Goat Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.64 Billion |

| Market Size (2031) | USD 11.16 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

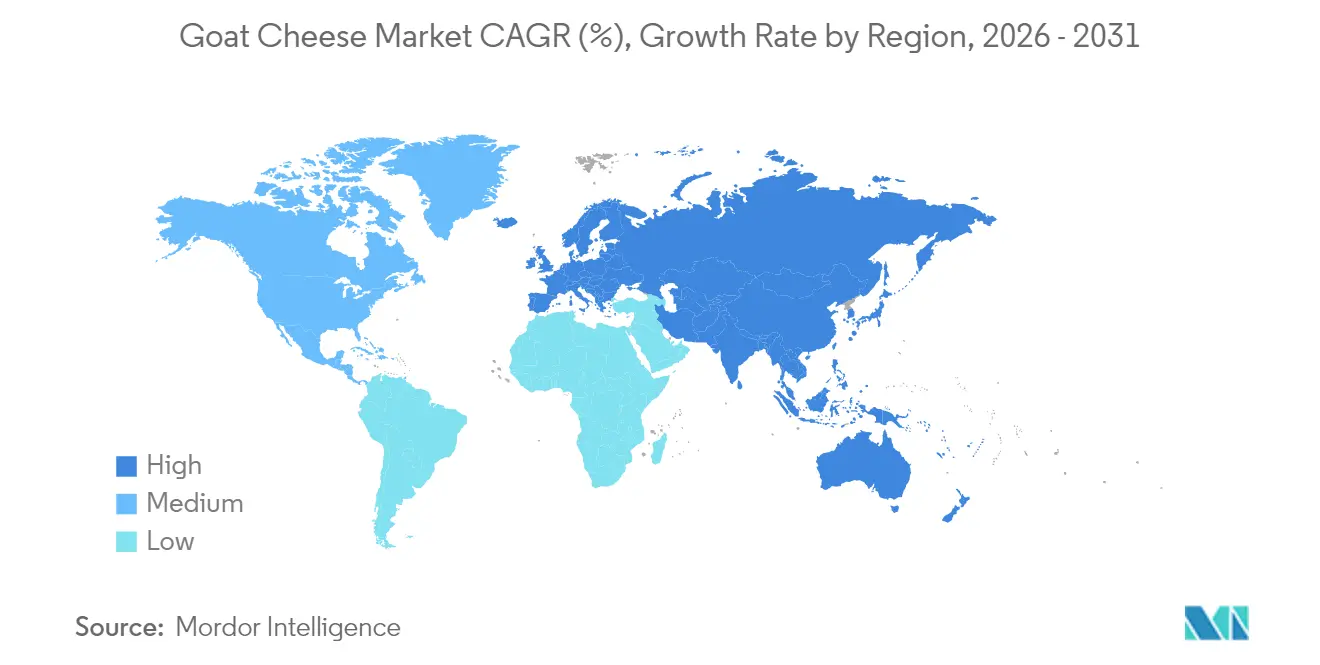

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

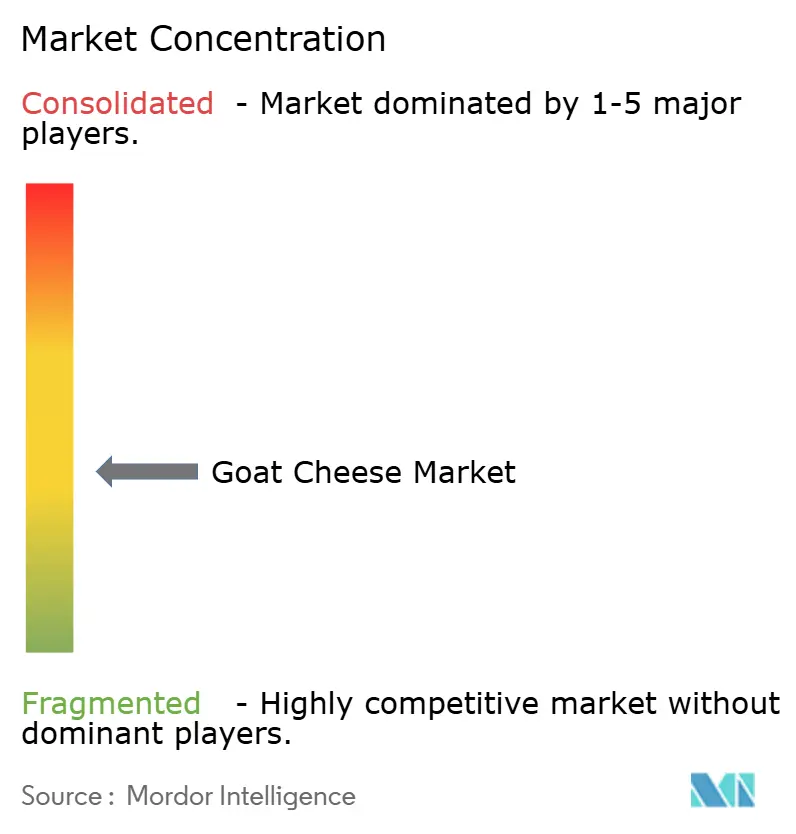

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Goat Cheese Market Analysis by Mordor Intelligence

The goat cheese market size in 2026 is estimated at USD 8.64 billion, growing from 2025 value of USD 8.21 billion with 2031 projections showing USD 11.16 billion, growing at 5.25% CAGR over 2026-2031. The market expansion is attributed to heightened consumer health consciousness. Goat cheese's reduced lactose content and enhanced digestibility compared to traditional cow's milk cheese create market opportunities among lactose-intolerant consumers and those seeking dairy alternatives. The market benefits from increased demand for premium and artisanal dairy products, reflecting consumers' evolving preferences for distinct flavors. Enhanced accessibility through e-commerce platforms and specialty food stores, combined with urbanization and busy lifestyles, has increased goat cheese consumption as a convenient food ingredient. Production technology improvements, sustainable farming practices, and enhanced packaging solutions support market development. The market also gains momentum from growing organic product preferences, an expanding foodservice industry, and increased online sales channels.

Key Report Takeaways

- By product type, chèvre led with 51.92% of goat cheese market share in 2025; mozzarella is projected to expand at an 8.34% CAGR to 2031.

- By form, logs and rolls captured 38.10% of the category in 2025; crumbles are poised for 5.78% CAGR through 2031.

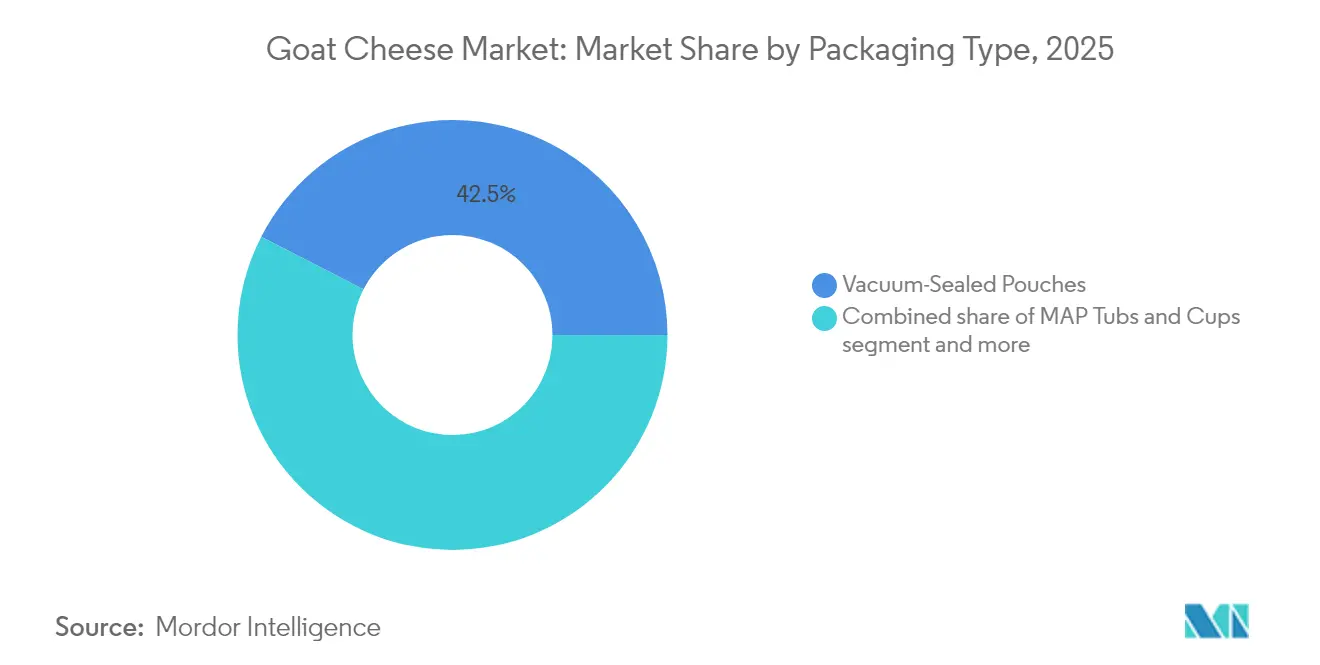

- By packaging, vacuum-sealed pouches commanded a 42.45% share in 2025; MAP tubs and cups are growing at 7.03% CAGR.

- By distribution channel, supermarkets/hypermarkets held 56.70% share in 2025; online retail is the fastest-growing at 8.28% CAGR to 2031.

- By geography, Europe dominated with 38.10% revenue share in 2025; Asia-Pacific is the fastest-growing region at 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Goat Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Popularity of lactose-friendly cheese among millennials | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising demand for artisanal and gourmet products | +0.9% | North America and Europe, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Expansion of foodservice industry | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Surge in organic and grass-fed goat cheese demand | +0.7% | North America and Europe, emerging in Australia | Long term (≥ 4 years) |

| Increased demand for ready-to-eat food products | +0.6% | Global, particularly urban centers | Short term (≤ 2 years) |

| Urbanization and changing food preferences | +0.5% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Lactose-Friendly Cheese among Millennials

The increasing consumer preference for lactose-friendly cheese among millennials significantly influences the global goat cheese market growth, driven by heightened awareness of lactose intolerance and evolving dietary preferences toward healthier options. Millennials demonstrate a strong inclination toward wellness-focused and dietary-inclusive food choices, particularly gravitating toward easily digestible cheese varieties. The inherently lower lactose content in goat cheese compared to traditional cow's milk cheese positions it as an optimal choice for consumers with lactose sensitivities. The market expansion potential is particularly pronounced in regions with considerable lactose intolerance prevalence. According to World Population Review data from 2025, 61% of India's population experiences lactose intolerance, while Canada reports 59%, and the United States records 36% of their respective populations [1]Source: World Population Review, "Lactose Intolerance by Country 2025", worldpopulationreview.com. These demographic patterns present substantial opportunities for goat cheese manufacturers to strengthen their market presence and address the expanding consumer segment seeking lactose-friendly dairy alternatives, thereby contributing to the sustained growth of the global goat cheese market.

Rising Demand for Artisanal and Gourmet Products

The global goat cheese market exhibits a substantial growth trajectory, primarily attributed to the increasing sophistication in consumer preferences for artisanal and gourmet dairy products. Market analysis demonstrates that consumers, particularly urban demographics and culinary connoisseurs, display pronounced preferences toward cheese varieties distinguished by their complex flavor profiles, traditional manufacturing methodologies, and authenticated geographical origins. This fundamental transformation in consumer behavior has compelled manufacturers to strategically develop products that emphasize traditional craftsmanship and regional heritage. For instance, in September 2024, Vermont Creamery executed a strategic product portfolio expansion through the introduction of Coupole and Bijou soft-ripened goat cheeses via premium retail establishments, including Whole Foods. These significant market developments, in conjunction with the evolving consumer preferences and increasing demand for premium dairy products, substantiate the robust growth trajectory and long-term market potential of artisanal goat cheese products in the global marketplace.

Expansion of Foodservice Industry

The foodservice industry's growth drives the global goat cheese market as restaurants, cafes, hotels, and catering services incorporate goat cheese into their menus to address evolving consumer preferences. The market expansion is attributed to increasing consumer demand for prepared food items and dining experiences, with goat cheese recognized for its versatility, distinct flavor profile, and nutritional benefits. With the rising trend of dining out and consumption of ready-to-eat meals due to busy lifestyles, foodservice operators integrate goat cheese across various menu items, including salads, pizzas, sandwiches, appetizers, and desserts. Dairy companies are strategically developing products for the foodservice segment. For instance, in May 2024, Belle Chevre Inc. launched two new goat cheese products: 1.5-oz portion cups of spreadable goat cheese in Original, Honey, and Fig flavors, and a 2.3-lb tub of flavored cheese cubes marinated in extra virgin olive oil under the CHEVOO brand. These product developments indicate the market's responsiveness to foodservice requirements and its potential for continued growth.

Surge in Organic and Grass-Fed Goat Cheese Demand

The global goat cheese market demonstrates increasing consumer demand for organic and grass-fed products, driven by sustainability awareness and clean-label preferences. Producers are modifying their production methods and obtaining certifications to support premium pricing. For example, Redwood Hill Farm sources milk from Certified Humane family farms that follow strict animal welfare and sustainable farming standards. According to Mondelēz International's 2023 State of Snacking: Future Trends report, 63% of consumers purchase snacks that minimize environmental impact through carbon offsets, local sourcing, and sustainable supply chains [2]Source: Mondelēz International, Inc., "State of Snacking: Future Trends 2023", mondelezinternational.com. This environmental consideration corresponds with the operational efficiency of goat cheese production. Goats consume 50% less water than cattle and generate reduced methane emissions, positioning goat cheese as a viable option for environmentally conscious consumers. As purchasing patterns demonstrate increased environmental considerations, goat cheese manufacturers can capitalize on this market opportunity through sustainable production methods. These sustainability advantages resonate with environmentally conscious consumers. The grass-fed segment demonstrates substantial growth, with consumers associating improved taste and nutritional value with pasture-raised production methods, indicating a sustained shift toward premium, environmentally conscious goat cheese products in the global market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile farm-gate goat milk prices globally | -0.8% | Global, particularly acute in Europe and North America | Short term (≤ 2 years) |

| High import tariffs on dairy in emerging markets | -0.6% | Emerging markets, especially India, China, Brazil | Medium term (2-4 years) |

| Shelf-life constraints for fresh goat cheese in hot climates | -0.4% | Middle East, Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Competition from plant-based cheese analogues | -0.3% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Farm-gate Goat Milk Prices globally

A significant restraint in the global goat cheese market stems from price volatility in goat milk procurement, which creates substantial margin pressure and supply chain uncertainty, particularly affecting smaller producers with limited hedging capabilities. According to Statistics Norway, the number of dairy goats in Norway decreased in 2024, with 32,374 dairy goats compared to 32,571 in 2023, exemplifying the supply constraints in major production regions. This supply-demand imbalance compels cheese manufacturers to either increase imports or reduce production volumes, disrupting established market relationships and pricing strategies. The market restraint is further intensified by goat farming's inherent seasonality and weather sensitivity, combined with limited producer scale that prevents effective risk management through forward contracting or vertical integration. As a result, artisanal producers, who represent a significant segment of the market, experience substantial operational constraints due to their limited financial resources to manage price risk through derivatives or long-term supply agreements, ultimately impacting the overall market growth potential.

High Import Tariffs on Dairy in Emerging markets

The global goat cheese market encounters a substantial challenge from the rapid expansion of plant-based cheese alternatives. This competitive pressure is most pronounced in developed markets, where consumer preferences have shifted significantly toward vegan and flexitarian dietary choices. Plant-based manufacturers have successfully enhanced their product offerings through improved texture and flavor profiles while maintaining competitive price points relative to premium goat cheese products. The implementation of advanced plant protein formulations and sophisticated fermentation technologies has enabled these manufacturers to achieve closer replication of traditional cheese characteristics. This technological progression has systematically diminished the distinctive taste and texture advantages that historically differentiated dairy cheese markets, thereby presenting a sustained impediment to the growth and market positioning of the goat cheese industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chèvre Dominance Faces Mozzarella Challenge

Chèvre cheese maintains a substantial 51.92% market share in 2025, establishing its position as the primary goat cheese product internationally. Its market leadership is attributed to extensive applications in international cuisine and foodservice sectors, supported by scalable production methodologies across manufacturing facilities worldwide. The mozzarella segment demonstrates significant expansion potential with an 8.34% CAGR through 2031, driven by international pizza chain proliferation and increasing adoption of Mediterranean cuisine across global markets. This market evolution indicates a substantial transformation in goat cheese consumption patterns beyond traditional formats.

Cheddar and ricotta segments exhibit consistent growth trajectories, capitalizing on their established presence in global culinary applications where goat milk variants offer premium alternatives. The international specialty cheese category, comprising aged and flavored varieties, presents substantial opportunities for market expansion within the cheese market through product innovation and international distribution networks. This global market diversification aligns with international dairy industry trends, where consumers across regions increasingly demand distinguished products in premium segments.

By Form: Logs and Rolls Lead Traditional Formats

Logs and rolls maintain market dominance with a 38.10% share in 2025, as these formats align with traditional goat cheese presentation methods and meet stringent portion control requirements across retail and foodservice sectors worldwide. The format's international dominance is attributed to its superior visual presentation and standardized portioning capabilities, enabling consistent pricing and display across diverse retail channels. Artisanal producers across regions prefer this format as it effectively demonstrates traditional crafting methods and premium quality positioning in the global marketplace.

Crumbles are experiencing the highest growth rate at 5.78% CAGR through 2031 in the international market, driven by increasing consumer demand for convenient, ready-to-use options in salads, pizzas, and culinary applications. Blocks and wheels formats primarily serve industrial and foodservice segments where volume efficiency and longer shelf life are prioritized over presentation. These formats demonstrate substantial growth potential in emerging markets where bulk packaging reduces costs and enables wider distribution networks. While slices and shreds constitute the smallest segment globally, they showcase significant advancement opportunities through innovative packaging technologies that preserve product quality and extend shelf life.

By Packaging Format: Innovation Drives Shelf-Life Extension

Vacuum-sealed pouches hold a 42.45% market share in 2025, driven by their ability to extend shelf life and protect against contamination, enabling wider geographic distribution. These pouches maintain product integrity during transportation and storage while offering clear product visibility for premium positioning. The format supports portion control and freshness preservation, addressing the needs of health-conscious consumers and small households. Moreover, vacuum packaging reduces preservative requirements, aligning with consumer demand for clean-label products.

MAP tubs and cups are projected to grow at 7.03% CAGR through 2031. This growth trajectory is supported by continuous advancements in barrier materials, gas composition optimization, and manufacturing processes that collectively enhance product preservation while maintaining organoleptic properties and regulatory compliance. Traditional foil-wrapped logs experience market pressure from advanced packaging alternatives offering superior barrier properties and consumer convenience features. The other category encompasses emerging packaging innovations, including bio-based materials, recyclable solutions, and integrated smart monitoring systems that enhance product safety and consumer confidence through real-time freshness indicators and environmental condition tracking.

By Distribution Channel: Digital Disruption Challenges Traditional Retail

The goat cheese market distribution is predominantly controlled by supermarkets/hypermarkets, commanding a substantial 56.70% market share in 2025. These retail establishments maintain their market leadership through sophisticated cold chain infrastructure, strategic store locations, and consistent consumer footfall patterns. Their market dominance is further strengthened by extensive product portfolios, economies of scale in procurement, and substantial investment in temperature-controlled display infrastructure. The increasing consumer preference for premium dairy products, rising health consciousness, and growing demand for artisanal cheese varieties contribute to their sustained growth.

Online retail demonstrates remarkable growth potential with an 8.28% CAGR through 2031, driven by technological advancements in cold chain logistics, improved last-mile delivery capabilities, and shifting consumer purchasing behaviors. This channel's expansion is further supported by the integration of artificial intelligence for personalized recommendations, blockchain technology for supply chain transparency, and sophisticated inventory management systems. Specialty cheese stores maintain their distinct market position through comprehensive product knowledge, curated selections, and specialized storage facilities. Convenience stores operate within the constraints of limited refrigeration infrastructure and rapid inventory turnover requirements, which inherently restrict their ability to maintain extensive goat cheese selections, despite serving immediate consumption needs.

Geography Analysis

Europe maintains a 38.10% market share in 2025, underpinned by established goat cheese production methodologies and sophisticated consumer preferences for artisanal dairy products. The region's competitive position is reinforced through stringent protected designation systems, standardized production protocols, and comprehensive distribution networks. Primary production regions, including Italy, Spain, and the Netherlands, maintain substantial output volumes while preserving distinct regional variants that generate premium market valuations through verified authenticity and geographical indications.

Asia-Pacific is growing at a 6.08% CAGR through 2031, driven by middle-class expansion and increased consumption of Western dairy products due to urbanization. China imported USD 895 million of cheese in 2024, according to The Observatory of Economic Complexity, with Tier-1 supermarkets/hypermarkets allocating more shelf space to specialty cheeses, including goat cheese . In India, the expanding middle class and higher lactose intolerance rates present opportunities for goat cheese as a dairy alternative.

North America shows consistent growth through health-conscious consumer preferences and artisanal food market expansion, particularly in the United States' specialty cheese segment. The region's developed cold chain infrastructure and retail networks support premium product distribution, while foodservice recovery increases specialty ingredient demand.

South America displays growth potential, especially in Brazil and Argentina, where European immigration has established cheese consumption patterns, though economic and currency instability affect market predictability. The Middle East and Africa represent developing markets where climate challenges necessitate advanced packaging, while expatriate communities and tourism create demand for premium imports.

Value Chain Analysis

The goat cheese value chain is shaped by branded processors and distributors such as Lactalis, Saputo, Land O'Lakes, Savencia, and Laura Chenel's Chèvre, Inc., with Vermont Creamery used as an example of an artisan network. In April 2026, Lactalis completed the acquisition of the consumer cheese business of Fonterra, extending its global processing footprint and supply capacity in Oceania and Asia.

Vermont Creamery operates through a network of more than 20 family farms, which helps branded players stabilize milk sourcing and reinforce product storytelling. Saputo converted a U.S. mozzarella facility in Reedsburg, Wisconsin into a dedicated goat cheese plant, reflecting a shift in capacity toward specialty cheese. Downstream, supermarkets and online retail depend on refrigerated logistics and protective packaging to maintain freshness and support multi-channel distribution.

Competitive Landscape

The global goat cheese market demonstrates moderate fragmentation, characterized by intense competition between established dairy conglomerates and specialized artisanal producers. Market competitiveness is driven by increasing consumer demand for specialty dairy products and growing health consciousness. Key market players include Lactalis Group, Saputo Inc., Land O’Lakes Inc., Laura Chenel's Chèvre, Inc., and Savencia Fromage & Dairy, which maintain their positions through extensive distribution networks and product diversification.

Companies are investing in advanced technology solutions to enhance their competitive advantage. The market is experiencing significant vertical integration and supply chain optimization, with companies securing goat milk supplies through strategic partnerships, long-term contracts, or direct farm ownership. These measures help manage input cost volatility, maintain quality standards, and ensure consistent supply in response to growing market demand.

Emerging markets present substantial growth opportunities due to limited local production capacity and high import dependency. The expansion potential is further supported by rising disposable incomes, changing dietary preferences, and increasing awareness of goat cheese products. Technological advancements in packaging solutions have addressed traditional shelf-life constraints, enabling companies to expand their geographical presence and market reach.

Goat Cheese Industry Leaders

-

Lactalis Group

-

Saputo Inc.

-

Land O’Lakes Inc.

-

Savencia Fromage & Dairy

-

Laura Chenel's Chèvre, Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunities are anchored in demand for protein-forward and premium goat cheeses. Lactalis UK & Ireland's 2026 Cheese Outlook points to high-protein cheese and enriched dairy as growth themes, which encourages goat cheese makers to highlight protein and wellness positioning while maintaining artisanal differentiation.

Asia-Pacific demand is supported by expanding modern retail and specialty cheese shelf space, and China importing USD 895 million of cheese in 2024 indicates room for differentiated goat cheese offerings where local production is limited. On the supply side, Savencia Fromage & Dairy signed a purchase agreement to acquire Quata Alimentos in Brazil in December 2025, strengthening regional manufacturing and distribution. Land O Lakes also announced a July 2026 investment at its Tulare, California facility to expand high-value dairy protein production and ultra-filtered milk, reinforcing the inputs used to build premium cheese portfolios.

Recent Industry Developments

- July 2026: Lactalis Group reached an agreement to acquire the fine cheese division of Agropur in Canada. The deal alters premium dairy supply dynamics in North America and expands Lactalis's premium cheese portfolio through vertical integration, improving its control over high-value cheese categories.

- March 2026: Savencia Fromage & Dairy published 2025 annual accounts describing structural integration of Ugalait and a merger with Savencia Gourmet to accelerate Premium Foodservice development. This supports expansion into premium foodservice channels and speeds go-to-market in high-value cheese segments.

- December 2025: Savencia Fromage & Dairy signed a purchase agreement to acquire Brazilian cheese and dairy manufacturer Quata Alimentos. The acquisition is designed to expand geographic footprint in Brazil and diversify its dairy product portfolio.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of goat cheese sold for human consumption across retail and foodservice channels, counted in USD at the level where the product is first sold into the market.

Scope exclusions: We exclude non-cheese goat dairy (milk, yogurt, infant formula ingredients), plant-based cheese alternatives, and homemade or informal sales that are not captured in trade and retail reporting.

Segmentation Overview

-

By Type

- Mozzarella Cheese

- Chèvre Cheese

- Cheddar Cheese

- Ricotta Cheese

- Others

-

By Form

- Crumbles

- Logs and Rolls

- Blocks/Wheels

- Slices and Shreds

-

By Packaging Format

- Vacuum-Sealed Pouches

- MAP Tubs and Cups

- Foil-Wrapped Logs

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Cheese Stores

- Online Retail

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the real demand pool and trade flows, and then turning that into a consistent value model. We relied on public agriculture and food statistics and trade databases, such as FAOSTAT, UN Comtrade, Eurostat, and USDA datasets, to understand milk output signals, cheese trade direction, and country level consumption context.

To keep assumptions grounded, we also reviewed labeling and food safety guidance, such as Codex Alimentarius texts and national food regulator publications, and then paired these with company annual reports, investor presentations, and credible press coverage for channel mix and pricing cues. Select paid subscriptions for company financials and news, along with an import-export shipment level database and a patent database, were used to validate corporate activity and product momentum without overfitting the model. This list is illustrative only, and many other sources were checked for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on pricing, channel splits, and what is actually sold as goat cheese in each region. We spoke with a mix of producers, distributors, retailers, foodservice buyers, and category specialists across major consuming markets, and then used the inputs to reconcile gaps where public data is thin.

We also revisited a few experts when numbers did not line up, since small changes in format mix (fresh versus aged) and packaging choice can shift the value outcome materially.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 48% |

| Mid tier: 57% | Functional/Unit leaders: 31% | EMEA: 31% |

| Smaller Players: 14% | Managers: 57% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production and trade indicators are used to reconstruct apparent consumption, which is then filtered through goat-cheese penetration and channel mix to arrive at value. The model uses a small set of repeatable inputs, such as goat milk availability signals, cheese import-export values and unit prices, share of fresh versus aged formats, on-trade versus off-trade splits, and typical retail price bands by major geography.

Those totals are then cross-checked with selective bottom-up approximations, like sampled country volumes multiplied by observed average selling prices, and distributor and retailer channel checks shared in interviews. Where data gaps exist for smaller countries, proxy ratios are applied from similar markets based on income level, dairy consumption patterns, and trade dependence, and then adjusted back to match regional control totals.

For forecasting, we used scenario analysis supported by short time-series smoothing on key drivers, followed by expert validation on how quickly premiumization and foodservice recovery are expected to translate into volume and price. The final outlook is kept practical, since the market is also shaped by supply seasonality in goat milk and by how fast cold chain and specialty retail expand in emerging cities.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as trade value trends, observable retail shelf pricing, and shifts in on-trade activity, before the numbers are finalized. If a country shows a sharp step change that is not supported by these signals, the assumptions are reworked and a small set of experts are re-contacted to confirm whether the change is real or model-driven.

A second analyst review is completed to look for variance issues across regions and to confirm that the logic is consistent across the time series. Reports are refreshed annually, and interim updates are made when material events occur that can move prices, availability, or demand. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Global Goat Cheese Market Size Compared With Other Published Estimates

Published market sizes for goat cheese can look far apart, even when they appear to cover the same product, because the scope and pricing basis are not always aligned. Differences usually come from what gets counted as goat cheese, the year used for pricing, and how on-trade sales are valued.

Some public figures fold in broader goat dairy value or add adjacent cheese categories when the milk source is mixed or unspecified. In Mordor Intelligence, goat cheese is counted only when it is a defined cheese product made from goat milk and sold through on-trade and off-trade channels, and then valued using a consistent USD conversion and the stated study years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.64 B (2026) | |

| Trade Journal A | USD 4.10 B (2024) | Uses an earlier base year and a narrower tracked set of products that can undercount specialty formats, and it may apply retail value assumptions unevenly across regions. |

| Regional Consultancy B | USD 6.50 B (2025) | Likely relies more on manufacturer-reported revenue and limited channel coverage, which can miss parts of foodservice and cross-border trade effects in high-import markets. |

The spread across the three values is mainly explained by year selection, channel valuation, and how strictly the product is defined as goat cheese. By keeping the inputs tied to trade signals, channel splits, and observed price behavior, the estimate stays traceable to a repeatable set of steps that can be rechecked as new data appears.

Key Questions Answered in the Report

What is the current size of the goat cheese market?

The goat cheese market is worth USD 8.64 billion in 2026 and is projected to reach USD 11.16 billion by 2031.

Which region leads goat cheese sales?

Europe holds the leading 38.10% share, supported by its long-standing cheese heritage and protected designation systems.

Which goat cheese type is growing the fastest?

Goat mozzarella cheese is forecast to expand at an 8.34% CAGR through 2031 as global pizza consumption rises.

Why is online retail important for goat cheese?

Online platforms offer detailed product stories and convenient delivery, helping the channel grow at 8.28% CAGR faster than any brick-and-mortar alternative.

Page last updated on: