairy corporations, established cheese manufacturers, and emerging specialty dairy brands competing across retail and commercial channels. Key players in the market include The Kraft Heinz Company, Arla Foods amba, Schreiber Foods Inc., Fonterra Co-operative Group, and Bel Group. These companies maintain strong market positions through extensive dairy sourcing capabilities, established cold-chain distribution systems, broad product portfolios, and strong brand recognition. Competitive intensity is rising as companies expand their product offerings across categories such as full-fat, low-fat, flavored, organic, lactose-free, and plant-based cream cheese to meet evolving consumer preferences and diversify revenue streams.

Companies are prioritizing innovation strategies to enhance market differentiation and improve consumer engagement. Manufacturers are introducing new flavor profiles, premium formulations, clean-label products, and health-oriented cream cheese variants with improved nutritional attributes. Product innovation efforts are increasingly focused on texture enhancement, creaminess optimization, shelf-life improvement, and formulation stability to cater to both retail and foodservice requirements. Additionally, significant investments are being made in plant-based and dairy-free cream cheese alternatives, leveraging advancements in ingredient technology and fermentation systems to enhance sensory quality and product performance. Premiumization remains a key strategy, with manufacturers expanding artisanal, cultured, organic, and minimally processed cream cheese offerings to appeal to consumers seeking authentic and indulgent dairy experiences.

Technological advancements are significantly influencing competition within the cream cheese market. Companies are adopting advanced dairy processing systems, automated production technologies, precision fermentation techniques, and improved refrigeration infrastructure to enhance operational efficiency and product consistency. Investments in packaging innovation, cold-chain logistics, and freshness-preservation technologies are enabling manufacturers to improve shelf stability, reduce spoilage risks, and strengthen supply chain performance. Furthermore, producers are utilizing data-driven consumer insights, digital marketing strategies, and product personalization approaches to enhance market responsiveness and build brand loyalty.

Cream Cheese Industry Leaders

-

The Kraft Heinz Company

-

Arla Foods amba

-

Schreiber Foods Inc.

-

Fonterra Co-operative Group

-

Bel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kite Hill launched a first-of-its-kind dairy-free protein product, offering 4g of protein per 2-tablespoon serving, with 0g sugar and 0g saturated fat.

- May 2025: Daiya introduced its first dairy-free cream cheese in convenient 1oz packets, designed specifically for foodservice operators. The product is free from top allergens, dairy-free, vegan, Halal, Kosher-Pareve, and Non-GMO Project Verified.

- April 2025: Masaka Farms launched its cream cheese in Kigali, designed for use in spreads, dips, and baking. The product is sourced from over 2,000 local Rwandan farmers, reflecting the company's commitment to community impact.

Global Cream Cheese Market Report Scope

Cream cheese is a soft, smooth, unripened cheese made from a blend of milk and cream. The cream cheese market is segmented by product type, source, flavor, distribution channel, and geography. Based on product type, the market is segmented into low-fat and fat-free cream cheese, full-fat cream cheese, whipped cream cheese, and cream cheese blend. Based on source, the market is segmented into dairy and dairy-free. Based on flavor, the market is segmented into plain and flavored. Based on distribution channel, the market is segmented into industrial (food processing), commercial, and retail. The commercial segment is further segmented into hotels and catering, restaurants, full-service restaurants, bakeries, cafes, and other restaurants. The retail segment is further segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other retail channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Low-Fat and Fat-Free Cream Cheese |

| Full-Fat Cream Cheese |

| Whipped Cream Cheese |

| Cream Cheese Blend |

| Dairy |

| Dairy-Free (Vegan & Lactose-Free) |

| Plain |

| Flavored |

| Industrial (Food Processing) | |

| Commercial | Hotels and Catering |

| Restaurants | |

| Full-Service Restaurants | |

| Bakeries | |

| Cafes | |

| Other Restaurants | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Low-Fat and Fat-Free Cream Cheese | |

| Full-Fat Cream Cheese | ||

| Whipped Cream Cheese | ||

| Cream Cheese Blend | ||

| By Source | Dairy | |

| Dairy-Free (Vegan & Lactose-Free) | ||

| By Flavor | Plain | |

| Flavored | ||

| By Distribution Channel | Industrial (Food Processing) | |

| Commercial | Hotels and Catering | |

| Restaurants | ||

| Full-Service Restaurants | ||

| Bakeries | ||

| Cafes | ||

| Other Restaurants | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving cream cheese demand from 2026 to 2031

Growth is being supported by clean-label appeal, functional nutrition demand, and wider use in cafés, bakeries, and QSR menus. The category is projected to grow from USD 28.1 billion in 2026 to USD 38.7 billion by 2031 at a 6.6% CAGR.

Which product type leads current sales

Full-Fat Cream Cheese was the largest product segment with a 48.5% share in 2025 because it remains deeply integrated into baking, cooking, and foodservice applications.

Which segment is growing the fastest by source

Dairy-Free is the fastest-growing source segment with a projected 7.9% CAGR through 2031, supported by lactose-intolerant consumers and stronger plant-based formulations.

Why is Asia-Pacific expanding faster than other regions

Asia-Pacific is projected to grow at 7.6% CAGR through 2031 because café culture, QSR menu expansion, bakery demand, and localized beverage and dessert formats are increasing category use.

Page last updated on: